STIR: NFP Reaction Holds, Claims In Brief Focus Before CPI Tomorrow

Feb-12 11:35

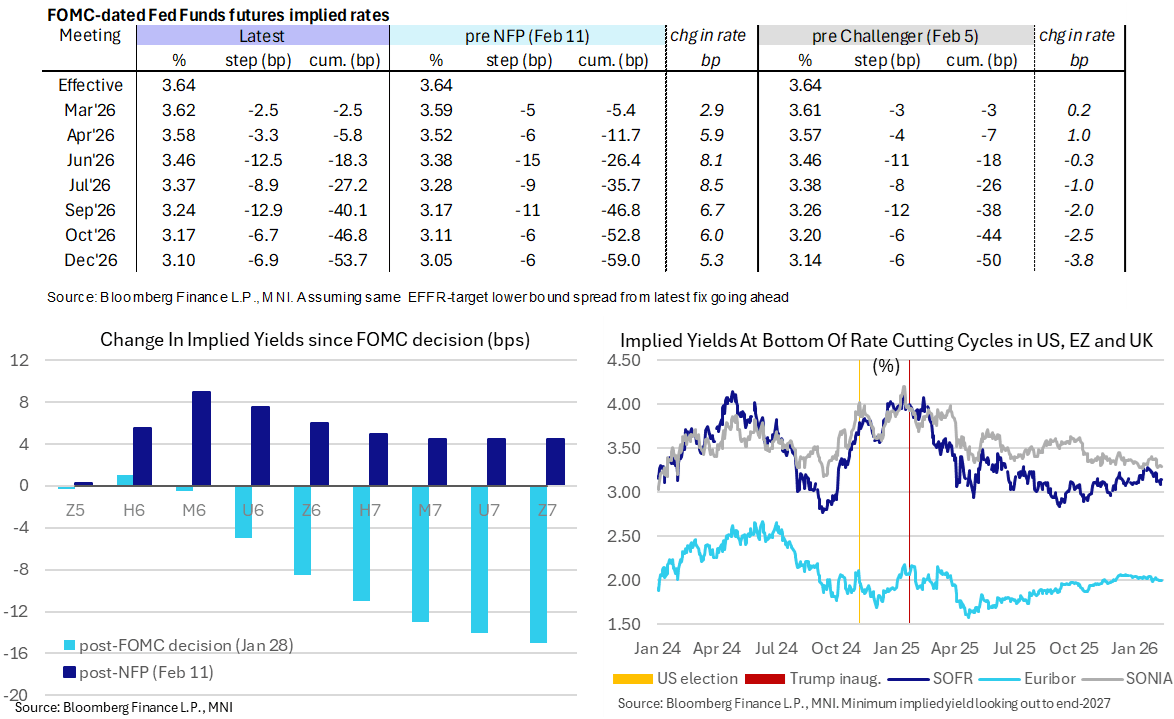

- Fed Funds implied rates still hold yesterday’s front-loaded hawkish reaction to payrolls, with today’s data focus on jobless claims as a minor stepping stone before tomorrow’s CPI release (MNI CPI Preview https://mni.marketnews.com/3OayQs6)

- Initial jobless claims were much higher than expected last week but were potentially boosted by extreme winter weather across much of the country in the last weeks of the month. They also appear to continue to see residual seasonality that could bias the trend higher heading into February.

- Cumulative cuts from 3.64% effective: 2.5bp Mar, 6bp Apr, 18.5bp Jun, 27bp Jul, 40bp Sep, 47bp Oct and 53.5bp Dec.

- SOFR futures are broadly unchanged on the day, with the terminal implied yield of 3.145% (H7) +5bp since NFPs. Still, it holds towards the lower end of the ytd range of 3.09-3.285% for closes.

- Today’s scheduled Fedspeak comes late on and we imagine won’t move the needle.

- 1900ET – Dallas Fed’s Logan (’26 voter, hawk) opening remarks. The nature of remarks should heavily limit any notable comments and she earlier this week said she needs to see “material” weakness in the labor market to support cuts.

- 1905ET – Gov. Miran (voter, dove) in moderated conversation at the Dallas Fed. He said briefly after yesterday’s NFP report that there are still a variety of reasons to lower rates, with a number of factors pushing supply side growth in the US.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Cross/JPY Extending Surge Higher as Domestic Politics Weighs

Jan-13 11:35

- Ongoing concerns surrounding the domestic political backdrop in Japan has further weighed on the Japanese currency Tuesday, while the strong rebound for the major equity benchmarks on Monday has continued to provide a supportive tone for cross/JPY.

- US treasuries are also approaching some pivotal levels, which could provide further headwinds for the Yen should the 10-year yield break meaningfully above 4.20. A test of the BOJ/MOF resolve currently looks inevitable and any move for USDJPY above 160.00 would dramatically increase the chances of the MOF getting involved. Until then, the path of least resistance remains higher for Cross/JPY.

- We have highlighted that GBPJPY has extended its sharp upswing, which gathered momentum on a break of 208.00 in December and now places the cross at the highest level since mid-2008. Today’s price action has taken spot to a fresh cycle high of 214.30 this morning, an impressive 400 pip rally from last week’s test of 20-day EMA support

- A key medium-term target is at 215.88, the July 2008 high, while above here, 219.45 is another notable level, the 76.4% retracement of the 2007-2011 range.

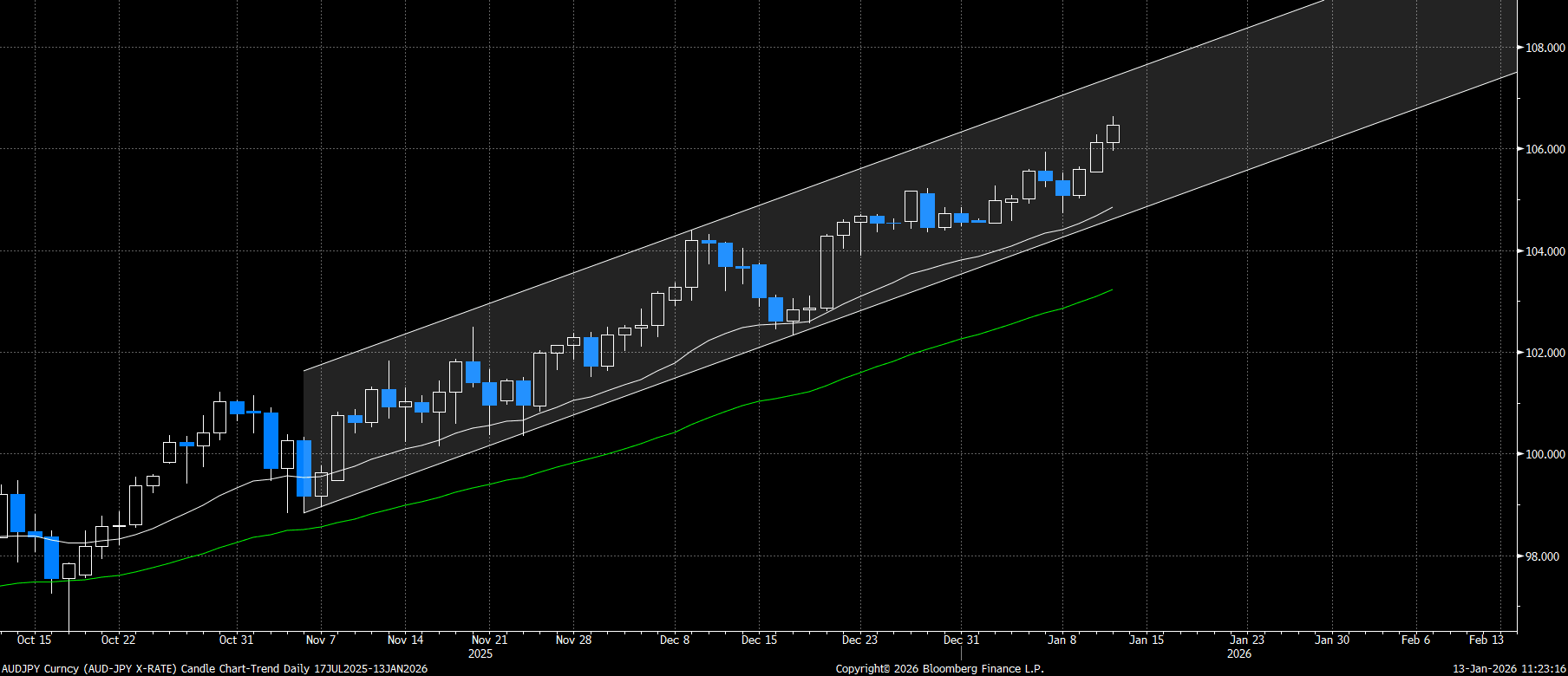

- Both AUDJPY and MXNJPY charts continue to standout as well, extending their recoveries from last year’s lows to around 24% and 30% respectively, and eroding solid portions of the global carry unwind induced selloffs in 2024.

- For AUDJPY, next resistance comes in at 107.41 - top of a bull channel drawn from the Nov 6 ' 25 low (shown below). Key resistance remains at 109.37, a break of which would place the cross at its highest point since 1991.

US 10YR FUTURE TECHS: (H6) Bear Threat Remains Present

Jan-13 11:34

- RES 4: 113-00+ 61.8% retracement of the Nov 25 - Dec 10 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25+ High Dec 30 / 31

- RES 1: 112-22 High Jan 7

- PRICE: 112-02 @ 11:23 GMT Jan 13

- SUP 1: 111-29 Low Dec 10 and the bear trigger

- SUP 2: 111-19 1.236 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 3: 111-11 1.382 proj of the Oct 17 - Nov 5 - 25 price swing

- SUP 4: 111-00 Round number support

Treasuries are softer but for now remain above a key support at 111-29, the Dec 10 low. The trend set-up is bearish and a breach of 111-29 would confirm a continuation of the bear cycle. Note that a head and shoulders reversal pattern on the daily chart also highlights a bearish threat. Scope is seen for a move towards 111-19 initially, a Fibonacci projection. Key short-term resistance is unchanged at 112-31, the Dec 18 high.

LOOK AHEAD: Tuesday Data Calendar: CPI, ADP Weekly, New Home Sales, 30Y Re-Open

Jan-13 11:29

- US Data/Speaker Calendar (prior, estimate). All times ET

- 01/13 0600 NFIB Small Business Optimism reported 99.5 vs. 99.0 prior

- 01/13 0815 ADP Weekly NER Pulse

- 01/13 0830 CPI MoM (0.3 est), YoY (2.7%, 2.7%)

- 01/13 0830 Core CPI MoM (0.3% est), YoY (2.6%, 2.7%)

- 01/13 0855 Redbook Retail Sales Index

- 01/13 1000 New Home Sales (715k est), MoM (-10.6% est)

- 01/13 1000 StL Fed Musalem outlook, Q&A event hosted by MNI

- 01/13 1130 US Tsy $75B 6W bill auction

- 01/13 1300 US Tsy $22B 30Y Bond auction re-open (912810UP1)

- 01/13 1400 Treasury Budget

- 01/13 1600 Richmond Fed Tom Barkin moderated discussion

- Source: Bloomberg Finance L.P. / MNI