MNI US MARKETS ANALYSIS - AUD Slides on Soft June Jobs

Highlights:

- Markets consolidate steepening after Trump-Powell ire

- Heavy Fedspeak day headlined by Waller, one of many names in the running to replace Powell

- AUD slips against broader G10 on the back of soft June jobs data

US TSYS: Trump-Powell Headline Steepening Consolidated, Busy Session Ahead

- Treasuries have pared modest losses overnight in moves that still on balance reflect the twist steepening seen on Trump’s reported threats of firing Powell before a caveated backtracking.

- Volumes are subdued ahead of a busy docket including retail sales, import prices and initial jobless claims for a payrolls reference week plus three senior FOMC appearances.

- Cash yields are 0.5-1bp higher. 10YY are 4.4593% remained below 4.50% throughout yesterday's session, having last cleared it on Jun 11.

- 2s10s at 56.1bp (-0.7bps) vs yesterday’s high of 62.7bp and pre-Powell headline levels of 52-53bp.

- That’s echoed further out, with 5s30s at 101.9bp vs a high of 108.5bp and pre-headline levels of ~97bp.

- TYU5 has lifted recently to 110-18+ from an overnight low of 110-13 although only back to nearly unchanged on the day, on light cumulative volumes of 240k.

- Yesterday’s high of 110-21+ stopped comfortably short of testing resistance at 111-00 (20-day EMA). It has previously set a softer tone, with support watched at 110-08+ (Jul 14/15 low) after which lies an important 110-03 (76.4% retrace of May 22-Jul 1 bull leg).

- Data: Retail sales Jun (0830ET), International trade prices Jun (0830ET), Weekly jobless claims (0830ET), Philly Fed Jul (0830ET), Business inventories May (1000ET), NAHB index Jul (1000ET), TIC Flows May (1600ET)

- Fedspeak: Kugler (0915ET), Daly (1245ET), Cook (1330ET), Waller (1830ET) – see FED bullet.

- Bill issuance: US Tsy $90B 4W, $80B 8W bill auctions (1130ET)

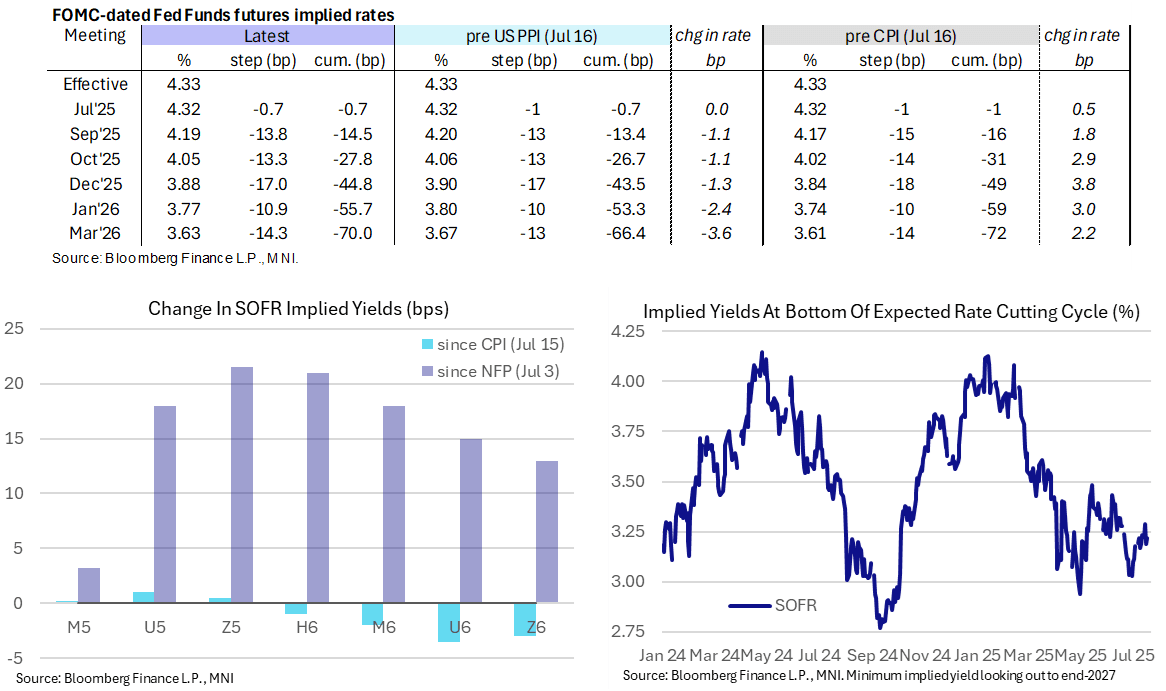

STIR: Trump-Powell Headline Impact Reversed For 2025 Rates, More Caution Beyond

- Fed Funds implied rates have pushed a little higher overnight, with 2025 meetings having reversed the slide seen on Trump-Powell headlines.

- It leaves a near-term path back close to levels seen after Wednesday’s PPI report, i.e. on net still holding a modest hawkish shift following Tuesday’s CPI report – see the below table for comparisons.

- Cumulative cuts from 4.33% effective: 0.5bp Jul, 14.5bp Sep, 28bp Oct, 45bp Dec, 55.5bp Jan and 70bp Mar.

- SOFR futures further out the curve still see some lasting impact from the latest threats to fire Powell, with SFRZ6 3 ticks lower on the day but still 2 ticks higher than pre-CBS headlines.

- The terminal yield is seen at 3.22% (SFRZ6), within the week’s range.

- NY Fed’s Williams (permanent voter) late yesterday said a restrictive Fed policy stance is entirely appropriate and allows time to analyze data - he expects tariff inflation to increase in coming months.

- See the previous FED bullet on a guide to today’s Fedspeak from Kugler, Daly, Cook and Waller.

FED: A Guide To Today’s Governor-Heavy Fedspeak

Along with a busy data docket including retail sales, import prices and jobless claims, today also sees Fedspeak from three permanent voters after Williams late yesterday. Kugler starts proceedings before an eagerly anticipated speech from Waller after the close. The increasingly dovish Waller is currently the last scheduled appearance before the FOMC media blackout starts Sat 0001ET.

- 0915ET – Gov. Kugler (permanent voter) on the housing market and economic outlook (text only). It will be a useful update after she said on Jun 5 "I view our current stance of monetary policy as well-positioned for any changes in the macroeconomic environment.” In May, she considered the policy stance as “somewhat restrictive”.

- 1245ET – SF Fed's Daly (non-voter) on Bloomberg TV. Talking at an MNI event on Jul 10, she thinks the Fed should start thinking about cutting interest rates, potentially twice this year, and it's possible that a large tariffs-driven increase in inflation does not materialize. To support a September rate cut, Daly said she's looking for "a continuation of what we've been seeing, which is modest" disinflation.

- 1330ET – Gov. Cook (permanent voter) on AI and innovation (text + Q&A). She hasn’t spoken since Jun 3 but those comments were noteworthy as she explicitly noted some openness to hikes when talking scenarios. “The current stance of monetary policy is well positioned to respond to a range of potential developments. […] "We have to be open to all possibilities. We don't know how tariffs are going to play out. One could imagine those scenarios - cutting, staying or hiking, happening."

- 1830ET – Gov. Waller (permanent voter, dove) on the economic outlook and mon pol (text + Q&A). He has continued to burnish his dovish credentials since the June FOMC, saying that Fed policy is too tight and it could consider cutting in July. Waller is likely one of the two June SEP dots for three cuts this year, with a reminder of how divided the FOMC is with seven dots looking for zero cuts.

US INFLATION: Fed Beige Book Warns On More Rapid Price Increases Ahead

- In case missed from yesterday’s Beige Book, probably the most important finding for the FOMC was that the biggest price increases are yet to come: "Contacts in a wide range of industries expected cost pressures to remain elevated in the coming months, increasing the likelihood that consumer prices will start to rise more rapidly by late summer."

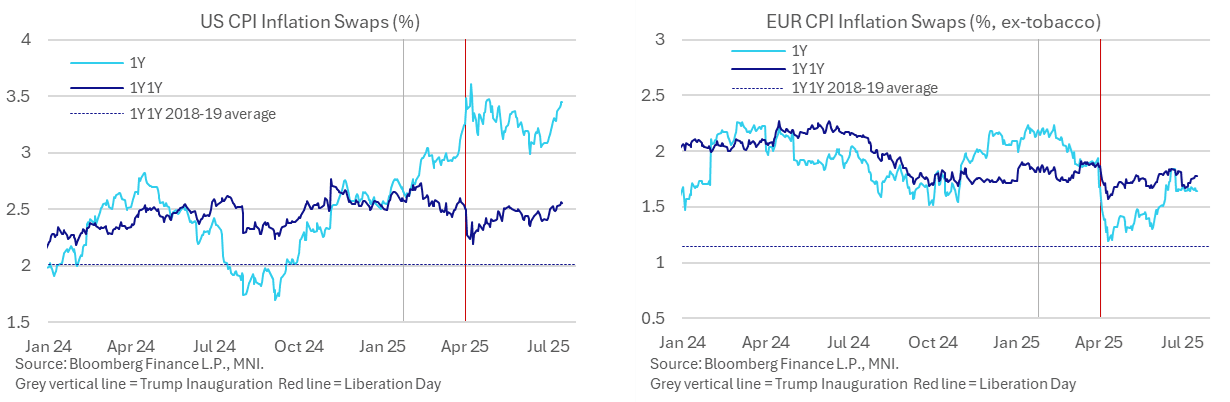

- Yesterday saw a volatile session for near-term inflation expectations, with 1Y inflation swaps falling 4bps to 3.40% on a dovish PPI report before surging almost 8bp on multiple media reports that Trump was considering firing Powell imminently. Trump himself then partly backtracked but with a for-clause caveat left open. It saw the 1Y swap close at 3.45% for highs seen after a hawkish CPI report on Tuesday.

- There has been a pronounced climb in 1Y expectations in the month to date, ending June at 3.08%. For context, it saw a high of 3.61% on Apr 8 before reciprocal tariff backtracking.

- The climb following the Powell firing headlines, and the associated legal challenges that could come with it, is also eye catching considering the 1Y swap is only running two months beyond when Powell’s Fed chair term expires.

- The inflation expectations profile continues to be front-loaded 1Y out but 1Y1Y expectations have also been drifting higher, closing at 2.56% for the past two days at highs since late March. That’s of course prior to Apr 2 reciprocal tariffs which were associated with expectations of a shorter-term spike in inflation.

SOFR: Mix Of Long Setting & Short Cover Seen In Futures On Wednesday

OI data points to a mix of net long setting and short cover during Wednesday’s uptick in SOFR futures.

- The most prominent individual net OI swings came via net short cover in SFRM5 & SFRU7, while the most meaningful net pack swing came via net long setting in the blues.

| 16-Jul-25 | 15-Jul-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,256,479 | 1,288,904 | -32,425 | Whites | +9,400 |

SFRU5 | 1,229,173 | 1,215,147 | +14,026 | Reds | +18,851 |

SFRZ5 | 1,298,761 | 1,284,154 | +14,607 | Greens | -15,539 |

SFRH6 | 1,010,094 | 996,902 | +13,192 | Blues | +26,508 |

SFRM6 | 870,312 | 860,460 | +9,852 |

|

|

SFRU6 | 829,318 | 816,688 | +12,630 |

|

|

SFRZ6 | 915,199 | 917,981 | -2,782 |

|

|

SFRH7 | 728,228 | 729,077 | -849 |

|

|

SFRM7 | 691,987 | 691,217 | +770 |

|

|

SFRU7 | 511,261 | 526,889 | -15,628 |

|

|

SFRZ7 | 448,681 | 446,185 | +2,496 |

|

|

SFRH8 | 307,323 | 310,500 | -3,177 |

|

|

SFRM8 | 231,070 | 228,677 | +2,393 |

|

|

SFRU8 | 207,344 | 201,739 | +5,605 |

|

|

SFRZ8 | 207,615 | 202,001 | +5,614 |

|

|

SFRH9 | 151,249 | 138,353 | +12,896 |

|

|

US TSY FUTURES: Net Short Cover Dominated On Wednesday

OI data points to net short cover in TY & UXY futures dominating during Wednesday’s rally, complemented by more modest short cover in FV & US.

- Modest rounds of net long setting in the wings (TU & WN) left curve-wide positioning tilted comfortably towards net short cover.

| 16-Jul-25 | 15-Jul-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,371,317 | 4,357,380 | +13,937 | +524,508 |

FV | 7,011,985 | 7,024,159 | -12,174 | -521,463 |

TY | 4,837,723 | 4,889,870 | -52,147 | -3,413,538 |

UXY | 2,405,903 | 2,417,895 | -11,992 | -1,034,296 |

US | 1,794,216 | 1,796,789 | -2,573 | -347,866 |

WN | 1,962,229 | 1,961,760 | +469 | +83,344 |

|

| Total | -64,480 | -4,709,312 |

EUROPE ISSUANCE UPDATE:

UK Auction Results: 4.375% Mar-30 Gilt

The 0.2bp tail at today’s 4.375% Mar-30 Gilt sale was in line with June’s reopening, but still tighter than the 0.5bp average across auctions since the start of this year. The 3.12x bid-to-cover ratio was broadly in line with the prior average of 3.15x, even if a little below June’s 3.26x and May’s 3.23x.

• The lowest accepted price of 101.225 was above 101.2125 pre-auction mid-price

• GBP4.75bln of the 4.375% Mar-30 Gilt. Avg yield 4.078% (bid-to-cover 3.12x, tail 0.2bp).

French Auction Results: MT OATs

Top of the E10-12bln range sold at today’s MT OAT auction, concentrated in the long 5-year on-the-run 2.70% Feb-31 OAT, where E5.213bln was sold.

• The bid-to-cover ratio for the Feb-31 line (2.72x) was weaker than the June re-opening (3.42x) but above the May sale (2.53x).

• Lowest accepted prices were above pre-auction mid prices across the three lines on offer.

• E3.953bln of the 2.40% Sep-28 OAT. Avg yield 2.27% (bid-to-cover 3.25x).

• E2.833bln of the 2.50% May-30 OAT. Avg yield 2.58% (bid-to-cover 3.49x).

• E5.213bln of the 2.70% Feb-31 OAT. Avg yield 2.74% (bid-to-cover 2.72x).

IL OATS

• E823mln of the 0.60% Jul-34 OATei. Avg yield 1.32% (bid-to-cover 3.04x).

•E432mln of the 0.10% Jul-38 Green OATei. Avg yield 1.64% (bid-to-cover 4.15x).

•E185mln of the 0.55% Mar-39 OATi. Avg yield 1.7% (bid-to-cover 4.08x).

Spanish Auction Results: Bono/Oblis

Overall, a well digested auction. Total of E5.684bln sold, in the mid/upper end of the E5-6bln range. Most of the sale was concentrated towards to the 10-year on-the-run 3.20% Oct-35 Obli (E2.392bln).

• For this line, the bid-to-cover ratio of 1.98x was above last month’s 1.73x. Today’s auction was the second re-opening of the bond after being launched via syndication in May.

• Pre-auction mid prices were above lowest accepted prices across the three lines on offer.

• E1.746bln of the 2.70% Jan-30 Bono. Avg yield 2.479% (bid-to-cover 1.94x).

• E2.392bln of the 3.20% Oct-35 Obli. Avg yield 3.303% (bid-to-cover 1.98x).

• E1.546bln of the 2.70% Oct-48 Obli. Avg yield 3.965% (bid-to-cover 1.60x).

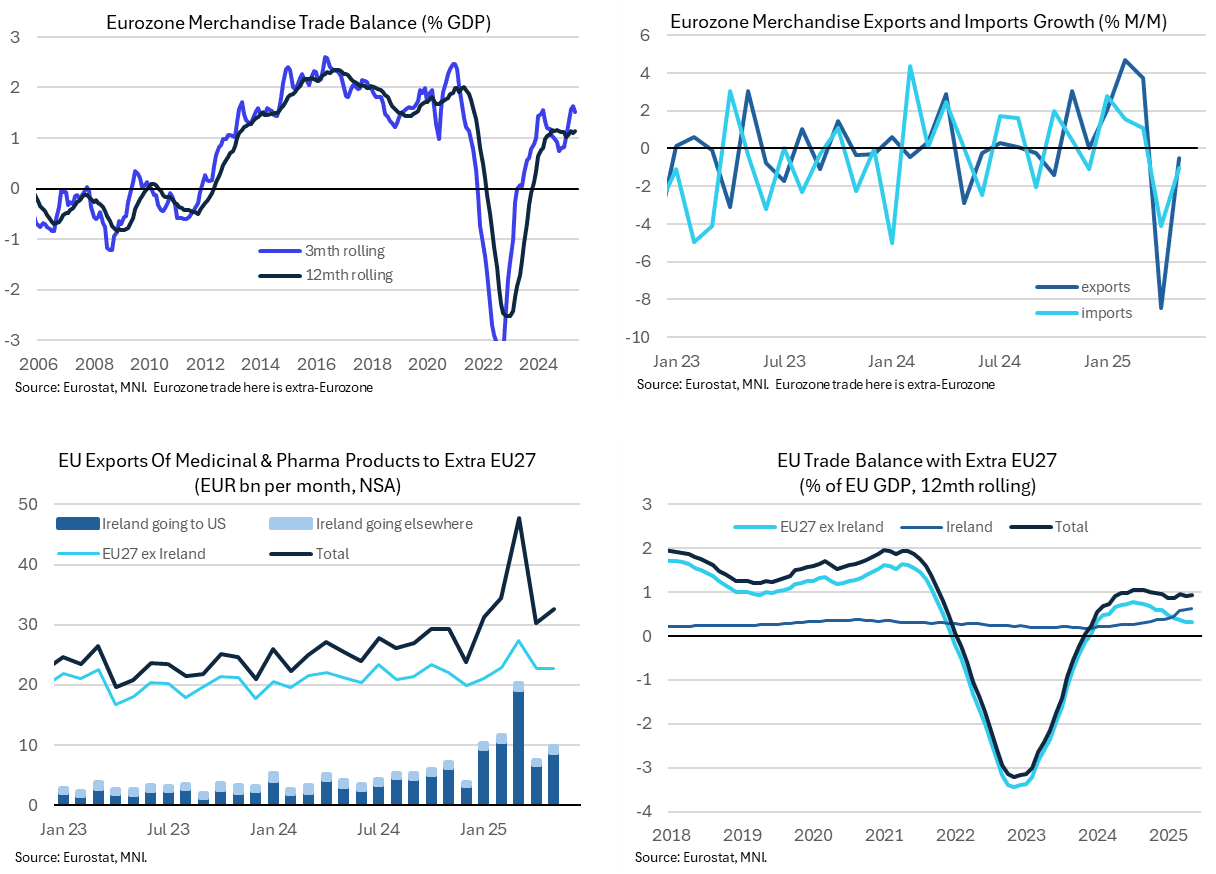

EUROPEAN DATA: Further Trade Surplus Normalization In May

Released yesterday (but with some issues getting hold of Eurostat data at the time):

- The Eurozone trade surplus was larger than expected in May at E16.2bn (SWDA, cons E14.0bn) after an upward revised E15.1bn (initial E14.0bn) in April.

- As hinted at in already released May trade data from major trading partners, it’s a second month of partial stabilisation after surpluses surged in Feb and Mar primarily on US tariff front-running of Irish pharmaceutical exports.

- Indeed, the average E15.7bn surplus over Apr-May compares with E28.8bn in March, E21bn in Feb, E13.4bn in Jan and an average E10.8bn in Q4 or E14.1bn in 2024 as a whole.

- It left goods trade surpluses worth ~1.2% GDP over Apr-May vs 1.6% GDP in Q1 and 0.8% GDP in Q4.

- Exports fell -0.5% M/M after a huge -8.4% M/M in April as that previous pharma surge unwound, whilst imports fell -1.0% M/M after -4.1% M/M (all swda figures).

- Latest exports weakness was commodities-led, with largest declines for crude materials (-6.0% M/M) and mineral fuels (-5.9% M/M, includes petroleum & petroleum products). Latest imports weakness was also partly in commodities (mineral fuels -6.9% M/M) whilst there was also -6.5% M/M drop in chemicals which looks like a lagged link to the previous surge in exports to the US.

- The broader EU trade data paint a similar picture, with a surplus of E13.4bn after E11.9bn in April following large surpluses in Feb and Mar (swda). It’s worth an average 0.8% GDP in Apr-May vs 1.1% GDP in Q1 and 0.5% GDP in Q4.

- The growing magnitude of Irish trade is clear to see: the extra EU surplus of 0.9% GDP over a rolling twelve-month basis is almost unchanged compared to a year ago. Over that period, the Irish trade surplus has doubled from 0.3% to 0.6% of EU GDP whereas the ex-Irish surplus has trimmed from 0.7% to 0.3% of EU GDP.

- EU imports from China remain elevated although narrowed their gap over 2024 levels as opposed to ramping higher. We don’t go into it here as have touched upon elsewhere with more timely data (see INTERNATIONAL TRADE: Still No Clear Signs of China-EU Trade Diversion In June – July 14).

US: Sentate Passes Trump's Rescissions Package, Raises Risk Of Govt Shutdown

The Senate has voted 51-48 to pass President Donald Trump's USD$9 billion request to cut Congressionally authorised funding for the State Department's foreign aid budget and public broadcasters. Two Republican Senators, Susan Collins (R-ME) and Lisa Murkowski (R-AK), voted against the measure.

- While the bill claws back a relatively small portion of federal government spending, Democrats view the request as part of a broader plan by the Trump administration to co-opt spending powers from Congress. Senate Minority Leader Chuck Schumer (D-NY) has linked the rescissions package to the FY26 appropriations process, which is likely to result in a short-term funding measure in late September that will need Democratic votes to prevent the government from shutting down.

- While conventional wisdom in Washington suggests that Democrats will never willingly shut down the government, Schumer has little other leverage to contest Trump's agenda.

- Top Democrat Appropriator Senator Patty Murray (D-WA) said: “We have never, never before seen bipartisan investments slashed through a partisan rescissions package... Do not start now. Not when we are working, at this very moment, in a bipartisan way to pass our spending bills."

- The implied probability of a shutdown is currently around 40%, according to Polymarket. That number is likely to rise in the coming weeks if the FY26 appropriations process continues to stall, as expected.

- As the only major Senate revision was to remove a USD$400 million cut to PEPFAR, a George W. Bush-era HIV-AIDS relief programme, the House is likely to send the bill to Trump's desk today or tomorrow.

HKD: USD/HKD Sell-Off Unlikely to be Triggered by HKMA

The USD/HKD rate underwent a spell of volatility shortly after the local close, with the rate slipping 80 pips before recovering across the European morning. No specific headlines or newsflow crossed to trigger the move, which may raise speculation of further intervention from HKMA as the rate pressures the weak-side of the band.

- HKMA have already intervened this week, buying HKD 14.8bln to defend the peg on Tuesday - but the price action is not consistent with the intervention style of the central bank, which tend to sit on the bid rather than push through sharp spot swings in prices.

- Similarly, there have been no parallel moves in either FX swap rates or a notable uptick in the HIBOR fix overnight. UBP in Singapore see "no news at all to drive" this move, citing positioning rebalancing for the intraday HKD rally.

- Some focus may be being paid to a revived listing filings of phone glass maker Biel Crystal, who have reportedly held prelim discussions with authorities after being forced to abandon a float as recently as 2022 valued at between $1-2bln. Such a float size would be among the largest corporate activity of the year, adding to an IPO pipeline that already includes Shein.

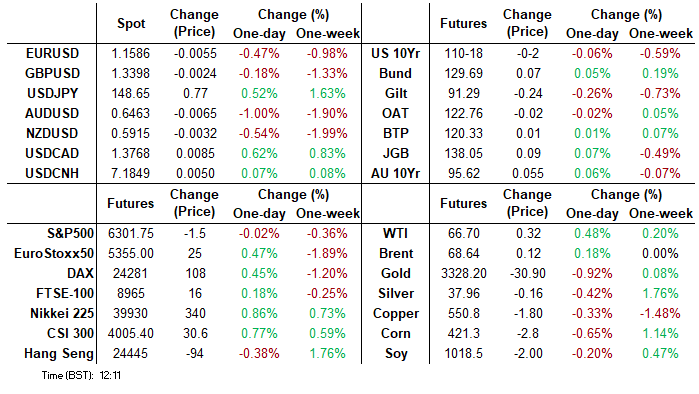

FOREX: Labour Market Developments Swiftly Change Tide for AUDUSD

- The primary driver for AUD (-0.86%) underperformance overnight has been the weaker-than-expected jobs report. Jobs growth disappointed at just +2k (Est. +20k) and notably this was weighed by full time jobs falling by 38.2k. Furthermore, the unemployment rate rose to 4.3% (Est. 4.1%).

- Analysts have been quick to point out that a solid job market has been a key reason why the RBA has been patient thus far in easing policy, and the latest data will open the door wider to further rate cuts ahead. An August cut is now fully priced, while markets currently expect ~65bps of easing by year end. Sure enough, Nomura now expect 25bp cuts in Aug, Nov and Feb.

- On top of the jobs report, consumer inflation expectation also dipped in July to 4.7%, and the cautious tone surrounding the Trump-Powell spat may provide a headwind to higher beta currencies, even if the dollar were to come under renewed selling pressure.

- For AUDUSD, today’s move below the 50-day EMA (intersects at 0.6490) appears meaningful, and a daily close below this average would be the first in over three months, highlighting a stronger reversal. The initial target for the move would be 0.6435 (Fib retracement) before 0.6373, the Jun 23 low and technical bear trigger.

- One FX strategist at ANZ believes that in the near term there are risks around a further move lower for AUDUSD, also forecasting RBA easing in both Aug and Nov.

FOREX: Dollar Erodes Trump-Powell Induced Selloff, AUD Underperforms

- The US dollar is on the front foot again Thursday, having eroded the majority of the sharp selloff induced by the Trump-Powell headlines late yesterday. The USD index trades 0.3% in the green but highs overnight remained just shy of the recovery highs posted at 98.91. The narrative around the potential firing of Federal Reserve Chair Jerome Powell has reintroduced a key bearish catalyst for the dollar, although Trump’s pushback has provided short-term stability.

- The primary driver for AUD (-0.86%) underperformance overnight has been the weaker-than-expected jobs report and the notable uptick in the unemployment rate, which have bolstered RBA easing expectations. For AUDUSD, today’s move below the 50-day EMA (intersects at 0.6490) appears meaningful, and a daily close below this average would be the first in over three months, highlighting a stronger reversal. The initial target for the move would be 0.6435 (Fib retracement) before 0.6373, the Jun 23 low and technical bear trigger.

- Elsewhere, the broad based usd strength has been notable against the Japanese yen, with USDJPY bouncing over 1% from yesterday’s lows. Yesterday’s highs at 149.17 will remain the short-term reference point above as markets await trade discussions between US/Japan officials and this weekend’s upper house election.

- The next focus will be on 149.38, the 50.0% retracement of the Jan 10 - Apr 22 bear leg, and 150.49, the Apr 2 high.

- GBP moderately outperforms on the back of this morning’s labour market data, which was a little firmer-than-expected on net and reduced any residual odds of sequential BoE cuts at this stage. With that said, GBPUSD remains around the 1.3400 mark, within close proximity of the recent lows at 1.3365.

- Later today, US retail sales, Philly Fed manufacturing and import prices highlight the calendar, alongside various Fed speakers.

OPTIONS: Expiries for Jul17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500-10(E1.9bln), $1.1525-40(E1.1bln), $1.1585-00(E1.3bln), $1.1600(E1.1bln), $1.1650-55(E1.1bln) $1.1700(E1.4bln), $1.1750-70(E1.4bln);

- USD/JPY: Y147.00($1.0bln), Y148.00($704mln), Y148.95-00($1.7bln)

- GBP/USD: $1.3425(Gbp500mln), $1.3445-60(Gbp1.2bln)

- EUR/JPY: Y171.00-20(E930mln)

- USD/CNY: Cny7.1691-05($549mln)

EQUITIES: Futures Mixed, E-mini Holds Bounce Off Weds Lows

- S&P E-Minis are still trading in a range, closer to their recent highs. The trend condition remains bullish. Recent activity has resulted in a break of resistance at 6128.75, the Jun 11 high. The breach confirmed a resumption of the uptrend that started Apr 7.

- A bull cycle in Eurostoxx 50 futures remains in play and the latest pullback still appears corrective. Support to watch lies at 5281.00, the low on Jul 1 and 4. A clear break of this price point would strengthen a bearish threat.

COMMODITIES: WTI Sticks Closely to 200-dma

- A bull cycle in Gold that started Jun 30, remains intact and the yellow metal is holding on to the bulk of its recent gains. Note that medium-term trend conditions are bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend.

- A bearish tone in WTI futures remains intact. The sharp reversal from the Jun 23 high continues to highlight scope for an extension lower and this suggests that recent gains have been corrective.

| Date | GMT/Local | Impact | Country | Event |

| 17/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 17/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/07/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1230/0830 | ** | Import/Export Price Index | |

| 17/07/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/07/2025 | 1230/0830 | *** | Retail Sales | |

| 17/07/2025 | 1315/0915 | Fed Governor Adriana Kugler | ||

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1400/1000 | ** | NAHB Home Builder Index | |

| 17/07/2025 | 1400/1000 | * | Business Inventories | |

| 17/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 17/07/2025 | 1645/1245 | San Francisco Fed's Mary Daly | ||

| 17/07/2025 | 1730/1330 | Fed Governor Lisa Cook | ||

| 17/07/2025 | 2000/1600 | ** | TICS | |

| 17/07/2025 | 2230/1830 | Fed Governor Christopher Waller | ||

| 18/07/2025 | 2330/0830 | *** | CPI | |

| 18/07/2025 | 0600/0800 | ** | PPI | |

| 18/07/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/07/2025 | 0900/1100 | ** | Construction Production | |

| 18/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 18/07/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |