MNI US MARKETS ANALYSIS - AUD Prints 10th Higher High

Highlights:

- Equities gain alongside US yield curve; Trump set to meet Sheinbaum & Carney

- USD stabilises headed through Friday crossover: US jobs report won't be released today, but personal income/spending numbers in focus

- Impulsive wave continues in AUDUSD; pair prints 10 sessions of higher highs

US TSYS: Broadly Back At Yesterday’s Lows With September PCE Eyed

Treasuries sit mildly lower as US desks filter in having reversed small gains seen in Asia hours, and for the most part are back near yesterday’s lows or lower still in the case of 30s. Today’s docket is focused on the delayed personal income and outlays report for September at 1000ET whilst Trump meeting Carney and Sheinbaum highlights the political calendar.

- Cash yields are 0.5-1.5bp higher on the day, with increases led by the long-end.

- TYH6 has recently touched yesterday’s low of 112-22 (-01) on very thin overnight volumes of 190k.

- A bear threat remains present with support at that 112-22 (Dec 2/4/5 lows) after which lies 112-10+ (Nov 20 low) before a key 112-07 (Nov 5 low).

- Data: Chicago Fed CARTS Retail Indicator Nov prelim (0830ET), Manheim used vehicle prices Nov (0900ET), PCE Report Sep (1000ET), U.Mich Dec prelim (1000ET), Consumer credit Oct (1500ET)

- Politics: Trump attends FIFA World Cup Draw (1140ET) and will meet with Canada’s Carney and Mexico’s Sheinbaum, Trump signs Executive Orders (1500ET)

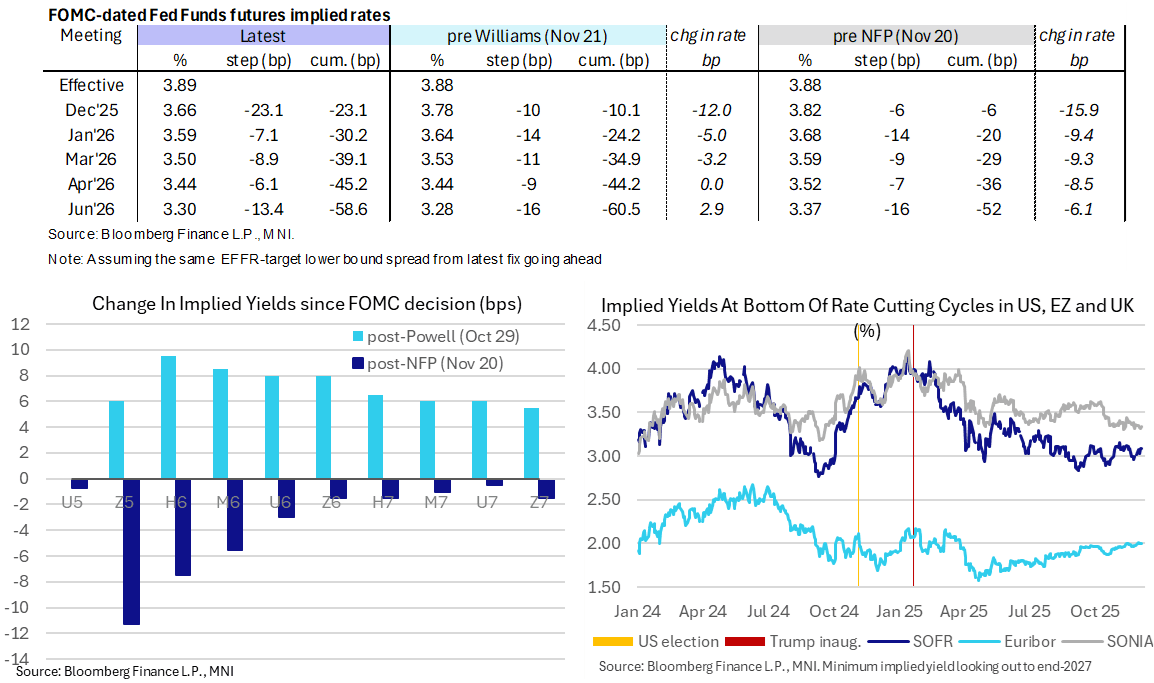

STIR: Fed Rates Hold Yesterday’s Hawkish Tilt, PCE Report In Focus

- Fed Funds implied rates are little changed overnight for meetings out to mid-2026, awaiting today’s personal income and outlays report for September at a later than usual 1000ET.

- Cumulative cuts from 3.89% effective: 23bp Dec, 30bp Jan, 39bp Mar, 45bp Apr and 58.5bp Jun.

- SOFR futures are also little changed on the day, with the terminal implied yield of 3.085% holding yesterday’s 5.5bp increase in a move aided that was supported by particularly low initial jobless claims even if they were caveated by a question mark over Thanksgiving adjustments.

- Core PCE inflation is seen increasing ~0.22% M/M in today’s September release after 0.24% in Aug and 0.26% in Jul with scope for small upward revisions there.

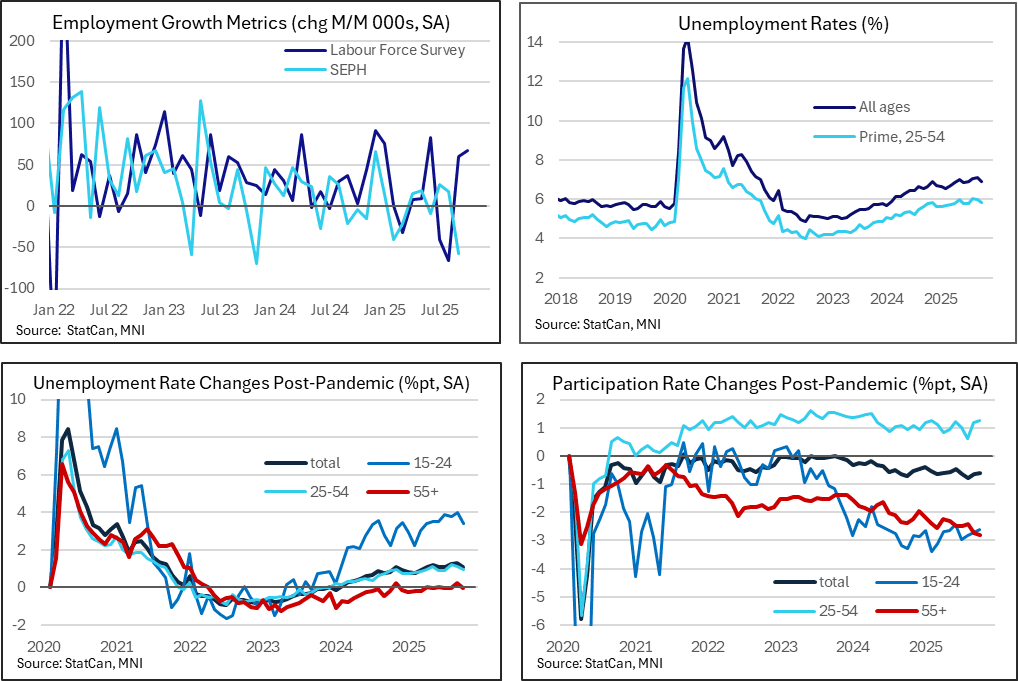

CANADA DATA: Labour Survey Expected To Show Steadier Jobs After Swings

- The labour force survey for November is released at 0830ET on Friday and should help shape expectations for how long the BoC is likely to remain on hold for after signalling a pause ahead in October.

- The overnight rate of 2.25% is deemed “about the right level to keep inflation close to 2% while helping the economy through this period of structural adjustment." BoC-dated OIS currently shows only 6-7bps of easing bias out to mid-2026.

- Employment growth is expected to have slowed materially in Nov with Bloomberg consensus for -2.5k after a far stronger than expected 67k increase in October that came entirely from part-time positions. Separate payrolls data showed a sharp decline back in September with -58k but the two have weak correlation on a month-to-month basis.

- However, remember that the 127k cumulative increase in labour force survey employment in Sep-Oct followed a 106k decline in Jul-Aug. These monthly changes have been volatile for some time now whilst the unemployment rate helps gives a better sense of labour market pressures.

- Bloomberg consensus currently eyes a 7.0% unemployment rate to lift again after a surprisingly low 6.9% in October pulled back from two months at 7.1% at what were the highest since mid-2021. Having increased through 2023 and 2024, the climb in the unemployment rate has levelled off having averaged 6.9% since late 2024.

SOFR: Short Setting Dominated In Futures On Thursday, IJC & Global Cues Noted

OI data points to net short setting dominating as SOFR futures ticked lower in the wake of yesterday’s weekly jobless claims data.

- Instances of net long cover were limited and isolated.

- The biggest net positioning swing came via net short setting in SFRH6 futures.

- A reminder that cues from Japan & Europe were bearish for SOFR futures in pre-NY trade.

| 04-Dec-25 | 03-Dec-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRU5 | 1,308,218 | 1,308,887 | -669 | Whites | +40,564 |

SFRZ5 | 1,596,001 | 1,594,261 | +1,740 | Reds | +33,746 |

SFRH6 | 1,394,571 | 1,355,196 | +39,375 | Greens | +6,463 |

SFRM6 | 1,145,840 | 1,145,722 | +118 | Blues | +10,733 |

SFRU6 | 1,080,410 | 1,075,434 | +4,976 |

|

|

SFRZ6 | 1,120,867 | 1,110,662 | +10,205 |

|

|

SFRH7 | 847,158 | 831,599 | +15,559 |

|

|

SFRM7 | 779,747 | 776,741 | +3,006 |

|

|

SFRU7 | 821,622 | 821,712 | -90 |

|

|

SFRZ7 | 845,239 | 843,125 | +2,114 |

|

|

SFRH8 | 441,689 | 433,005 | +8,684 |

|

|

SFRM8 | 403,779 | 408,024 | -4,245 |

|

|

SFRU8 | 381,998 | 378,027 | +3,971 |

|

|

SFRZ8 | 321,437 | 321,238 | +199 |

|

|

SFRH9 | 195,315 | 195,364 | -49 |

|

|

SFRM9 | 212,359 | 205,747 | +6,612 |

|

|

EUROPE ISSUANCE UPDATE

[UK DMO UPDATE] FQ4 Operations:

The only new news is the confirmation of the week for the long syndi (W/C 19 Jan) and the ISIN for the medium green.

[EGB FUNDING UPDATE] Belgium 2026 Funding Plan:

- Gross borrowing requirement E59.55bln (up from E5.90bln from E53.65bln in 2025; original estimate was E44.65bln, then increased by E8.bln in June largely due to defence spending).

- Net financing requirement is E26.37bln (down from E27.43bln in 2025; original 2025 estimate was E19.43bln)

- Green: "The BDA does not anticipate launching a new Green OLO in 2026... Both existing Green OLOs... can be reopened." Green issuance limit expected at E5.0bln.

- Full funding plan available here.: https://www.debtagency.be/sites/default/files/content/download/files/borrowingreq-2026.pdf

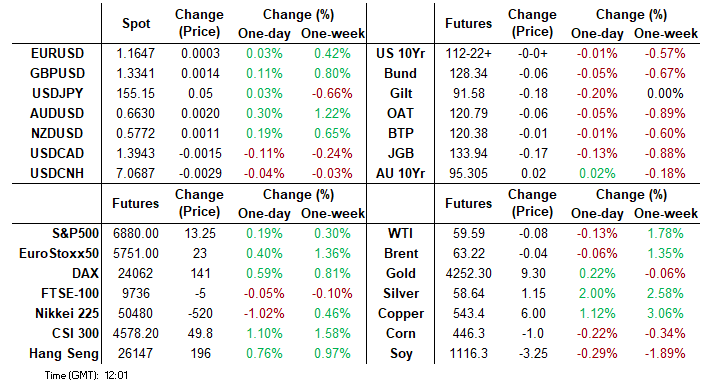

FOREX: USDJPY Prints Pullback Lows, AUD Extends Higher Highs Streak

- USDJPY saw renewed volatility overnight, setting fresh pullback lows at 154.35 before recovering back up around the 155.0 handle. This came despite weak Japanese household spending data being a sign of fragile domestic demand, with consolidating expectations for a BoJ hike at the Dec 18-19 meeting holding sway in the short term.

- The current retracement in USDJPY is allowing a recent overbought condition to unwind. The recent extension lower exposes the 50-day EMA, currently intersecting at 153.41. USD1.94b of options expire today at 155.0, which could act as a magnet as we approach the NY cut.

- AUDUSD continues its slow but steady ascent, trading further above the late October highs of 0.6618 to reach an intra-day peak of 0.6635. The pair has now posted 10 consecutive sessions of higher highs, as the bullish impulsive wave extends. With a number of resistance points being cleared, targets on the topside are now found at 0.6660 (Sep 18 high) and 0.6723, the Oct 21 2024 high.

- German Chancellor Merz is travelling to Belgium today to push for the backing of a loan to the Ukraine with frozen Russian assets. While the US has reportedly lobbied against such a setup, an agreement between European countries on the deal would strengthen Ukraine's position in current negotiations, and hence be EUR-supportive. EURUSD will be monitoring a weekly close above 1.1656 resistance, that has been pierced this week.

- September PCE data will headline the data calendar for today, with Michigan sentiment to be published simultaneously. Canadian November employment data is also due, while ECB's Villeroy and Lane are scheduled to speak.

OPTIONS: Expiries for Dec05 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.2bln), $1.1715(E959mln)

- USD/JPY: Y155.00($1.4bln)

- GBP/USD: $1.3210(Gbp745mln), $1.3250(Gbp653mln)

- AUD/USD: $0.6500(A$1.1bln)

- USD/CAD: C$1.3990-15($1.3bln)

EQUITIES: Bullish E-Mini S&P Theme Intact, Contract Above 20-, 50-Day EMAs

- A bull cycle in Eurostoxx 50 futures remains intact. Price has recently cleared the 20- and 50-day EMAs, signaling scope for a stronger recovery. Sights are on 5742.40 next (pierced), the 76.4% retracement of the Nov 13 - 21 bear leg. Clearance of this price point would pave the way for an extension towards 5825.00, the Nov 13 high and a key resistance. First key support lies at 5617.30, the 50-day EMA.

- A bullish theme in S&P E-Minis is intact and the contract continues to appreciate. Price remains above the 20- and 50- day EMAs. Note that recent gains signal the likely end of the corrective cycle between Oct 30 and Nov 21. A continuation higher would highlight potential for a move towards the key resistance and bull trigger at 6953.75, the Oct 30 high. Key support lies at 6525.00, the Nov 21 low. First support is at 6788.55, the 20-day EMA.

COMMODITIES: Gold Key Resistance and Bull Trigger Marked at $4381.52

- Short-term gains in WTI futures appear corrective. Note that moving average studies are in a bear-mode position, highlighting a dominant downtrend. A resumption of the bear leg would open the key support and the bear trigger at $55.99, the Oct 20 low. Clearance of this level would resume the downtrend. Key short-term resistance to watch is $61.84, the Oct 24 high. A clear break of this hurdle would signal scope for a stronger correction.

- The trend needle in Gold continues to point north. The bear phase between Oct 20 and 28 appears to have been a correction and note that the recovery since Oct 28 signals the end of that corrective cycle. Key support to watch lies at the 50-day EMA, at $4024.3. Clearance of this EMA would signal scope for a deeper retracement. Sights are on key resistance and the bull trigger at $4381.5, the Oct 20 high.

| Date | GMT/Local | Impact | Country | Event |

| 05/12/2025 | 1330/0830 | *** | Labour Force Survey | |

| 05/12/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 05/12/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 05/12/2025 | 1500/1000 | *** | Personal Income and Consumption | |

| 05/12/2025 | 1510/1610 | ECB Lane in Panel at CEPR Paris Symposium | ||

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 05/12/2025 | 2000/1500 | * | Consumer Credit |