MNI US MARKETS ANALYSIS - 10% Odds of 50bps Fed Cut Into PPI

Highlights:

- Russian incursion into Poland airspace triggers NATO Article 4, consultations expected

- Treasury curve twist steeper into PPI, first PCE input of the week

- Fed pricing eyes 10% odds of 50bps cut in September, totality of this week's data could be decisive

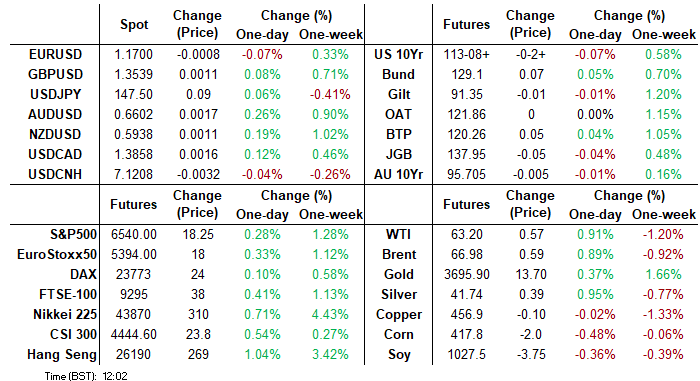

US TSYS: Modestly Twist Steeper With PPI, Geopol and 10Y Supply In Focus

- Treasuries sit modestly twist steeper around the US crossover, with the front end paring yesterday’s decent-sized losses considering headline/data flow at the time.

- The long end sees little sign of haven flow following Poland triggering Article 4 after numerous drones violated its airspace. A press conference with E5 defense ministers is due at 0900ET today.

- Away from geopol, today’s scheduled focus will be on PPI inflation at 0830ET before the 10Y auction at 1300ET after last month’s poorly received offering.

- Cash yields range from 1.5bp lower (2s) to 1.2bp higher (30s).

- The moves do little to dent recent flattening away from multi-year steeps in 5s30s, at 113.5bp vs recent highs of 126.bps.

- TYZ5 trades at 113-08+ (-02+) in what have been relatively narrow ranges on thin cumulative volumes only just hitting 200k.

- A bullish theme remains in play with resistance seen at 113-21+ (Sep 5 high, post-NFPs) before 113-26+ (Fibo proj). An overnight low of 113-06 didn’t trouble support at 112-28+ (Sep 5 low).

- Data: MBA mortgage applications, PPI Aug (0830ET), Wholesale trade sales/inventories Jul/Jul F (1000ET)

- Coupon issuance: US Tsy $39B 10Y Note auction re-open - 91282CNT4 (1300ET). Last month’s 10Y auction tailed by 1bp along with a sizeable decline in the bid-to-cover from 2.61 to 2.35.

- Bill issuance: US Tsy $65B 17W bill auction (1130ET)

- Politics: No publicly scheduled events for Trump, with an intelligence briefing at 1130ET and a dinner at 1900ET.

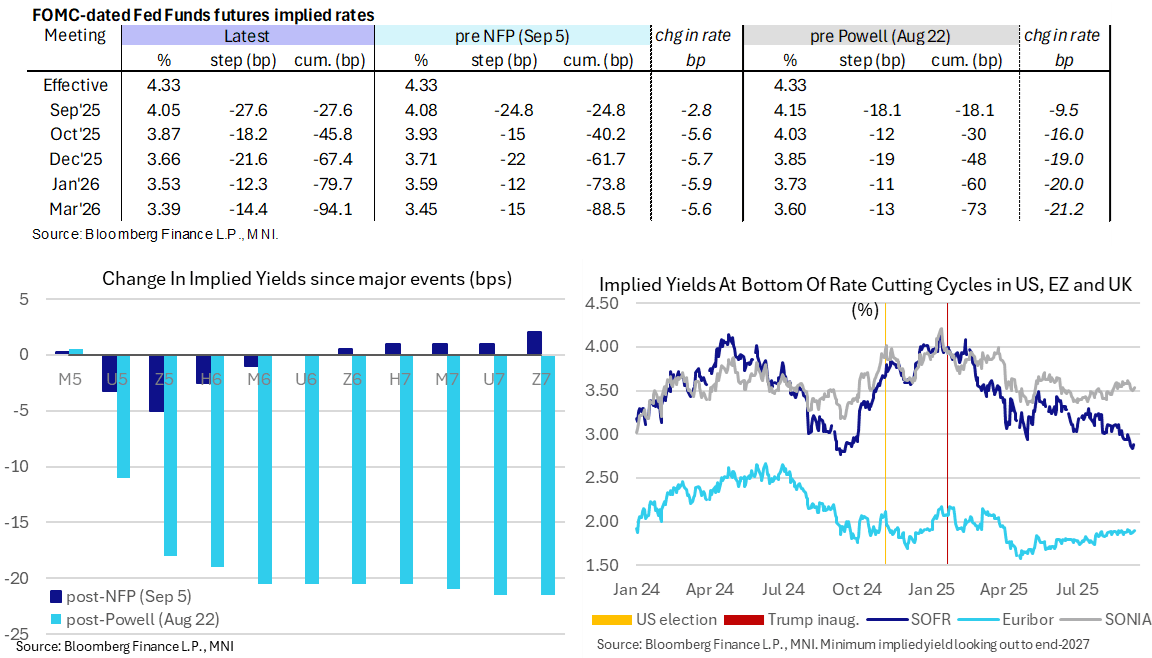

STIR: Still ~10% Odds Of 50bp Fed Cut Next Week With PPI Ahead

- Fed Funds implied rates have cooled a little from yesterday’s push higher, a move that was mostly seen through the session after admittedly very large downward revision estimates for payrolls were within wide ranges for analyst estimates.

- It still sees ~10% odds of a 50bp cut with the FOMC decision next week ahead of today’s PPI report for August at 0830ET after a surprising surge in July. CPI then unusually follows tomorrow.

- Cumulative cuts from 4.33% effective: 27.5bp Sep 17, 46bp Oct, 67.5bp Dec, 79.5bp Jan and 94bp Mar.

- The SOFR implied terminal yield of 2.895% (SFRH7) is just 1bp higher on the day, a little off Monday’s lowest close since Sep 2024 with 2.84% and towards cycle lows.

- Latest on the Cook lawsuit: A federal judge Tuesday night granted a preliminary injunction blocking President Donald Trump from firing Federal Reserve Governor Lisa Cook while her lawsuit challenging her termination is resolved. The FOMC is set to meet again September 16-17. "At this preliminary stage, the Court finds that Cook has made a strong showing that her purported removal was done in violation of the Federal Reserve Act’s 'for cause' provision," Judge Jia Cobb wrote.

- Just recently, the White House has pushed back on the ruling, saying it is not the last say on the matter.

MNI ECB Preview: Growth Outlook Watched Amidst Data Dependence

Download Full Report Here

Resending from yesterday due to email distribution issues.

Executive Summary

- The ECB is fully expected to leave its three key rates on hold on Thursday, with its deposit rate at 2.00%.

- ECB President Lagarde is expected to continue to suggest policy is in a good place.

- A data-dependent and meeting-by-meeting approach is expected to be reiterated in a continuation of July’s “deliberatively uninformative” communication approach around future rate decisions.

- Lagarde’s characterisation of economic resilience and/or the extent to which uncertainty has been alleviated by the US-EU trade deal should help shape market reaction.

- Fresh economic projections aren’t expected to be material.

- Recent resilience sees cuts no longer fully priced, with a cumulative 18bp of cuts seen out to mid-2026.

- We judge that the median analyst no longer looks for another cut although the bias is clearly still lower, with 7 of 25 looking for one more cut and 4 looking for two more.

- EUR/USD approaches the meeting after recent strength has seen it tilt back closer to 1.18, a level shortly after which drew unusually direct comments from ECB’s De Guindos back at the Sintra conference.

SECURITY: Incursion Of Polish Airspace Exposes Fragility Of NATO's Article 5

A NATO spokesperson confirmed that up to 10 Russian drones violated Polish airspace overnight. A number of the drones were shot down by a multinational NATO air operation, including Italian and Dutch assets, in what appears to be the first direct military confrontation with Russia on NATO territory.

- Polish PM Donald Tusk confirmed on X that Poland shot down drones that “posed a direct threat”, adding in later comments that the “violation of Poland's airspace was likely large-scale provocation."

- The EU's top diplomat, Kaja Kallas, said that the incident was “the most serious European airspace violation by Russia since the war began, and indications suggest it was intentional, not accidental.”

- A NATO spokesperson said, per Reuters, that the alliance is not treating the incursion “as an attack” but confirmed that NATO believes the Poland incident “was an intentional incursion by Russian drones”. NATO members will discuss their response at a regular council meeting this morning.

- While the NATO statement suggests the alliance is managing expectations about a collective response, the incursion is a major challenge to NATO’s ‘Article 5’ principle, with the alliance struggling to define the parameters of an attack that would warrant a collective response, leaving a large grey area for Moscow to conduct hybrid and low-level kinetic operations in NATO member states.

- European Commission President Ursula von der Leyen signalled that the incursion necessitates additional sanctions on Russia, including financing Kyiv with frozen Russian sovereign assets but it is unclear how quickly the EU can pass new sanctions, with Hungary and Slovakia likely to oppose any new measures.

- Notably, the incursion comes ahead of the five-day ‘Zapad’ joint Russian/Belarusian military exercises near the Polish border, starting September 12. The exercises are officially expected to involve around 13,000 troops, but analysts caution the real number is likely to be far higher, per CEPA. Military experts warn that the exercises could provide cover for expanded Russian operations in Ukraine or mask a build-up of Russian military assets on NATO’s eastern flank.

SOFR: Net Short Setting Dominated In Futures On Tuesday

OI data points to net short setting across much of the SOFR futures strip on Tuesday, with only fairly limited rounds of net long cover in SFRU6 and and SFRH7 breaking the wider theme.

| 09-Sep-25 | 08-Sep-25 | Daily OI Change |

| Daily OI Change In Packs |

SFRM5 | 1,226,097 | 1,225,497 | +600 | Whites | +88,268 |

SFRU5 | 1,427,566 | 1,421,657 | +5,909 | Reds | +11,973 |

SFRZ5 | 1,639,511 | 1,611,543 | +27,968 | Greens | +35,315 |

SFRH6 | 1,196,308 | 1,142,517 | +53,791 | Blues | +30,985 |

SFRM6 | 1,010,351 | 987,750 | +22,601 |

|

|

SFRU6 | 883,230 | 892,152 | -8,922 |

|

|

SFRZ6 | 1,004,052 | 994,559 | +9,493 |

|

|

SFRH7 | 705,550 | 716,749 | -11,199 |

|

|

SFRM7 | 838,559 | 831,734 | +6,825 |

|

|

SFRU7 | 669,554 | 660,917 | +8,637 |

|

|

SFRZ7 | 647,308 | 634,378 | +12,930 |

|

|

SFRH8 | 440,844 | 433,921 | +6,923 |

|

|

SFRM8 | 356,966 | 348,383 | +8,583 |

|

|

SFRU8 | 258,028 | 252,002 | +6,026 |

|

|

SFRZ8 | 266,934 | 258,791 | +8,143 |

|

|

SFRH9 | 176,041 | 167,808 | +8,233 |

|

|

US TSY FUTURES: Net Long Cover Dominated On Tuesday

OI data points to net long cover in most contracts as Tsy futures settled lower on Tuesday.

- Modest rounds of net short setting in UXY & WN futures broke the broader trend.

- The largest DV01 equivalent positioning swing came in US futures.

| 09-Sep-25 | 08-Sep-25 | Daily OI Change | OI DV01 Equivalent Change ($) |

TU | 4,485,021 | 4,499,161 | -14,140 | -577,163 |

FV | 6,789,828 | 6,797,362 | -7,534 | -336,257 |

TY | 5,263,443 | 5,282,797 | -19,354 | -1,327,159 |

UXY | 2,365,379 | 2,358,821 | +6,558 | +597,880 |

US | 1,828,158 | 1,854,170 | -26,012 | -3,695,960 |

WN | 2,021,065 | 2,015,958 | +5,107 | +948,801 |

|

| Total | -55,375 | -4,389,858 |

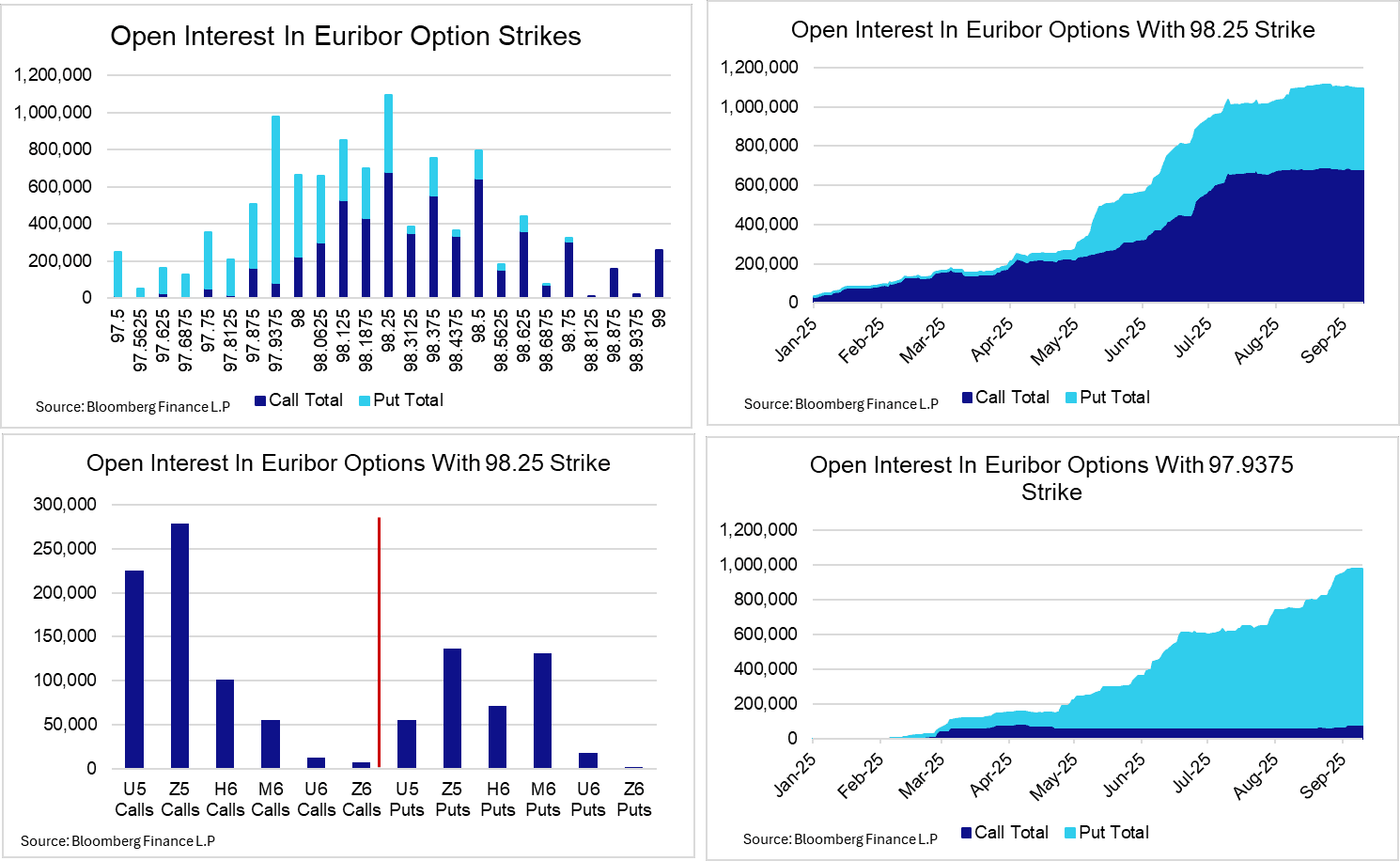

ECB: EUR STIR Options Flow More Balanced As Terminal Approaches

With the ECB now at or close to its assumed terminal rate, recent EUR STIR options flow has been much more balanced than earlier this year (where it was dominated by demand for dovish call structures).

- A divergence in participants’ views likely reflect differing opinions on (i) the underlying strength of Eurozone domestic demand and the impact of past rate cuts, (ii) the eventual economic impact of a higher US effective tariff rate and (iii) the eventual impulse from higher German fiscal spending.

- Thursday’s communication and updated projections will provide an update on how the ECB currently assesses these drivers, and will be key in shaping any market reaction on the day.

- Popular dovish plays in recent weeks have included significant purchases of the ERM6 98.3125/98.4375 call spread, alongside other upside call structures in Z5 and H6. On a shorter-term basis, today’s flow has included a buyer of the ERU5 98.00/98.06 call spread. These options expire on Sep 15th, so essentially capture tomorrow’s ECB decision in isolation.

- However, there has also been demand for more hawkish put spreads and flies expiring through the course of next year during the past few weeks.

- Looking at options in ERU5, ERZ5, ERH6, ERM6, ERU6 and ERZ6, the 98.25 strike currently has the highest open interest, followed by the 97.9375 strike. While 98.25 strike OI is fairly evenly split between calls (60%) and puts (40%), 97.9375 is dominated by puts (90%). We note that put sales have been used to fund dovish call structures through this year, but recent increases in OI have also reflected increased demand for the hawkish put structures noted above.

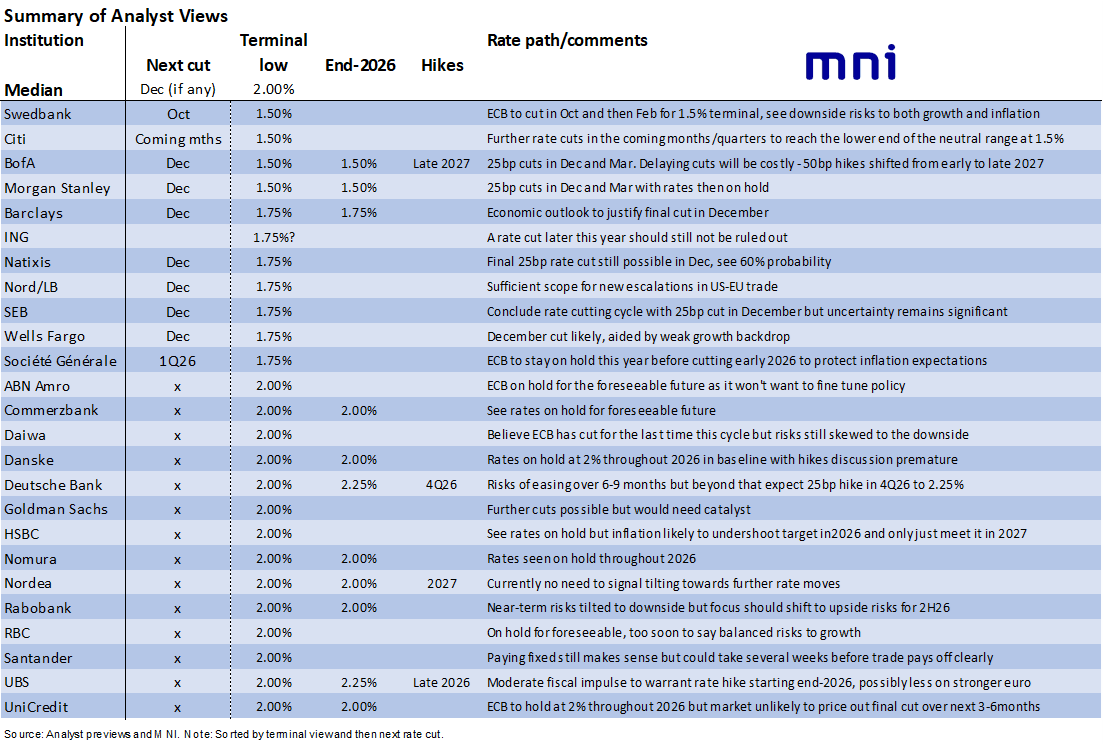

ECB: Analysts' EUR STIR Views Ahead Of Thursday’s Decision

Summarising some select EUR STIR views ahead of Thursday’s decision:

- Bank of America maintain their “received Oct ECB €str recommendation (Entry 1.765, target 1.565, current 1.905)". Even though they "see little chance of a rate cut by October given the lack of data between the two meetings, given only 2 bp are priced, we view the trade at this stage as a tail risk hedge”

- RBC believe that if the ECB will remain on hold going forward, it “makes sense to take short volatility positions on near-term Euribor options, for example being short straddles”. They note that “these positions are short gamma and short vega and hold positive carry since the term structure of Euribor option volatility is still upward sloping”.

- Morgan Stanley “find it unlikely that the ECB meeting will result in a hawkish enough outcome to further challenge the easing currently priced in”. They think that “short-dated rates have room to reprice lower” and “continue to favour Oct-Dec flattening given the low implied probability of a 25bp cut for December”.

- Santander instead believe “the risk bias across the EUR curve remains tilted to the upside, though it may take until later in the year for materially higher rates to materialise. Paying fixed in the front end still makes sense, but it will likely take several weeks before the trade pays off clearly.”

- MNI's full ECB preview is here.

EUROPE ISSUANCE UPDATE:

Luxembourg Syndication: Final terms

- E2.5bln of the new 10-Year Sep-35 LGB (MNI pencilled in a transaction size of E1.00-1.75bln so this is larger than we expected). Spread set at MS+30bp (guidance was MS+35bps area then revised to MS+32bps area), books in excess of E18bln.

UK auction results

- Strong gilt auction with the largest volume of bids for the 4.00% Oct-31 gilt since that issue was launched (even thought the prior auction was larger) and seeing a strong bid-to-cover of 3.27x.

- The LAP was above the level seen in the last 40 minutes of the auction window.

- No wider impact on gilt futures, however.

- GBP4bln of the 4.00% Oct-31 Gilt. Avg yield 4.208% (bid-to-cover 3.27x, tail 0.2bp).

Germany auction results

- Weak demand on German primary also filtering through to the 15-year segment here, with very poor demand metrics of 1.28x bid-to-cover / 0.77x bid-to-issue for the 4.75% Jul-40 Bund. That bid-to-issue was the lowest on a German auction since October 2022.

- The low price achieved at the auction (121.22) was also below the secondary market mid price seen right before the cutoff (121.264).

- The line is seeing some weakness, with its price dropping to 121.188 at time of writing - but remaining above the intraday lows of 121.116 seen shortly after the cash open. Bund futures see some marginal weakness, if any.

- The 2.60% May-41 Bund auction fared better, meanwhile, with a bid-to-cover of 2.25x and a bid-to-offer of 1.75x, and the auction low price above the secondary market mid price.

- E1bln (E603mln allotted) of the 4.75% Jul-40 Bund. Avg yield 2.96% (bid-to-offer 0.77x; bid-to-cover 1.28x).

- E1.5bln (E1.167bln allotted) of the 2.60% May-41 Bund. Avg yield 3.03% (bid-to-offer 1.75x; bid-to-cover 2.25x).

Portugal auction results

- E621mln of the 3.00% Jun-35 OT. Avg yield 3.059% (bid-to-cover 1.57x).

- E510mln of the 1.15% Apr-42 OT. Avg yield 3.637% (bid-to-cover 1.74x).

FOREX: Risk-Off Phase Short-lived Despite Higher Geopolitical Tensions

- Incursion of Russian drones into Polish airspace have dominated headline flow and market sentiment so far Wednesday. Poland's government have triggered NATO's Article 4 in response - meaning NATO consultations are set to get underway to assess the risks and threats after Poland shot down several drones.

- Given this morning's incursion represents the most serious breach of air defences since the beginning of the Ukraine war, risk sentiment dipped through the European open - albeit only briefly. EUR/USD edged through the overnight lows of 1.1690 as the USD rallied - although haven currencies (JPY, CHF) saw only minimal gains. With Article 4 triggered - the path for de-escalation is relatively clear - allowing markets to correct back to neutral levels.

- That said, oil-tied FX are on the front-foot as WTI and Brent crude futures correct higher on geopolitical risk. This is compounding strength in the NOK on the back of the higher-than-expected underlying Norwegian CPI print (3.1% Y/Y vs. Exp. 2.9%). As a result, EUR/NOK trades heavy and clear of the September lows. The cross has shown through 61.8% retracement for the upleg posted off the June low, opening next support into 11.5416.

- PPI data marks the first inflation salvo this week, with markets expecting PPI to slow on a monthly basis, but hold first on a Y/Y, final demand basis. The PPI release may take on greater importance than usual given it comes ahead of tomorrow's CPI - both of which feed directly in to the Fed's PCE inflation gauge and could prove decisive for the September FOMC meeting and the scale of any potential easing. Both the Fed and ECB remain inside their media blackout periods, meaning we're unlikely to get much policy-relevant commentary following the PPI print.

OPTIONS: Expiries for Sep10 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1600(E1.0bln), $1.1650(E697mln), $1.1675-80(E963mln), $1.1780(E593mln), $1.1800(E541mln)

- USD/JPY: Y145.25($566mln), Y145.50($575mln), Y145.90-10($1.2bln), Y146.40-50($1.4bln), Y147.75-85($949mln)

- AUD/USD: $0.6535-50(A$1.2bln)

- NZD/USD: $0.5850-70(N$540mln)

EQUITIES: Corrective Bear Cycle in Eurostoxx 50 Futures Remains in Play

- A corrective bear cycle in Eurostoxx 50 futures remains in play. Recent weakness resulted in a breach of 5369.17, the 50-day EMA. The clear break of this average strengthens a short-term bearish threat and signals scope for a deeper retracement towards 5166.00, the Aug 1 low and a key support. On the upside, the contract has recovered above the 20-day EMA - a bullish development. A stronger reversal would open 5445.00, the Aug 26 high.

- A bull cycle in S&P E-Minis remains intact and the latest pullback has once again proved to be a shallow correction. The contract traded to a fresh cycle high last week, breaching the Aug 28 high of 6523.00. This confirmed a resumption of the uptrend and maintains the price sequence of higher highs and higher lows. Sights are on 6543.75 next, a Fibonacci projection. Initial support to watch is 6456.35, the 20-day EMA.

COMMODITIES: WTI Futures Extend Recovery Off Last Week's Lows

- The trend condition in WTI futures is unchanged - a bear cycle remains intact. The pullback from the Sep 2 high highlights a possible reversal and the end of the corrective phase. Initial resistance to watch is $66.03, the Sep 2 high. Key short-term resistance has been defined at $69.36, the Jul 30 high. A stronger resumption of weakness would pave the way for a move towards $57.71, the May 30 low.

- Gold remains in a clear bull cycle and last week’s gains plus this week’s bullish start to the week, reinforce current conditions. The yellow metal has traded to a fresh all-time high. The break also confirms a resumption of the primary uptrend and an extension of the sequence of higher highs and higher lows. The next objective is $3674.8, a Fibonacci projection. Initial firm support lies at $3474.7, the 20-day EMA.

| Date | GMT/Local | Impact | Country | Event |

| 10/09/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 10/09/2025 | 1145/1345 | SNB's Schlegel on Central Bank Communication in Vezia | ||

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1230/0830 | *** | PPI | |

| 10/09/2025 | 1400/1000 | ** | Wholesale Trade | |

| 10/09/2025 | 1400/1000 | ** | Wholesale Trade | |

| 10/09/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 10/09/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 10/09/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 11/09/2025 | - | European Central Bank Meeting | ||

| 11/09/2025 | 0600/0800 | *** | Final Inflation Report | |

| 11/09/2025 | 0600/0800 | *** | Final Inflation Report | |

| 11/09/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 11/09/2025 | - | *** | Money Supply | |

| 11/09/2025 | - | *** | New Loans | |

| 11/09/2025 | - | *** | Social Financing | |

| 11/09/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 11/09/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 11/09/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 11/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 11/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 11/09/2025 | 1230/0830 | * | Household debt-to-income | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1230/0830 | *** | CPI | |

| 11/09/2025 | 1245/1445 | ECB Press Conference | ||

| 11/09/2025 | 1415/1615 | ECB Lagarde Presents Rate Decision on ECB Podcast | ||

| 11/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 11/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 11/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 11/09/2025 | 1700/1300 | *** | US Treasury Auction Result for 30 Year Bond | |

| 11/09/2025 | 1800/1400 | ** | Treasury Budget |