MNI EUROPEAN OPEN: Waller Gets Yields Lower In Asia

EXECUTIVE SUMMARY

- FED’S WALLER ARGUES FOR JULY CUT; SUPPORTS MORE THIS YEAR - MNI

- FED’S POWELL RESPONDS TO WHITE HOUSE ON FED HEADQUARTERS RENOVATION - RTRS

- TRUMP AI GUIDELINES EPXTECED TO LOOSEN RULES, PURSUE ENERGY - BBG

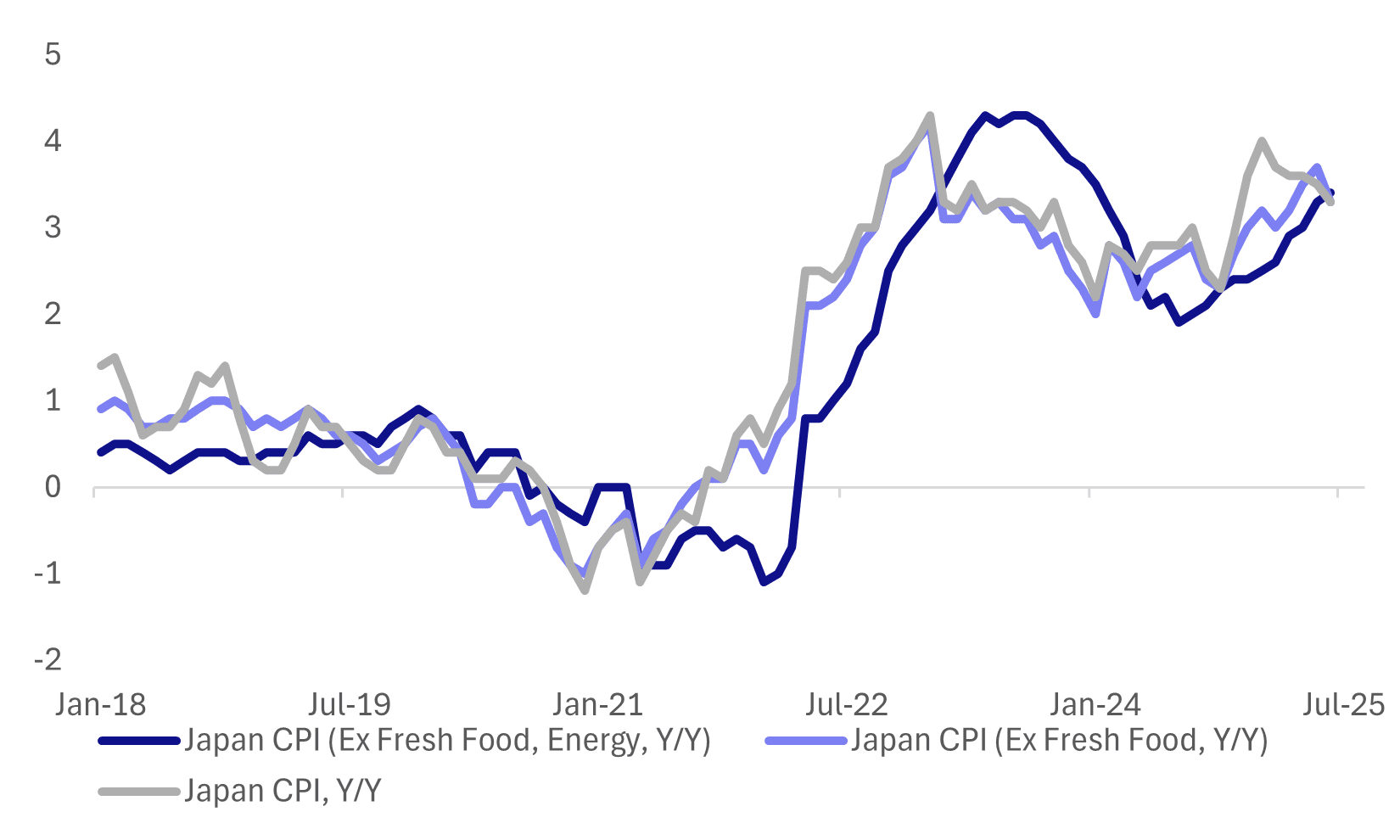

- JAPAN’S JUNE CORE CPI REACHES 3.3% - MNI BRIEF

Fig 1: Japan CPI Y/Y Trends

Source: Bloomberg Finance L.P./MNI

UK

UK/US (BBG): “Prime Minister Keir Starmer hinted the UK may join Germany in purchasing weapons from the US to give to Ukraine, as western allies seek to shore up the conflict-torn nation’s defenses in its war against Russian invaders.”

EU

SPAIN (BBG): “The US should pull back on sharing intelligence with Spain, given that the country allegedly relies on Chinese network vendor Huawei Technologies Co. to support its wiretap system, according to the heads of the House and Senate intelligence committees.”

US

FED (MNI): Federal Reserve Governor Chris Waller said Thursday he supports cutting U.S. interest rates by 25 basis points at the FOMC meeting later this month, adding that if underlying inflation remains in check and the economy continues to grow slowly then he'd support more 25 basis point cuts later this year.

FED (RTRS): “Federal Reserve Chair Jerome Powell on Thursday responded to a Trump administration official's demands for information about cost overruns for a renovation project at the central bank's Washington headquarters campus, saying the project was large in scope and involved a number of safety upgrades and hazardous materials removals.”

INFLATION (MNI BRIEF): Artificial intelligence is likely to boost productivity and could help the economy achieve higher growth while reducing inflationary pressures over the long run, Federal Reserve Governor Lisa Cook said Thursday, calling the technology transformative for research and policymaking.

TARIFFS (MNI BRIEF): Federal Reserve Bank of San Francisco President Mary Daly said Thursday firms in her district are now "cautiously optimistic" about their ability to grow in spite of the material hike in tariffs this year, rather than waiting to see how trade policy will settle.

FED (MNI BRIEF): The Director of the Office of Management and Budget, Russell Vought, said Thursday President Donald Trump is unlikely to try to fire Federal Reserve Chair Jerome Powell.

AI (BBG): "President Donald Trump is expected to announce policy guidelines for artificial intelligence that will call for easing regulation and expanding energy sources for data centers, while urging Congress to consider federal legislation to preempt state oversight of the emerging technology."

STABLECOIN (MNI INTERVIEW): The rapid expansion of stablecoins to trillion-dollar levels by 2030 could prove to be a significant new source of Treasury funding while complicating the jobs of central banks, former Office of the Comptroller of the Currency economist Rashad Ahmed told MNI.

OTHER

CANADA (MNI INTERVIEW): Growing Canadian exports this year remains possible even with the U.S. trade war as new oil and gas terminals open up overseas markets and other firms take advantage of tariff rates still below global competitors, the government trade bank’s deputy chief economist told MNI.

JAPAN (MNI BRIEF): Japan's annual core consumer inflation rate decelerated to 3.3% y/y in June, from May’s 3.7%, marking 39 consecutive months above the Bank of Japan’s 2% inflation target, data released by the Ministry of Internal Affairs and Communications showed on Friday.

MIDDLE EAST (BBG): “Deadly sectarian clashes in Syria eased Thursday, after a ceasefire was announced between groups fighting in the Druze-majority southern province and Israel signaled air strikes over recent days were suspended.”

BRAZIL (BBG): "“We sent a negotiation proposal to the US in May, we expected a response, and what we received was unacceptable blackmail in the form of threats to Brazilian institutions,” President Luiz Inácio Lula da Silva said on Thursday night in a TV and radio address to the nation."

CHINA

US/CHINA (BBG): “The US Commerce Department will impose preliminary anti-dumping duties of 93.5% on imports of Chinese graphite, a key battery component, after concluding the materials had been unfairly subsidized.”

EMERGING INDUSTRIES (BBG): "President Xi Jinping questioned the need for local governments across China to crowd into the same emerging industries, a rare rebuke that reflects growing concerns about deflation at home and trade tensions abroad."

MNI: PBOC Net Injects CNY102.8 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY187.5 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY102.8 billion after offsetting the maturity of CNY84.7 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4524% at 09:25 am local time from the close of 1.5223% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 49 on Thursday, compared with the close of 52 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1498 Fri; +1.34% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1498 on Friday, compared with 7.1461 set on Thursday. The fixing was estimated at 7.1734 by Bloomberg survey today.

MARKET DATA

JAPAN JUNE NATL CPI Y?Y 3.3%; MEDIAN 3.3%; PRIOR 3.5%

JAPAN JUNE NATL CPI EX FRESH FOOD Y/Y 3.3%; MEDIAN 3.4%; PRIOR 3.7%

JAPAN JUNE NATL CPI EX FRESH FOOD, ENERGY Y/Y 3.4%; MEDIAN 3.3%; PRIOR 3.3%

MARKETS

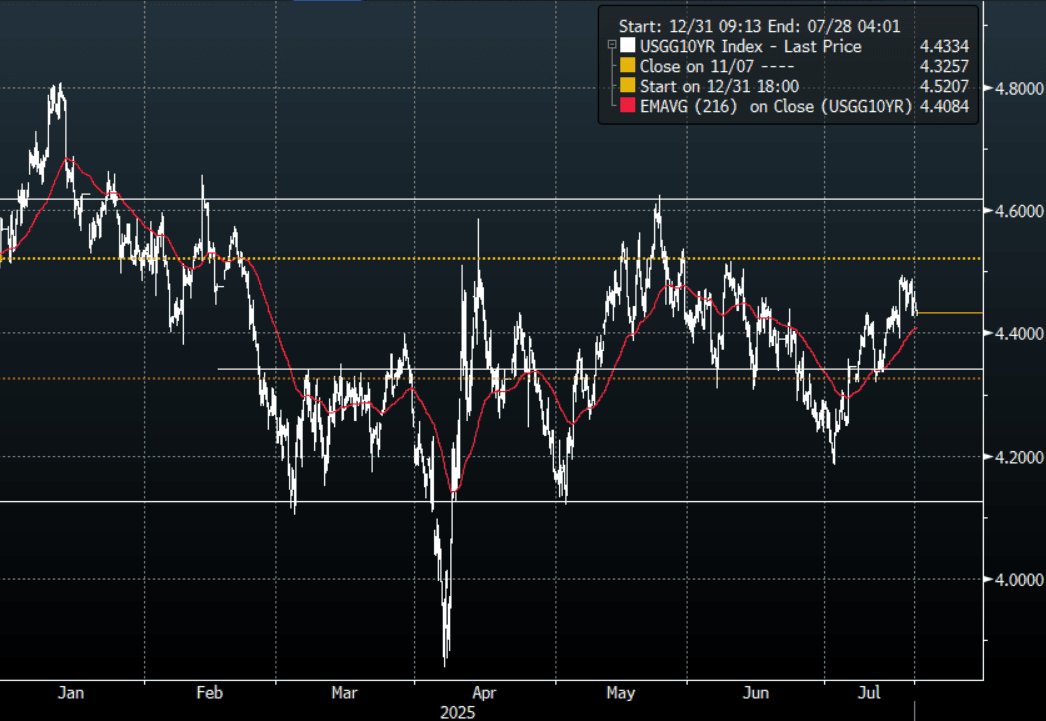

US TSYS: Asia Wrap - Waller Gets Yields Lower In Asia

The TYU5 range has been 110-19 to 110-24 during the Asia-Pacific session. It last changed hands at 110-23, up 0-06+ from the previous close.

- The US 2-year yield has moved lower trading around 3.887%, down 0.02 from its close.

- The US 10-year yield has moved lower trading around 4.433%, down 0.02 from its close.

- The 10-year yield broke above 4.45% in response to the CPI Data, this implies price is likely to turn its focus back to 4.65% and could see further paring back of longs. Support is now back towards the 4.35/40% area which has been the pivot in the larger 4.10% - 4.65% range.

- Nick Timiraos on X: “Waller removes any doubt: He'll vote for a July cut. The opening line of the speech gets to the point: My purpose this evening is to explain why I believe that the FOMC should reduce our policy rate by 25 basis points at our next meeting. Waller arrives at this out-of-consensus position (relative to his colleagues) because he thinks the Fed should look through tariffs and move rates closer to neutral. “We should not wait until the labor market deteriorates before we cut the policy rate.”

- “Torsten Slok, chief economist at Apollo Management, believes "The market is way, way too eager to price in cuts," and sees one rate cut by the end of 2025, while the market is leaning to two cuts.” - BBG

- (Bloomberg) -- “Fed Chair Jerome Powell pushed back against criticism over a $2.5 billion renovation project at its headquarters in Washington, saying the bank takes its responsibility to be good stewards of public resources seriously.”

Data/Events: Housing Starts, U. of Mich. Sentiment survey

Fig 1: 10-Year US Yield Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Bull-Flattener Ahead Of Upper House Elections

JGB futures are stronger and at Tokyo session highs, +25 compared to settlement levels.

- (Bloomberg) - "BOJ's Eye Will Be on Heat Hidden in Cooler CPI. Japan's June CPI report reveals mixed inflation dynamics, with softer energy costs tempering headline and core price gains. Firms continued to pass on higher costs of labour as well as rice to consumers in a variety of areas, nudging up the gauge that excludes fresh food and energy. The Bank of Japan will focus on the underlying strength, a sign the wage-price cycle is gaining traction and moving inflation closer to its 2% target."

- (Bloomberg) - "Polls for Japan's July 20 upper house election suggest Prime Minister Shigeru Ishiba's Liberal Democratic Party and its coalition partner Komeito risk losing their majority in the chamber. That outcome would leave Ishiba heading a weakened coalition - unable to drive key legislation or, in the worst case, stepping down as leader."

- Cash US tsys are ~1bp richer in today's Asia-Pac session.

- Cash JGBs are 2-5bps richer across benchmarks, with a flatter curve. The benchmark 10-year yield is 3.4bps lower at 1.534% versus the cycle high of 1.60%.

- Swap rates are 1-7bps lower, with longer-dated swap spreads tighter.

- On Monday, the local calendar will be out for the Marine Day holiday.

AUSSIE BONDS: Slightly Richer But Off Bests, RBA Minutes On Tuesday

ACGBs (YM +1.0 & XM +0.5) are slightly stronger but well off Sydney session bests.

- Cash US tsys are 1-2bps richer in today’s Asia-Pac session.

- Nick Timiraos on X: "Waller removes any doubt: He'll vote for a July cut. The opening line of the speech gets to the point: My purpose this evening is to explain why I believe that the FOMC should reduce our policy rate by 25 basis points at our next meeting. Waller arrives at this out-of-consensus position (relative to his colleagues) because he thinks the Fed should look through tariffs and move rates closer to neutral."

- Cash ACGBs are 1-2bps richer with the AU-US 10-year yield differential at -10bps versus -13bps early in the session.

- The bills strip has seen a modest bull-flattener, with pricing flat to +1.

- RBA-dated OIS pricing is softer across meetings today. A 25bp rate cut in August is given a 99% probability, with a cumulative 65bps of easing priced by year-end.

- On Monday, the local calendar will be empty, ahead of the RBA Minutes for the July Meeting on Tuesday.

- A new 21 October 2036 Treasury Bond is planned to be issued via syndication in the week beginning 21 July 2025 (subject to market conditions).

BONDS: NZGBS: Closed On A Weak Note, Underperforms $-Bloc, Q2 CPI On Monday

NZGBs closed modestly cheaper, with benchmark yields 2-3bps higher, after trading in narrow ranges. Cash US tsys are ~2bps richer in today’s Asia-Pac session.

- Accordingly, the NZ 10-year has underperformed its $-bloc counterparts, with the NZ-US and NZ-AU yield differentials 6bps and 4bps wider, respectively.

- June Credit Card Spending falls 1.1% m/m, +0.9% y/y.

- Swap rates closed 1-2bps higher, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed 1-4bps firmer across meetings. 16bps of easing is priced for August, with a cumulative 31bps by November 2025.

- On Monday, the local calendar will see Q2 CPI data, with consensus expecting +0.7% q/q and 2.8% y/y.

- Westpac: "We estimate that New Zealand consumer prices rose by 0.6% in the June quarter. The annual inflation rate is expected to rise to 2.8% (up from 2.5% in the year to March). Price pressures are easing in interest rate sensitive areas of the economy, like in the services sector and discretionary spending categories. However, increases in food prices and firmness in administered prices are pushing overall inflation higher.”

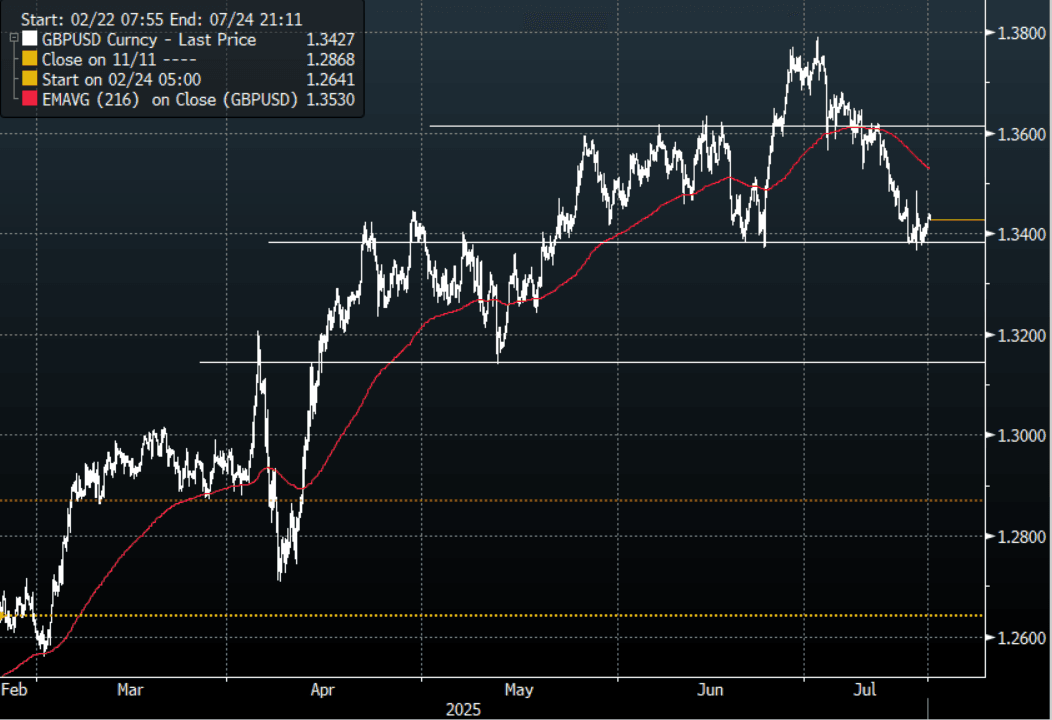

FOREX: Asia FX Wrap - BBDXY Drifts Lower On Waller Comments

The BBDXY has had a range of 1205.49 - 1207.31 in the Asia-Pac session, it is currently trading around 1206, -0.10%. The USD has drifted lower in our session and as we head into the weekend the market will be wary of any negative Powell news to potentially come out so it is tough for the market to get long of USD’s with this risk over its head. (Bloomberg) - “Well, evidence for the whole “sell America” theme weakened a bit from the latest TIC data, which showed a huge net inflow of $259.4 billion into US long-term assets in May...the biggest net capital inflow since March of 2021. The buying was dominated by private sector names, and appetite was strong across assets, with inflows of more than $100 billion into both Treasuries and equities.”

- EUR/USD - Asian range 1.1592 - 1.1634, Asia is currently trading 1.1620. The pair is testing its first support around the 1.1600 area. The price still looks a little stretched in the short term and is vulnerable to any correction in the USD, first support around 1.1600 then more importantly the 1.1450 area.

- GBP/USD - Asian range 1.3411 - 1.3441, Asia is currently dealing around 1.3425. The support around 1.3350/1.3400 proved to be solid first up. Bounces back towards 1.3500/1.3550 should now see offers first up.

- USD/CNH - Asian range 7.1805 - 7.1856, the USD/CNY fix printed 7.1498, Asia is currently dealing around 7.1850. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3335, US 10-Year 4.43%, BBDXY 1206, Crude oil $67.70

- Data/Events : EZ Current Account & Construction Output, Germany PPI, Spain Trade Balance, Italy Current Account

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

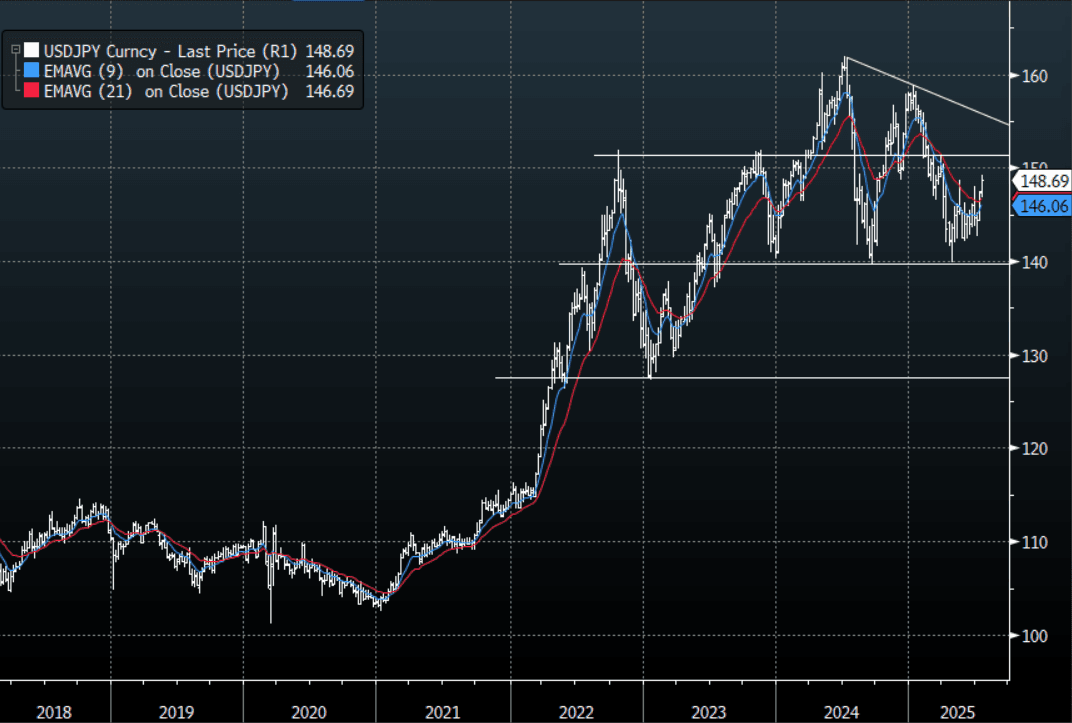

JPY: Asia Wrap - USD/JPY Not Letting Up, Eyes 150/151

The Asia-Pac USD/JPY range has been 148.29 - 148.73, Asia is currently trading around 148.70, +0.07%. This pair is just not backing off and the price action suggests the JPY longs could face further angst as a test of the 150.00/151.00 area is looking likely unless something changes(Powell being removed ?). Support should now be seen back towards 147.00 first up, then more importantly the 145.00 area. A close back above 151.00 would be very worrying for USD/JPY and it was interesting to see Japanese Officials rattling the cage yesterday regarding the speed of the move.

- (Bloomberg) - “BOJ’s Eye Will Be on Heat Hidden in Cooler CPI. Japan’s June CPI report reveals mixed inflation dynamics, with softer energy costs tempering headline and core price gains. Firms continued to pass on higher costs of labor as well as rice to consumers in a variety of areas, nudging up the gauge that excludes fresh food and energy. The Bank of Japan will focus on the underlying strength, a sign the wage-price cycle is gaining traction and moving inflation closer to its 2% target.”

- (Bloomberg) - “Polls for Japan’s July 20 upper house election suggest Prime Minister Shigeru Ishiba’s Liberal Democratic Party and its coalition partner Komeito risk losing their majority in the chamber. That outcome would leave Ishiba heading a weakened coalition — unable to drive key legislation or, in the worst case, stepping down as leader.”

- Should Prime Minister Shigeru Ishiba’s ruling coalition lose its majority this could see further JPY weakness in response.

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($1.25b).Upcoming Close Strikes : 147.00($1.29b July 22), 145.50($1.29b July 21) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

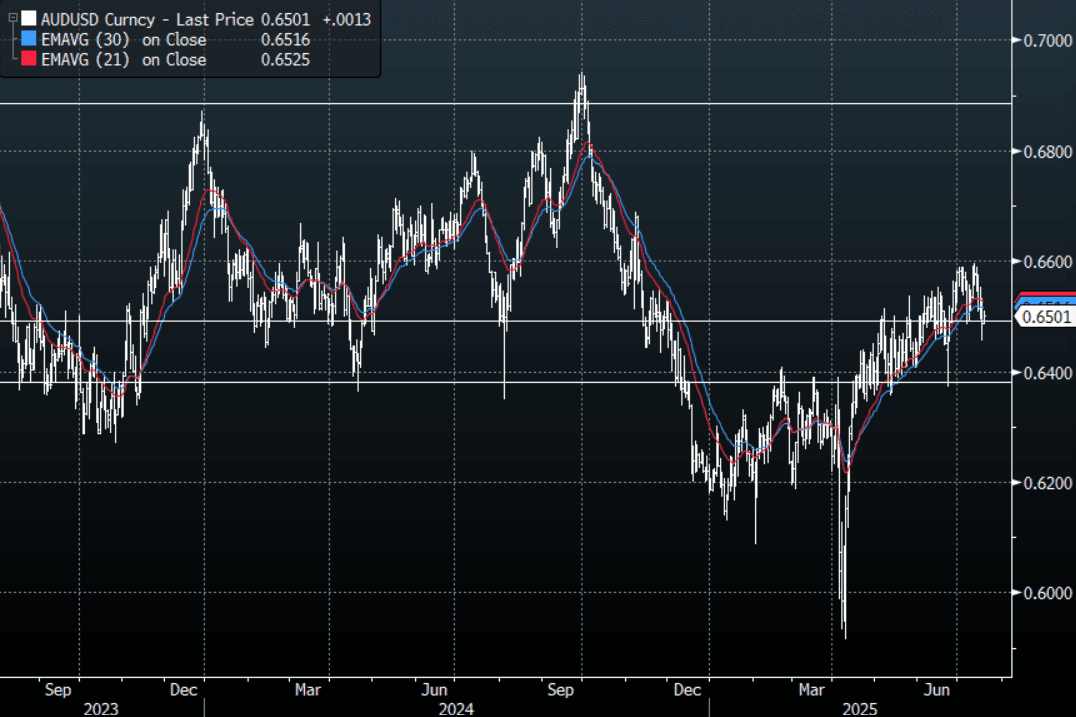

AUD: Asia Wrap - AUD/USD Drifts Back Above 0.6500 As The USD Recovery Stalls

The AUD/USD has had a range of 0.6484 - 0.6511 in the Asia- Pac session, it is currently trading around 0.6505, +0.25%. Decent demand was seen towards the 0.6450 area and we opened in Asia back towards the 0.6500 area once more. Dovish comments this morning by Waller have seen US yields and the USD move lower. This has seen AUD/USD move back above 0.6500 confirming the false break lower overnight, expect offers to reemerge back towards 0.6525/50, but the big USD is going to be the one that ultimately determines where this pair ends up. The market will be wary of any negative Powell to potentially come over the weekend so it is tough for the market to get long of USD’s with this risk.

- Nick Timiraos on X: “Waller removes any doubt: He'll vote for a July cut. The opening line of the speech gets to the point: My purpose this evening is to explain why I believe that the FOMC should reduce our policy rate by 25 basis points at our next meeting. Waller arrives at this out-of-consensus position (relative to his colleagues) because he thinks the Fed should look through tariffs and move rates closer to neutral. “We should not wait until the labor market deteriorates before we cut the policy rate.”

- (Bloomberg) - “ BHP has just released its latest production report. The world’s biggest miner said output of key revenue-earner iron ore rose 2% in the fourth quarter, compared with the year before. Copper output also rose 2%.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6480(AUD916m), 0.6460(AUD395m), 0.6500(AUD375m) . Upcoming Close Strikes : 0.6500(AUD739m July 21), 0.6600(AUD725m July 21) - BBG

- AUD/JPY - Today's range 96.34 - 96.74, it is trading currently around 96.65, +0.30%. The pair found good demand back towards the breakout area around 96.00, and this will need to hold to build a platform from which to probe higher again. The positive risk backdrop is providing tailwinds.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

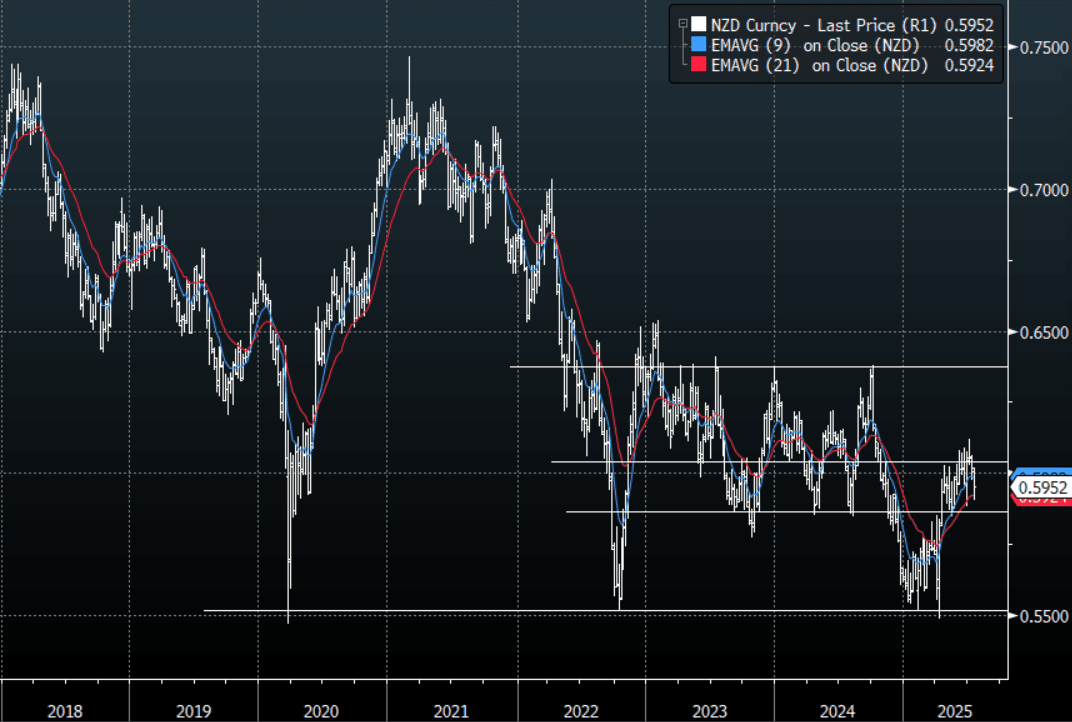

NZD: Asia Wrap - NZD/USD Bounces Off 0.5900, Trying To Consolidate Above Support

The NZD/USD had a range of 0.5928 - 0.5964 in the Asia-Pac session, going into the London open trading around 0.5955, +0.40%. Dovish comments this morning by Waller have seen US yields and the USD move lower. Decent demand was seen towards the 0.5900 area and we have managed to bounce off this support in our session. This 0.5850/0.5900 area is important support if the pair is to eventually push higher, a weekly close below 0.5850 would turn the picture quite bearish. See Weekly graph below.

- “New Zealand June Credit Card Spending Falls 1.1% M/m, RBNZ Says.” - BBG

- (Bloomberg) -- “Bank of America says the dollar could be poised for a summer rally if the Federal Reserve keeps interest rates steady and institutional investors slow the pace of dollar sales. “We are bearish USD over the medium-term but risk of a summer rally has risen,” FX strategists led by Adarsh Sinha write in a note.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5932(NZD317m). Upcoming Close Strikes : 0.5905(NZD380m July 21), 0.5750(NZD348m July 23) - BBG

- CFTC Data shows Asset Managers added slightly to their newly built longs in NZD +9229, the Leveraged community added slightly to their shorts last week -8654

- AUD/NZD range for the session has been 1.0916 - 1.0944, currently trading 1.0920. The cross has moved lower in response to the AU Employment data. Dips back to 1.0850/1.0900 should still find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Most Markets Higher, Taiwan Outperforms, Japan And Korea Lag

The general backdrop for Asia Pac equities has mostly been positive in the first part of Friday trade. This follows the firm gains for US and EU markets on Thursday, with US markets reaching fresh record highs. Futures are a touch higher so far today.

- Japan markets aren't tracking higher, with the Topix and the Nikkei 225 down marginally. We have the Japan upper house elections this weekend, which may be creating some caution. Opinion polls have suggested the ruling LDP may struggle to hold a majority. Longer dated JGB yields are lower though, while USD/JPY is little changed.

- Taiwan's market is outperforming, up around 1% at this stage. This puts the Taiex index to fresh multi month highs. This follows the solid TSMC results late yesterday, which boosted broader sentiment in the AI/chip space.

- South Korea's market is struggling though, last down around 0.50%. The Kospi hasn't been able to hold above 3200 recently, potentially waiting for the next reform positive catalyst. This has followed a very strong run higher though since late May.

- China and Hong Kong markets are tracking higher, the HSI up around 0.70%, the CSI 300 +0.50% firmer.

- The ASX 200 is up around 1.3% in Australia, which also puts this index at fresh record highs. BHP results aided sentiment in the resource/material space.

- In SEA, Indonesian markets continue to rally, last up around 1.3%, while it has been a quieter so far for the Thailand SET, little changed after yesterday's bumper 3.5% rally. Optimism around a more dovish BoT (with a new Governor coming in a few months), while offshore inflows have also returned to this market.

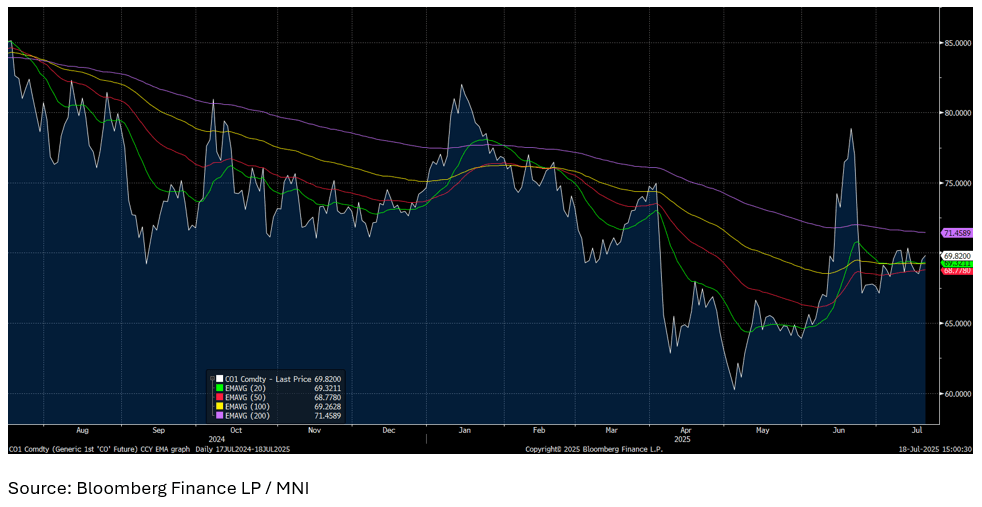

Oil Heading for Weekly Fall on Supply Concerns

- Oil has clawed back some gains in the Asia trading day but if the current trajectory remains, is on track for a weekly loss.

- Oil had a strong night on indications that there is the potential for short term dynamics to increase demand.

- US crude inventory data declined last week at a time when the White House seems adamant that the US stockpile needs to be replenished.

- Additionally, news from Northern Iraq saw drone attacks on Kurdistan oil production which has interrupted supply by up to 200,000 bbl a day it is estimated.

- Iraq approved a plan for its semi-autonomous Kurdish region to transfer oil to Baghdad, a key step toward resuming exports that have been halted for more than two years. The Kurdistan Regional Government will supply Iraq’s state oil marketer SOMO at least 230,000 barrels a day for export, and Baghdad will release funds for salaries of Kurdistan government employees.

- Currently up +0.44% at US$67.84 bbl, WTI remains lower by -0.90% for the week.

- Brent has gained +0.47% in the Asia trading day, yet remains lower by -0.74% week to date.

- Brent sits between the converged 20-day EMA of $69.32 and below the 200-day EMA of $71.45

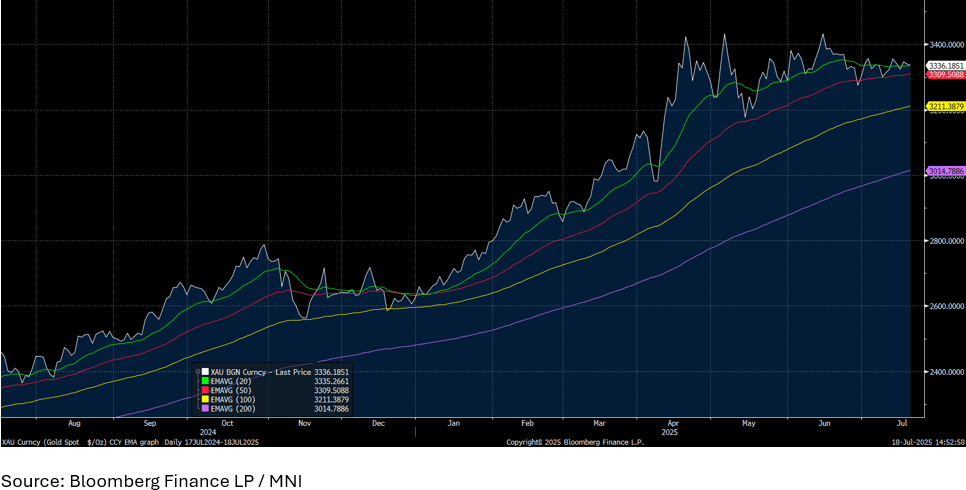

Gold Down Modestly, Set for Weekly Fall

- Gold is down -0.15% at US$3,335.50 in the Asia trading day.

- At these levels, gold remains just $96 off the June high of $3,432.34.

- For the week, gold has lost ground by -0.61%, for it's first weekly loss for the month should the European and US sessions follow suit.

- Gold is highly correlated to US interest rate moves and the data out this week on the US economy has not cemented the idea of a near term interest rate cut.

- Gold is up over 26% year to date on safe haven appeal which this week has been less pronounced.

- Should the ongoing spat between the US President and the the FED Chairman intensify, gold's status could be amplified in the near term.

- Gold remains in line with the 20-day EMA of $3335.25.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 18/07/2025 | 0600/0800 | ** | PPI | |

| 18/07/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/07/2025 | 0900/1100 | ** | Construction Production | |

| 18/07/2025 | - | ECB Cipollone At G20 Meeting | ||

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1230/0830 | *** | Housing Starts | |

| 18/07/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 18/07/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 18/07/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |