FOREX: Asia FX Wrap - BBDXY Drifts Lower On Waller Comments

The BBDXY has had a range of 1205.49 - 1207.31 in the Asia-Pac session, it is currently trading around 1206, -0.10%. The USD has drifted lower in our session and as we head into the weekend the market will be wary of any negative Powell news to potentially come out so it is tough for the market to get long of USD’s with this risk over its head. (Bloomberg) - “Well, evidence for the whole “sell America” theme weakened a bit from the latest TIC data, which showed a huge net inflow of $259.4 billion into US long-term assets in May...the biggest net capital inflow since March of 2021. The buying was dominated by private sector names, and appetite was strong across assets, with inflows of more than $100 billion into both Treasuries and equities.”

- EUR/USD - Asian range 1.1592 - 1.1634, Asia is currently trading 1.1620. The pair is testing its first support around the 1.1600 area. The price still looks a little stretched in the short term and is vulnerable to any correction in the USD, first support around 1.1600 then more importantly the 1.1450 area.

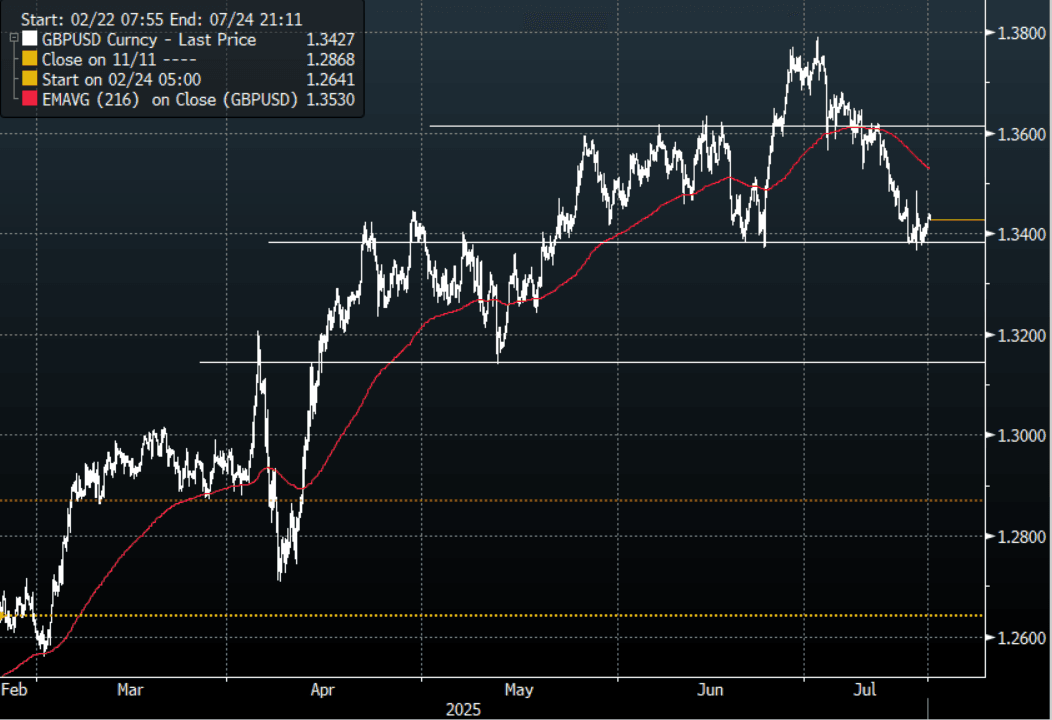

- GBP/USD - Asian range 1.3411 - 1.3441, Asia is currently dealing around 1.3425. The support around 1.3350/1.3400 proved to be solid first up. Bounces back towards 1.3500/1.3550 should now see offers first up.

- USD/CNH - Asian range 7.1805 - 7.1856, the USD/CNY fix printed 7.1498, Asia is currently dealing around 7.1850. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.15%, Gold $3335, US 10-Year 4.43%, BBDXY 1206, Crude oil $67.70

- Data/Events : EZ Current Account & Construction Output, Germany PPI, Spain Trade Balance, Italy Current Account

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: Hang Seng Drags Others Lower

The Hang Seng was one of the worst regional performers today, weighing heavy on other major bourses. As escalating Middle East tensions dominate this week's Federal Reserve meeting has markets sidelined to see if the FED will alter the direction for US interest rates.

The Middle East tensions are driving oil prices higher raising concerns as to the return of inflation as a catalyst for interest rates in the region.

- China's Hang Seng is down -1.15% and is down -2.75% over the last five days of trading. This dragged the CSI 300 with it, albeit marginally, down -0.07%, the Shanghai Comp was softer by -0.20% and the Shenzhen Comp down -0.36%

- The KOSPI's good run continued and is up +0.45% today and approaching a +2.00% gain over the last week.

- The FTSE Malay KLCI barely moved today and is where it started the trading day despite the BNM governor's positive comments about the economy.

- The Jakarta Composite fell -0.54%, taking back yesterday's gains.

- The FTSE Straits Times in Singapore fell -0.33% and the PSEi in the Philippines fell -0.10%

- The NIFTY 50 is up +0.20% so far today, looking to recover yesterday's losses of -0.37%

AUSSIE BONDS: Subdued Session Ahead Of FOMC Announcement

ACGBs (YM +1.0 & XM +1.0) sit marginally stronger on a subdued pre-FOMC session.

- Cash US tsys are slightly cheaper ahead of today's FOMC Decision including a Summary of Economic Projections (Dots). The June FOMC meeting communications should reflect an increasingly patient attitude from May and certainly since March's projections.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at -16bps.

- The bills strip little changed with pricing flat to +2.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in July is given a 83% probability, with a cumulative 76bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- May jobs data are released tomorrow and Bloomberg consensus is expecting labour market tightness to continue, one of the reasons the RBA remains cautious regarding the monetary policy outlook.

- Consensus is forecasting a 21.2k increase in new jobs, close to the 3-month average of 23k, with the unemployment rate steady at 4.1%. In May the RBA projected 4.2% in Q2 and employment growth of 2.1% y/y. New jobs rose a stronger-than-expected 89k and 2.7% y/y in April.

- The AOFM plans to sell A$800mn of the 1.00% 21 December 2030 bond on Friday.

GOLD: Bullion Monitoring Fed & Middle East Developments

Gold prices range traded on Tuesday and that trend has continued in today’s APAC session as markets await the Fed decision later. They fell to $3370.75/oz but have rebounded to $3399.0 to be up 0.3% today supported by the softer US dollar (USD BBDXY -0.1%). Treasury yields are little changed. Bullion continues to be dependent on the Middle East too with any escalation driving safe-haven flows.

- Medium-term trend signals are bullish with moving average studies in a bull mode. Initial resistance is at $3451.3, 16 June high, while support is at $3340.2, 20-day EMA.

- Prospects of the US assisting Israel in its attacks on Iran have increased. President Trump has demanded that Iran surrender but said that they won’t assassinate the Ayatollah “for now” but his patience with Iran is “wearing thin”.

- Silver is 0.4% higher at $37.267 today to be up 13% this month. The intraday high of $37.282 is also the high for June. A bull wave persists and has broken above a number of resistance levels opening $37.478, March 2012 high.

- The Fed is widely expected to leave rates unchanged but the dot plot will be monitored closely (see MNI Fed Preview). Inflation and jobs data have yet to show an impact from tariffs but some activity/survey data have slowed. The Fed is likely to want more time to evaluate the impact and now oil prices are up over 20% this month, it will also monitor its impact on inflation if sustained. A prolonged hold would likely weigh on gold prices, depending on other events.

- There are also a number of ECB speakers including de Guindos, Elderson, Lane, Machado and Donnery and BoC’s Macklem appears. In terms of data, US May housing starts/permits, jobless claims, euro area May CPI and UK May CPI are released.