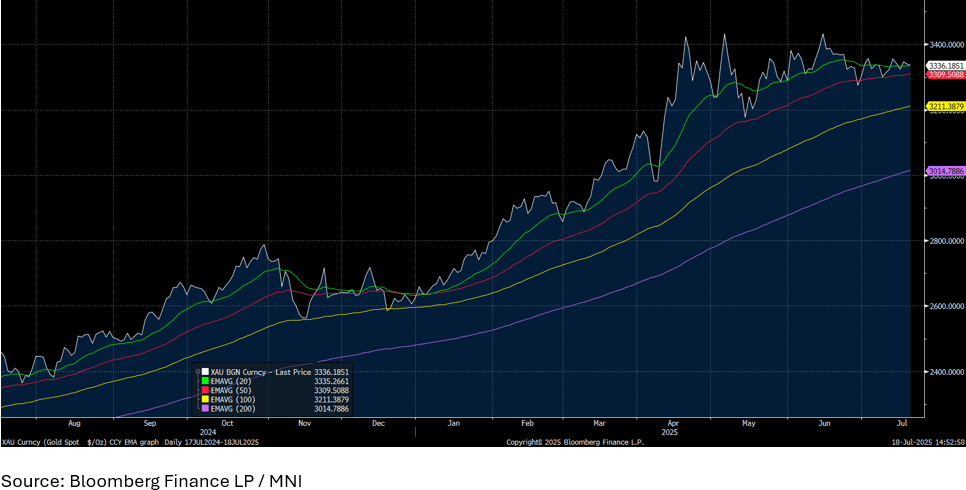

GOLD: Gold Down Modestly, Set for Weekly Fall

- Gold is down -0.15% at US$3,335.50 in the Asia trading day.

- At these levels, gold remains just $96 off the June high of $3,432.34.

- For the week, gold has lost ground by -0.61%, for it's first weekly loss for the month should the European and US sessions follow suit.

- Gold is highly correlated to US interest rate moves and the data out this week on the US economy has not cemented the idea of a near term interest rate cut.

- Gold is up over 26% year to date on safe haven appeal which this week has been less pronounced.

- Should the ongoing spat between the US President and the the FED Chairman intensify, gold's status could be amplified in the near term.

- Gold remains in line with the 20-day EMA of $3335.25.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Subdued Session Ahead Of FOMC Announcement

ACGBs (YM +1.0 & XM +1.0) sit marginally stronger on a subdued pre-FOMC session.

- Cash US tsys are slightly cheaper ahead of today's FOMC Decision including a Summary of Economic Projections (Dots). The June FOMC meeting communications should reflect an increasingly patient attitude from May and certainly since March's projections.

- Cash ACGBs are 1bp richer with the AU-US 10-year yield differential at -16bps.

- The bills strip little changed with pricing flat to +2.

- RBA-dated OIS pricing is little changed across meetings today. A 25bp rate cut in July is given a 83% probability, with a cumulative 76bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- May jobs data are released tomorrow and Bloomberg consensus is expecting labour market tightness to continue, one of the reasons the RBA remains cautious regarding the monetary policy outlook.

- Consensus is forecasting a 21.2k increase in new jobs, close to the 3-month average of 23k, with the unemployment rate steady at 4.1%. In May the RBA projected 4.2% in Q2 and employment growth of 2.1% y/y. New jobs rose a stronger-than-expected 89k and 2.7% y/y in April.

- The AOFM plans to sell A$800mn of the 1.00% 21 December 2030 bond on Friday.

GOLD: Bullion Monitoring Fed & Middle East Developments

Gold prices range traded on Tuesday and that trend has continued in today’s APAC session as markets await the Fed decision later. They fell to $3370.75/oz but have rebounded to $3399.0 to be up 0.3% today supported by the softer US dollar (USD BBDXY -0.1%). Treasury yields are little changed. Bullion continues to be dependent on the Middle East too with any escalation driving safe-haven flows.

- Medium-term trend signals are bullish with moving average studies in a bull mode. Initial resistance is at $3451.3, 16 June high, while support is at $3340.2, 20-day EMA.

- Prospects of the US assisting Israel in its attacks on Iran have increased. President Trump has demanded that Iran surrender but said that they won’t assassinate the Ayatollah “for now” but his patience with Iran is “wearing thin”.

- Silver is 0.4% higher at $37.267 today to be up 13% this month. The intraday high of $37.282 is also the high for June. A bull wave persists and has broken above a number of resistance levels opening $37.478, March 2012 high.

- The Fed is widely expected to leave rates unchanged but the dot plot will be monitored closely (see MNI Fed Preview). Inflation and jobs data have yet to show an impact from tariffs but some activity/survey data have slowed. The Fed is likely to want more time to evaluate the impact and now oil prices are up over 20% this month, it will also monitor its impact on inflation if sustained. A prolonged hold would likely weigh on gold prices, depending on other events.

- There are also a number of ECB speakers including de Guindos, Elderson, Lane, Machado and Donnery and BoC’s Macklem appears. In terms of data, US May housing starts/permits, jobless claims, euro area May CPI and UK May CPI are released.

JPY: Asia Wrap - USD/JPY In The Middle Of Its Recent Range, Can FOMC move it ?

The Asia-Pac USD/JPY range has been 144.93 - 145.44, Asia is currently trading around 144.93. USD/JPY has drifted lower in a muted Asian session, -0.25%. With the USD bouncing across the board as risk digests the potential of the US entering the fray in the middle east, the long JPY positions continue to be challenged. You would normally expect the JPY to outperform in this scenario but the outsized move in oil and a market that is already positioned very long is providing headwinds to the trade.

- Japan Data - Exports Dip Y/Y, Trade Surplus With US Narrows : Japan's May trade data was close to expectations, with export growth at -1.7%y/y, versus -3.7% forecast. The April outcome was +2.0%. On the import side, we were -7.7%y/y, against a -5.9% forecast (-2.2% was recorded for April). The trade deficit was -637.6bn, close to forecasts but wider than the -115.6bn print in April.

- "ISHIBA: HAD FRANK DISCUSSIONS ON TARIFFS WITH TRUMP, WILL WORK WITH US TOWARD A WIN-WIN DEAL" - BBG

- "ISHIBA: TARIFFS WILL HAVE BIG IMPACT ON COMPANIES, NAMELY AUTOS, SAYS JAPAN MUST NOT SACRIFICE NATIONAL INTEREST FOR DEAL" - BBG

- “ISHIBA: WAGE INCREASE MORE IMPORTANT THAN CUTTING SALES TAX, IMPACT OF CASH HANDOUT IS MORE IMMEDIATE THAN TAX CUT" - BBG

- USD/JPY found decent demand yesterday every time it had a look towards the 144.50 area yesterday. This price action stands out considering the risk backdrop and could hint at a market that is already very long JPY.

- Price is back in the middle of its recent 142.00 - 147.00 range and will need a break either side of that to get a clearer direction. Can FOMC be that catalyst ?

- The market is clearly looking for a move lower in USD/JPY but with positioning quite large now we have seen the risk of pullbacks increase. A break above 147.00 would be needed to challenge the conviction of any shorts.

- Options : Close significant option expiries for NY cut, based on DTCC data: 144.00($725m). Upcoming Close Strikes : 146.00($1.92b June 20), 143.00($925m June 20)

Fig 1 : USD/JPY Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P