MNI EUROPEAN OPEN: USD Up From Lows, Trump Hails Trade Talks

EXECUTIVE SUMMARY

- TRUMP HAILS ‘BIG PROGRESS’ AFTER JUMPING INTO JAPAN TARIFF TALKS - RTRS

- POWELL SAYS FED IN WAIT-AND-SEE MODE ON TRADE WORRIES - MNI

- FED'S POWELL - TARIFFS STYMIE DUAL MANDATE GOALS - MNI BRIEF

- BOJ UEDA, UNCERTAINTIES LINKED TO TARIFFS SURGE - MNI BRIEF

- FORMER RBNZ OFFICIAL DISCUSSES THE FUTURE OCR PATH - MNI INTERVIEW

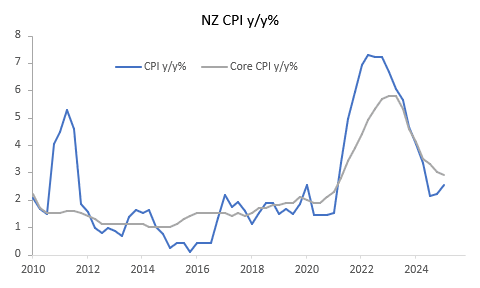

Fig 1: NZ Core Inflation Trending Lower

Source: MNI - Market News/Bloomberg/Refinitiv.

EU

ECB (MNI SOURCES): ECB Likely To Adjust Or Remove 'Restrictive'

ITALY (BBC): “Italian Prime Minister Giorgia Meloni is heading to the US to meet Donald Trump – a visit that will see her walk a tightrope between representing the interests of the EU and remaining in the US president's good books.”

EU (POLITICO): “With three months to go, political plotting is underway to end Irish Finance Minister Donohoe’s five-year stint as the head of the Eurogroup, a club of 20 eurozone ministers who meet every month, usually in Brussels, to coordinate economic policy.”

UKRAINE (POLITICO): “Ukraine’s determination to defend its territorial integrity will never flag, Foreign Ministry spokesman Heorhii Tykhyi told a press briefing in Kyiv on Wednesday, brushing aside a claim by U.S. special envoy Steve Witkoff that a permanent peace deal with Russia hangs on Kyiv’s relinquishing five regions currently under Moscow’s control.”

US

US/JAPAN (RTRS): “President Donald Trump said there was "big progress" when he made the surprise move on Wednesday to negotiate directly with a Japanese trade delegation in Washington about the barrage of tariffs he has imposed on global imports.”

FED (MNI): Federal Reserve Chair Jerome Powell said Wednesday the FOMC should wait before making any interest rates moves given that President Donald Trump's high tariffs could raise both inflation and unemployment, putting the Fed in a "challenging scenario."

FED (MNI BRIEF): Federal Reserve Chair Jerome Powell said Wednesday tariffs are likely to raise both unemployment and inflation, which will either move the central bank away from its goals or at least prevent it from making fresh progress toward achieving them.

MARKETS (MNI BRIEF): Federal Reserve Chair Jerome Powell said Wednesday volatility in stock and bond markets has been high in the face of President Donald Trump's rapid changes in trade policy, but added they are functioning in an orderly manner.

FED (MNI BRIEF): Federal Reserve Bank of Kansas City President Jeff Schmid said Wednesday the risks of veering away from full employment and price stability are "on the upswing," though the U.S. economy is starting from a good position.

FED (MNI): Policy uncertainty in Washington is raising risks to both sides of the Federal Reserve’s dual mandate, making it the best course of action to hold interest rates steady for now while policymakers wait for clarity, Cleveland Fed President Beth Hammack said Wednesday.

OTHER

JAPAN (MNI BRIEF): Bank of Japan Governor Ueda warned on Thursday that uncertainties linked to U.S. tariffs have increased sharply and the bank will assess their impact on the economy and prices without preconditions, and conduct policy appropriately.

JAPAN (MNI BRIEF): Bank of Japan board member Junko Nakagawa warned on Thursday that uncertainties from tariff policies have risen and the Bank will conduct monetary policy appropriately while carefully monitoring the evolving economy, prices and financial markets at home and abroad.

JAPAN (RTRS): “Japan's exports rose for a sixth straight month in March, data showed on Thursday, as the threat of sweeping U.S. tariffs drove Japanese companies to ramp up shipments while sparking concerns about the outlook of the country's export-reliant economy.”

NEW ZEALAND (MNI INTERVIEW): A former RBNZ official discusses the future path of the OCR. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CHINA

GEOPOLITICS (BBG): “Chinese President Xi Jinping promoted the idea of an “Asian family” and called for regional unity during a tour of Southeast Asia, in an apparent effort to counter US pressure on nations to limit trade ties with Beijing.”

BONDS (SECURITIES TIMES): “Government bond issuance will accelerate in Q2 to CNY7.8 trillion with net financing at CNY4.3 trillion, according to Securities Times, citing estimates from Industrial Securities.”

CHINA MARKETS

MNI: PBOC Net Injects CNY179.6 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY245.5 billion via 7-day reverse repos, with the rate unchanged at 1.50%. The operation led to a net injection of CNY65.9 billion after offsetting the maturities of CNY65.9 billion reverse repos today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.6078% at 10:04 am local time from the close of 1.7176% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 43 on Wednesday, compared with the close of 44 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.2085 Thurs; -0.97% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.2085 on Thursday, compared with 7.2133 set on Wednesday. The fixing was estimated at 7.3121 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND Q1 CONSUMER PRICES +0.9% Q/Q; EST. +0.8%; Q4 +0.5%

NEW ZEALAND Q1 CONSUMER PRICES +2.5% Y/Y; EST. +2.4%; Q4 +2.2%

NEW ZEALAND Q1 NON-TRADABLE PRICES +1.1% Q/Q; EST. +0.8%; Q4 +0.7%

NEW ZEALAND Q1 TRADABLE PRICES +0.8% Q/Q; EST. +0.8%; Q4 +0.3%

NEW ZEALAND Q1 RBNZ CORE CPI 2.9% Y/Y; Q4 3.0%

AUSTRALIA MARCH EMPLOYMENT +32.2K M/M; EST. 40.0K; FEB. -57.5K

AUSTRALIA MARCH FULL-TIME EMPLOYMENT +15.0K M/M; FEB. -43.8K

AUSTRALIA MARCH PART-TIME EMPLOYMENT +17.2K M/ML FEB. -13.6K

AUSTRALIA MARCH JOBLESS RATE 4.1%; EST. 4.2%; FEB. 4.0%

AUSTRALIA MARCH PARTICIPATION RATE 66.8%; EST. 66.9%; FEB. 66.7%

JAPAN MARCH EXPORTS +3.9% Y/Y; EST. 4.4%; FEB. +11.4%

JAPAN MARCH IMPORTS RISE 2.0% Y/Y; EST. 3.1%; FEB. -0.7%

JAPAN MARCH TRADE BALANCE 544.1B YEN; EST. 464.9B YEN; FEB. 590.5B

MARKETS

US TSYS: Asia Wrap - Yields Try Find A Base

TYM5 has traded heavy with a range of 111-05+ to 111-16 during the Asia-Pacific session. It last changed hands at 111-06, down 0.07 from the previous close.

- The US 10-year yield has moved higher, dealing around 4.31% from a close around 4.27%.

- The market is trying to see positives emanating from the US-Japan trade talks, with stocks holding onto their session gains.

- Jerome Powell crushed the hopes of any traders still expecting the Fed to rescue them with cuts. Signalling a wait-and-see approach and tipping price stability over employment, thus removing any notion of a Fed Put.

- “Japanese investors sold 512 Billion Yen worth of foreign bonds in the week ended April 11, a slower pace than the previous week.”(per BBG)

- “This marks the sixth straight week of outflows from overseas debt, amid a 2.4% drop in treasuries, the biggest decline since 2001.”(per BBG)

- Dips back towards 4.25% support for the 10-year have found sellers first up.

- Data/Events: Housing starts, Initial Jobless claims

Fig 1: Jap Foreign Bond Flows

Source: MNI - Market News/Bloomberg

JGBS: Cheaper, US-Japan Trade Talks In Focus, Natl CPI Tomorrow

JGB futures are sharply weaker, -48 compared to the settlement levels, hovering just above session lows.

- (MNI) BoJ Governor Ueda warned on Thursday that uncertainties linked to US tariffs have increased sharply and the bank will assess their impact on the economy and prices without preconditions, and conduct policy appropriately. Ueda told lawmakers that the tariffs will put downward pressure on the Japanese economy through exports, while uncertainty worsens corporate and consumer sentiment and spending, and has an adverse impact on the financial markets.

- (MNI) BoJ Board member Nakagawa warned on Thursday that uncertainties from tariff policies have risen and the Bank will conduct monetary policy appropriately while carefully monitoring the evolving economy, prices and financial markets at home and abroad.

- Cash US tsys are 1-4bps cheaper, with a flattening bias, in today's Asia-Pac session after yesterday's solid rally. US tsys have been pressured by risk-on sentiment emanating from the US-Japan trade talks, with stocks showing gains.

- The cash JGB curve is showing a bear-flattener, yields flat to 6bps higher, with the futures-linked 7-year leading the way.

- Swap rates are +4bps to -1bps, with a flattening bias. Swap spreads are mostly tighter.

- Tomorrow, the local calendar will see National CPI data.

AUSSIE BONDS: Bull-Steepener Heading Into Easter Long W/E

ACGBs (YM +2.0 & XM +6.5) are holding richer on the day, little changed after the release of the March Employment Report.

- While the employment numbers were volatile in Q1 due to an increase in the number of retirees, other labour data, including underutilisation, are showing that the labour market remained tight over the quarter, with steady conditions. The RBA is unsure how tight the labour market is, given that price and wage inflation is moderating, and thus this data will continue to be watched closely.

- While to one decimal place, the unemployment rate rose 0.1pp to 4.1%, looking deeper, it was almost unchanged at 4.05% after 4.04% in February, which was revised down only 0.01pp.

- Cash ACGBs are 2-7bps richer on the day with the AU-US 10-year yield differential at -3bp.

- Bill strip pricing has twist-flattened, with pricing -3 to +2.

- RBA-dated OIS pricing is mixed today, with 2025 meetings 1-3bps firmer and 2026 1-3bps softer. A 50bp rate cut in May has been scaled back to a 20% probability, with a cumulative 118bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- The local market is closed until Tuesday for the Easter weekend.

BONDS: NZGBS: Closed With A Bull-Flattener Ahead Of Easter W/E

NZGBs closed showing a bull-flattener, with benchmark yields flat to 6bps lower. While the 10-year closed near bests, the 2-year finished 6bps cheaper than the session's best levels.

- The NZ-US 10-year yield differential finished 4bps tighter at +22bps.

- Cash US tsys are 2-4bps cheaper in today's Asia-Pac session after yesterday's solid rally.

- Domestically, Q1 inflation printed higher than expected at 0.9% q/q, bringing the annual rate to 2.5% up from 2.2% in Q4. However, the RBNZ's measure of underlying inflation from its sector factor model printed at 2.9% in Q1 after 3% in Q4, which was revised 0.1pp lower. Core inflation is now just under the top of the RBNZ's 1-3% target band and its lowest rate since Q2 2021.

- Today’s sale of NZ$275mn of the 3.00% Apr-29 bond and NZ$225mn of the 4.25% May-36 bond showed cover ratios of 3.20x to 4.00x, respectively.

- Swap rates closed flat to 4bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed flat to 2bps firmer across meetings after the release of Q1 CPI data. 27bps of easing is priced for May, with a cumulative 79bps by November 2025. The local market is closed until Tuesday for the Easter weekend.

FOREX: FX Wrap - USD Bounces With Risk

The BBDXY had an Asian range of 1224.11 - 1228.83. The USD is bouncing as the market is trying to see positives emanating from the US-Japan trade talks with US equity futures holding onto their session gains. The USD has looked has fallen sharply in recent weeks as a rotation out of US assets seems to be gathering momentum and normal correlations with yield are breaking down. There may be scope to pare back some of these positions as we move into the long weekend.

- EUR/USD - Asian range 1.1356 - 1.1409, has drifted lower most of our session. Traders are targeting a move back to 1.2000 in the Euro as the USD’s safe haven role is reassessed. Do not discount some dips on route.

- GBP/USD - Asian range 1.3203 - 1.3254, dealing near the session lows. GBP seems to have finally found some offers back towards 1.3300, expects buyers to reemerge on dips back to 1.30/31.

- USD/CNH - Asian range 7.2978 - 7.3163, the USD/CNY fix printed lower at 7.2085. BBG reports, “ The Yuan could find support from Chinese importers as they start selling USD longs that they took out as hedges against the impact of trade wars.”

- USD/JPY - Asian range 141.62 - 142.86, went bid as the market chose to view comments coming out of the US-Japan talks as positive, price has not been able to hold onto the break sub 142.00, expect sellers back towards the 144/145 zone with some 145.00($1.4bln) expiries tonight. Huge support level around 140, a break here could see yen gains accelerate.

- Cross asset : SPX futures +0.75%, Gold 3340, US 10yr 4.30%, BBDXY 1228, Crude oil 63.37.

- Data/Events : Ger PPI, ECB rate, US Housing starts, Initial Jobless claims.

Fig 1: USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

FOREX: Antipodean Wrap - AUD & NZD Struggling At Their Highs

The market is trying to see positives emanating from the US-Japan trade talks with equity futures holding onto their session gains (Eminis +0.75%). USD/CNY Fix prints 7.2085, the PBOC showing they are not in any hurry to get this cross higher.

- AUD/USD - Asian range 0.6345 - 0.6377, AUD has traded heavy for most of the Asian session. Australia’s jobless rate rose to 4.1% in March, employment increased by 32k, less than the forecast of 40k. The market will be watching for signs of exhaustion in the A$ as the move higher finally stalls towards the 0.6400 area. Dips back to the 0.6250 area should find buyers once more.

- AUD/JPY - Asian range 90.25 - 90.81, AUD/JPY has bounced alongside risk as the market prefers to see put a positive spin on feedback from the US-Japan talks. Price goes into the London open around 90.50 firmly within its range of the week 0.8950/0.9150. The market wants a positive outcome, should it get this outcome expect the highs of 91.50/92.00 to be tested. Any negative slant though and we will see price action similar to yesterday and the JPY will be a favourite to own once more.

- NZDUSD - Asian range 0.5909 - 0.5944, an upside surprise in CPI rules out a 50bps cut ? The market initially tried to bounce but once again traded poorly back towards the 0.5950 area and has fallen quickly back to go into London near the overnight lows. Price action like the AUD is pointing to momentum stalling and potential for some reversion back to the mean. Expect buyers to return first around 0.5800/30, then around 0.5750.

- AUD/NZD - Asian range 1.0725 - 1.0761, the cross has drifted sideways in the Asian session, not shifting greatly following the data outcomes.

Fig 1 : AUD/USD Spot 15min Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: A Broadly Positive Day Ahead of Holidays

A mostly positive day across the region after the US and Japan trade negotiations showed positive signs, with President Trump suggesting progress was happening. Tariff risks and trade talks are quick to drive sentiment at present as the trade war looms large over the region.

- China’s Hang Seng was one of the strongest in the region, rising +1.62%, following yesterday’s declines. The Hang Seng has risen in seven out of eight trading sessions capping off a remarkable period. The CSI 300 didn’t follow suit today finishing where it started whilst Shanghai Comp was up +0.20% and Shenzhen up +0.75%.

- The KOSPI rose +0.64% today, following the BOK’s decision to remain on hold, clawing back half of yesterday's losses.

- In Singapore the Straits Times has had a very strong day rising +1.35%, whilst in the Philippines the PSEi was one of the few fallers today, down -0.80%.

- Malaysia’s FTSE Malay KLCI was up +0.53% to almost erase yesterday’s losses.

- Indonesia’s Jakarta Composite was up +0.20% recouping a third of yesterday's losses.

- India’s NIFTY 50 is opening weaker today, down -0.20% following a very strong start to the week.

OIL: Crude’s Rally Continues On Iran Supply Outlook & US Stock Data

Oil prices have continued Wednesday’s rally during today’s APAC trading driven by the US stating it will be stricter on Iranian exports and will pressure them to zero if needed. The fall in crude stocks at Cushing and the better risk tone have also contributed to the rally. They rose over 2% yesterday and are around 1% higher today.

- WTI is up 1.4% to $63.37/bbl, close to the intraday high, after rising 2.1% yesterday. Brent is 1.1% higher at $66.59/bbl following Wednesday’s 2.15% increase. Both remain below initial resistance.

- The EIA reported that US crude stocks rose 515k barrels last week, the third consecutive weekly rise, but they fell 650k at Cushing and product inventories continued to decline with distillate down 1.85mn and gasoline 1.96mn, the seventh straight fall. The 0.4pp drop in refinery utilisation to 86.3% likely contributed to the trends but fuel demand looks solid.

- The US Treasury has penalised a second refinery in China for allegedly accepting Iranian crude, according to Bloomberg, but both countries have found ways to avoid detection. But Iran has warned that nuclear talks could be derailed if the US “moves the goalposts”.

- OPEC decided to reduce its output cuts this month more than expected in exchange for greater quota compliance. However, Russia, Iraq and especially Kazakhstan continue to overproduce.

- Later the Fed’s Barr speaks and US March housing data, jobless claims and April Philly Fed print. The ECB decision is announced and it is expected to cut rates another 25bp (see MNI ECB preview).

- Oil won’t trade on Good Friday.

- Gold leapt above all prior highs overnight, smashing through the US$3,300 barrier and challenging all forecasts at the beginning of 2025

- Federal Reserve Chairman Powell warned that the trade tension and tariff war could result in inflation and hence the US Central Reserve is in no rush to cut rates whilst the WTO cut is forecast for merchandise trade as uncertainty reigns on tariffs. This equities lower and gold higher overnight which carried into the opening of the trading day in Asia.

- Opening at $3,342.19 and moving higher initially to $3,357.78, gold retreated in the afternoon in Asia to reach $3,339.75.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/04/2025 | 0600/0800 | ** | PPI | |

| 17/04/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 17/04/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 17/04/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 17/04/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 17/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 17/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 17/04/2025 | 1230/0830 | * | International Canadian Transaction in Securities | |

| 17/04/2025 | 1230/0830 | *** | Housing Starts | |

| 17/04/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 17/04/2025 | 1245/1445 | ECB Monetary Policy press conference | ||

| 17/04/2025 | 1400/1000 | * | US Bill 08 Week Treasury Auction Result | |

| 17/04/2025 | 1400/1000 | ** | US Bill 04 Week Treasury Auction Result | |

| 17/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 17/04/2025 | 1530/1130 | ** | US Treasury Auction Result for TIPS 5 Year Note | |

| 17/04/2025 | 1545/1145 | Fed Governor Michael Barr | ||

| 17/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 17/04/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 18/04/2025 | 2330/0830 | *** | CPI |