MNI EUROPEAN OPEN: US To Send Letters On Tariff Rates Today

EXECUTIVE SUMMARY

- TRUMP SAYS COUNTRIES WILL START PAYING TARIFFS FROM AUGUST 1 - BBG

- REPUBLICANS MUSCLE TRUMP’S SWEEPING TAX-CUT AND SPENDING BILL THROUGH CONGRESS - RTRS

- BOSTIC SAYS FED CAN WAIT FOR MORE CLARITY ON OUTLOOK - MNI

- MNI DISCUSSES BOJ’S POTENTIAL HIKING STRATEGY - MNI

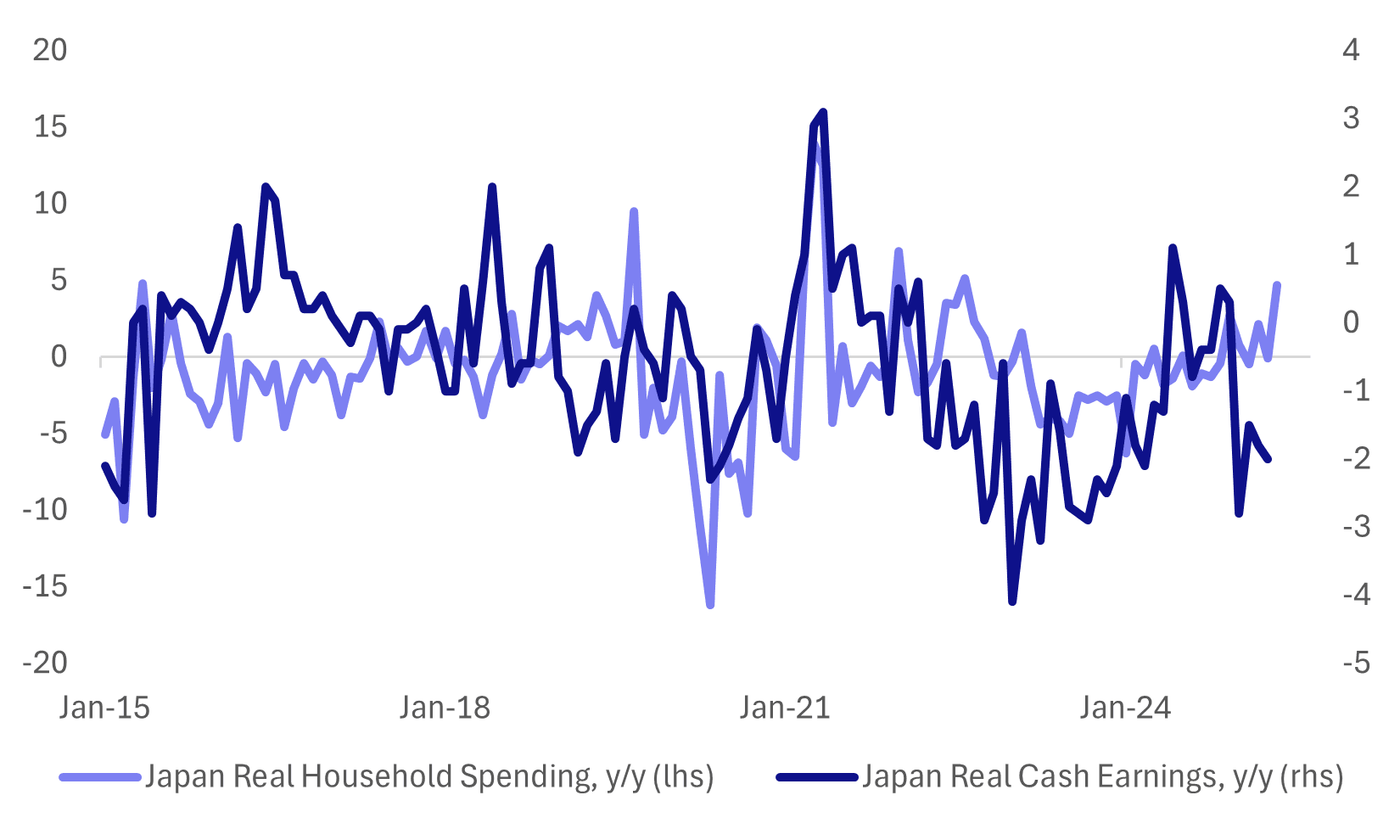

- JAPAN'S HOUSEHOLDS BOOST SPENDING BY MOST SINCE SUMMER 2022 - BBG

Fig 1: Japan Household Spending Surged In May

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

PENSIONS (FT/BBG): "UK Chancellor Rachel Reeves is expected to announce a review of UK pensions in a speech 15, including the amount companies and staff set aside for retirement, the Financial Times reports, citing two unidentified executives familiar with her plans.'

EU

ECB (MNI INTERVIEW): The European Central Bank’s success in delivering monetary policy goals has come despite a “new normal” of heightened uncertainty, and policymakers are well-positioned to respond to any shocks, Bank of Latvia Governor and ECB Governing Council member Martins Kazaks told MNI.

ECB (BBG): "A temporary undershoot of euro-area inflation is no reason for concern and the European Central Bank can wait with any further interest-rate moves, according to Governing Council member Joachim Nagel."

EU/CHINA (BBG): “The Chinese government intends to cancel part of a summit with European Union leaders planned for later this month, in the latest sign of the tensions between Brussels and Beijing.”

AUTOS (YICAI): “Chinese auto-part exporters are offsetting slower U.S. growth with faster demand from other markets, with European business up 20% in some cases, according to manufacturers interviewed by Yicai.”

US

TARIFFS (BBG): "President Trump reiterates that letters on tariff rates will be sent out tomorrow, without naming any countries. Trump says by July 9 “they’ll be fully covered and they’ll range in value from maybe 60 or 70% tariffs to 10 and 20% tariffs”. Says countries “will start to pay on August 1”"

TARIFFS (BBG): “US President Donald Trump said that his administration may begin sending out letters to trading partners as soon as Friday setting unilateral tariff rates ahead of a July 9 deadline for negotiations.”

FISCAL (RTRS): “President Donald Trump 's tax-cut legislation cleared its final hurdle in the U.S. Congress on Thursday, as the Republican-controlled House of Representatives narrowly approved a massive package that would fund his domestic agenda and push millions of Americans off health insurance”

FED (MNI): Atlanta Federal Reserve President Raphael Bostic said Thursday the effects of US trade tariffs may be slower and more persistent than initially expected, and there is no immediate need for shifts in monetary policy.

FED (MNI BRIEF): Atlanta Federal Reserve President Raphael Bostic said Thursday the tariff rollout will likely cause a slow, incremental impact on prices and the back-and-forth makes it difficult to provide guidance on borrowing costs.

SERVICES (MNI INTERVIEW): US Services Growth Seen Gaining Momentum - ISM

OTHER

JAPAN (MNI POLICY): MNI discusses the BOJ's potential hiking strategy.

JAPAN (BBG): "- Japan’s household spending rose the most since the summer of 2022 in a sign that consumer may be getting used to persistent inflation and could support for an economy that’s taking a hit from US tariffs."

CHINA

POPULATION (BBG): "China is planning to offer cash handouts to families as an incentive for couples to have children, according to people familiar with the matter, as years of population decline threaten the world’s No. 2 economy."

CONSUMPTION (YICAI): “China should increase consumption propensity through redistributive reforms such as raising the proportion of disposable income in the household sector and boosting spending on public services, wrote Sheng Songcheng, dean at the China Chief Economist Forum Institute, in an Yicai.com article.”

OVERCAPACITY (SECURITIES TIMES): " Companies across industries, from automobiles and solar to batteries, have begun reducing production or curbing price cuts, as the government intensifies efforts to rein in cut-throat competition, the Securities Times reports Friday."

SOLAR (Ministry of Industry and Information Technology): “China’s photovoltaic industry must manage disorderly low-price competition, deepen the construction of a unified national market and promote the orderly exit of outdated capacity, according to Jin Zhuanglong, party secretary of the Ministry of Industry and Information Technology”.

MNI: PBOC Net Drains CNY491.9 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY34 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY491.9 billion after offsetting the maturity of CNY525.9 reverse repo today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4352% at 09:35 am local time from the close of 1.4674% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 45 on Thursday, compared with the close of 47 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1535 Fri; +1.60% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1535 on Friday, compared with 7.1523 set on Thursday. The fixing was estimated at 7.1697 by Bloomberg survey today.

MARKET DATA

AUSTRALIA MAY HOUSEHOLD SPENDING M/M 0.9%; MEDIAN 0.5%; PRIOR 0.0%

AUSTRALIA MAY HOUSEHOLD SPENDING Y/Y 4.2%; MEDIAN 3.5%; PRIOR 3.8%

JAPAN MAY HOUSEHOLD SPENDING 4.7%; MEDIAN 1.2%; PRIOR -0.1%

SOUTH KOREA MAY BOP CURRENT ACCOUNT $10141.5MN; PRIOR $5701.7MN

SOUTH KOREA MAY BOP GOODS BALANCE $10664.9MN; PRIOR $8988.8MN

MARKETS

US TSYS: Asia Wrap - Futures Edge Higher With No Cash Market

The TYU5 range has been 111-07 to 111-11 during the Asia-Pacific session. It last changed hands at 111-10+, up 0-03+ from the previous close.

- No cash market today.

- The 10-year yield has seen a strong bounce in reaction to the better NFP print. This 4.35/40% area offers those who would like to express a long the opportunity to fade. A sustained close back above 4.40/4.45% area though would not be great for the bulls and would see more of the longs prepared back.

- Bob Elliot on X: ”Employment report internals confirm continued labor market weakening. Private sector jobs are weak. Strong payrolls number driven by unusual surge in gov jobs. HH survey employment down since Jan. Unemployment is up. Labor force participation falling. Wage growth is slowing.”

- Bloomberg - “Goldman Sachs has lowered its forecasts for US Treasury yields, expecting 2- and 10-year yields to end the year at 3.45% and 4.20%, respectively. The move follows Goldman's economists revising their expectations for Fed rate cuts, now predicting cuts in September, October, and December.”

- MNI FED: Atlanta's Bostic: "No Time For Significant Shifts" In Policy. Atlanta Fed President Bostic largely reiterates previous commentary on current monetary policy (including at Monday's MNI event) in a speech in Frankfurt. "A period characterized by such widespread uncertainty is no time for significant shifts in monetary policy." "That is especially the case against the backdrop of a still resilient macroeconomy, which offers space for patience."

JGBS: Modest Bear-Steepener, Narrow Ranges With The US Markets Out

JGB futures are slightly stronger and at session highs, +2 compared to settlement levels.

- Japan's real household spending for May rose 4.7%y/y, well above market forecasts of a 1.2% gain. The April outcome was -0.1%y/y. In m/m terms, spending was up a strong 4.6%.

- (Bloomberg) - The grind higher in JGB long-end yields isn't done yet, with Japan's spring wage talks delivering the biggest pay bump in 34 years. Add to that today's pop in household spending -- the strongest since mid-2022 -- and the data drumbeat is starting to give the BOJ exactly what it's been looking for.

- "TACHIBANA: POLICY UNCHANGED FOR SINCERE TARIFF TALKS WITH US" – BBG

- Cash JGBs are flat to 2bps cheaper across benchmarks, with a steepening bias. The benchmark 10-year yield is 0.4bps higher at 1.446% versus the cycle high of 1.596%.

- Ranges have, however, been narrow with the US markets out for the 4th of July holiday. US 10-year futures are trading slightly higher.

- Swaps have twist-steepened, with rates 1bp lower to 1bp higher.

- On Monday, the local calendar will see Labor & Real Cash Earnings and Coincident/Leading Index.

AUSSIE BONDS: Slightly Cheaper, Narrow Ranges, HH Spend Solid

ACGBs (YM -2.0 & XM -1.5) are cheaper but at the Sydney session bests. Ranges have, however, been narrow with the US markets out for the 4th of July holiday. US 10-year futures are trading slightly higher.

- (Bloomberg) Australia's May spending data presents a mixed picture, with weak retail trade data suggesting consumers are cautious, but stronger-than-expected broader spending data showing a surge in discretionary spending.

- Cash ACGBs are 1-2bps cheaper.

- The bills strip is cheaper, with pricing -3 to-4.

- On Monday, the local calendar will see ANZ-Indeed Job Advertisements and Foreign Reserves. The RBA Policy Decision is on Tuesday.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in July is given a 92% probability, with a cumulative 76bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- Next week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035 bond on Wednesday and A$1000mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Closed Flat After Reversing Early Weakness

NZGBs closed flat after reversing early weakness (4bps cheaper) following yesterday’s post-payrolls sell-off in US tsys.

- US markets are out today for the 4th of July holiday. US 10-year futures are trading slightly higher.

- The local calendar was empty today. The next major event on the calendar will be the RBNZ Monetary Policy Review next Wednesday.

- (Bloomberg) - "The market reaction to fresh US economic data on Thursday shows traders remain unconvinced that uncertainty from President Trump's trade war will significantly disrupt the global economy. A rally in global equity indexes as well as a robust bid for credit show increasingly resilient risk sentiment, and rising yields across the globe indicate a lack of demand for safe haven assets."

- Swap rates closed 1bp higher.

- RBNZ dated OIS pricing closed flat to 3bps firmer across meetings. 3bps of easing is priced for July, with a cumulative 31bps by November 2025.

- Interest rate expectations across dollar-bloc economies were firmer over the past week, led by a 14bp gain in the US. Canada, Australia and New Zealand saw modest firming in the range of 2-6bps.

FOREX: Asia FX Wrap - The USD Drifts Lower

The BBDXY has had a range of 1189.73 - 1191.48 in the Asia-Pac session, it is currently trading around 1189. The USD has drifted lower in a quiet Asia-Pac session, -0.18%, the price action is particularly poor given the surge in US yields and a market that is supposedly extremely short. “ The Chinese government plans to cancel the second day of a two-day summit with European leaders, scheduled for later this month, due to tensions between Brussels and Beijing”(BBG). "China Industries Cut Output Amid Price War Crackdown: Sec. Times. Companies across industries, from automobiles and solar to batteries, have begun reducing production or curbing price cuts, as the government intensifies efforts to rein in cut-throat competition, the Securities Times reports Friday." BBG

- EUR/USD - Asian range 1.1754 - 1.1780, Asia is currently trading 1.1775. While the USD remains on the back foot the EUR will be the main beneficiary. This market will now be looking towards 1.2000 and beyond, the price is starting to look a little stretched in the short term. First support is back towards 1.1600.

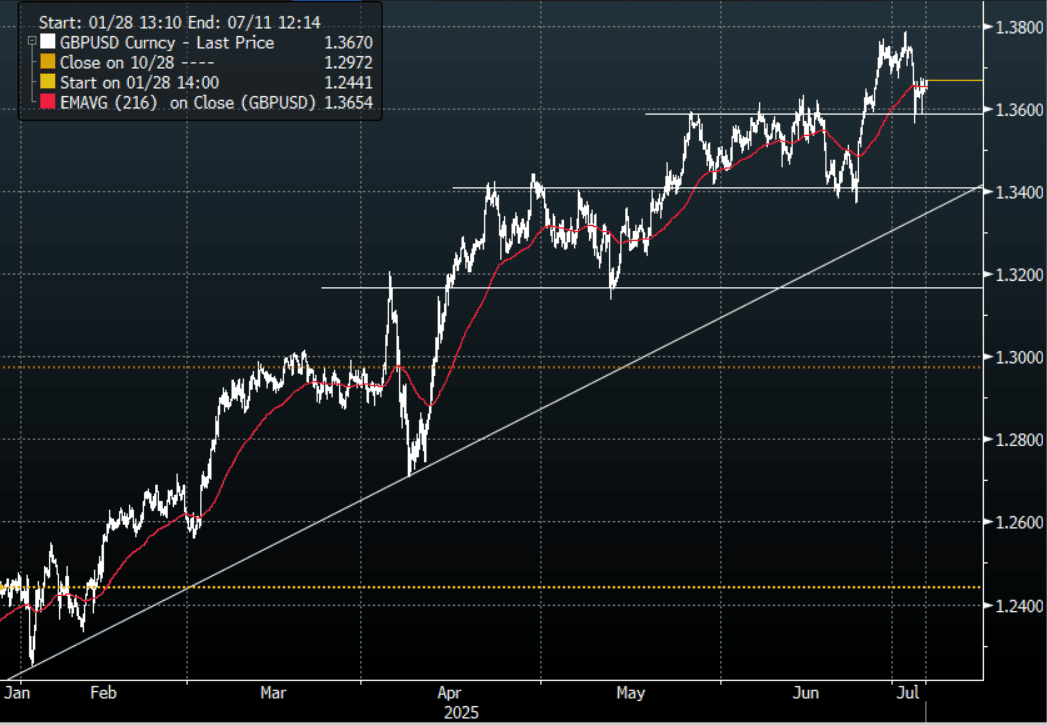

- GBP/USD - Asian range 1.3645 - 1.3668, Asia is currently dealing around 1.3670. For the second time strong demand was seen below 1.3600 helping the support to hold. A sustained move sub 1.3550 needed to signal a deeper correction.

- USD/CNH - Asian range 7.1626 - 7.1709, the USD/CNY fix printed 7.1535, Asia is currently dealing around 7.1630. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.30%, Gold $3340, TYU5 111-11, BBDXY 1189, Crude oil $66.88

- Data/Events : Italy Retail Sales, France Industrial Production, EZ PPI, Spain Industrial Production, Germany Factory Orders, HCOB Construction PMI

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

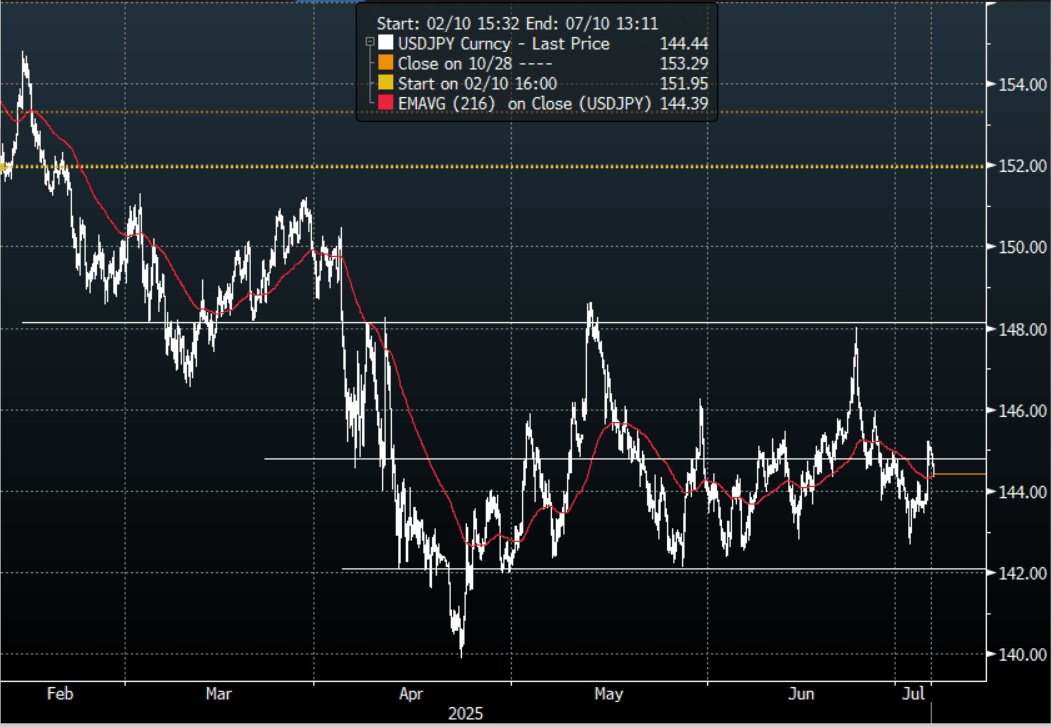

JPY: Asia Wrap - USD/JPY Gives Back Some Of Its NFP Gains

The Asia-Pac USD/JPY range has been 144.34 - 144.98, Asia is currently trading around 144.45, -0.35% drifting off its overnight highs in our session. The market wants to be short USD/JPY so will be disappointed with last night's result as the JPY longs would have been hoping for a reason to test lower. Price is now back in the middle of the wider 142.00 - 148.00 range and the pair will probably continue to take its cue from the US rates market which was also wrongly positioned for a better NFP.

- JAPAN DATA May Household Spending Surges, Diverging From Softer Real Wages : Japan real household spending for May rose 4.7%y/y, well above market forecasts of a 1.2% gain. The April outcome was -0.1%y/y. In m/m terms spending was up a strong 4.6%.

- (Bloomberg) - The grind higher in JGB long-end yields isn’t done yet, with Japan’s spring wage talks delivering the biggest pay bump in 34 years. Add to that today’s pop in household spending -- the strongest since mid-2022 -- and the data drumbeat is starting to give the BOJ exactly what it’s been looking for.

- "TACHIBANA: POLICY UNCHANGED FOR SINCERE TARIFF TALKS WITH US” - BBG

- The rejection of 148.00 points to a potential top being in place now and shows just how quick the market is to return to selling USD’s. USD/JPY was looking for a fresh catalyst to probe the lower end of its range again but NFP did not provide that so we are now back in the middle of the range. The JPY bulls will be hoping the move higher in US yields is capped pretty soon as a break higher in rates would start to make a very long JPY market vulnerable.

- Options : Close significant option expiries for NY cut, based on DTCC data: 142.00($984m), 140.00($1.04b).Upcoming Close Strikes : 142.75($855m July8).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Consolidates In A Quiet Session

The AUD/USD has had a range of 0.6563 - 0.6579 in the Asia- Pac session, it is currently trading around 0.6570, -0.05%. The pair has traded sideways in a very subdued session. US Equity futures have drifted off their overnight highs in Asia, ESU5 -0.22%, NQU5 -0.20%. With US yields surging higher and staying there the USD’s inability to hold onto any gains is a worrying sign for the currency, especially when positioning is supposedly all the same way and at extreme levels. Look for some consolidation again in the AUD/USD as the pair continues to build a base from which to move higher.

- AUSTRALIA DATA - Household Spending Firms In May, Y/Y Trend Improving Modestly: Australian May Household spending data was stronger than forecast, rising 0.9%m/m, against a 0.5% forecast. In y/y terms we printed 4.2%, against an expected gain of 3.5% and prior 3.8% outcome. The April outcome was revised to flat in m/m terms, after initially being reported as a 0.1% gain.

- Today's print contrasts with the earlier retail sales this week, which came in below market forecasts (+0.2%m/m, versus +0.5% forecast). More weight should be given to today's May household spending outcome though, as it will replace the retail sales print from the end of this month

- "REUTERS POLL-RESERVE BANK OF AUSTRALIA TO CUT CASH RATE TO 3.60% ON JULY 8, SAID 31 OF 37 ECONOMISTS; SIX SAID NO CHANGE" - RTRS

- The AUD/USD is breaking through the top of its recent range as the pressure on the USD increases. First support is seen back towards the 0.6500 area.

- The AUD needs a sustained break above 0.6550/0.6600 to potentially start building momentum for an extended move higher, a close back above 0.6600 and the focus would turn back to 0.6900/0.7000.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD2.59b), 0.6500(AUD 1.38b). Upcoming Close Strikes : 0.6600(AUD884m July 7), 0.6375(AUD722m July 8)

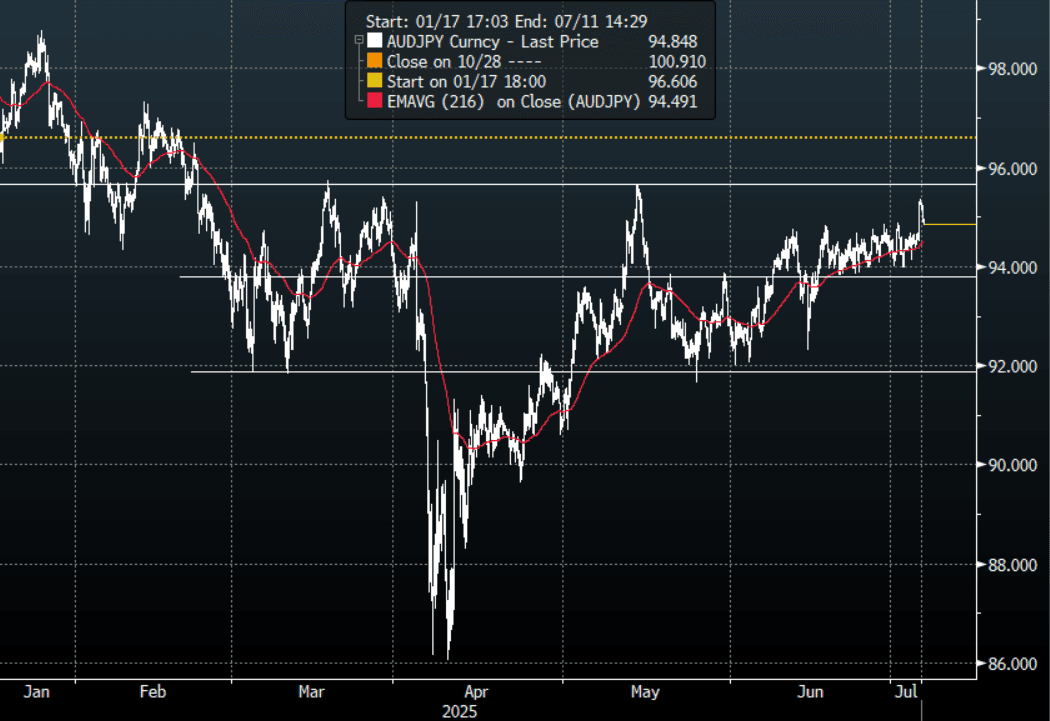

- AUD/JPY - Today's range 94.84 - 95.37, it is trading currently around 94.85, -0.42%. The pair broke above its recent highs around 95.00 overnight and with risk sentiment turning positive it could be turning its focus back towards the 96.00 area.

Fig 1: AUD/JPY spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Trades Sideways In A Subdued Session

The NZD/USD had a range of 0.6064 - 0.6082 in the Asia-Pac session, going into the London open trading around 0.6070, -0.05%.The pair has traded sideways in a very subdued session. US Equity futures have drifted off their overnight highs in Asia, ESU5 -0.3%, NQU5 -0.28%. With US yields surging higher and staying there the USD’s inability to hold onto any gains is a worrying sign for the currency, especially when positioning is supposedly all the same way and at extreme levels. NZD/USD continues its attempt to build a solid base from which to push higher.

- (Bloomberg) - “The market reaction to fresh US economic data on Thursday shows traders remain unconvinced that uncertainty from President Trump’s trade war will significantly disrupt the global economy. A rally in global equity indexes as well as a robust bid for credit show increasingly resilient risk sentiment, and rising yields across the globe indicate a lack of demand for safe haven assets.”

- “Trade Letters May Go Out Later Today, Informing Countries Of Tariff Levels : In earlier remarks US President Trump stated that the administration is likely to start sending letters later today informing countries of where tariff rates will be set. This comes ahead of next week's reciprocal tariff pause deadline.”(BBG)

- A huge bounce from sub 0.5900 and the NZD has now established a foothold above 0.6000, with the USD breaking lower the NZD/USD looks to be building for a potential break higher of its own. A clear break of 0.6100 could provide the momentum to begin a larger move higher, initially targeting the 0.6400/0.6500 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6075(NZD519m July 9).

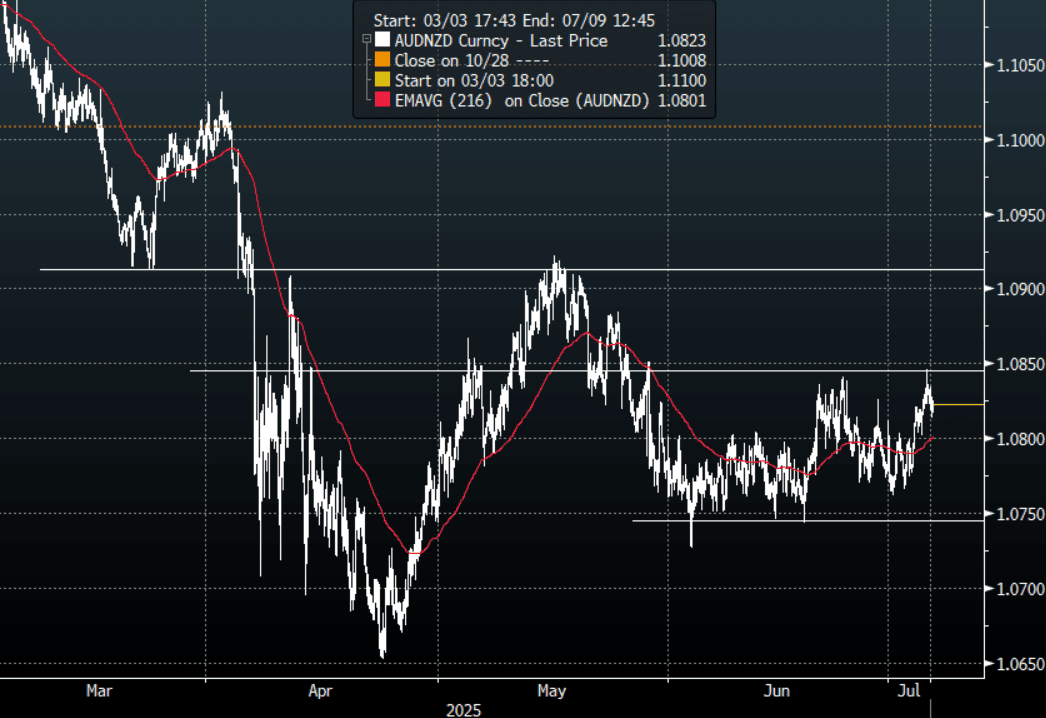

- AUD/NZD range for the session has been 1.0813 - 1.0834, currently trading 1.0820. The cross is struggling to get any momentum for now. It looks to be in a 1.0750 - 1.0850 range for now as it awaits a catalyst to provide some clearer direction.

Fig 1: AUD/NZD Spot Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: KOSPI Down Heavily on Tariff Concerns

As the deadline for tariffs looms large, Korea's KOSPI has had heavy falls into the week's end as investors begin to fear the resumption of tariffs on the export orientated economy. After posting strong gains yesterday on the hope that bills to improve governance in the country will be beneficial to equity investors, today saw falls that erased those gains and could see the KOSPI finish lower for the week. This weighed on several key markets in the region with very few delivering any meaningful gains.

- China's major bourses have had a mixed end to the week. The Hang Seng is down with Shenzhen whilst the CSI 300 and Shanghai are up. The Hang Seng is down -0.62% today and -1.66% for the week. The CSI 300 is up +0.41% today and +1.60% for the week and the Shanghai Comp up +0.41% and +1.50% for the week. The Shenzhen Comp is down -0.07% today but has had a strong week up +1.50%.

- Taiwan's TAIEX if down -0.66% today and -0.26% for the week.

- The KOSPI is down -1.61% today and holding on to modest gains of +0.35% for the week.

- The FTSE Malay KLCI is up modestly by +0.13% and has had a strong week delivering gains of +1.50%.

- The Jakarta Composite is down -0.21% today and -0.50% for this week.

- The FTSE Straits Times in Singapore is down -0.30% today but up +1.05% for the week whilst the PSEi in the Philippines fell heavily today by -0.95% and is currenlty flat for the week.

- India's NIFTY 50 is doing very little in their morning session and will need a strong rally to erase the gains week to date of -0.92%

Oil Down Today but Set for Weekly Gain

- In a market where liquidity was low ahead of the US holiday, stronger than expected jobs data and the ongoing discussions from OPEC+ about an increase supply were enough to push oil lower in the Asia trading day.

- WTI is down in the Asia trading session by -0.46% at US$66.86 bbl but remains up over 2% for the week.

- WTI sits marginally above the 20-day EMA of $66.76 and below the 200-day EMA of $66.27.

- Brent is down -0.39% today at $68..59 and for the week is up +1.20% following strong gains on Wednesday.

- American refiners are relying on oil supplies from the country's biggest shale basins more than ever as flows of denser varieties from places like Mexico and Canada ebb. US drillers are using the lightest oil on record, according to recent government data, leaning heavily on shale formations in Texas, New Mexico and North Dakota. The shift comes as heavy crude supplies are strained by falling production from Mexico, a trade spat with Canada and a de facto US ban on imports of Venezuelan oil. (source BBG)

- China avoided purchasing US crude for the third straight month - the longest stretch since 2018 - delivering a fresh blow to shale drillers already facing lower oil prices.

- Iranian oil output reached a 46-year high in 2024 and is expected to increase again this year, despite US oil sanctions. The country's energy sector has emerged unscathed, with energy export revenue hitting a 12-year high of $78 billion last year.

Gold Set to Finish Week Higher

- With the US out and trading volumes low, gold looks set to finish the week higher thanks to gains on Monday and Tuesday.

- With Middle East tensions easing, gold traders turn their attention to US data as a guide for interest rates and trade talks. As data overnight indicated a stronger economy the probability of interest rate cuts are being pushed out. With a deal announced with Vietnam it is anticipated in the coming days further new announcements with countries be revealed.

- Gold is up +1.93% and is currently trading at US$3,337.90 just $94.44 off the May high.

- Year to date gold is up +28%. If it were to hold those returns it would be the best year since 2010 in which it delivered 29.5% of gains.

- Gold move today sees is just above the 20-day EMA of $3,337.34

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/07/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 04/07/2025 | 0645/0845 | * | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Industrial Production | |

| 04/07/2025 | 0700/0900 | ** | Unemployment | |

| 04/07/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 04/07/2025 | 0800/1000 | * | Retail Sales | |

| 04/07/2025 | 0800/1000 | ECB Elderson Speech At IMF OEDNE/World Bank Meeting | ||

| 04/07/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 04/07/2025 | 0900/1100 | ** | PPI | |

| 04/07/2025 | 1500/1600 | BOE Taylor Speech On Natural Interest Rate |