MNI EUROPEAN OPEN: US Senate Moves To End Shutdown

EXECUTIVE SUMMARY

- SHUTDOWN NEARS END AS DEMOCRATS AGREE TO FUNDING DEAL - BBG

- FED FLAGS HIGH FINANCIAL SECTOR LEVERAGE - MNI BRIEF

- A FORMER BOJ BOARD MEMBER SHARES HIS POLICY RATE OUTLOOK - MNI INTERVIEW

- BOJ OPINIONS: MEMBERS SEE RATE HIKE, BUT NO IMMINENT MOVE - MNI

- RBA CHALLENGED BY AUSTRALIA’S THIN SPARE CAPACITY, HAUSER SAYS - BBG

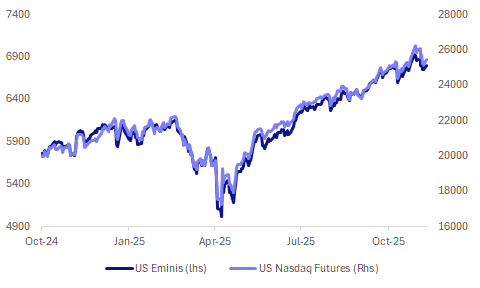

Fig 1: US Equity Futures Firm On Hopes Shutdown Coming To An End

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

FISCAL (TIMES): “Cabinet ministers have privately warned Rachel Reeves that increasing income tax in the budget may spell electoral disaster for the Labour Party.”

FISCAL (BBG): “UK Culture Secretary Lisa Nandy said party manifesto promises “matter,” suggesting support for Labour’s new deputy leader who opposes plans for an income tax rise at the budget later this month.”

POLITICS (TIMES): “David Lammy has privately urged the prime minister to rein in his overseas travel, warning that frequent trips abroad risked distracting him from urgent challenges at home.”

DEFENCE (BBC): “Britain is providing military support to Belgium after a series of suspected Russian drone incursions into its airspace, the new chief of the defence staff has said.”

ECONOMY (TIMES): “One in six employers expect artificial intelligence to reduce the size of their workforce over the next year, amid weak employer confidence, according to new research.”

EU

EU (POLITICO): “The European Commission proposed several changes to its next seven-year EU budget in an effort to avert a rebellion in the European Parliament, according to a document seen by POLITICO. The Commission’s move comes before a crucial virtual meeting on Monday between Commission President von der Leyen, European Parliament President Metsola and Danish Prime Minister Frederiksen, whose country holds the rotating presidency of the Council of the EU.”

TRADE (POLITICO): “Beijing will grant exemptions to its licensing requirements provided that purchasers promise to use the chips only for civilian purposes, EU Trade Commissioner Maroš Šefčovič said.”

TRADE (POLITICO): ““We were informed by China that they will enable the resumption of supplies from Chinese factories from Nexperia,” Dutch Prime Minister Dick Schoof told Bloomberg.”

EU/UKRAINE (POLITICO): ““Slovakia won’t take part in any legal or financial schemes to seize frozen assets if those funds would be spent on military costs in Ukraine,” Fico said, Bloomberg reported, citing the interview with STVR. The EU is trying to agree on a plan to use revenues from immobilized Russian assets to provide a €140 billion loan to Ukraine, without seizing the assets.”

RUSSIA (POLITICO): “Sergey Lavrov, the veteran Russian foreign minister, said he’s ready to hold an in-person meeting with U.S. Secretary of State Marco Rubio but insisted that Moscow’s interests need to be taken into account when discussing the war in Ukraine.”

UKRAINE (BBC): “25 locations across Ukraine, including the capital city Kyiv, were hit, leaving many areas without electricity and heating. Prime Minister Yulia Svyrydenko said on Telegram that major energy facilities were damaged in the Poltava, Kharkiv and Kyiv regions, and work was under way to restore power.”

HUNGARY (BBC): “Donald Trump has exempted Hungary from sanctions over its continued purchases of Russian oil and gas for one year, a White House official has confirmed to BBC News. Earlier, the US president said he would consider an opt-out for Hungarian Prime Minister Viktor Orban.”

US

GOVERNMENT (BBG): “The record-breaking US government shutdown is nearing an end after a group of moderate Senate Democrats agreed to support a deal to reopen the government and fund some departments and agencies for the next year, people familiar with the talks said.”

LEVERAGE (MNI BRIEF): High levels of debt in the U.S. financial sector pose a potential risk to stability as asset valuations remain elevated, although household and business balance sheets remain sound as does the broader banking system, the Federal Reserve said Friday.

OTHER

JAPAN (MNI INTERVIEW): A former BOJ board member shares his policy rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

JAPAN (MNI BRIEF): Bank of Japan board member Junko Nakagawa said Monday the Bank will continue raising the policy interest rate and adjusting the degree of monetary accommodation in line with improvements in economic and price developments.

JAPAN (MNI): Bank of Japan board members largely agreed on the need to raise the policy interest rate eventually, but saw no urgency to act at the Oct 29-30 meeting, preferring to confirm sustained wage momentum and the firmness of underlying inflation, according to the summary of opinions released Monday.

AUSTRALIA (BBG): “Australia’s monetary policy is being challenged by an apparent lack of spare capacity in the economy, Reserve Bank Deputy Governor Andrew Hauser said, a week after policy makers signaled an extended interest-rate pause.”

CHINA

INFLATION (MNI BRIEF): China’s Consumer Price Index unexpectedly rose 0.2% y/y in October, reversing September's 0.3% fall and beating expectations for a 0.1% drop, as policies kicked in and week-long holidays drove demand, according to data from the National Bureau of Statistics released Sunday.

INFLATION (SHANGHAI SECURITIES NEWS): “China’s consumer prices will stabilize and recover slowly amid policies boosting domestic demand and spending, as well as ending price wars, according to a report in the Shanghai Securities News on Monday, citing economists and researchers.”

CONSUMPTION (SHANGHAI SECURITIES NEWS): “China plans to allow certain former defaulters who have fully repaid their loans to restore their credit records under a policy set to take effect early next year, according to a report by Shanghai Securities News Monday.”

MNI: PBOC Net Injects CNY41.6 Bln via OMO Monday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY119.9 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY41.6 billion after offsetting maturities of CNY78.3 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.4357% at 09:31 am local time from the close of 1.4130% on Friday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 52 on Friday, compared with the close of 50 on Thursday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.0856 Mon; +1.52% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0856 on Monday, compared with 7.0836 set on Friday. The fixing was estimated at 7.1191 by Bloomberg survey today.

MARKET DATA

CHINA OCT. CPI +0.2% Y/Y; EST. -0.1%; SEP. -0.3%

CHINA OCT. PPI -2.1% Y/Y; EST. -2.2%; SEP. -2.3%

MARKETS

US TSYS: Sell Off Gathers Pace in PM Trading on Shutdown Hopes

The sell off of US bonds continued into the afternoon, as bond futures all dipped. The US 10-Yr bond future is down -09 at 112-18+ and is at the mid-point below the 50-day EMA of 112-25+ and above the 100-day EMA of 112-12+.

Cash sold off as the US inches towards a resolution of the shutdown, with bonds wearing the brunt. A sharp sell off at the opening of cash trading slowed as the morning went on but gathered some pace after the lunch time break, with most maturities a further 0.5bps to 1.0bps higher in the afternoon alone.

- The 2-Yr is up +3.3bps to 3.597%

- The 5-Yr is up +3.8bps to 3.724%

- The 10-Yr is up at 4.136%, +3.7bps higher

- The 30-Yr is up +3.7bps to 4.738%.

The key auction tonight will be a US$86bn 13-week and US$77bn 26-week bills auction. The key test will be the US$42bn 10-Yr on the 13th.

There is no scheduled Tier 1 data tonight, but markets will focus predominantly on the vote to end shutdown with news that enough Democrats in the senate will vote to pass a bill to end the impasse.

JGBS: Bear-Steepener Ahead Of Tomorrow's 30Y Supply

JGB futures are weaker and near session lows, -20 compared to settlement levels.

- "JAPAN PM TAKAICHI: NOT RULING OUT SALES TAX CUT AS OPTION IN FUTURE, BUT IMMEDIATE PRIORITY IS TO COMPILE PACKAGE OF STEPS TO CUSHION BLOW FROM RISING COST OF LIVING, CHANGING SALES TAX RATE WOULD TAKE TIME, SO DECISION ON WHETHER TO DO SO WOULD NEED TO TAKE INTO ACCOUNT WAGE, INFLATION LEVELS AT THE TIME - [RTRS]"

- MNI: BOJ board members largely agreed on the need to raise the policy interest rate eventually but saw no urgency to act at the Oct 29-30 meeting, preferring to confirm sustained wage momentum and the firmness of underlying inflation, according to the summary of opinions released Monday.

- Cash US tsys are 3-4bps cheaper in today's Asia-Pac session after headlines that key US Senate Democrats will advance a GOP bill to end the government shutdown. Risk appetite is firmer.

- Cash JGBs have bear-steepened across benchmarks, with yields flat to 3bps higher. This leaves the 2/30 curve within its well-established range ahead of tomorrow’s 30-year supply. (see chart)

- The benchmark 30-year yield is 2.6bps higher at 3.13% versus the cycle high of 3.351%.

- Swap rates are 1-3bps higher.

- Tomorrow, the local calendar will see Trade balance and Bank Lending data alongside 30-year supply.

AUSSIE BONDS: Cheaper With YM1 Testing Support

ACGBs (YM -5.0 & XM -5.0) are weaker with US tsys after headlines that key US Senate Democrats will advance a GOP bill to end the government shutdown. Risk appetite is firmer.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at +26bps.

- The bills strip has bear-steepened, with pricing -2 to -5.

- The main takeaway from RBA Deputy Governor Hauser's Q&A today was that the economy could already be close to trend growth, and therefore, supply constraints make further rate cuts difficult.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at an 8% probability, with a cumulative 16bps of easing priced by mid-2026.

- Tomorrow, the local calendar will see Westpac Consumer and NAB Business Confidence data.

- However, the highlight of this week's AUS calendar will be Thursday's October jobs data. The unemployment rate rose 0.2pp to 4.5% in September.

- Last month's weak employment data triggered a solid ACGB rally, but those gains were more than fully reversed after the much hotter-than-expected Q3 CPI report. YM1 is currently testing horizontal support at 96.28 (see chart).

- This week, the AOFM plans to sell A$1200mn of the 4.25% 21 December 2035bond on Wednesday and A$800mn of the 1.75% 21 November 2032 bond on Friday.

Bloomberg Finance LP

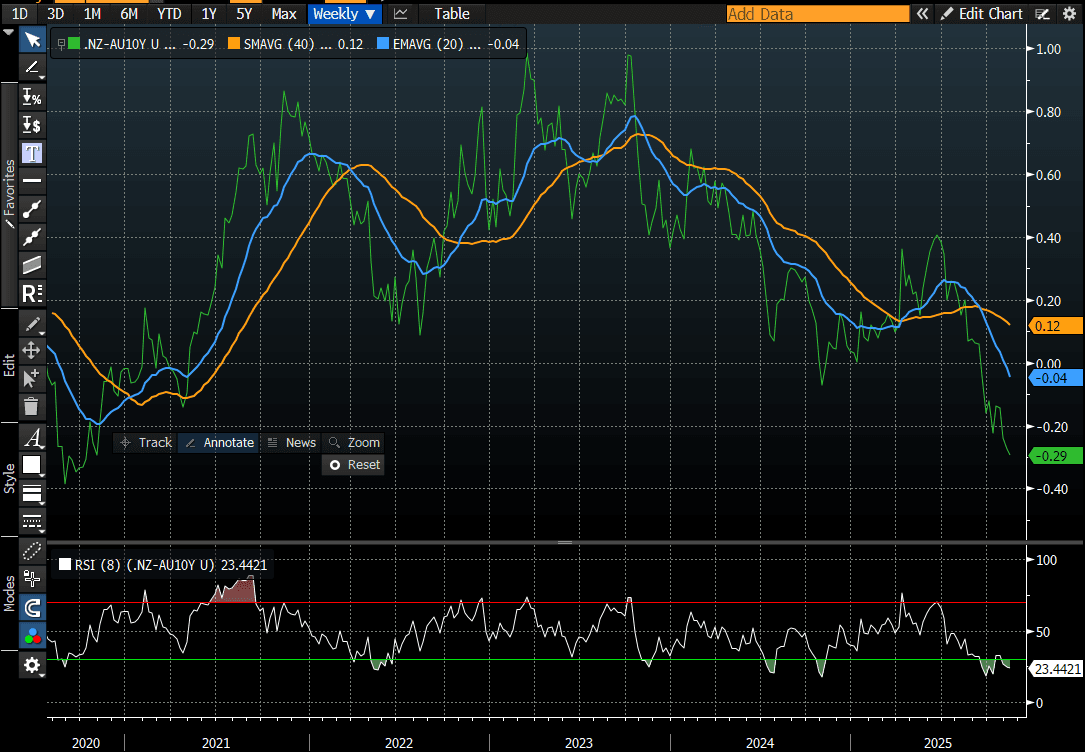

BONDS: Bear-Steepener, NZ-AU 10Y Diff Lowest Since 2020

NZGBs closed showing a modest bear-steepener, with benchmark yields flat to 2bps higher.

- NZGBs outperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 2bps and 4bps tighter, respectively.

- At -29bps, the NZ-AU differential is at its lowest since 2020. (see chart)

- Swap rates closed flat to 2bps higher.

- RBNZ dated OIS pricing closed little changed across meetings. 28bps of easing is priced for November, with a cumulative 37bps by February 2026.

- Tomorrow, the local calendar will see the RBNZ's Inflation Expectations data.

- On Thursday, the NZ Treasury plans to sell NZ$250mn of the 4.50% May-30 bond, NZ$150mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

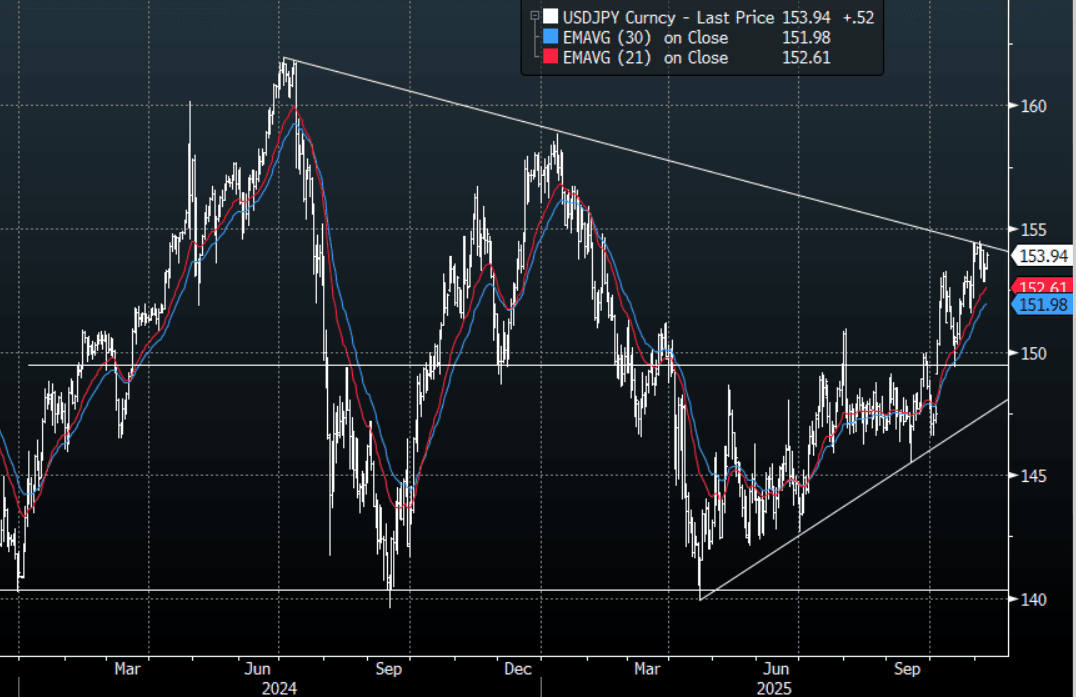

JPY: Asia-Pac: USD/JPY Challenging 154.00 Again After Turnaround In Risk

The USD/JPY range today has been 153.45 - 154.03 in the Asia-Pac session, it is currently trading around 153.95, +0.35%. The pair initially gapped higher on the Asian open as reports of a potential deal on the US shutdown made the rounds; it has continued to build on these initial gains as these reports of Dems crossing the aisle have been confirmed. USD/JPY found solid demand around the 153.00 area on Friday again, this positive scenario returns the focus back toward the 154-155 area resistance area once more. A sustained break above is needed to potentially see the uptrend regain upward momentum, the focus would then turn toward the 160 area where I would start to become wary of intervention risks.

- "JAPAN PM TAKAICHI: NOT RULING OUT SALES TAX CUT AS OPTION IN FUTURE, BUT IMMEDIATE PRIORITY IS TO COMPILE PACKAGE OF STEPS TO CUSHION BLOW FROM RISING COST OF LIVING, CHANGING SALES TAX RATE WOULD TAKE TIME, SO DECISION ON WHETHER TO DO SO WOULD NEED TO TAKE INTO ACCOUNT WAGE, INFLATION LEVELS AT THE TIME - [RTRS]"

- MNI: BOJ board members largely agreed on the need to raise the policy interest rate eventually, but saw no urgency to act at the Oct 29-30 meeting, preferring to confirm sustained wage momentum and the firmness of underlying inflation, according to the summary of opinions released Monday.

- Options : Close significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : none - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

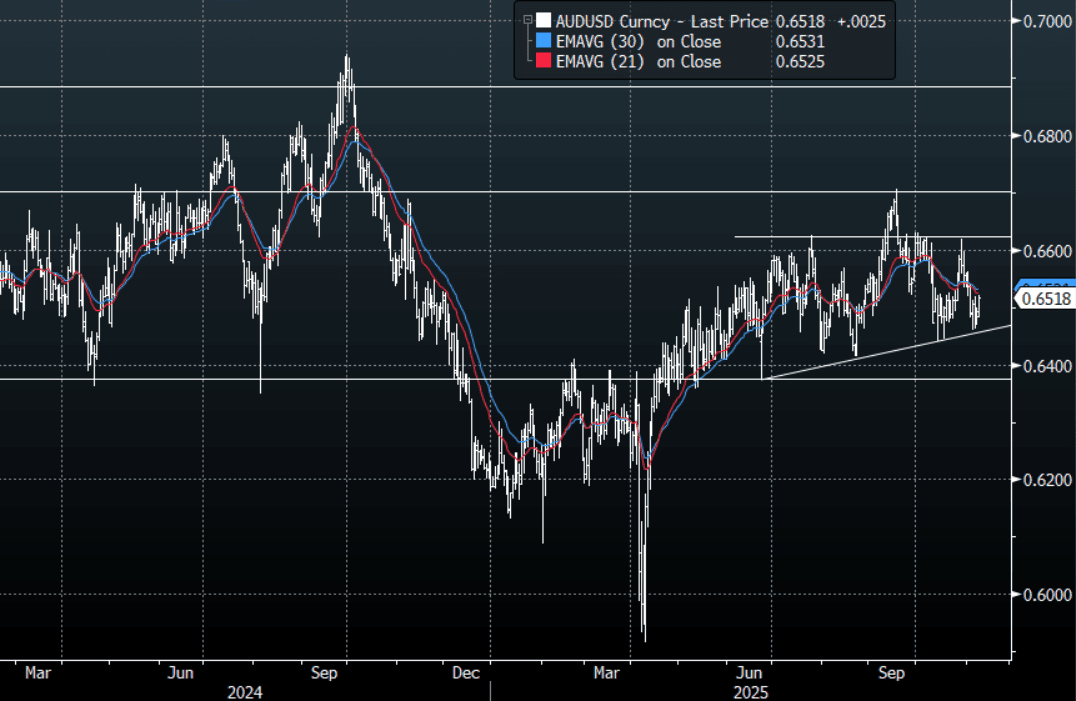

AUD: Asia-Pac: AUD/USD Builds On Support As Risk Turns Higher, Eyes 0.6550

The AUD/USD has had a range today of 0.6483 - 0.6522 in the Asia- Pac session, it is currently trading around 0.6520, +0.40%. A combination of what looks like the end of the US shutdown and better China Inflation data has seen the AUD trade with a clear bid tone to start the week. The AUD/USD has found support and bounced nicely off the 0.6450 area. If risk continues to build on this change in sentiment expect the AUD to remain supported, resistance is around the 0.6550 area. A break above 0.6550 is needed to turn the focus back toward the 0.6650/0.6700 area.

- "SENATE HAS VOTES TO ADVANCE BILL TO END SHUTDOWN" - BBG

- China Inflation: Over the weekend, we had Oct inflation data, which was stronger than expected. Notably, CPI rose 0.2%y/y, against a -0.1% forecast and -0.3% prior outcome. PPI deflation remained at -2.1%y/y, but was a slight improvement on the Sep outcome. On a monthly basis, CPI rose 0.2%, edging up from September's 0.1% growth. Core CPI, which excludes food and energy, rose 1.2% from September's 1.0%, marking the sixth consecutive month of increase and reaching its highest level since Mar 2024

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6560(AUD447m), 0.6615(AUD 464m), 0.6630(AUD462m). Upcoming Close Strikes : 0.6500(AUD1.22b Nov 12), 0.6530(AUD882m Nov 12)- BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia- Pac: NZD/USD Still Trades Heavy But Wary Of Positioning

The NZD/USD had a range today of 0.5616 - 0.5634 in the Asia-Pac session, going into the London open trading around 0.5630, +0.15%. A combination of what looks like the end of the US shutdown and better China Inflation data has seen the NZD start the week drifting back up off its lows. The NZD continues to trade heavy but it is prudent to be wary of what the reaction to the end of the US shutdown might look like. I am a little wary of positioning in the NZD market though I still suspect any decent bounce will again attract sellers. The first sell area on a pullback would be around 0.5750 and then the more pivotal 0.5850 area.

- "NZ'S PM LUXON WANTS BANKS TO PASS ON RBNZ RATE CUTS FASTER" - BBG

- Bloomberg reports the NZ Treasury says, “New Zealand Economic Recovery Still Emerging. New Zealand’s economy has more spare capacity than previously assumed while a broad-based recovery is still emerging, the Treasury Department says in its Fortnightly Economic Update.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5380(NZD460m Nov 13), 0.5600(NZD538m Nov12), 0.5800(NZD461m Nov 12) - BBG

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: Asia-Pac FX: USD Drifts Higher In Asia On USD/JPY Move

The BBDXY has had a range today of 1219.55 - 1221.03 in the Asia-Pac session; it is currently trading around 1220, +0.10%. The USD opened stronger in Asia on reports the US shutdown might be ending, this saw risk and Yen-crosses gap higher on the open. The USD/JPY movement dominated the Asian session but I suspect the USD will be sold against risk currencies like the AUD & NZD and even the EUR into the London open should risk build on this initial reaction. Intra-day I suspect sellers should re-emerge back toward the 1223.50 area, the first real buy zone is back toward the 1215 area. Look for the USD to do some work and chop around within the 1215-1230 range. "SENATE HAS VOTES TO ADVANCE BILL TO END SHUTDOWN" - BBG

- EUR/USD - Asian range 1.1542 - 1.1562, Asia is currently trading 1.1550. The pair continued to build on its support below 1.1500, I suspect rallies will now find sellers toward the 1.1650 area initially. This has been the pivot with the larger 1.1400-1.1900 range over the past few months.

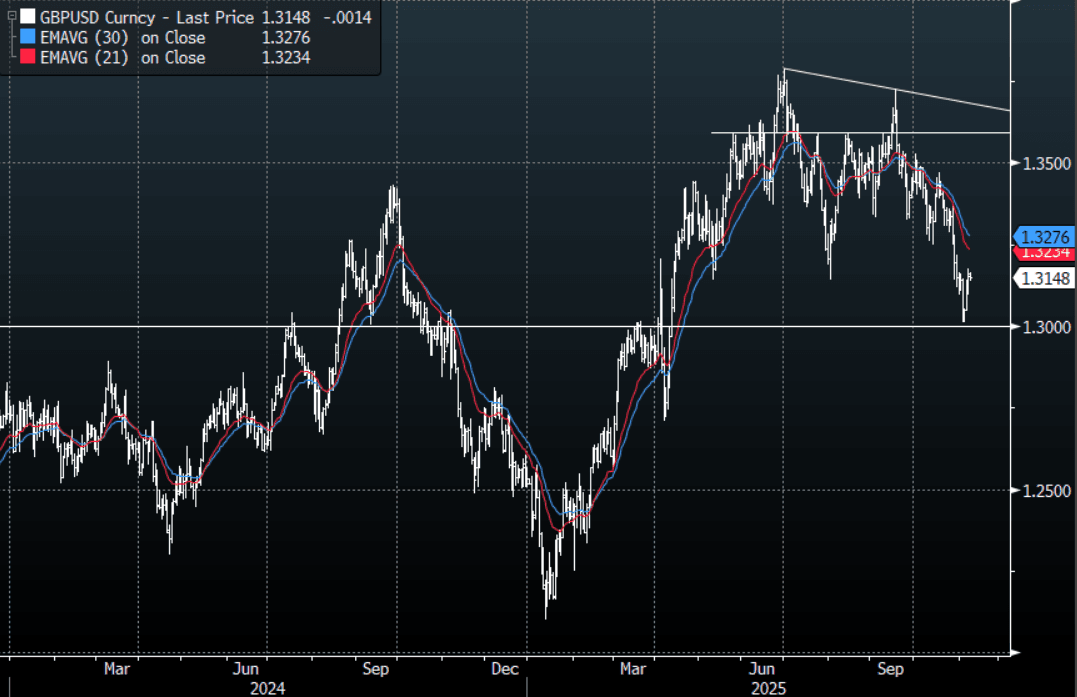

- GBP/USD - Asian range 1.3137 - 1.3164, Asia is currently dealing around 1.3145. The pair continues to build on its bounce off the 1.3000 area. I continue to favor fading rallies though as GBP looks to have put in a medium term top. I suspect the 1.3250-1.3300 area is the place to fade if we see that level again.

- Cross asset : SPX +0.70%, Gold $4050, US 10-Year 4.1340%, BBDXY 1220, Crude Oil $60.20

- Data/Events : EZ Sentix Investor Confidence

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Tech Bounces Again, NIFTY 50 Nears Key Technical

The sell off in Asia's tech sector appears short lived as bell weather shares like SK Hynix in Korea, jump over 7% today. Last week's decline was the worst in over six months for the tech sector with many key names delivering record breaking gains. Last week's falls started in Wall Street and wasn't helped by warnings from the Korea exchange and is a reminder of stock bubbles of the past. Some key bourses in Asia (like the KOSPI and TAIEX) face concentration risk with the tech sector given their surge, as the sector's share of the index reaches new highs. Risk appetite returned today as it appears the US shutdown could be ending, with most major bourses higher today.

- The NIKKEI delivered gains of +0.93% to reach 50,755, just back from last week's high of 50,752 whilst the KOSPI rose almost 3.00% to reach a new recover more than half of last week's falls.

- In China the story was more mixed with the onshore offshore divide on show. The Hang Seng is up +0.61% whilst onshore bourses are all down modestly. The CSI 300 fell -0.24% to 4,667 but remains above the 20-day EMA of 4,639.

- The FTSE Malay KLCI is up +0.63% whilst the JCI in Indonesia +0.22%. Both retain their positions above all major moving averages.

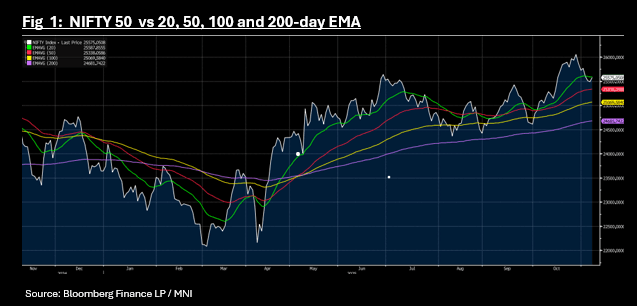

- In India, as P/E's continue to look stretched and at year end forecasts, the NIFTY 50 fell modestly last week despite the turmoil elsewhere. The falls however took it below the 20-day EMA for the first time since September. The gains this morning takes it to 25,568, just below the 20-day EMA of 25,587.

OIL: Positive Risk Sentiment Drives Oil Higher As US Shutdown May End Soon

News of an imminent end to the lengthy US government shutdown has boosted risk sentiment in Monday’s trading and thus helped to drive oil prices higher. The impasse was seen to be costly to the economy and would as a result weigh on energy demand. WTI is up 0.8% to $60.25/bbl, close to the intraday high, after falling to $59.74 early in the session. Brent is 0.7% higher at $64.08/bbl after falling to $63.60. Prices remain range bound as the market looks for new information.

- News from the US says that enough Democrats in the senate will vote to pass a bill to end the government shutdown which is in its sixth week.

- The US dollar is slightly higher while the S&P e-mini is up 0.7% and copper +1.6%.

- The market will monitor monthly reports closely this week for any deterioration in the excess supply situation. The IEA increased its 2026 surplus forecast in its October monthly report. It publishes updates on 13 November, while its annual outlook, EIA short-term energy outlook & OPEC report are out 12 November.

- The uncertain impact of additional sanctions against Russia has been providing a floor to oil prices. However, US President Trump has given Hungary a one year exemption from the US sanctions on Russia’s Rosneft and Lukoil, as “it’s very difficult for him [Hungarian PM Orban] to get the oil and gas from other areas”. According to Bloomberg, Hungary imports 90% of its oil from Russia.

Gold Rallies On Hopes US Data Releases Will Clarify Fed Outlook

Gold has rallied 1.3% to $4054.0/oz today despite a slightly stronger US dollar, higher yields and a 0.7% rise in the S&P e-mini. It appears to be a delayed reaction to the softer-than-expected November Uni of Michigan consumer sentiment released on Friday. The move may also be in anticipation of the delayed US data printing softer following reports that a deal has been reached to end the US government shutdown impasse. Thus increasing expectations of further Fed easing.

- Gold broke above initial resistance at $4046.2, 31 October high, opening up $4161.4, 22 October high. It reached a high of $4055.50 but has mainly traded around $4040-4050.

- News from the US says that enough Democrats in the senate will vote to pass a bill to end the government shutdown which is in its sixth week.

- Fed Chair Powell said another rate cut in December is not a given and so the market has around a 60% chance of one priced in with 100% by January. Monetary easing supports non-interest bearing gold.

- The PBoC built its gold reserves in October for a twelfth consecutive month, according to Bloomberg. There was an 8% y/y fall in gold consumption in China in the year to September according to the Gold Association.

- Silver is 1.8% higher at $49.18 but has been unable to break above initial resistance at $49.456, 23 October high. It reached $49.299 earlier.

- Later the Fed’s Daly and Musalem speak as well as BoE’s Lombardelli. There are no material data releases.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 10/11/2025 | 0700/0800 | *** | CPI Norway | |

| 10/11/2025 | 0700/0800 | ** | Private Sector Production m/m | |

| 10/11/2025 | 0910/0910 | BOE Lombardelli at BOE/Ghana Central Bank Conference | ||

| 10/11/2025 | - | *** | Money Supply | |

| 10/11/2025 | - | *** | New Loans | |

| 10/11/2025 | - | *** | Social Financing | |

| 10/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 10/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 10/11/2025 | 1700/1200 | *** | USDA Crop Estimates - WASDE | |

| 10/11/2025 | 1800/1300 | *** | US Note 03 Year Treasury Auction Result | |

| 11/11/2025 | 2350/0850 | Balance of Payments | ||

| 11/11/2025 | 0001/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 11/11/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 11/11/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - AWE & Unemployment | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 11/11/2025 | 0700/0700 | *** | Labour Market - Payrolls & Claimants | |

| 11/11/2025 | 0820/0920 | ECB Lagarde Video Message at Bank of Albania | ||

| 11/11/2025 | 0830/0930 | Riksbank Minutes | ||

| 11/11/2025 | 0830/0830 | BOE Greene in Panel at UBS European Conference | ||

| 11/11/2025 | 1000/1100 | *** | ZEW Current Expectations Index | |

| 11/11/2025 | 1100/0600 | ** | NFIB Small Business Optimism Index | |

| 11/11/2025 | 1200/0700 | ** | Brazil Final CPI | |

| 11/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index |