MNI EUROPEAN OPEN: Trump Talks To Asia Pac Leaders

EXECUTIVE SUMMARY

- ZELENSKY WELCOMES AMENDMENTS TO PROPOSED PEACE PLAN - BBC

- TRUMP TALKS TO XI, THEN TAKAICHI AS US WALKS TAIWAN TIGHTROPE - BBG

- TRUMP SAID HE WILL VISIT CHINA IN APRIL - MNI BRIEF

- A CHINA GOVT ADVISOR ON CHINA AI ENERGY DEMAND - MNI INTERVIEW

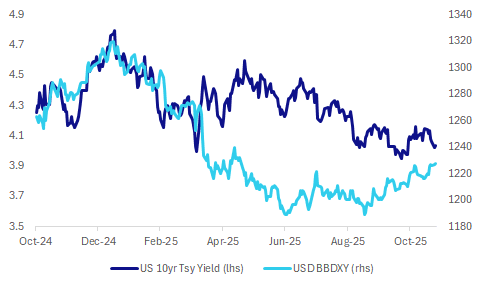

Fig 1: USD BBDXY Index & Nominal 10yr Tsy Yield

Source: Bloomberg Finance L.P./MNI

UK

POLITICS (TIMES): “A “bruised” government left “with little room for manoeuvre” is presiding over an incoherent strategy, the outgoing chairman of the CBI has said. Rupert Soames, in closing remarks to the business lobby group’s annual conference in London, said “few would have predicted how far and how fast the government has lost its confidence and room for manoeuvre”.”

POLITICS (TIMES): “Allies of Wes Streeting are calling for a coronation rather than a contest to install him as Labour leader, probably after the May elections. Ministers and senior MPs backing the health secretary warned against a lurch to the left and said privately that a rival candidate such as Angela Rayner would be too radical and would face greater pressure to call a snap general election.”

EU

UKRAINE (BBC): “Ukrainian President Volodymyr Zelensky has welcomed proposed changes to the controversial 28-point peace plan for ending the war with Russia. "Now the list of necessary steps to end the war can become doable..." he said on Telegram. "Many correct elements have been incorporated into this framework."”

FISCAL (MNI): EU governments will find further fiscal consolidation efforts even more difficult to achieve as a result of the recent fall in inflation and higher refinancing rates on their debt, the European Commission will say on Tuesday in its European Semester package.

UKRAINE (DW): “The head of the Foreign Affairs Committee in the Estonian Parliament, Marko Mihkelson, told DW on Monday that the Donald Trump's peace plan, designed to end the war in Ukraine, would not bring about lasting peace and fits Moscow's "strategic goals."”

TRADE (POLITICO): “The EU’s push for the U.S. to scrap its tariffs on steel and aluminum has opened the door to an old demand from Washington: Loosen your digital rulebook, and we’ll meet you halfway.”

BELGIUM (BBC): “Belgium is bracing for widespread disruption across sectors including public transport and schools this week as unions hold a three-day national strike. The action was called in response to Prime Minister Bart De Wever's attempts to shrink Belgium's debt by changing labour laws and reforming unemployment benefits and pensions.”

GERMANY (MNI INTERVIEW): German energy price caps will have only limited positive effects on growth unless public spending is redirected towards infrastructure investment and away from consumption, a member of the German Council of Economic Experts told MNI.

US

GEOPOLITICS (BBG): " Donald Trump held back-to-back calls with the leaders of China and Japan, signaling the US president’s desire to balance ties with Asia’s top economies as tensions rise over Taiwan."

US/CHINA (MNI BRIEF): U.S. President Donald Trump said on Tuesday via Truth Social that he has agreed to visit Beijing in April and has invited Chinese President Xi Jinping for a state visit later next year, following a phone call between the two leaders.

DATA (BBG): "The Bureau of Economic Analysis announced it will release its initial estimate of third quarter US gross domestic product at 8:30 a.m. in Washington on Dec. 23."

OTHER

CANADA (BBC): “Canada's Prime Minister Mark Carney says trade talks with the US will resume "when it's appropriate", dismissing questions about his most recent communication with President Donald Trump.”

CANADA (MNI BRIEF): Canada has "cards" to play against President Donald Trump's threats of economic domination because America has just seven years of reserves on hand and its biggest source of imports comes from north of the border, Energy Minister and former Goldman Sachs banker Tim Hodgson told lawmakers Monday.

INDIA (BBG): "The International Monetary Fund is expected to soon announce a change in how it classifies India’s exchange rate regime, according to people familiar with the matter, two years after the Washington-based lender upset the local central bank by suggesting it was intervening too heavily in the currency market."

JAPAN (BBG): "In a letter to the United Nations, Japan criticized an earlier missive from China as mis-representing the nature of remarks Prime Minister Sanae Takaichi made on Taiwan, saying Beijing’s letter was “inconsistent with the facts and unsubstantiated.”

CHINA

ELECTRICITY (MNI INTERVIEW): A government energy advisor provides insight into China AI energy demand and petrochemical transition. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

CHINA/US (XINHUA): “Chinese President Xi Jinping said on Monday that during a phone call with U.S. President Donald Trump, China and the U.S should keep up the momentum in ties and continue to move forward on the basis of equality, respect and mutual benefit, the Xinhua News Agency reported.”

LIQUIDITY (YICAI): “The People’s Bank of China is expected to continue injecting medium-term liquidity through outright reverse repos and the medium-term lending facility, following four consecutive months of CNY600 billion in net monthly injections, Yicai.com reported, citing Wang Qing, an analyst at Golden Credit Rating.”

HOUSING (SECURITIES DAILY): “The total transaction volume of new and second-hand homes in 30 key cities remained at 274 million square meters in the first 10 months, basically the same as same period last year, indicating a sign of stabilisation, Securities Daily reported citing data by China Real Estate Information Corporation.”

MNI: PBOC Net Drains CNY105.4 Bln via OMO Tuesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY302.1 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY105.4 billion after offsetting maturities of CNY407.5 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4096% at 09:32 am local time from the close of 1.4703% on Monday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 51 on Monday, compared with the close of 50 on Friday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.0826 Tues; +2.32% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.0826 on Tuesday, compared with 7.0847 set on Monday. The fixing was estimated at 7.1047 by Bloomberg survey today.

MARKET DATA

SOUTH KOREA NOV. CONSUMER CONFIDENCE 112.4; OCT. 109.8

MARKETS

US TSYS: Give Back Some of O/N Gains: Eyes Turn to Data Tonight

US bond futures are doing very little today with volumes moderate. The US 10-Yr is flat at 113-11, consolidating it's position above all major moving averages. With data releases continuing, even though some are viewed as stale, the market is highly sensitive for FED members comments.

We saw 2,349 of FVZ5 traded today traded at 109-21 1/4 early afternoon, which had followed a sell of 2,945 of TYZ5 in the morning session at 113-11 and a buy of 2,845 of TUZ5 at 104-15.

Cash is more active with yields higher across the curve by 0.5bps to 1.0bps, with intermediate maturities the worst performers.

- The 2-Yr is at 3.512% (+1.3bps)

- The 5-Yr is at 3.607% (+1.4bps)

- The 10-Yr is at 4.038% (+1.2bps)

- The 30-Yr is at 4.679% (+0.7bps)

Tonight sees a US$85bn 6-week bill, US$50bn 52-week bill, US28bn 2-Yr FRN and US$70bn 5-Year auctions.

This week's data calendar picks up overnight, highlighted by retail sales and PPI inflation for September, although the Conference Board's consumer survey and its labor differential should also command attention, with indicators looking for solid retail sales numbers. PPI data likely viewed as stale and not market relevant. For Wednesday then sees weekly jobless claims brought forward for Thanksgiving, including of note the payrolls reference period for continuing claims in November, along with the catching up of the September durable goods report, the MNI Chicago PMI for November and the Fed's Beige Book.

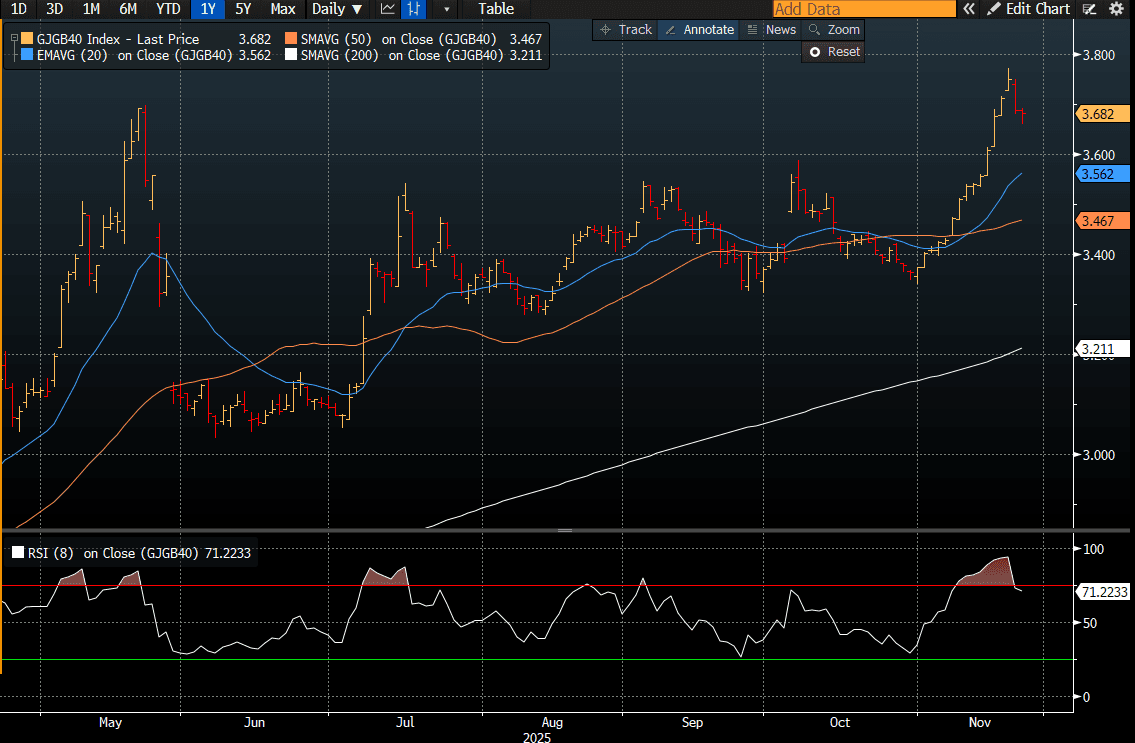

JGBS: 40Y Outperforms Ahead Of Tomorrow's Supply

JGB futures are weaker, -21 compared to settlement levels, and at lows after a choppy start to the session.

- Local calendar has been light, with Dept Sales data due later.

- Japanese PM Takaichi has confirmed she has spoken with US President Trump via a telephone call this morning. The call was made at the request of US President Trump. It came after US President Trump and Chinese President Xi spoke on Monday. Japan/China tensions have been elevated in recent weeks in the aftermath of Takaichi's comments in relation to Taiwan.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session.

- Cash JGBs have twist-flattened across benchmarks, with yields 2.7bps higher (7-year) to 0.6bp lower (40-year), ahead of tomorrow's 40-year supply.

- The benchmark 40-year yield is at 3.682% versus the cycle high of 3.772%, with the 2/40 yield curve currently positioned at the midpoint of its recent range. (see chart)

- The last 40-year auction was on September 25. That bond auction drew a bid-to-cover ratio of 2.6x compared with 2.127x at the prior auction. At that time, the 40-year bond yielded 3.30%.

- Swap rates are ~2bps higher across the curve.

- Tomorrow, the local calendar will see PPI Services, Machine Tool Orders and Leading/Coincident Index data alongside 40-year supply.

Source: Bloomberg Finance LP

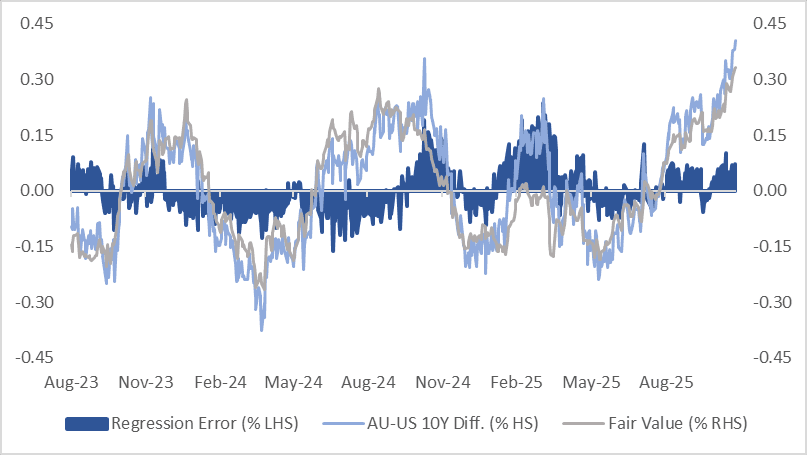

AUSSIE BONDS: AU-US 10Y Diff In Focus As It Pushes Further Out Of Range

ACGBs (YM -0.5 & XM +1.0) are slightly mixed ahead of tomorrow’s October CPI data.

- A partial basket has been published for a while, but the focus has remained on the quarterly series, as they contained updates for all components. RBA Governor Bullock said that the Board will continue to concentrate on quarterly CPI for now as it assesses the trends in the new monthly CPI.

- Cash US tsys are ~1bp cheaper in today’s Asia-Pac session.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +40bps — its widest level since September 2022.

- This move has pushed the differential decisively above the ±30bps range that had persisted since November 2022.

- However, a simple regression of the 10-year yield differential against the AU–US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is around 7bps too wide relative to fair value.

- Even so, with markets still pricing a 45% chance of an RBA cut by mid-2026, despite recent RBA commentary, it may be premature to position for the narrowing of the differential.

- The bills strip is little changed.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 11bps of easing priced by mid-2026.

Bloomberg Finance LP / MNI

BONDS: NZGBS: Slightly Richer Ahead Of Tomorrow's RBNZ Policy Decision

NZGBs closed 1-2bps richer across benchmarks ahead of tomorrow’s RBNZ Policy Decision.

- The RBNZ is likely to cut rates 25bp on 26 November to 2.25%, edging below its estimate of "neutral". 2/24 analysts on Bloomberg are forecasting 50bp. The data released since the October decision have been consistent with a gradual but soft recovery and, importantly, close to the RBNZ's August expectations, and thus there is unlikely to be another outsized 50bp easing.

- Total new residential mortgage lending in New Zealand rose to NZ$8.36 billion in October from NZ$8.18 billion in September, according to data from the RBNZ. – MTN via BBG

- RBNZ-dated OIS pricing is mostly unchanged across meetings today ahead of tomorrow’s policy decision.

- Notably, pricing is 6–15bps softer across meetings compared with levels before the October 9 meeting, November 2025 leading.

- Most of that decline occurred on the day the RBNZ cut the OCR by 50bps; pricing has been relatively stable since.

- The market currently prices 27bps of easing for tomorrow’s meeting and a cumulative 35bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-34 bond.

Bloomberg Finance LP

FOREX: USD - BBDXY Trades Firm As Risk-On Rally Fades

The BBDXY has had a range today of 1226.03 - 1227.37 in the Asia-Pac session; it is currently trading around 1227, +0.05%. This week the standout has been the huge bounce in global risk together with a repricing of a potential US December rate cut, as of yet though there has been a distinct lack of a reaction from the USD, yet ? While the price remains above 1223/24 I would be skewed toward expressing a long, looking for a retest of the 1230-1240 area at some point. A move back through this support and we are back in the 1210/15-1230/35 range.

- EUR/USD - Asian range 1.1519 - 1.1530, Asia is currently trading 1.1515. The pair continues to consolidate around the 1.1500 area. While the EUR remains capped below the 1.1545-65 area the bears remain in charge, and while that is the case I would be skewed short. Above there and the market will start to refocus on the 1.1650 area.

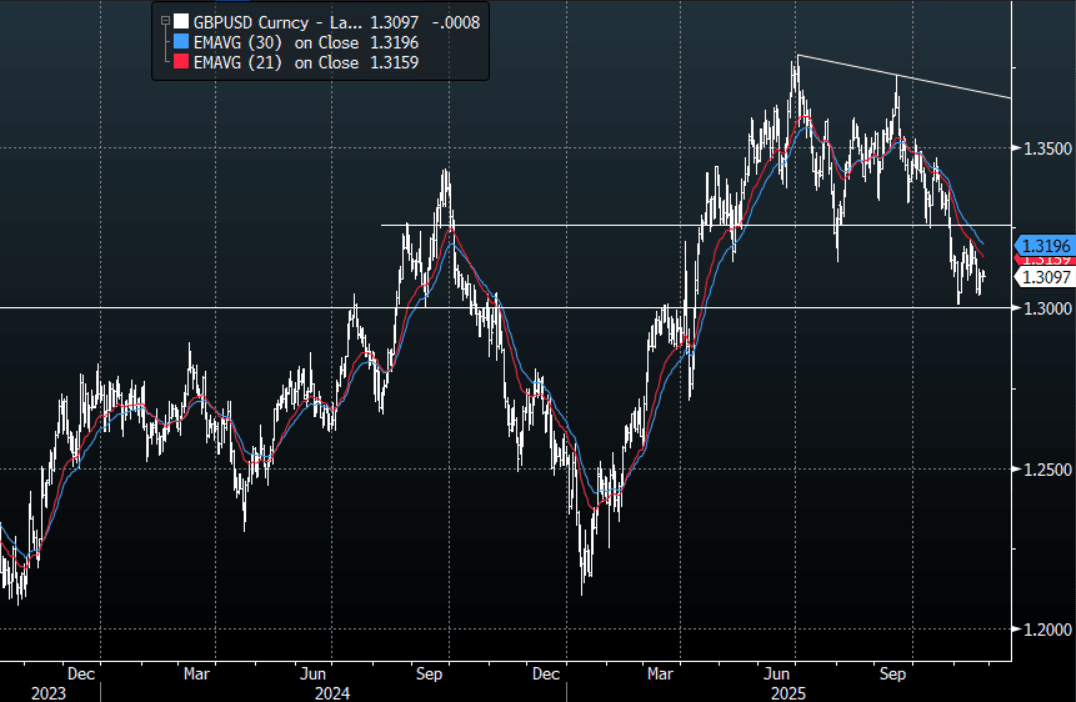

- GBP/USD - Asian range 1.3102 - 1.3116, Asia is currently dealing around 1.3100. The pair traded sideways overnight, unable to move back above the 1.3130-60 area. I continue to favor fading rallies, as GBP looks to have put in a medium term top. While below the 1.3130-60 area I remain skewed toward shorts, a break above here could signal better entry levels back toward the 1.3250 area. Lots of event risk this week with the budget presented on the 26th November.

- Cross asset : SPX -0.02%, Gold $4145, US 10-Year 4.036%, BBDXY 1227, Crude Oil $58.59

- Data/Events : Germany GDP, EZ EU27 New Car Registrations, France Consumer Confidence, Spain PPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Consolidates On A 156 Handle

The USD/JPY range today has been 156.56 - 156.98 in the Asia-Pac session, it is currently trading around 156.80, -0.05%. The pair has drifted a little lower in a very quiet session even with Japan returning. The price action looks pretty clear for now though and Japanese officials would have to do something extraordinary to change the narrative. The path of least resistance is now a higher USD/JPY and I suspect any dips back toward the 154-155 area would be used as buying opportunities. Shorter term first support looks to be towards 156.00-156.30, and topside is 157.00-157.30 a break of which would open up a retest of the 158.00 area. The large stimulus package has been approved but the market is asking how do you fund this extravagance when you have the highest debt-GDP ratio in the world and yields are exploding higher.

- Chester Ntonifor of BCA research pointed to Yen positioning as a reason this move could still have more to go, “One of the reasons the yen has been weakening by more than dollar strength will suggest is that a lot of speculators have just started to unwind their long positions.”

- Takaichi Speaks With Trump Amid China/Japan Tensions: Japan PM Takaichi has confirmed she has spoken with US President Trump via a telephone call this morning. The call was made at the request of US President Trump. It came after US President Trump and China President Xi spoke on Monday. Japan/China tensions have been elevated in recent weeks in the aftermath of Takaichi's comments in relation to Taiwan.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($339m),156.00($909m), 157.00($433m). Upcoming Close Strikes : 154.00($2.14b Nov 26), 154.00{$1.28b Nov 28), 155.00($1.86b Nov 26) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 99 Points

AUD/USD - Drifting Lower As Risk Turns Back Down In Asia

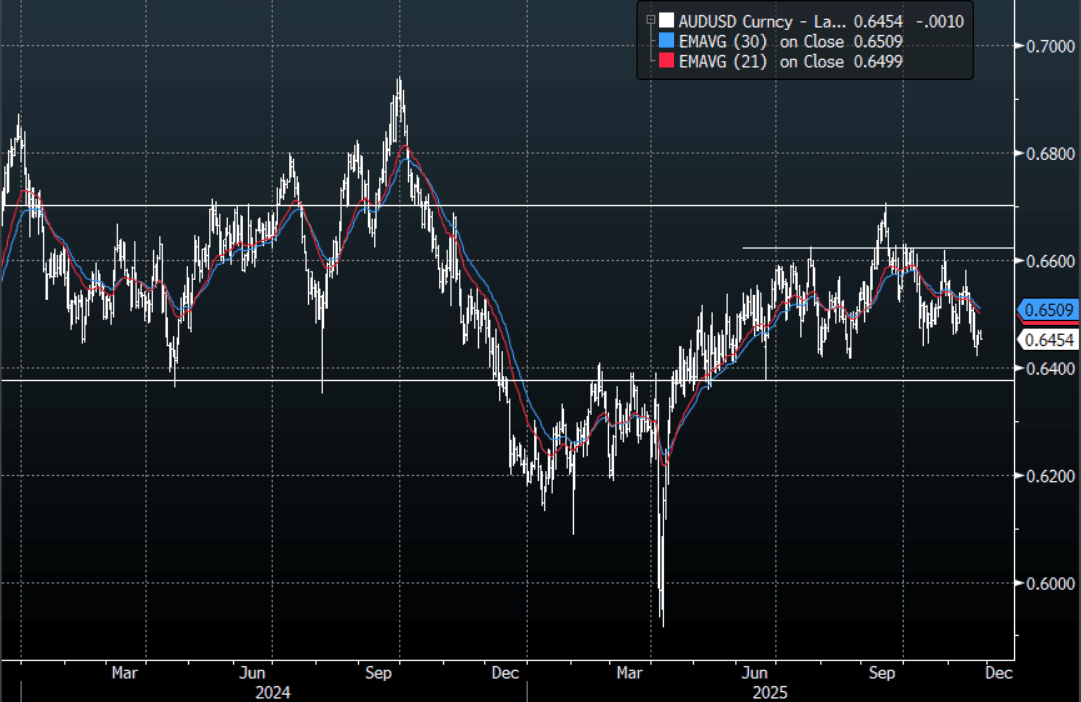

The AUD/USD has had a range today of 0.6452 - 0.6469 in the Asia- Pac session, it is currently trading around 0.6455, -0.15%. The AUD/USD has drifted lower in a quiet Asian session, where risk has not followed through with the overnight strength seen. The AUD continues to consolidate around 0.6450 but given the size of the moves overnight I would have expected a bigger reaction, are currencies lagging or do they just not believe in the rally? The 0.6440-0.6450 area continues to be supportive, a sustained break below here is needed to target the 0.6350 area. On the day, watch to see if price can move above 0.6470-90, If price cannot push back above there then its back toward testing the support.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD330m), 0.6650(AUD349m). Upcoming Close Strikes : 0.6450(AUD1.04b Nov 26), 0.6500(AUD1.07b Nov 26), 0.6535(AUD1.69b Nov 26) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD/USD - Trades Heavy Around 0.5600 As Risk-On Fizzles In Asia

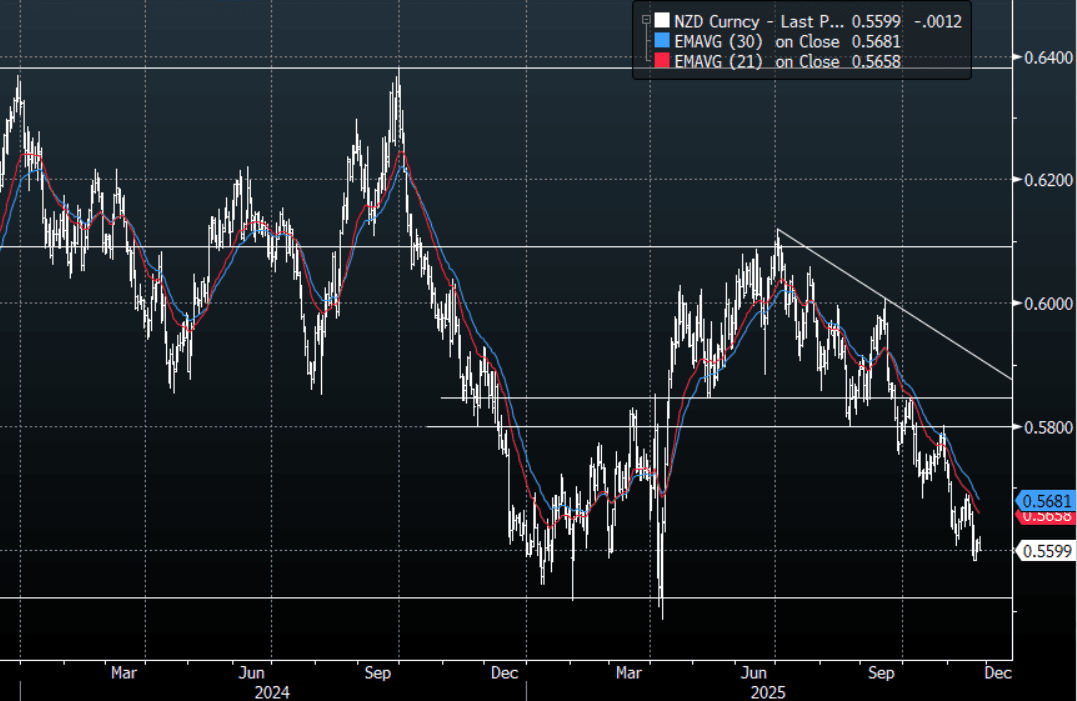

The NZD/USD had a range today of 0.5598 - 0.5622 in the Asia-Pac session, going into the London open trading around 0.5600, -0.20%. The NZD/USD has drifted lower in a quiet Asian session, where risk has not followed through with the overnight strength seen. The NZD is consolidating around the 0.6600 area and like the AUD considering the move in risk overnight I am a little surprised it didn't try to push a little higher. The RBNZ this week will be important as they start to approach neutral, the market is already short NZD so I am mindful of any dovish disappointment. On the day though, while 0.5635-50 caps price the bears remain in charge, a move back below 0.5580 and the market will start lasering onto the pivotal 0.5500 area.

- MNI AU - The RBNZ is likely to cut rates 25bp on 26 November to 2.25%, edging below its estimate of "neutral". 2/24 analysts on Bloomberg are forecasting 50bp. The data released since the October decision have been consistent with a gradual but soft recovery and importantly close to the RBNZ's August expectations and thus there is unlikely to be another outsized 50bp easing.

- The focus will be on revisions to the RBNZ’s OCR path. Q1 will be the interesting quarter. There is only one meeting scheduled in Q1 on 18 February and a 2.1% would signal further easing. The market currently has 27bps of easing priced for November's meeting and a cumulative 35bps by February 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5600(NZD600m), 0.5640(NZD360m), 0.5720(NZD646m). Upcoming Close Strikes : 0.5670(NZD788m Nov 26) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 37 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China Tech Valuations Lead Bourses Higher

With Japan playing catch up today, more positive cues from Fed Speakers that a rate cut could come at the next Fed meeting has underscored equity markets today. China's major onshore bourses led the way today with Shenzhen Comp up by +1.9% with onshore press suggesting that a bounce in China's tech sector is driving returns. The tech led rally in the US thanks to Alphabet's AI upgrade announcement helped. China's tech valuations are a factor also given they haven't rallied as much as Japan and Korean AI stocks in recent months.

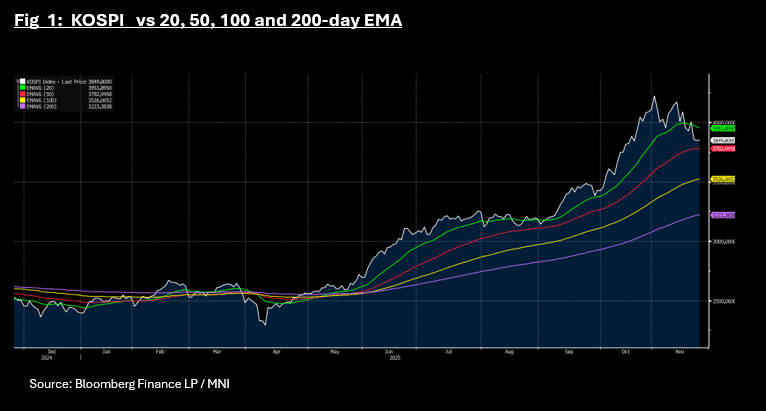

- The NIKKEI appeared to have stayed on holiday from yesterday, rising a mere +0.13% today whilst the KOSPI was flat. The KOSPI's falls in recent days now sees it at the midpoint between the 20-day EMA and the 50-day EMA, looking for a catalyst to break above or below.

- China's major bourses held centre stage with the Hang Seng up +0.62%, the CSI 300 +1.25%, Shenzhen +1.92% and Shanghai +1.1%.

- Despite outflows from Taiwan stocks gathering pace, TSMC's rise of +2.2% today helped the TAIEX rise by +1.40%

- SE Asia' major bourses were mixed with the JCI down heavily after reaching new highs yesterday. In what appeared profit taking the JCI is down -0.75%, taking the FTSE Malay KLCI with it with falls of -0.25% whereas the SE Thai is up +1.05% following very strong import data released for October with local press suggesting it has a sign of improving domestic demand.

- In India the NIFTY 50 is barely positive, unable to recover yesterday's losses despite the RBI Governor suggesting that the upcoming decision on rates could see a cut in the base rate.

OIL: Crude Lower Despite Russian Attack On Kyiv, US Inventories In Focus

After unwinding Friday’s losses on Monday, oil is down slightly during Tuesday’s APAC session but has moved in a narrow range. Brent is down 0.5% to $63.07/bbl, while WTI is 0.4% lower at $58.60/bbl, both close to their intraday troughs.

- While Ukraine developments remain important for oil, it looked through reports of a major Russian bombardment of Kyiv, which suggests that it is unlikely to agree to a revised peace plan consistent with earlier comments that Europe’s proposal “doesn’t fit us at all”. Russian obstinacy should be positive for oil prices, as it means sanctions are unlikely to be eased while the stance persists.

- The US peace plan has apparently been changed to address most of the Ukraine’s issues but disagreements over security guarantees and sovereignty are yet to be resolved. US army secretary Driscoll is meeting Russian officials in Abu Dhabi according to CBS.

- With a record oil surplus forecast for 2026, supply/demand fundamentals remain important. US industry-based inventory data are released later on Tuesday with the official EIA on Wednesday. OPEC meets 30 November to decide January production but last time said that it would hold quotas steady in Q1.

- Later delayed US September retail sales and PPI print as well as US preliminary ADP weekly employment, November Philly & Dallas Fed non-manufacturing, Richmond Fed November indices, November consumer confidence and September house prices. Also, German Q3 GDP is released and ECB’s Donnery and Cipollone speak.

Gold Range Trading Ahead Of US PPI & Retail Data Today

Gold is moderately higher on Tuesday but has range traded as it waits for US data out later today and its impact on Fed cutting expectations. The market currently has around an 86% chance of 25bp of easing on 10 December.

- Bullion is up 0.2% to $4145.0/oz, holding above initial resistance at $4132.9, after a high of $4155.81 which followed a low of $4122.70. Both the US dollar and 2-year yield are slightly higher.

- Silver is 0.3% higher at $51.54, close to the intraday peak, after falling to $51.016.

- Equities are mixed with the S&P e-mini flat, Topix down 0.3% but Hang Seng up 0.6%. Oil prices are lower with WTI -0.4% to $58.60/bbl. Copper is up 1.8%.

- Later delayed US September retail sales and PPI print as well as US preliminary ADP weekly employment, November Philly & Dallas Fed non-manufacturing, Richmond Fed November indices, November consumer confidence and September house prices. Also, German Q3 GDP is released and ECB’s Donnery and Cipollone speak.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 25/11/2025 | 0700/0800 | ** | PPI | |

| 25/11/2025 | 0700/0800 | *** | GDP (f) | |

| 25/11/2025 | 0745/0845 | ** | Consumer Sentiment | |

| 25/11/2025 | 0800/0900 | ** | PPI | |

| 25/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 25/11/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 25/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 25/11/2025 | 1330/0830 | *** | PPI | |

| 25/11/2025 | 1330/0830 | *** | PPI | |

| 25/11/2025 | 1330/0830 | *** | Retail Sales | |

| 25/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 25/11/2025 | 1330/0830 | *** | Retail Sales | |

| 25/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 25/11/2025 | 1400/0900 | ** | S&P Case-Shiller Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Quarterly Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Quarterly Price Index | |

| 25/11/2025 | 1400/1500 | ECB Cipollone Keynote at Central Bank of Ireland | ||

| 25/11/2025 | 1500/1000 | ** | NAR Pending Home Sales | |

| 25/11/2025 | 1500/1000 | *** | Conference Board Consumer Confidence | |

| 25/11/2025 | 1500/1000 | ** | Richmond Fed Survey | |

| 25/11/2025 | 1500/1000 | * | Business Inventories | |

| 25/11/2025 | 1500/1000 | * | Business Inventories | |

| 25/11/2025 | 1530/1030 | ** | Dallas Fed Services Survey | |

| 25/11/2025 | 1630/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 25/11/2025 | 1800/1300 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 25/11/2025 | 1800/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 26/11/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 26/11/2025 | 0030/1130 | *** | Quarterly construction work done | |

| 26/11/2025 | 0030/1130 | *** | CPI Inflation Monthly | |

| 26/11/2025 | 0100/1400 | *** | RBNZ official cash rate decision | |

| 26/11/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 26/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 26/11/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 26/11/2025 | 1230/1230 | Chancellor Reeves to deliver UK Budget | ||

| 26/11/2025 | 1330/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders |