MNI EUROPEAN OPEN: Tokyo CPI Sub Forecast, Wages Revised Down

EXECUTIVE SUMMARY

- TRUMP SLAPS FRESH US TARIFFS ON HEAVY TRUCKS, DRUGS AND KITCHEN CABINETS - RTRS

- TREASURY’S LAVORGNA SEES 3% GROWTH INTO 2026 - MNI INTERVIEW

- TRUMP TAKES AIM AT CHIP MAKERS WITH NEW PLAN TO THROLLTE IMPORTS - WSJ

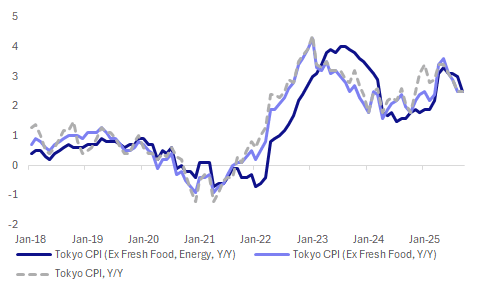

- JAPAN SEPT TOKYO CORE CPI RISES 2.5% VS. AUG 2.5% - MNI BRIEF

- CHINA ADVISORS SHARE THEIR PROPERTY MARKET OUTLOOK - MNI

Fig 1: Tokyo CPI Y/Y Off Recent Highs

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

POLITICS (RTRS): "British Prime Minister Keir Starmer said on Thursday he was focused on "economic stability" after one of his party's mayors said he had been privately encouraged to launch a leadership challenge following criticism of the government's record."

EU

NATO (BBG): “Western militaries can’t keep shooting down incoming drones with expensive missiles, NATO Secretary General Mark Rutte said on Thursday, adding that NATO is rapidly learning from Ukraine on how to counter Russian drones and will deploy new technologies in coming weeks.”

RUSSIA (BBG): “European diplomats warned the Kremlin this week that NATO is ready to respond to further violations of its airspace with full force, including by shooting down Russian planes, according to officials familiar with the exchange.

TURKEY (BBG): “ President Donald Trump pressed Turkish President Recep Tayyip Erdogan to stop buying oil from Russia and left the door open to Ankara obtaining F-35 fighter jets, as the leaders looked to resolve a number of longstanding issues that have strained ties between the NATO allies.”

US

TARIFFS (RTRS): “President Donald Trump on Thursday unleashed a fresh round of punishing tariffs on a broad range of imported goods, saying the U.S. will impose 100% duties on branded drugs and 25% tariffs on heavy-duty trucks, among other import tariffs, starting next week.”

GROWTH (MNI INTERVIEW): The U.S. economy is on the verge of an investment boom that will lead to sustained GDP growth of around 3% into next year, although Federal Reserve interest rates must come down further so as not to stifle the outlook, Joseph Lavorgna, counselor to the U.S. Treasury secretary, told MNI.

REPO (MNI): The Federal Reserve should target the tri-party repo rate used in transactions between cash investors and large dealers as its benchmark overnight rate as market for the federal funds rate has become more fragile, Federal Reserve Bank of Dallas President Lorie Logan said Thursday.

FED (MNI): The Federal Reserve must be cautious about cutting interest rates too quickly in response to signs of weakness in the labor market because inflation remains well above the central bank’s target, Chicago Fed President Austan Goolsbee said Thursday.

US/CHINA (BBG): “President Donald Trump advanced plans for American investors to buy TikTok’s US operations from its Chinese owner ByteDance Ltd., with officials setting a potential value of $14 billion and outlining measures to ensure security of the new venture.”

CHIPS (WSJ): " The Trump administration is weighing a new plan to reduce dramatically the U.S.'s reliance on semiconductors made overseas, hoping to spur domestic manufacturing and reshape global supply chains."

OTHER

JAPAN (MNI BRIEF): Tokyo’s core CPI rose 2.5% y/y in September, unchanged from August and above the Bank of Japan's 2% target for the 11th straight month, the Ministry of Internal Affairs and Communications said Friday. Processed food prices rose 5.7% y/y, down from 6.0%, while services prices accelerated to 2.0% from 1.5%. The data showed a slowing pace of gains inline with the BOJ's expectations, backing its view of gradual rate hikes.

JAPAN (RTRS): "Japan revised real wages in July to a 0.2% fall from a previously reported growth of 0.5%, a labour ministry release showed on Friday. With the revision, Japan's inflation-adjusted real pay has been logging contraction for seven consecutive months, casting doubt on the Bank of Japan's ability to adjust its ultra-loose monetary policy."

CANADA (MNI BRIEF): Canada's postal service is broke and the government says continued subsidies aren't the answer, the minister responsible Joel Lightbound told reporters Thursday as he faces a further showdown with unionized workers who have been taking job action for much of this year.

CANADA (MNI BRIEF): Canada's Parliamentary Budget Office said Thursday increased spending and a slowdown from the U.S. trade war will lead Prime Minister Mark Carney to break a campaign promise of lowering national debt as a percentage of GDP.

MIDDLE EAST (RTRS): "U.S. President Donald Trump said on Thursday that he would not allow Israel to annex the West Bank, rejecting calls from some far-right politicians in Israel who want to extend sovereignty over the area and snuff out hopes for a Palestinian state."

CHINA

HOUSE PRICES (MNI): Chinese advisors share their property market outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

COAL (BBG): “China Coking Industry Association suggests the entire coke industry to cut production by over 30% during a recent market analysis meeting of its committee, the Futures Daily reports, citing unidentified people"

CAPITAL FLOWS (SECURITIES TIMES): “China is set to further expand access to its capital markets, with regulators planning more institutional reforms and cross-border cooperation to attract foreign capital, Securities Times reports.”

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY165.8 billion via 7-day reverse repos, with the rate unchanged at 1.40%, along with CNY600 billion via 14-day reverse repos. The operation led to a net injection of CNY411.5 billion after offsetting maturities of CNY354.3 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.5088% at 09:32 am local time from the close of 1.6017% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Thursday, compared with the close of 48 on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.1152 Fri; -0.81% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.1152 on Friday, compared with 7.1118 set on Thursday. The fixing was estimated at 7.1459 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND SEP ANZ CONSUMER CONFIDENCE 94.6; PRIOR 92.0

JAPAN SEP TOKYO CPI Y/Y 2.5%; MEDIAN 2.8%; PRIOR 2.5%

JAPAN SEP TOKYO CPI EX FRESH FOOD Y/Y 2.5%; MEDIAN 2.8%; PRIOR 2.5%

JAPAN SEP TOKYO CPI EX FRESH FOOD, ENERGY Y/Y 2.5%; MEDIAN 2.9%; PRIOR 3.0%

SOUTH KOREA SEP COMPOSITE BUSINESS SURVEY MANUFACTURING 93.4; PRIOR 93.3

SOUTH KOREA SEP COMPOSITE BUSINESS SURVEY NON-MANUFACTURING 90.5; PRIOR 89.4

MARKETS

US TSYS: Asia Wrap - Yields Mixed In A Quiet Friday Session

The TYZ5 range has been 112-09 to 112-13+ during the Asia-Pacific session. It last changed hands at 112-11, up 0-00+ from the previous close.

- The US 2-year yield has edged lower trading 3.647%, down 0.01 from its close.

- The US 10-year yield is trading around 4.174%.

- 10-Year yields extended their retracement higher moving towards the 4.20% area, I suspect buyers should be around 4.20% initially and look to fade the move higher. Only a move back above 4.35%/4.40% would negate the downtrend.

- Nick Timiraos on X: “Every living former Fed chair (Greenspan, Bernanke, Yellen) … have joined several former Treasury secretaries (Rubin, Summers, Paulson, Geithner, Lew)... and CEA chairs (Hubbard, Mankiw, Romer, Furman, Rouse, Bernstein) who served presidents of both parties … in an amicus brief to the Supreme Court warning a ruling against Lisa Cook's ability to stay in her job would significantly erode Fed independence.”

- Andy Constan on X: “Less than 4 cuts priced into the next 10 Fed meetings of which the Trump nominated chair will be chair for 5 of them. How exactly is the market pricing in a policy mistake?”

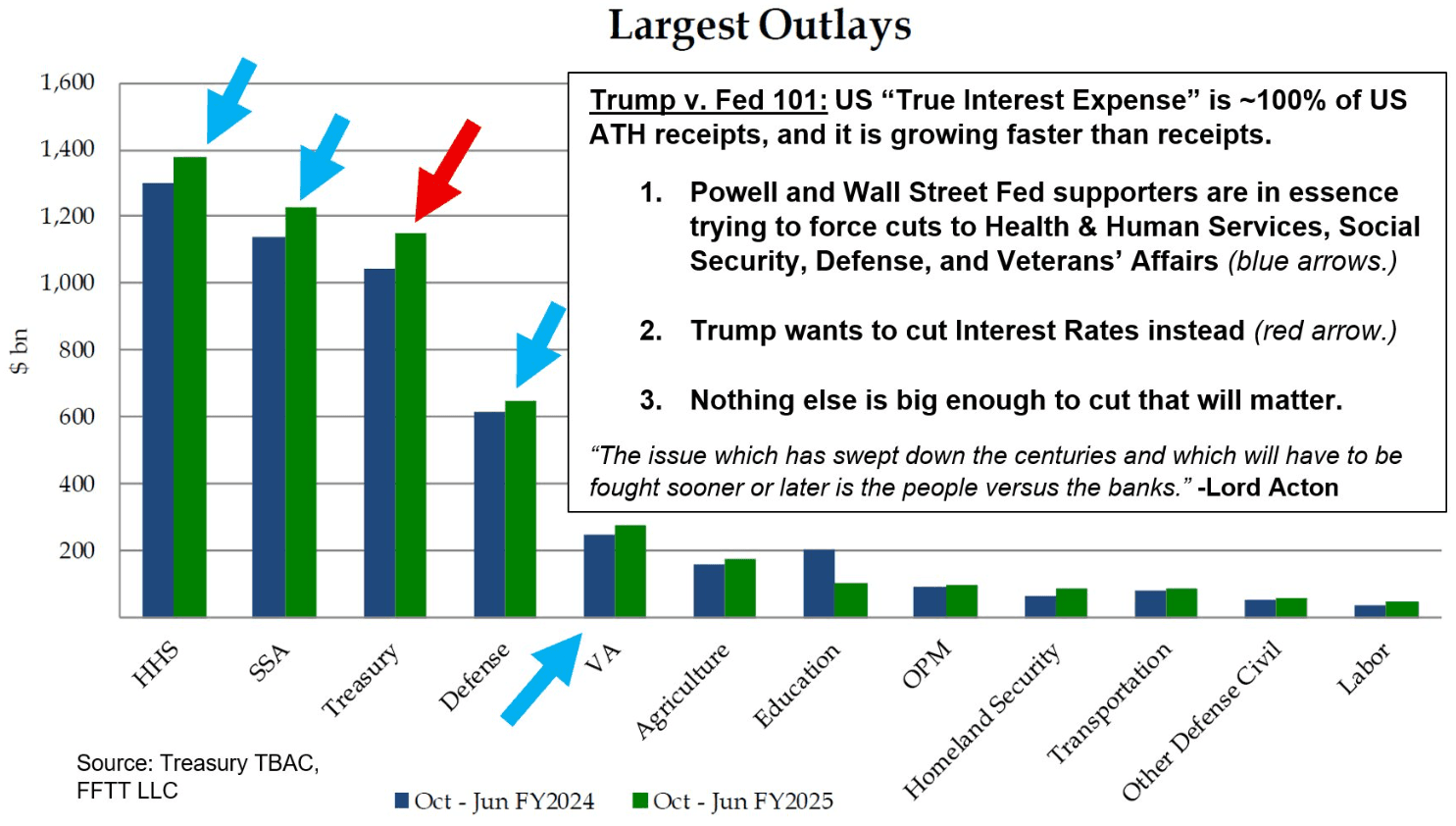

- Luke Gromen on X: “TRUMP v. FED, IN ONE EASY CHART. To paraphrase Richard Gere in "An Officer and a Gentleman": "I got nothing else to cut...I GOT NOTHING ELSE TO CUT!" See Graph Below.

Data/Events: Bloomberg Sept. United States Economic Survey, Personal Income, PCE Price Index, Core PCE Price Index, U. of Mich. Sentiment, Kansas City Fed Services Activity

Fig 1: Largest Outlays

Source: MNI - Market News/@LukeGromen/Treasury TBAC

JGBS: JGB Futures Edge Higher Post Data, US-JP 10yr Diff Up From Recent Lows

JGB futures sit modestly higher, last 135.86, +.04 versus settlement levels. Data outcomes today have lent support to futures. US 10yr futures are little changed, but JGBs have lagged the recent softness in the US 10yr. The US-JP government bond yield spread was last +252bps, up from recent lows of +245bps.

- Despite today's JGB futures gain, a bear threat remains from a technical standpoint. The latest sell-off has also resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection. Key short-term resistance has been defined at 137.30, the Sep 8 high.

- On the data front, earlier we had the Tokyo CPI print, which came in well below forecast. The headline and core measures printing at 2.5%y/y. Services prices were down in the month, but still up 2.0% y/y. Elsewhere headlines crossed that Japan's July wages data have been revised lower. Via Rtrs: "Japan revised real wages in July to a 0.2% fall from a previously reported growth of 0.5%", while nominal growth was revised down to 3.4%y/y, after originally being reported as a 4.1% gain. The trend in real wage y/y momentum is positive, but is coming from a noticeably lower base that originally thought.

- These outcomes today are likely to reinforce, at the margin, the BoJ's wait and see approach.

- In the cash JGB space, yields are little changed across the curve. We saw some early softness for the back end, but this had no follow through. The 10yr was last around 1.65%. The 2/30s curve was last +221bps, slightly steeper for the session.

- Next week the main focus will be on the Tankan survey out on Wednesday. The market expects a resilient to slightly better backdrop large manufacturing firms, while capex is seen at +11.0% (prior was 11.5%).

AUSSIE BONDS: Futures Maintain Negative Bias, RBA Next Week - Seen On Hold

Aussie bonds futures are holding a negative bias as Friday trade unfolds. 3yr (YM) futures are down 4bps, last at 96.385, with 10yr futures (XM) off by 3.5bps to 95.575. We are slightly up from session lows for both benchmarks.

- This keeps the recent downside bias in futures intact. For the 10yr, key short-term support to watch has been defined at 95.510, the Sep 3 low.

- In the cash ACGB space, we are holding around 2-3bps firmer across the curve (except the 30y, up 1bps). The 3yr yield last around 3.58%. We did get close to 3.60% in the first part of trade, fresh highs since mid May. The 10yr was last near 4.37%.

- The ACGB 3/10s curve is under 80bps, but little changed so far today. SocGen sees risks of a flatter curve in light of recent firmer data outcomes/potentially more hawkish RBA (via BBG).

- The AU-US 10yr spread is back above +20bps, up around 3bps so far today.

- All focus next week will be on the RBA outcome, due on Tuesday. Any chance of a move was removed this week with a firmer monthly Aug CPI backdrop. the sell-side consensus is for no change as well. Focus is likely to be on the outlook for the final two meetings of this year. Per WIRP we have Dec OIS pricing at around 3.44%, implying a 16bps reduction in rates from the current effective RBA rate of 3.60%. Prior to this week's CPI print we had around 22bps priced in.

BONDS: NZGBS: Yields Off Earlier Highs, NZ-US 10yr Spread Down To +5bps

The early positive impetus for NZGB yields has cooled as Friday's session has progressed, particularly towards the back end of the curve. The 2 and 5yr benchmarks are still up over 1bps, but the rest of the curve is closer to unchanged. The 2yr outright yield, last 3.385%, while the 10yr was around 4.21%. The 10yr did get close to 4.24% in the first part of trade.

- The NZ 2/10s curve is a touch flatter around +148bps. The NZ-US 10yr spread is down close to 2bps, last near +5bps. This is close to multi month lows. The 2yr swap rate is back under 2.53%.

- In general, NZ yields have lagged both US and Australian developments, with poorer data outcomes/dovish RBNZ expectations in play in recent weeks. The AU-NZ 2yr swap spread has surged toward +90bps.

- On the data front, we had the ANZ Sep consumer confidence index print earlier. The index rose 2.8% in Sep, putting the index back up to 94.6 (from 92.0 in Aug). The improvement will be welcome, but we still sit off recent highs from late 2024. More broadly it doesn't suggest much change to the consumer spending backdrop in the near term.

- Looking ahead to next week, Monday delivers filled jobs for Aug, while Tuesday sees the ANZ activity and business confidence outlook for Sep.

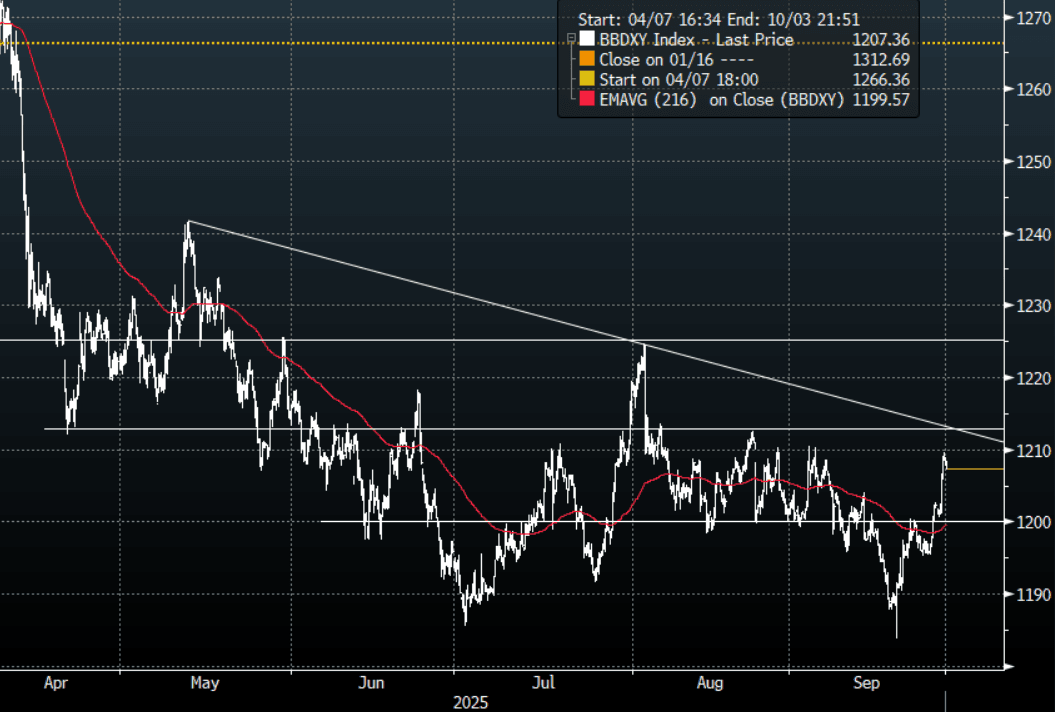

FOREX: Asia FX Wrap - The USD Challenging Leveraged Shorts Into Corp Month-End

The BBDXY has had a range of 1207.36 - 1208.86 in the Asia-Pac session; it is currently trading around 1207, -0.10%. The USD has built on its gains above 1200, with the stronger US data seeing it surge up towards the 1210 area. The price action suggests the market has been caught over its skis in terms of positioning and is having to scale back shorts. Next resistance is back towards the 1215-1225 area where I would expect sellers to remerge initially. The big question is at what level do the global asset managers return to selling for hedging purposes, at the moment the shorter-term leveraged crowd is being squeezed. Corporate month-end continues today and should add to the USD tailwinds underpinning the move higher in the short-term.

- EUR/USD - Asian range 1.1658 - 1.1682, Asia is currently trading 1.1680. The pair has broken through its initial support around 1.1700, this could signal a deeper correction back to the 1.1550 area first and then potentially 1.1350/1.1400.

- GBP/USD - Asian range 1.3330 - 1.3355, Asia is currently dealing around 1.3355. The pair has regained momentum lower and is pressing its first support around the 1.3300 area, a break below here opens up a move back to the 1.3100 area. The market should be looking for bounces to fade.

- USD/CNH - Asian range 7.1404 - 7.1457, the USD/CNY fix printed 7.1152, Asia is currently dealing around 7.1410. The pair has found demand towards the 7.1000 area and is looking to potentially revert back to the mean. Expect sellers first up but a move back above 7.15/16 is needed to potentially signal a deeper correction. Though sellers should be around again on any bounce back toward the 7.2000/2200 area. A move above 7.2500 is needed to see a test of the USD Shorts conviction.

- Cross asset : SPX -0.05%, Gold $3745, US 10-Year 4.172%, BBDXY 1207, Crude Oil $65.21

- Data/Events : Spain GDP, EZ ECB 1&3 Year CPI Expectations, Italy Consumer Confidence Index/Economic Sentiment

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

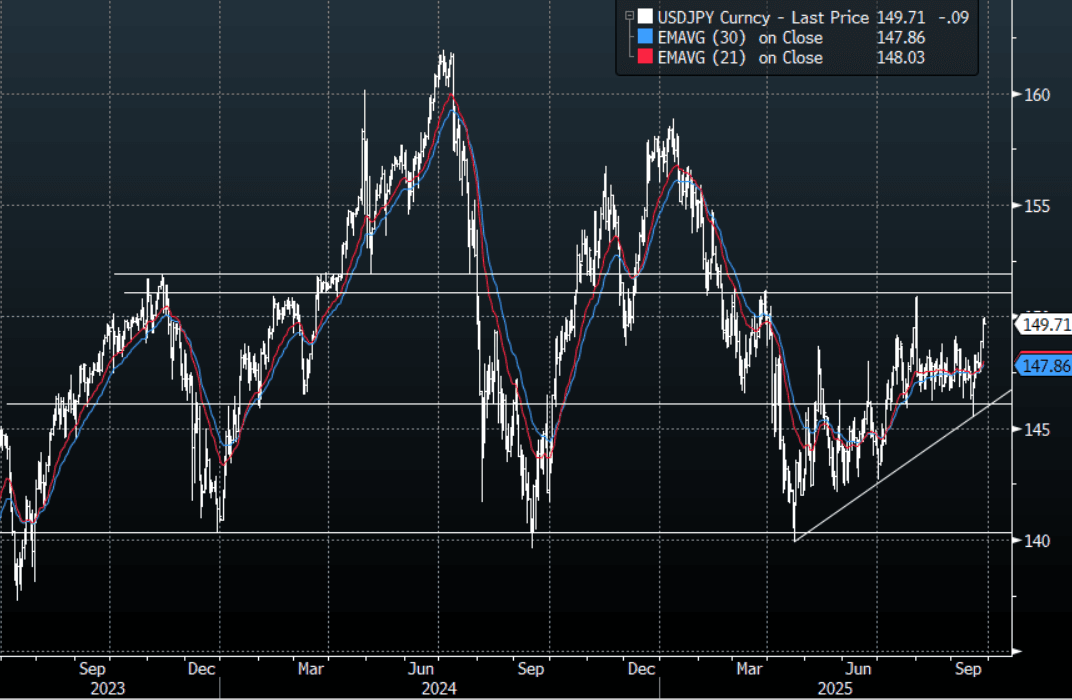

JPY: Asia Wrap- USD/JPY Drifts Off 150.00, Dips To Be Supported After Breaks 149

The USD/JPY range has been 149.63 - 149.96 in the Asia-Pac session, it is currently trading around 149.70, -0.07%. The USD surged higher across the board on stronger data overnight. This gave USD/JPY the momentum it needed to break through the 149.00 area and extend higher. The pair should now see buyers on dips and the focus will turn toward the pivotal 151-152 area. The corporate month-end continues today and this should keep demand for the USD underpinned in the short-term but the USD’s reaction to the data does potentially point to a positional problem. The other thing that stands out is with risk pulling back the market is no longer trading the JPY as a safe haven for the moment. Some Jaw-Boning from officials today but I suspect they will not enter the market until we are back above 155.00 again.

- MNI AU - Tokyo CPI Below Forecast, Likely Adding To BoJ Wait & See Approach: Tokyo Sep CPI was noticeably weaker than forecast. All three inflation measures - headline, core ex fresh food, and core ex fresh food and energy, printed at 2.5%y/y. Expectations were in the 2.8-2.9% region. The core ex fresh food, energy measure was 3.0%y/y in August, so this is a noticeable slowdown.

- "Japan revised real wages in July to a 0.2% fall from a previously reported growth of 0.5%, a labour ministry release showed on Friday. With the revision, Japan's inflation-adjusted real pay has been logging contraction for seven consecutive months, casting doubt on the Bank of Japan's ability to adjust its ultra-loose monetary policy. After the revision, July's nominal wages or total cash earnings rose 3.4% from the same month a year before, down from the preliminary reading of 4.1% gain." RTRS

- "KATO: WE'RE CURRENTLY NOT INTERVENING IN FX MARKET, WILL REFRAIN FROM COMMENTING ON CURRENT FX MOVES" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 149.00($771m), 152.00($1.67b). Upcoming Close Strikes : 146.50($1.09b Oct 1) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

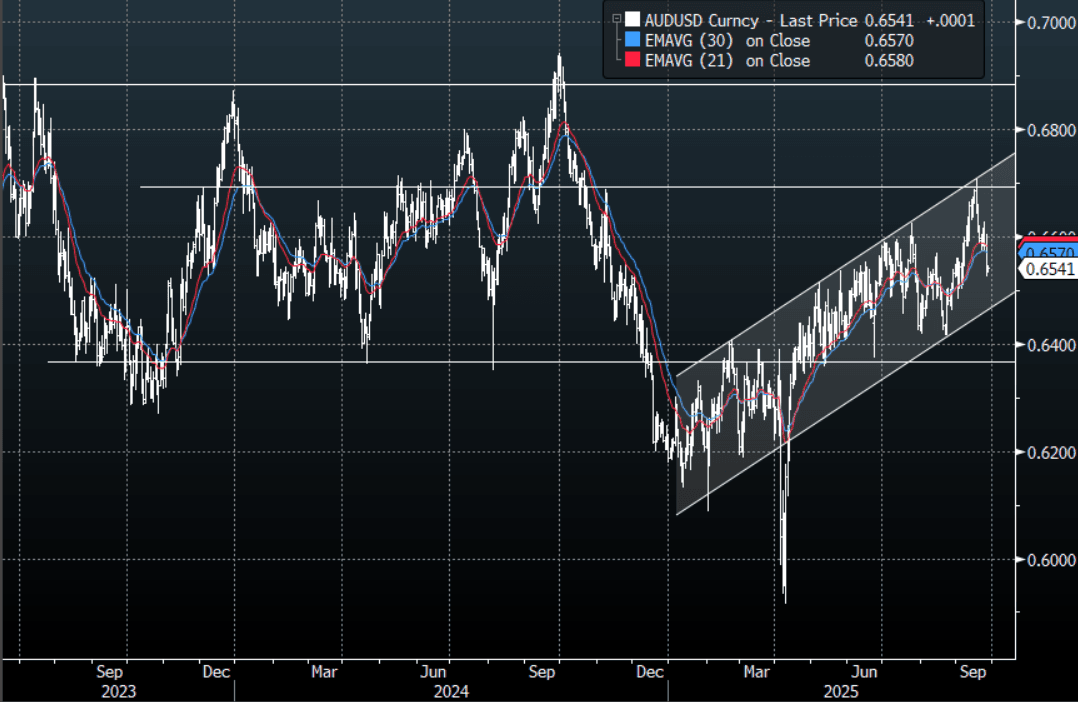

AUD: Asia Wrap - AUD/USD Consolidates Below 0.6550, Eyes 0.6500 Support

The AUD/USD has had a range of 0.6531 - 0.6541 in the Asia- Pac session, it is currently trading around 0.6540, +0.05%. US stocks took another leg lower and the USD accelerated higher on much stronger US data. The AUD support around 0.6580 gave way and the pair then moved lower very quickly overnight, closing around -0.65%. The first buy-zone is just below the 0.6500 area and we should see some buyers return towards here initially, but the price action in the USD would be a concern as it again points to a positional problem. Corporate month-end flows should continue today adding to the USD’s tailwinds so the probability is skewed to a test of the 0.6500 area at some point. The crosses remain the best place to express AUD outperformance for now.

- Bloomberg - “Sizzling Aussie Auction May Show Bond Slump Reaching Limits. The sale of A$900m of November 2029 notes recorded a coverage ratio of 5.97, it went off very nicely with the strongest demand for any offering since October 2024. That signals that the post-CPI sell-off for the country’s government bonds may have gone far enough as yields hit levels to entice buy-and-hold investors.”

- “Dollar Holds Steady Before Key Inflation Reading. “The risk is PCE inflation surprises to the upside, causing the market to pare back pricing of FOMC rate cuts and pushing up the USD, especially against the backdrop of resilient economic growth,” Carol Kong, a strategist at Commonwealth Bank of Australia, wrote in a note.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD478m), 0.6625(AUD364m). Upcoming Close Strikes : 0.6625(AUD1.29b Sept 29), 0.6700(AUD1.64b Oct 1), 0.6725(AUD1.19bm Sept 29) - BBG

- CFTC Data last week shows Asset managers started to significantly reduce their shorts, -41095(Last -68333). The Leveraged community has pulled back their shorts to be almost flat, -1519(Last -5081).

- AUD/JPY - Asia-Pac range 97.83 - 98.03, Asia is trading around 97.95. The pair found solid demand back towards 97.00 and bounced this week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

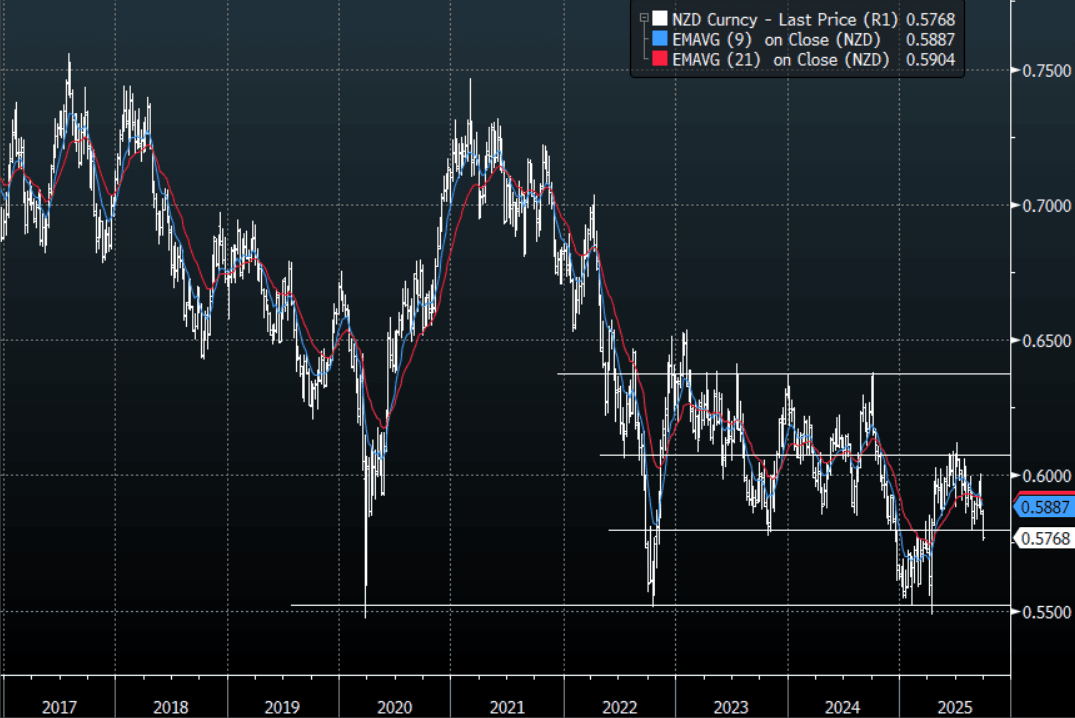

NZD: Asia Wrap - NZD/USD Focus Turns Lower After Breaking Below 0.5800

The NZD/USD had a range of 0.5756 - 0.5776 in the Asia-Pac session, going into the London open trading around 0.5865, +0.02%. US stocks took another leg lower and the USD accelerated higher on much stronger US data. The NZD broke through its pivotal 0.5800 support on the back this and extended lower. The price action in the USD stands out and there could be a positional problem, this together with the clear break of the support should see the NZD continue to be sold on rallies. First sell zone would be just above 0.5800, though corporate month-end continues today and this should keep demand for the USD underpinned.

- MNI: Markets Overestimating Lower OCR - Ex-RBNZ Officials. New Zealand’s Q2 GDP miss is unlikely to push the Reserve Bank to lower the 3% Official Cash Rate below 2.5% without weaker inflation data, former RBNZ officials told MNI, noting recent market pricing had likely overreacted to the economic growth miss

- (Bloomberg) -- RBNZ reduced its foreign currency intervention capacity to NZ$26.1b at the end of August, according to data released by the central bank on its website. Total foreign currency assets dropped to NZ$39b from NZ$39.2b in July. The RBNZ’s net open foreign currency position increased to NZ$8.6b.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5855(NZD305m). Upcoming Close Strikes : 0.5785(NZD754m Sept 30), 0.5875(NZD372m Sept 30) - BBG

- CFTC Data of last week shows Asset Managers beginning to rebuild their short positions in the NZD, -11933(Last -3121). The Leveraged community is doing the same as it looks to rebuild its own shorts, -5327(Last -1874). Positioning shows the market is again turning bearish on the NZD.

- AUD/NZD range for the session has been 1.1330 - 1.1351, currently trading around 1.1340. The Cross has broken above the multiple highs around the 1.1200 area and is beginning to accelerate higher, helped by the AU CPI print. Dips should now continue to be supported as the market turns its focus towards the 1.1400/1.1500 area.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Trump Targets Semi Conductors and Pharma

The Trump administration is seeking to become more self sufficient in the production of semiconductors rather than being reliance on semiconductors made overseas, hoping to spur domestic manufacturing and reshape global supply chains (as reported in WSJ) This comes as the US announced Friday that 100% tariffs will be levied on pharmaceutical products, seemingly targeting China and India. The semi-conductor news saw the likes of TSMC down -1.50% and Samsung -4.30% whilst Pharma companies in India. Market leaders like Dr. Reddy's, Aurobindo Pharma, Zydus Lifesciences, Sun Pharma and Gland Pharma derive between 30-50% of their overall revenues from the American market with some down 3-4% this week.

- China's key bourses have had a weak end Friday, falling across the board. The HSI is down -0.65% and is down -0.87% for the week. The CSI 300 is down -0.42% but up +1.60% for the week, Shanghai down -0.18% but up +0.69% for the week and Shenzhen down -0.56% but up +0.91% for th week.

- Having hit new highs earlier in the week, the NIKKEI gave back today with falls of -0.46%. It remains however up 0.55% for the week, having hit a new high of 45,754.

- The TAIEX in Taiwan got dragged lower by TSMC and the semi conductor sector in general and is down -1.95% today, wiping out earlier weekly gains to be down -0.21%.

- The KOSPI has been hit hard by the semi conductor sector falls and is down -2.9% today, wiping out all of the gains for the week.

- The FTSE Malay KLCI has done very little all week yet has eked out gains of +0.45% today.

- The Jakarta Composite is up +0.38% today and +0.25% despite the challenges for the currency.

- The NIFTY 50 has opened Friday down -0.40% and is down -2.2% for the week.

Oil Set for Weekly Gains on EU / Russian Tensions

- WTI is up by +0.20% in Asia today, consolidating gains and on track for weekly gains of over 3%.

- Brent is up also today, by +0.13% and over 4% for the week, triggering key technical levels and reaching highest levels since early August.

- Despite the realities of the increase in supply from OPEC+ members, the focus for oil for the week has been the mounting tensions between EU members and Russia.

- EU leaders have been clear in their message to Russia that a NATO alliance would be ready to respond to repeated violations of European airspace by Russia, predominantly with drones.

- This comes after President Trump said this week that NATO should shoot down any Russian aircraft that cross into European space. US Defense Secretary Pete Hegseth ordered an urgent meeting of top military commanders for an unusual meeting early next week, fueling concerns over wider unrest that could imperil global crude flows.

- This political tension has given a bid to oil with a strong start to the trading week, though signs overnight that that strength is waning.

- Iraq's long standing disagreement with the Kurdistan region is close to ending after the federal government approved a deal that will see crude from Kurdistan be delivered to Iraq's state oil marketing company SOMO, which will handle shipments through a pipeline to Turkey's Ceyhan port. The resumption of shipments will add 230,000 barrels a day to international markets, rising to as much as half-a-million barrels a day in the future.

GOLD: Sixth Successive Week of Gains for Gold

- Gold's strength continued this week, despite small loses Friday.

- Up over +1.6% for the week, gold has delivered gains in excess of 8% for the week.

- For the year gold is up +43% marking one of the best years in several decades.

- Gold jewelry sales in India are set to drop during the upcoming festival season, as record bullion prices push buyers toward less costly alternatives in one of the world’s largest markets. Demand for ornaments is likely to drop by as much as 27% from a year ago in volume terms during the three-week buying period, according to Surendra Mehta, national secretary at the India Bullion and Jewelers Association. (per BBG)

- Gold's rally in September has taking it to overbought territory for the first time since the trade war uncertainty of April drove the precious metal higher.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 26/09/2025 | 0700/0900 | *** | GDP (f) | |

| 26/09/2025 | 0715/0915 | ECB Cipollone At ECB-CEPR Conference | ||

| 26/09/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 26/09/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 26/09/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 26/09/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 26/09/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 26/09/2025 | 1300/0900 | Richmond Fed's Tom Barkin | ||

| 26/09/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 26/09/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 26/09/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 26/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/09/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 26/09/2025 | 1700/1300 | Fed Vice Chair Michelle Bowman |