JGBS: JGB Futures Edge Higher Post Data, US-JP 10yr Diff Up From Recent Lows

JGB futures sit modestly higher, last 135.86, +.04 versus settlement levels. Data outcomes today have lent support to futures. US 10yr futures are little changed, but JGBs have lagged the recent softness in the US 10yr. The US-JP government bond yield spread was last +252bps, up from recent lows of +245bps.

- Despite today's JGB futures gain, a bear threat remains from a technical standpoint. The latest sell-off has also resulted in a break of support at 136.19, the Sep 4 low and a bear trigger. Clearance of this level confirms a resumption of the downtrend and opens 135.39 next, a Fibonacci projection. Key short-term resistance has been defined at 137.30, the Sep 8 high.

- On the data front, earlier we had the Tokyo CPI print, which came in well below forecast. The headline and core measures printing at 2.5%y/y. Services prices were down in the month, but still up 2.0% y/y. Elsewhere headlines crossed that Japan's July wages data have been revised lower. Via Rtrs: "Japan revised real wages in July to a 0.2% fall from a previously reported growth of 0.5%", while nominal growth was revised down to 3.4%y/y, after originally being reported as a 4.1% gain. The trend in real wage y/y momentum is positive, but is coming from a noticeably lower base that originally thought.

- These outcomes today are likely to reinforce, at the margin, the BoJ's wait and see approach.

- In the cash JGB space, yields are little changed across the curve. We saw some early softness for the back end, but this had no follow through. The 10yr was last around 1.65%. The 2/30s curve was last +221bps, slightly steeper for the session.

- Next week the main focus will be on the Tankan survey out on Wednesday. The market expects a resilient to slightly better backdrop large manufacturing firms, while capex is seen at +11.0% (prior was 11.5%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: Asia FX Wrap - The USD Finds Some Demand Into Month-End

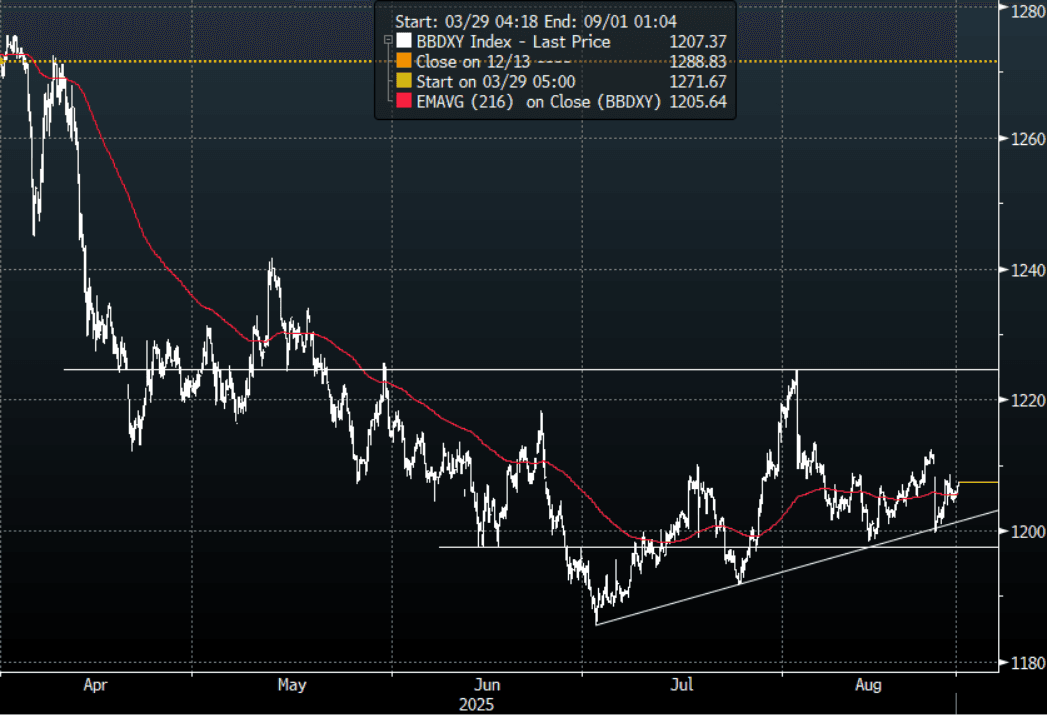

The BBDXY has had a range of 1204.99 - 1207.46 in the Asia-Pac session, it is currently trading around 1207, +0.16%. The USD has been consolidating around 1205, managing to hold above its support in the face of the ongoing Fed debacle. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows. We are heading into corporate month-end and this could explain the market's reticence to press the USD lower as we could see some USD demand potentially over today and tomorrow.

- EUR/USD - Asian range 1.1621 - 1.1649, Asia is currently trading 1.1620. The pair is consolidating just above its support. First support is back towards 1.1550, a move back below here could signal a deeper pullback as the market tries to find a base from which to build for another extension higher.

- GBP/USD - Asian range 1.3454 - 1.3483, Asia is currently dealing around 1.3450. The pair is consolidating just below 1.3500. Back in the middle of its recent 1.3350-1.3650 range, the USD’s fate will have a direct impact on which side is tested.

- USD/CNH - Asian range 7.1457-7.1578, the USD/CNY fix printed 7.1108, Asia is currently dealing around 7.1550. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.08%, Gold $3376, US 10-Year 4.27%, BBDXY 1207, Crude Oil $63.26

- Data/Events : Germany GfK Consumer Confidence, Spain Total Mortgage Lending

Fig 1: BBDXY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Trades Heavy

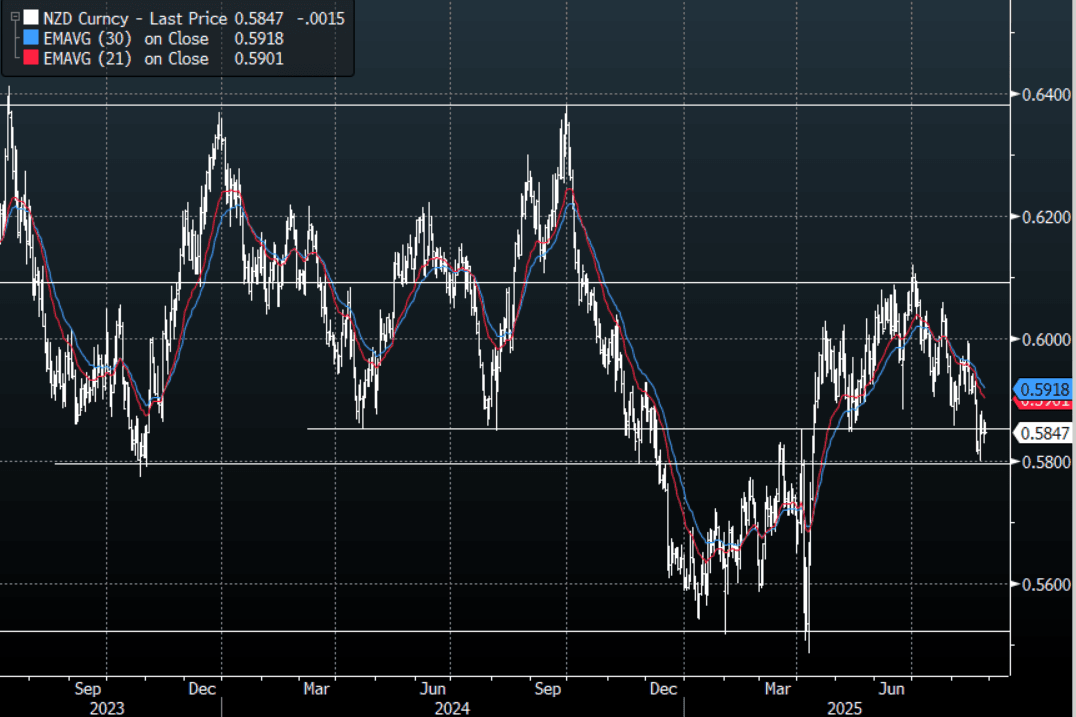

The NZD/USD had a range of 0.5843 - 0.5864 in the Asia-Pac session, going into the London open trading around 0.5845, -0.30%. US equities once again found buyers on the dip and the USD traded a little soft overnight. The NZD traded heavy all through Asia as the USD found a bid tone this morning. We are approaching the corporate month-end so there could be some demand for USD today or tomorrow. US Futures have traded slightly higher this morning, E-minis +0.10%, NQU5 +0.12%.

- Bloomberg - “RBNZ increased its foreign currency intervention capacity to NZ$26.3b at the end of July, according to data released by the central bank on its website. The capacity - foreign currency assets that are readily liquefiable less foreign currency liabilities that fall due in the next 12 months - rose from NZ$25.6b in June”

- “The strengthening yuan is opening the door for more upside for regional peers, particularly those most sensitive to the Chinese currency’s moves such as the Aussie and kiwi dollar, Korean won and Singapore dollar.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6200(NZD355m). Upcoming Close Strikes : none - BBG

- CFTC Data of last week shows Asset Managers slightly reduced their new short position in the NZD -3198(Last -3679), the Leveraged community also reduced their own shorts slightly -4004(Last -4190).

- AUD/NZD range for the session has been 1.1079 - 1.1109, currently trading 1.1095. The dovish RBNZ has seen the Cross surge higher breaking back above 1.100 convincingly. This move should now continue to see dips supported as it looks to build momentum to push higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD Demand Sees USD/JPY Move Back To 148.00

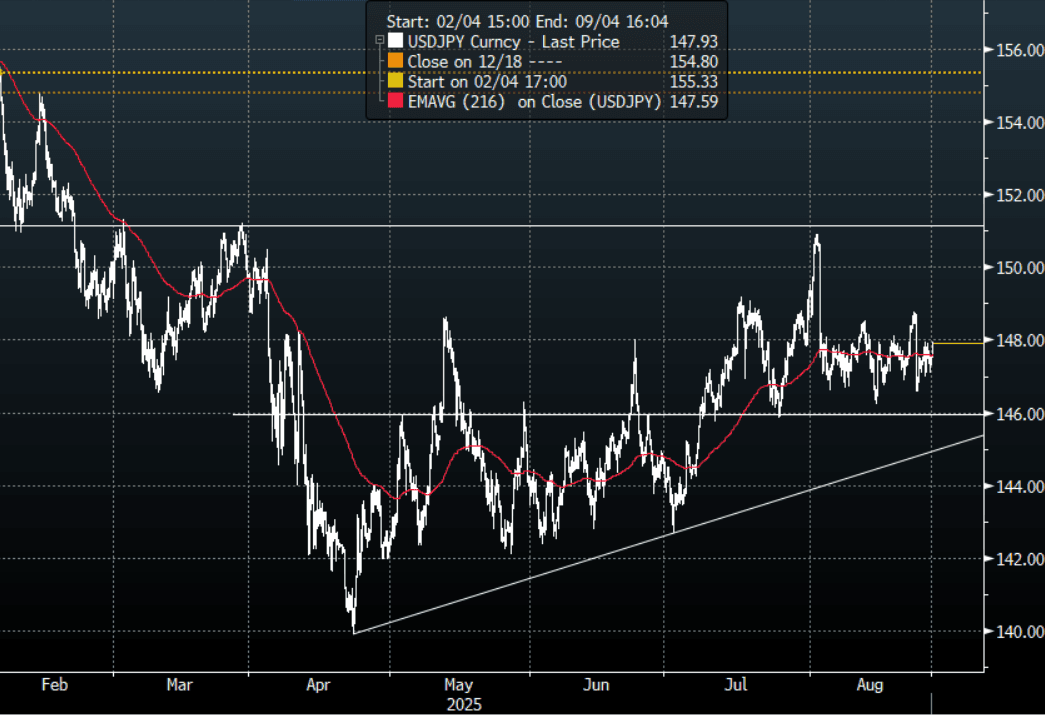

The Asia-Pac USD/JPY range has been 147.30-147.95, Asia is currently trading around 147.90, +0.35%. The demand towards 146.00 has been pretty solid all of July and August, keeping us for the most part in a 146.00-149.00 range. CFTC data for last week shows leveraged accounts again added to JPY shorts so the initial reaction to Powell would have been unwelcome and they would be breathing a little easier as the support continues to hold. We are approaching the corporate month-end so watch for USD demand today and tomorrow. This pair was bid all day today, which does hint at some USD demand flow being executed.

- Kyodo News via BBG - “Long-term interest rates rise to 1.625%, the highest level in 17 years: The yield on the newly issued 10-year government bond (379th issue, nominal interest rate 1.5%), which is an indicator of long-term interest rates, rose to 1.625% at one point, the highest level in about 17 years since October 2008.”

- (Bloomberg) - JGB traders see shorting long-term debt as the gift that keeps giving, with an assist from rising G-10 yields as well as Japan’s Ministry of Finance requesting a bigger budget for its debt financing needs. It’s a vicious cycle for JGBs -- the longer the Bank of Japan stalls in hiking interest rates, the more compensation investors demand for holding super-long bonds as stagflation fears rise.

- “HAYASHI: AKAZAWA VISIT TO THE US NOT DECIDED YET" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.25($765m), 147.95($1.04bm), 148.00($997m).Upcoming Close Strikes : 145.00($1.17b Aug 29), 146.50($1.14b Aug 29), 147.50($806m Aug 29) - BBG.

- CFTC data shows last week asset managers have begun to add to their JPY longs after a consistent period of reduction +71379( Last +60866), leveraged funds though again used the dip to add to their newly built short JPY position -50848(Last -41257).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P