MNI US Macro Weekly: Too Solid For Comfort

Sep-26 20:10By: Tim Cooper

Federal Reserve+ 1

Download Full Report Here

- The US economy now appears to be on more solid footing than it seemed a week ago. Versus 45bp in Fed rate reductions through the remainder of 2025 as of last Friday, futures markets now price 40bp. Half of that retracement came Thursday at 0830ET, when Q2 GDP data, initial jobless claims, durable goods orders, and goods trade data all pointed to stronger ongoing GDP growth than previously anticipated.

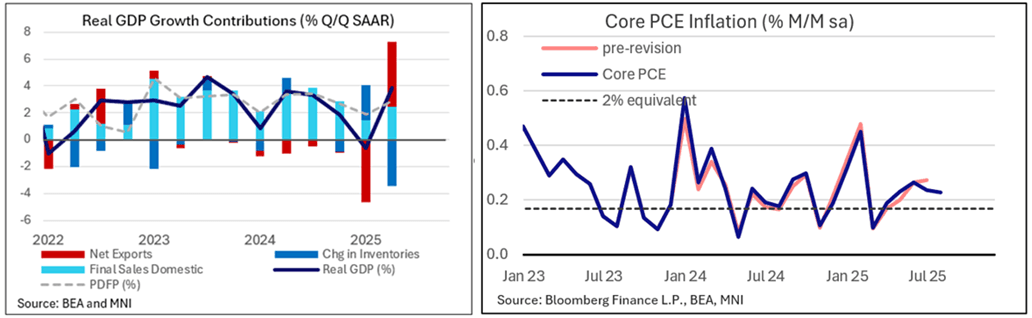

- Q2 GDP growth was revised up significantly in the 3rd and final reading, to 3.84% Q/Q SAAR from 3.29% in the 2nd reading (consensus had expected this to be unchanged in the 3rd). And while that’s in the past, the latest monthly data saw the Atlanta Fed's GDPNow estimate for Q3 jump to 3.9% from 3.3% last week.

- Friday’s PCE data suggested solid consumption dynamics through August (and no nasty surprises in the core inflation data). As such, the week’s data almost unambiguously portrayed a better domestic demand story through – and beyond – a volatile first half of the year related to tariff policy shifts.

- That poses something of a quandary for a Fed that has shifted its sights to labor market risks. GDP is not employment, but a case for rate cuts at a time when inflation is still pushing 3% is tougher to make when the economy is growing at close to a 4% real pace and equities remain at or near all-time highs.

- October's cut is no longer such a sure thing as it seemed after the September meeting, with a 25bp ease now priced at 21bp (~84% implied prob), versus closer to 23bp (90+%) at the end of the prior week.

- While we heard the monetary policy views of 6 of 12 current FOMC voters this week, there were no real surprises. Chair Powell reiterated that policy is not on a preset course; Gov Bowman and Gov Miran reiterated their more-dovish-than-median views; Musalem and Schmid suggested only limited scope for easing; and Goolsbee eyed neutral rates 100-125bp lower but was “uneasy” with too much front-loading.

- Appropriately, the upcoming week’s data schedule centers around the US labor market, including JOLTS job openings data, ADP private sector employment, and Challenger job cuts. And we hear from some of the few FOMC participants who haven’t yet commented since the September meeting, including 2025 voters Waller (Monday), Jefferson (Tuesday and Friday), and Collins (Tuesday).

- Of course, the upcoming week’s schedule culminates with the September Employment report scheduled for Friday. It’s expected to show a continuation of the sluggish growth in U.S. payrolls seen over the prior 4 months, with early consensus estimates eyeing 50k overall gains (22k prior) made up entirely of private employment at 50k (38k prior). Just as closely-eyed, the unemployment rate is seen steady at an unrounded 4.3%, having broken out to a 46-month high 4.32% in August.

- We’re not even guaranteed to get an employment report in the coming week: there is a high probability of a federal government shutdown beginning on October 1 that could prevent the Bureau of Labor Statistics from releasing the data. MNI's Political Risk team wrote Friday that a shutdown "now appears inevitable".