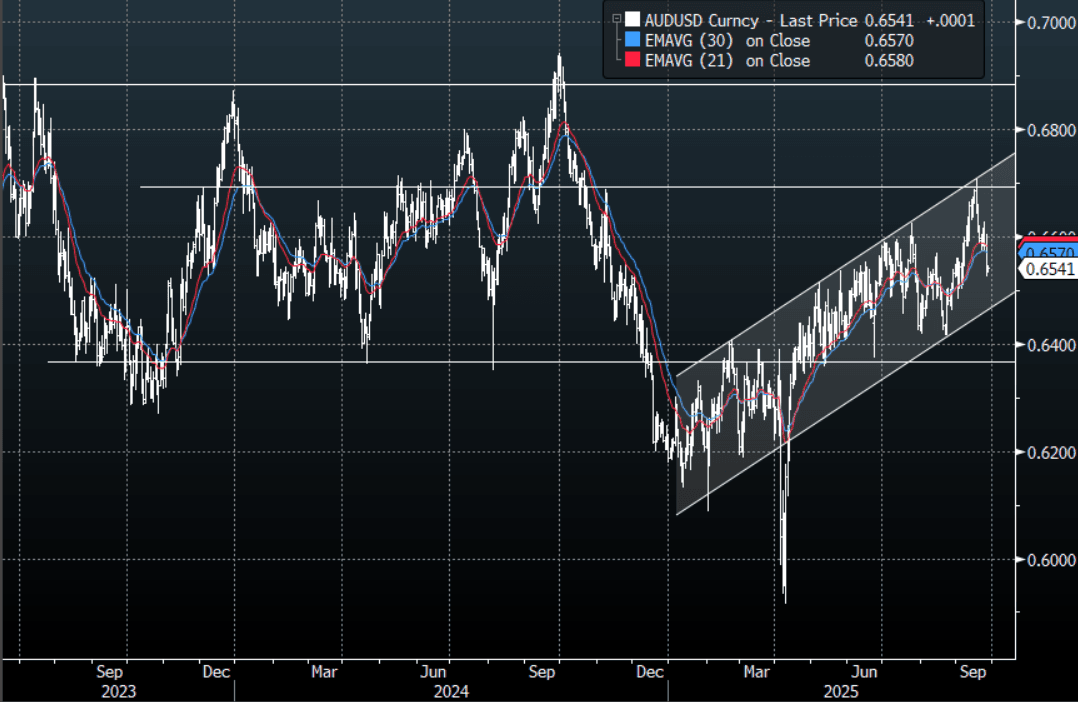

AUD: Asia Wrap - AUD/USD Consolidates Below 0.6550, Eyes 0.6500 Support

The AUD/USD has had a range of 0.6531 - 0.6541 in the Asia- Pac session, it is currently trading around 0.6540, +0.05%. US stocks took another leg lower and the USD accelerated higher on much stronger US data. The AUD support around 0.6580 gave way and the pair then moved lower very quickly overnight, closing around -0.65%. The first buy-zone is just below the 0.6500 area and we should see some buyers return towards here initially, but the price action in the USD would be a concern as it again points to a positional problem. Corporate month-end flows should continue today adding to the USD’s tailwinds so the probability is skewed to a test of the 0.6500 area at some point. The crosses remain the best place to express AUD outperformance for now.

- Bloomberg - “Sizzling Aussie Auction May Show Bond Slump Reaching Limits. The sale of A$900m of November 2029 notes recorded a coverage ratio of 5.97, it went off very nicely with the strongest demand for any offering since October 2024. That signals that the post-CPI sell-off for the country’s government bonds may have gone far enough as yields hit levels to entice buy-and-hold investors.”

- “Dollar Holds Steady Before Key Inflation Reading. “The risk is PCE inflation surprises to the upside, causing the market to pare back pricing of FOMC rate cuts and pushing up the USD, especially against the backdrop of resilient economic growth,” Carol Kong, a strategist at Commonwealth Bank of Australia, wrote in a note.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD478m), 0.6625(AUD364m). Upcoming Close Strikes : 0.6625(AUD1.29b Sept 29), 0.6700(AUD1.64b Oct 1), 0.6725(AUD1.19bm Sept 29) - BBG

- CFTC Data last week shows Asset managers started to significantly reduce their shorts, -41095(Last -68333). The Leveraged community has pulled back their shorts to be almost flat, -1519(Last -5081).

- AUD/JPY - Asia-Pac range 97.83 - 98.03, Asia is trading around 97.95. The pair found solid demand back towards 97.00 and bounced this week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

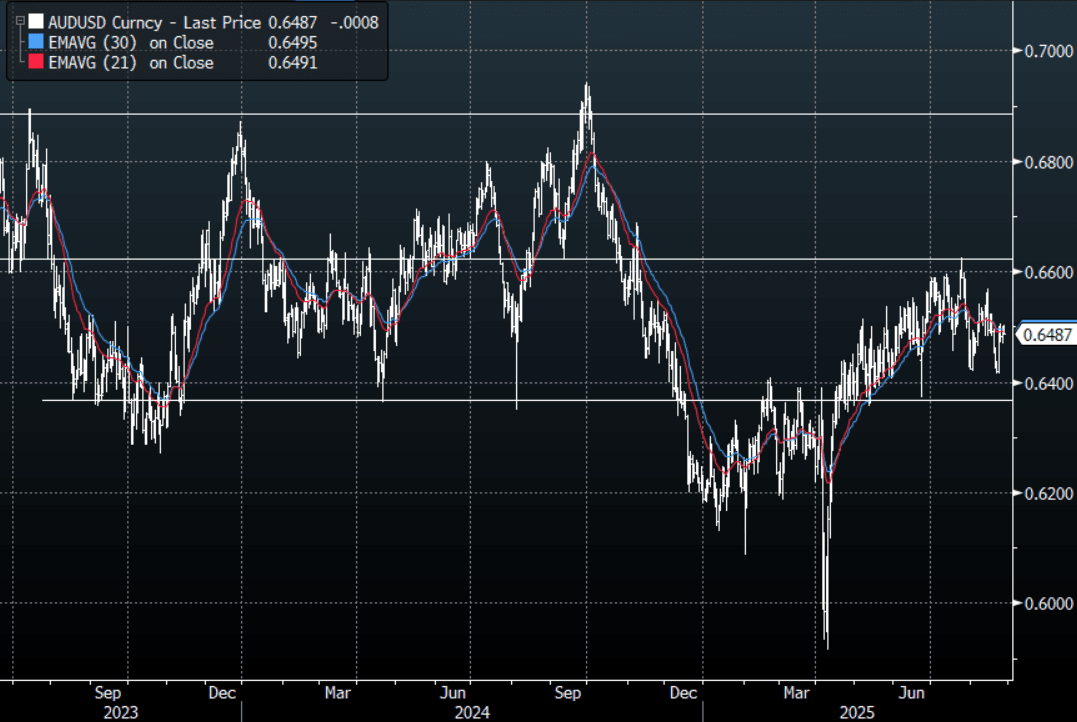

AUD: Asia Wrap - AUD/USD Tries And Fails Above 0.6500 On CPI Print

The AUD/USD has had a range of 0.6487 - 0.6504 in the Asia- Pac session, it is currently trading around 0.6490, -0.10%. The AUD initially tried to push higher after the CPI print but stalled above 0.6500 and drifted back lower for the rest of our session. The AUD finds itself firmly back in the middle of its recent multi-month range of 0.6350-0.6650 and will need a clearer direction from both the USD and risk to embark on a decent move in either direction. We are approaching the corporate month-end so there could be some demand for USD today or tomorrow which is worth looking out for.

- Underlying Inflation Picks Up But Volatile: July trimmed mean CPI inflation jumped to 2.7% y/y from 2.1% and headline to 2.8% from 1.9%. The monthly data are incomplete, for instance services aren’t updated in the first month of the quarter, and headline continues to be impacted in both directions by government electricity rebates. As a result, the RBA continues to focus on the quarterly data with Q3 not released until October 29. Comprehensive monthly CPI data is scheduled for November 26 but it will take time for seasonal trends to emerge.

- Narrow Rise In Construction Work: Q2 the real value of construction work done rose 3% q/q & 4.8% y/y, highest since Q4 2023 and , stronger than expected, after -0.3% q/q & 3.0% y/y. The rise was driven by engineering work with the building components lacklustre. Q2 GDP is released September 3 with private capex data Thursday, inventories September 1 and net exports and public demand contributions September 2

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD695m). Upcoming Close Strikes : 0.6400(AUD571m Aug 28), 0.6500(AUD782m Aug 29), 0.6455(AUD555m Sept 1) - BBG

- AUD/JPY - Asia-Pac range 95.61 - 96.00, Asia is trading around 95.95. The pair continues to grind higher back towards the 96.00 area. This pair’s direction will be determined by the market's ability to follow on with this risk-on move or not. A sustained move back above 96.50 would turn the trend higher again but until then sellers should be around looking for this move to top out.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

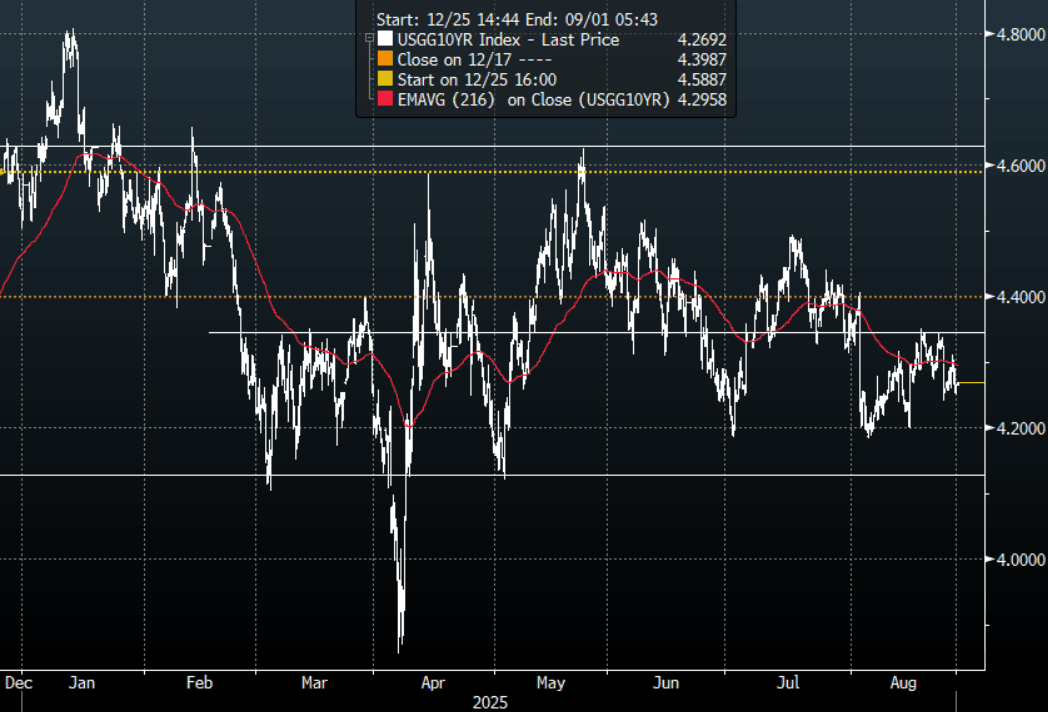

US TSYS: 2s10s Moves Higher

The TYU5 range has been 112-03+ to 112-05+ during the Asia-Pacific session. It last changed hands at 112-04, down 0-02+ from the previous close.

- The US 2-year yield has edged lower trading around 3.6557%, down 0.02 from its close.

- The US 10-year yield has moved higher trading around 4.267%, up 0.01 from its close.

- This has seen the 2s10s steepen in Asia, +2.30 at 60.347.

- 10-Year Yields found buyers above 4.30% again overnight. While the 4.35% area continues to hold, bounces should be met with demand, with the 30-Year taking the brunt of the selling related to challenging the Fed independence. First target is the recent lows around 4.18% then the bottom of the range towards 4.10% comes back into focus.

- Andrew Ackerman on X: “The Fed has deferred any decision on Cook's status because they are expecting a quick decision from a court on Cook's coming request for a judicial order/TRO, according to a Fed official. Would note the Fed has no board meetings scheduled for this week, while Cook is in limbo.”

- ISABELNET on X: “10Y Yield: When the Fed prioritizes the labor market over inflation, it can reduce the immediate risk of recession by sustaining employment. However, this is likely to increase inflation expectations and push yields higher”

- RenMac on X: “Consumers see increasing slack in the jobs market. The Labor Differential continues to soften, falling to a fresh low of 9.7 in August. In particular, we saw a notable jump in those saying “jobs hard to get.” See Fig.1 Below

- Data/Events: MBA Mortgage Applications

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

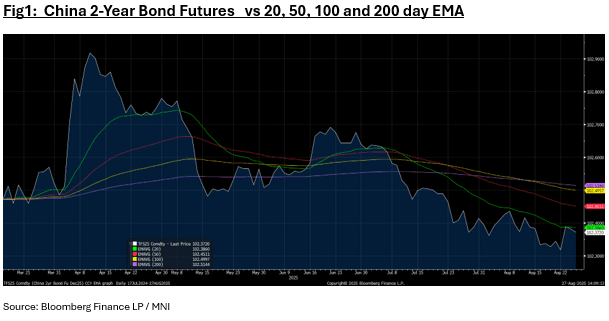

CHINA: Bond Futures Edge Lower in Morning Trade

- China's bond futures are edging lower in the morning trade with the 10-year leading.

- The 10-year is down -0.05 at 107.88, below all major moving averages. The nearest being the 20-day EMA of 108.11.

- The 2-year bond future is lower by -0.01 at 102.37, as it edges further lower having touched the 20-day EMA in recent days.

- Government bond yields are steady with the CGB 10yr at 1.77%