MNI EUROPEAN OPEN: Offshore Inflows Continue For Japan Equity

EXECUTIVE SUMMARY

- FED WELL-PLACED TO ASSESS TWO-WAY RISKS - JULY MINUTES - MNI

- FED’S COOK SAYS SHE WON’T BE BULLIED INTO STEPPING DOWN - BBG

- VANCE SAYS EUROPE WILL HAVE TO TAKE ‘LION’S SHARE’ OF BURDEN FOR UKRAINIAN SECURITY - RTRS

- META FREEZES AI HIRING AFTER BLOCKBUSTER SPENDING SPREE- WSJ

- LOCAL ANALYSTS SHARE INSIGHT INTO CHINA’S H2 STEEL DEMAND - MNI

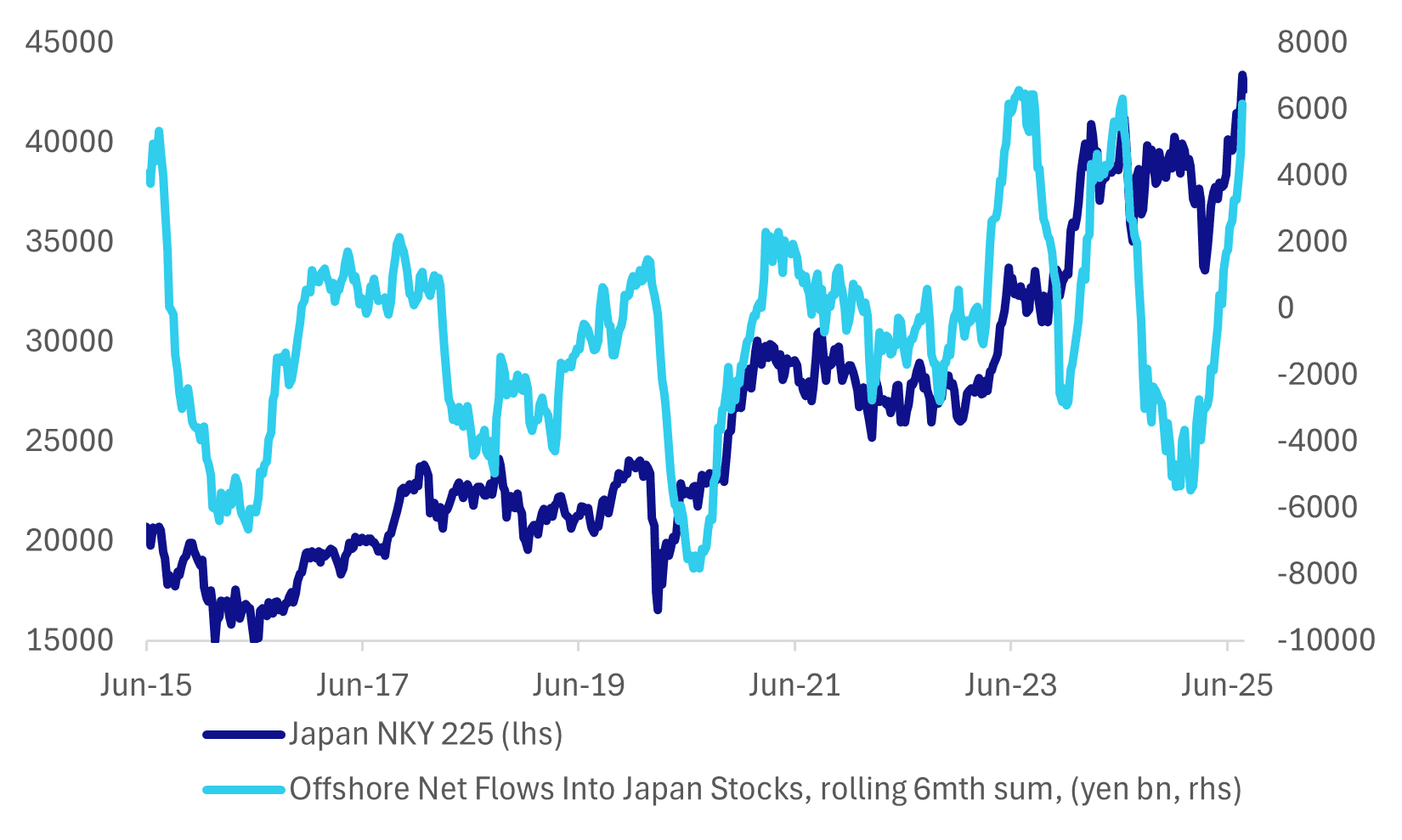

Fig 1: Offshore Investors Have Been Strong Buyers Of Japan Equities In The Past 6mths

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

HOUSEHOLDS (BBG): “UK consumers remained subdued this month as rising prices threaten to eat into household budgets, a survey by the British Retail Consortium showed.

EU

UKRAINE (POLITICO): “Pentagon says US will play a minimal role in Ukraine’s security guarantee. Meetings between NATO and U.S. defense officials left allies concerned that President Donald Trump would leave Europe to ensure a lasting peace in the war-scarred country.”

RUSSIA (BBG): “ Vice President JD Vance said negotiations over ending Russia’s war in Ukraine are focused on security guarantees for Ukraine and territory Russia wants to control — including Ukrainian territory that Russia isn’t occupying — as the US tries to broker a peace deal between the two nations.”

UKRAINE (RTRS): “U.S. Vice President JD Vance said on Wednesday that European countries will have to pay the "lion's share" of costs for Ukraine's security guarantees.”

GERMANY (DW): “Foreign Minister Johann Wadephul told DW that Germany would welcome China taking a more active role in the peace process in Ukraine. "Hardly any other country, any other government, has such a strong influence on Russia as China. Unfortunately, China hasn't used its opportunities so far, but it is never too late," Wadephul said in an interview with DW's Rosalia Romaniec.”

POLAND (POLITICO): “A Russian military drone crashed in eastern Poland early Wednesday, jolting NATO’s eastern flank just as Western leaders struggle to advance fragile peace efforts with Moscow over Ukraine.”

ITALY (ECONOMIST): “Shareholders in Mediobanca, a Milan-based investment bank, will hold a vote on Thursday on a move that could have far-reaching implications for Italy’s financial sector. Mediobanca is the target of a takeover bid by Monte dei Paschi di Siena (MPS), the world’s oldest lender.”

US

FED (MNI): Federal Reserve policymakers discussed upside inflation risks and downside risks to the labor market at last month's policy meeting as "almost all" policymakers decided to keep interest rates on hold for a fifth time this year, according to minutes of the meeting.

FED (BBG): “Federal Reserve Governor Lisa Cook signaled her intention to remain at the central bank, defying calls for her resignation by President Donald Trump over allegations of mortgage fraud.”

TECH (WSJ): “Meta Platforms has frozen hiring in its artificial-intelligence division after spending months scooping up 50-plus AI researchers and engineers, according to people familiar with the matter.”

POLITICS (RTRS): “Texas legislators on Wednesday approved a new state congressional map drawn at the behest of President Donald Trump to flip five Democratic-held U.S. House seats in next year's midterm elections, after dozens of Democratic lawmakers ended a two-week walkout that had temporarily blocked passage.”

OTHER

CENTRAL BANKS (MNI INTERVIEW): Threats to central bank independence are set to feature in talks among policymakers at this year’s Jackson Hole symposium, Sweden’s central bank chief told MNI, and continued heightened uncertainty over geopolitics is dampening the boost to consumption from interest rate cuts in Europe.

MIDDLE EAST (RTRS): “Israel’s military announced the first steps of an operation to take over Gaza City on Wednesday and called up tens of thousands of reservists while the government considered a new ceasefire proposal to pause nearly two years of war.

NEW ZEALAND (BBG): “RBNZ Governor speaks to parliament select committee Thursday in Wellington, following decision to cut interest rates yesterday and signal potentially two further 25 bps reductions.”

CHINA

STEEL (MNI): Local analysts share insight into China's H2 steel demand.

HOUSEHOLDS (YICAI): “China's financial assets such as equities and funds can become the dominant component of household wealth, surpassing traditional asset classes, if the stock market exceeds CNY300 trillion by 2030, up from around CNY100 trillion as of August 2025, according to Teng Tai, president of the Wanbo New Economy Research Institute.”

YUAN (RTRS): "China is considering allowing the usage of yuan-backed stablecoins for the first time to boost wider adoption of its currency globally, sources familiar with the matter said, in a major reversal of its stance towards digital assets."

INVESTMENT (SECURITIES DAILY): China’s investment activity is expected to regain momentum in the later stages, despite the recent slowdown in nominal investment growth, as short-term pressures ease and the impact of pro-investment policies take effect, according to Wang Qing, chief macro analyst at Dongfang Jincheng.

MNI: PBOC Net Injects CNY124.3 Bln via OMO Thursday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY253 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY124.3 billion after offsetting maturities of CNY128.7 billion today, according to Wind Information

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4736% at 09:43 am local time from the close of 1.5680% on Wednesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Wednesday, compared with the close of 64 on Tuesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1287 Thurs; -0.69% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1287 on Thursday, compared with 7.1384 set on Wednesday. The fixing was estimated at 7.1773 by Bloomberg survey today.

MARKET DATA

AUSTRALIA S&P GLOBAL AUG. FLASH MANUFACTURING PMI 52.9; JULY 51.3

AUSTRALIA S&P GLOBAL AUG. FLASH SERVICES PMI 55.1; JULLY 54.1

AUSTRALIA S&P GLOBAL AUG. FLASH COMPOSITE PMI 54.9; JULY 53.8

AUSTRALIA MI AUG. INFLATION EXPECTATIONS 3.9%; JULY 4.7%

NEW ZEALAND JULY TRADE DEFICIT NZ$578M; JUNE +NZ$203M

NEW ZEALAND JULY 12-MONTHS YTD TRADE DEFICIT NZ$3.94B; JUNE -$4.38B

JAPAN S&P GLOBAL AUG. FLASH MANUFACTURING PMI 49.9; JULY 48.9

JAPAN S&P GLOBAL AUG. FLASH SERVICES PMI 52.7; JULY 53.6

JAPAN S&P GLOBAL AUG. FLASH COMPOSITE PMI 51.9; JULY 51.6

SOUTH KOREA JULY PRODUCER PRICE INDEX +0.5% Y/Y; JUNE +0.5%

SOUTH KOREA JULY PRODUCER PRICE INDEX +0.4% M/M; JUNE +0.1%

SOUTH KOREA AUG 1-20 TRADE BALANCE AT PROVISIONAL $+0.83 BLN

SOUTH KOREA AUG 1-20 EXPORTS +7.6% Y/Y; PRIOR -2.2%

SOUTH KOREA AUG 1-20 IMPORTS +0.4% Y/Y; PRIOR -4.3%

MARKETS

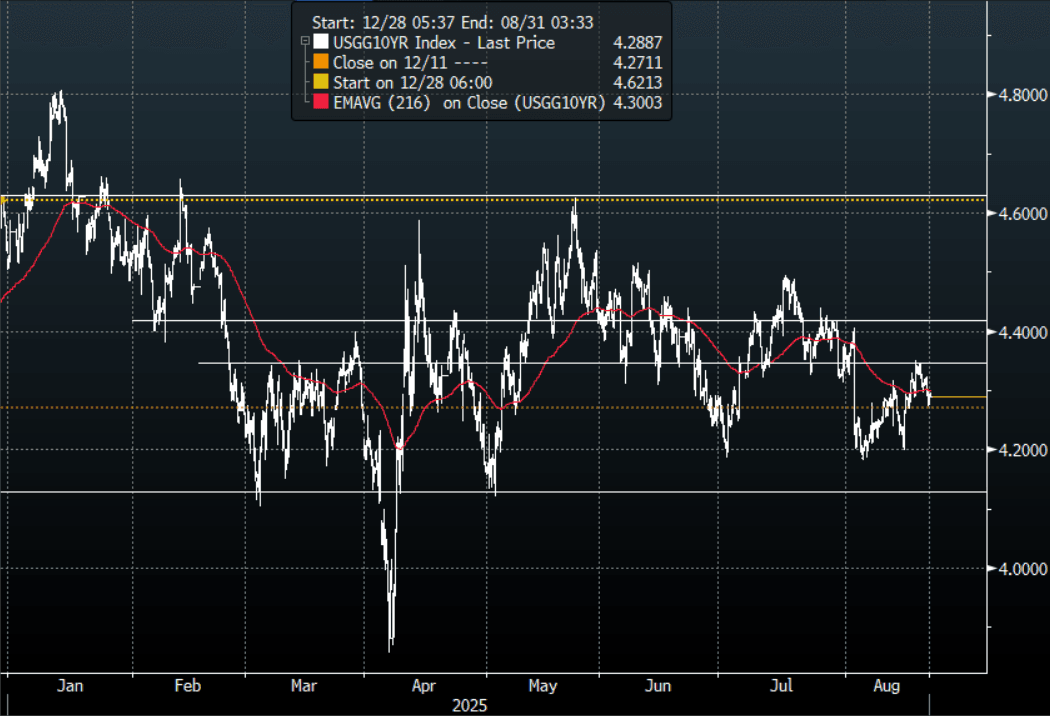

US TSYS: Quiet Session Looking Toward Jackson Hole

The TYU5 range has been 111-26 to 111-29 during the Asia-Pacific session. It last changed hands at 111-27+, unchanged from the previous close.

- The US 2-year yield is trading around 3.745%.

- The US 10-year yield is trading around 4.29%.

- 10-Year Yields are still firmly within its wider 4.10%-4.65% range. The 4.35% pivot area found solid demand capping the move higher for now, the market will now be waiting for any clues from Powell's upcoming Jackson Hole speech.

- RenMac on X: “The July FOMC minutes show that it is really tough to push through a 50bp cut in September. Too many on the FOMC are concerned about upside inflation risks and even after a weak jobs number many see the slowdown as a benign labor supply story.”

- Daily Chartbook on X: "Foreigners are not too concerned about a debt crisis in the US. They continue to be significant buyers of US Treasury notes and bonds as well as US government agency bonds and domestic corporate bonds."@yardeni

- Financial Times on X: “Central banks are under growing pressure to keep interest rates artificially low to offset the cost of record government borrowing.”

- Data/Events: Initial Jobless Claims, Phil Fed Business Outlook, S&P US PMI’s, Leading Index, Existing HOme Sales

Fig 1: 10-Year US Yield 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Futures Weaken In Afternoon Session, Natl CPI Tomorrow

JGB futures are little changed, +2 compared to the settlement levels.

- (Bloomberg) JGB futures are turning softer in the afternoon, as traders balk at the extra ¥650 billion of bonds sold today, which is helping to nudge 10-year yields to highest since 2008. Investors have been nibbling at long-term JGBs this week as yields approached cyclical highs, but it is the bond bears in the futures market who are calling the shots before BOJ Governor Ueda’s appearance at Jackson Hole.

- (Bloomberg) “Japan’s 20-year government bond yields climbed to fresh multi-decade highs, driven by persistent concerns over fiscal expansion and fading demand from key investors. Yields on bonds of various maturities rose, with the 10-year yield climbing to 1.61%, a level unseen since 2008, and 30-year notes rising to 3.18%, approaching the all-time peak of 3.2% seen in July.”

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs are slightly mixed across benchmarks, with yields flat to 2bps higher and the curve steeper. The benchmark 10-year yield is 0.1bp lower at 1.61% versus the cycle high of 1.621% set yesterday.

- Swap rates are 1-2bps higher. Swap spreads are wider.

- Tomorrow, the local calendar will see National CPI.

AUSSIE BONDS: Richer & Near Session Bests, Jun-54 Supply Tomorrow

ACGBs (YM +2.0 & XM +4.0) are stronger and close to the session’s bests.

- The S&P Global PMI is suggesting that growth picked up in Australia in Q3. The preliminary August composite index rose to 54.9 from 53.8 driven by improvements in both the manufacturing and services sectors. This is the fastest growth in activity since April 2022, before the RBA began its tightening cycle.

- In June, Melbourne Institute consumer inflation expectations jumped 1pp to 5%. They moderated to 4.7% in July and in August to 3.9%, the first print below 4% since March's 3.6%. Looking at the trend, the series has been moving sideways for around the last year.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally.

- Cash ACGBs are 2-4bps richer with the AU-US 10-year yield differential at -3bps.

- The bills strip has twist-flattened, with pricing -1 to +2.

- RBA-dated OIS pricing is slightly softer across meetings today. A 25bp rate cut in September is given a 28% probability, with a cumulative 37bps of easing priced by year-end (based on an effective cash rate of 3.59%).

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$300mn of the 4.75% 21 June 2054 bond.

BONDS: NZGBS: Extends Post-RBNZ Rally Into The Close

NZGBs closed richer, extending yesterday’s strong post-RBNZ decision by 2-4bps.

- Today’s weekly supply saw solid demand, with cover ratios ranging from 3.11x (May-35) to 4.00x (May-30).

- The NZ-US 10-year yield differential closed 3bps tighter at 6bps, the tightest since February.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally. Today’s US Data/Events: Initial Jobless Claims, Phil Fed Business Outlook, S&P US PMIs, Leading Index and Existing Home Sales.

- Swap rates closed 1-4bps lower, with the 2s10s curve flatter.

- RBNZ dated OIS pricing closed 17-26bps softer across meetings versus yesterday’s pre-RBNZ Policy Decision levels. The market had priced 22bps of yesterday’s 25bp cut going into the decision. 19bps of easing is priced for October, with a cumulative 37bps by November 2025 versus 12bps before the. decision.

- Tomorrow, the local calendar will see Trade Balance data.

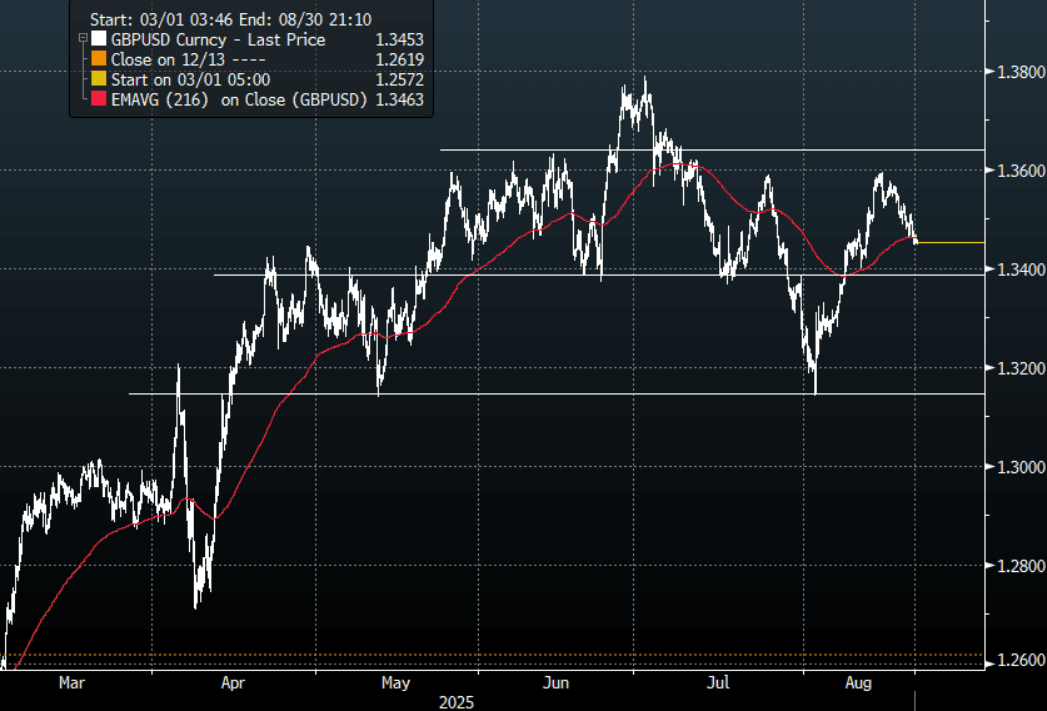

FOREX: Asia FX Wrap - The USD Is Steady Heading Into Jackson Hole

The BBDXY has had a range of 1206.68 - 1207.81 in the Asia-Pac session, it is currently trading around 1207, +0.05%. The USD consolidated its recent gains overnight as we await Powell's speech at Jackson Hole. Depending on the contents of Powell's speech this could change very quickly but the BBDXY looks to be putting in a third higher low which would be a worrying sign to the bears that we could be putting in a short-term base. A sustained break below 1197/1195 is needed to regain the momentum lower and retest the year's lows, but risk is more likely skewed to the USD shorts continuing to be reduced into Powell's speech.

- EUR/USD - Asian range 1.1641 - 1.1656, Asia is currently trading 1.1645. The market is trading sideways in a 1.1600-1.1750 range heading into Jackson Hole. The pair is unlikely to extend too far as the market awaits Powell's speech.

- GBP/USD - Asian range 1.3448 - 1.3467, Asia is currently dealing around 1.3455. Having broken back above its pivot look for dips to again be supported, with risk retracing the pair is probing its first support seen towards 1.3400.

- USD/CNH - Asian range 7.1716-7.1842, the USD/CNY fix printed 7.1287, Asia is currently dealing around 7.1760. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.01%, Gold $3338, US 10-Year 4.29%, BBDXY 1207, Crude Oil $63.07

- Data/Events : EZ HCOB PMI’s/Construction Output/Consumer confidence, Germany HCOB PMI’s, France HCOB PMI’s

Fig 1: GBP/USD Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

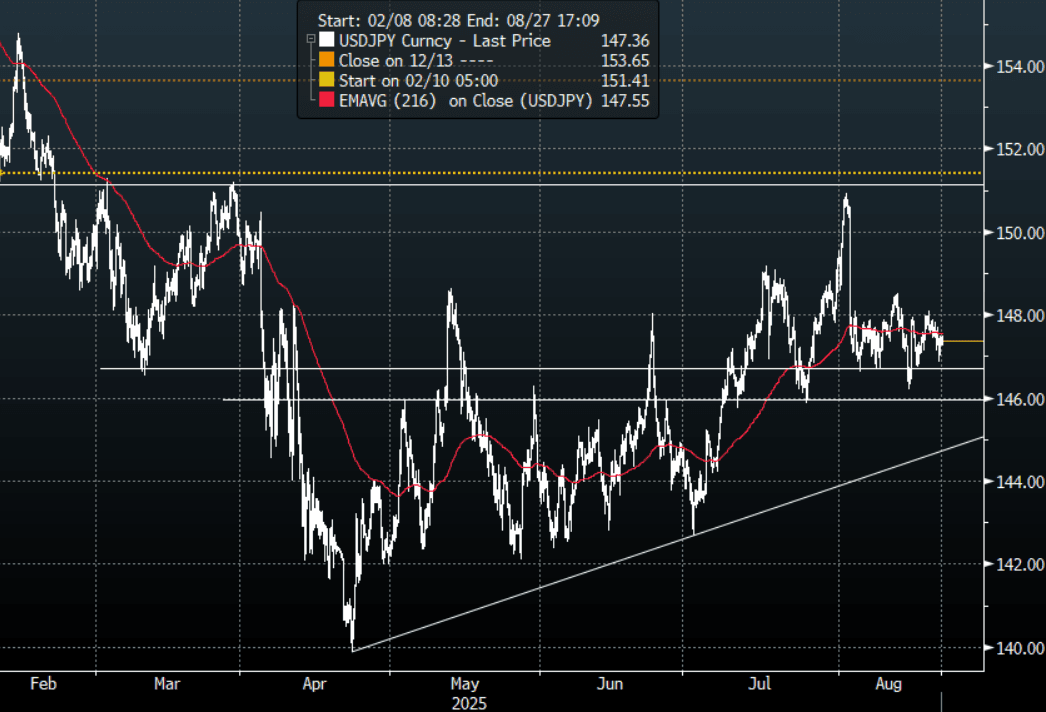

JPY: Asia Wrap - USD/JPY Holds Above 147.00 Ahead Of Jackson Hole

The Asia-Pac USD/JPY range has been 147.26-147.51, Asia is currently trading around 147.40, +0.05%.USD/JPY again found solid demand on a 146 handle overnight as US stocks recovered from a weak opening. Price continues to hold above the support area between 146.00/147.00, a sustained move below this support is needed to turn the momentum potentially lower again. While this plays out it looks to be more range trading within the wider 146.00-151.00 range.

- CFTC Data shows leveraged funds have bought this dip in USD/JPY betting the support remains intact. Powell's speech at Jackson hole will have a say in whether it continues to hold or not.

- Japan Data: August Manufacturing PMI Rises But Still Sub 50.0 : Japan preliminary PMIs for August were mixed. Manufacturing improved to 49.9 from 48.9, but services eased to 52.7 from 53.6. This left the composite index slightly higher at 51.9 (versus 51.6 in July).

- (Bloomberg) - Japan 20-Year Government Bond Yield Rises to Highest Since 1999: Yields on Japan’s super-long government bonds climbed to multi-decade highs, driven by persistent concerns over fiscal expansion and fading demand from key investors.

- "LDP REPORT ON ELECTION TO BE DELAYED TO EARLY SEPT.: TV ASAHI" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.80($1.35b), 150.00($1.06b).Upcoming Close Strikes : 147.90($1.54b Aug 22), 143.00($1b Aug 25), - BBG.

- CFTC data shows last week asset managers maintained their JPY longs +60866( Last +60532), leveraged funds used the dip to add to their newly built short JPY position -41257(Last -29308).

Fig 1 : USD/JPY Spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Drifts Lower

The AUD/USD has had a range of 0.6419 - 0.6437 in the Asia- Pac session, it is currently trading around 0.6425, -0.15%. The AUD has continued to trade heavy in our session. The AUD broke below its support just below 0.6500 earlier in the week and looks likely to continue to trade heavy into Powell’s speech. Pivotal support is back towards 0.6300/50 which has been the bottom in its recent multi-month range of 0.6350-0.6650.

- AU Data: Inflation Expectations Back Below 4%In June, Melbourne Institute consumer inflation expectations jumped 1pp to 5%. They moderated to 4.7% in July and in August to 3.9%, the first print below 4% since March's 3.6%. Looking at the trend, the series has been moving sideways for around the last year. It is still too soon to say that inflation expectations are drifting down again with the next few months key in determining that.

- PMI Suggests H2 Pickup In Growth: The S&P Global PMI is suggesting that growth picked up in Australia in Q3. The preliminary August composite index rose to 54.9 from 53.8 driven by improvements in both the manufacturing and services sectors as well as higher new orders, including external, and increased hiring to fill them. This is the fastest growth in activity since April 2022, before the RBA began its tightening cycle. The PMI suggests that while Q2 growth could again be lacklustre there was probably an improvement in H2

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD514m), 0.6600(AUD1.34b). Upcoming Close Strikes : 0.6525(AUD350m Aug 22), 0.6510(AUD520m Aug 25), 0.6400(AUD346m Aug 25) - BBG

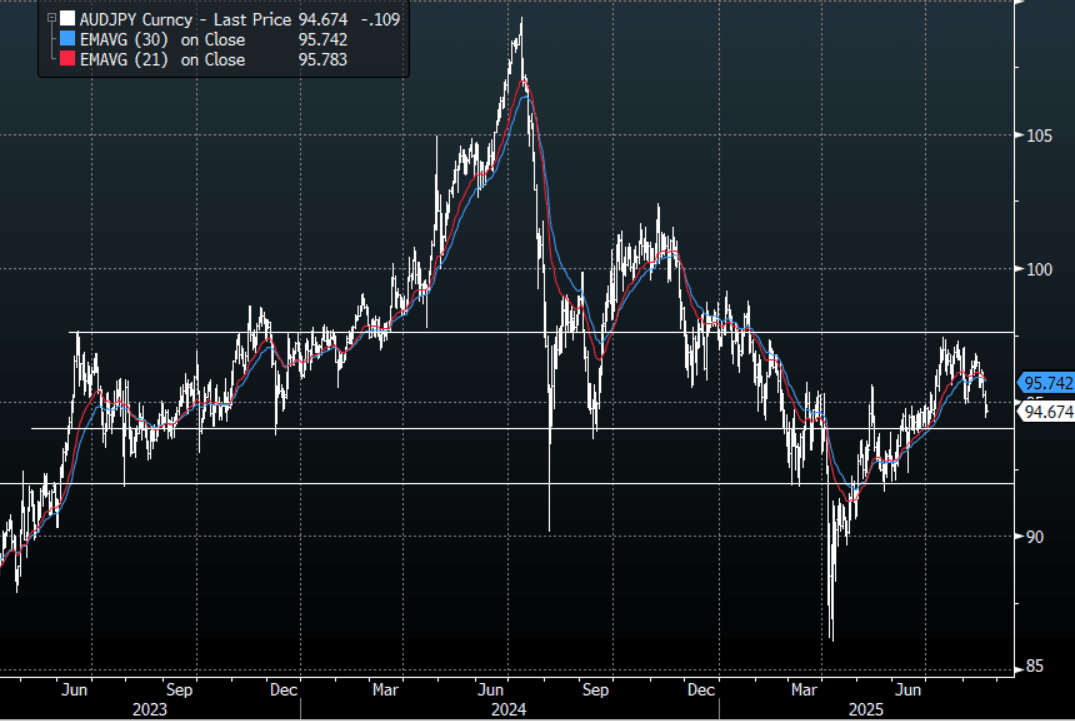

- AUD/JPY - Asia-Pac range 94.59 - 94.91, Asia is trading around 94.65. The pair extended its move lower overnight after breaking below 95.50. Although the price is still in the 94.00-97.50 range the multiple failures towards 97.00 looks like a rounded top and with risk looking vulnerable a test of the lower end of the range looks possible. A sustained break below the 94.00/94.50 area is needed to potentially begin a trend lower again.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

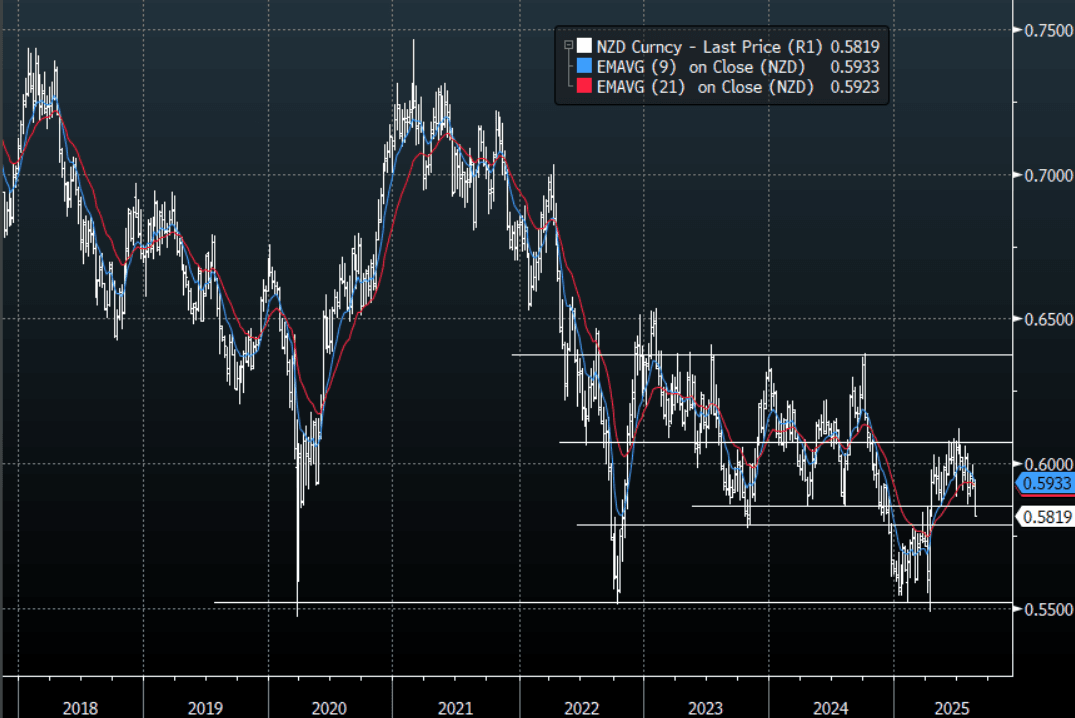

NZD: Asia Wrap - NZD/USD Trading Heavy Testing 0.5800 Support

The NZD/USD had a range of 0.5815 - 0.5833 in the Asia-Pac session, going into the London open trading around 0.5815, -0.12%. A dovish RBNZ that contemplated a cut of 50bps saw NZD/USD break lower yesterday and is now probing some pivotal support in the 0.5800 area. Some of the crosses have broken some key levels AUD/NZD above 1.1000 & NZD/JPY below 86.50, pointing to further NZD weakness ahead. US Futures have had a muted range today, E-minis +0.01%, NQU5 +0.10%.

- (Bloomberg) - RBNZ’s Hawkesby Says Commodity Price Gains Support Economy: Elevated food commodity prices have insulated the New Zealand economy from the negative shock the world is facing, RBNZ Governor Christian Hawkesby said in interview broadcast by CNBC. “It’s one of the things that gives us confidence that with low interest rates and high commodity prices, you’ve got the ingredients there in New Zealand for an economic recovery over the second half of this year and into next”

- "FONTERRA LIFTS FY25 FARMGATE MILK PRICE TO NZ$10.15/KG, SEES FY26 FARMGATE MILK PRICE NZ$9-11/KG" - BBG

- First Trade Deficit Since January: After five consecutive merchandise trade surpluses, NZ recorded a deficit in July of $578mn bringing the 12mth sum to $3.94bn down from $4.38bn. Export growth remains strong, which has been a bright spot in a soft economy.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5980(NZD660m). Upcoming Close Strikes : none - BBG

- CFTC Data shows Asset Managers have cut their longs completely and started to rebuild a short adding slightly in the NZD -3679(Last -1811), the Leveraged community though reduced their own shorts slightly -4190(Last -6778).

- AUD/NZD range for the session has been 1.1029 - 1.1056, currently trading 1.1035. The dovish RBNZ has seen the Cross surge higher breaking back above 1.100 convincingly. This move should now see dips supported as it looks to build momentum to push higher.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Japan Softens Further, Other Markets Higher

Outside of further Japan equity market weakness, most Asia Pac equity indices are firmer in the first part of Thursday trade. US equity futures are a touch higher, as are EU futures. In Wednesday cash trade, US markets lost further ground, but both the SPX and the Nasdaq finished well above intra-session lows from the session.

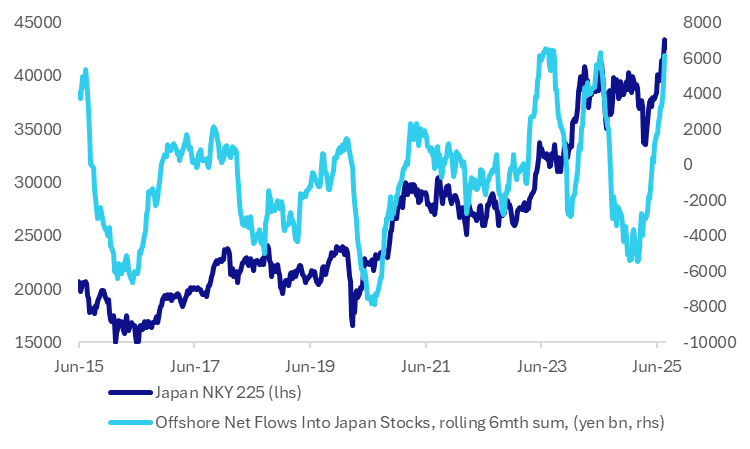

- In Japan, the Topix is off around 0.50%, while the NKY is down slightly more (off 0.60%). Both markets are only marginally off recent record highs. Earlier data showed, up until the end of last week, continued inflows into local stocks from offshore investors. Indeed, since the start of April there has only one week of net selling of local equities out of the past 20 weeks.

- The chart below plots the rolling 6 mth sum of offshore inflows into Japan stocks and the NKY 225 index. We are back close to cycle highs on this flow metric. Loss of momentum in this space could impact Japan equity trends if history is a guide.

- Elsewhere, Taiwan's Taiex has recouped some of yesterday's losses, the index up a little over 1% (after dipping nearly 3% yesterday, amidst nearly $2.4bn in offshore selling). South Korea's Kospi is also tracking up, last up around 0.90%.

- Hong Kong's HSI is down a little, but the CSI 300 in China continues to rally, up a further 0.70% putting the index around the 4300 level. The index continues to close in on intra-session highs from Oct last year.

- Australia's ASX 200 is up firmly, +0.85% to fresh record highs, amidst a broad based rally. NZ markets also continued to rise, up a further 1.1%, after yesterday's strong gains post the dovish RBNZ cut.

- In South East Asia, outside of modest losses for Thailand and Indonesia, markets are modestly higher. The Philippines is out today.

Fig 1: Offshore Inflows Have Surged Into Japan Stocks

Source: Bloomberg Finance L.P./MNI

OIL: Crude Higher Again Today On Large US Crude Drawdown

Oil prices have continued trending higher today consolidating Wednesday’s rally which was driven by a larger-than-expected US crude drawdown reported by the EIA. WTI is up 0.6% to $63.07/bbl following a peak of $63.19, while Brent is 0.4% higher at $67.12 after rising to $67.29. Crude has trended lower through most of August. The USD index is slightly higher.

- With the IEA forecasting a record oil surplus in 2026, attention is firmly on supply and demand information. For now the US market is looking robust with high refining utilisation and falling inventories.

- The EIA reported a significant crude inventory drawdown of 6.01mn barrels last week. Gasoline stocks fell 2.72mn, fifth consecutive decline, while distillate rose 2.34mn. The refining utilisation rate rose 0.2pp to 96.6%, 4.3pp higher than the same time last year, suggesting demand is robust.

- Later the Fed’s Bostic appears. US preliminary August S&P Global PMIs, August Philly Fed, July lead index, July existing home sales and jobless claims print. There are also European preliminary PMIs and UK July public sector net borrowing.

Gold Lower, Waiting For Fed Powell’s Speech Friday

After rising a percent on Wednesday in reaction to concerns over Fed independence, gold prices are 0.2% lower at $3340.8/oz, close to the intraday low, during today’s APAC trading. The slightly stronger US dollar (USD BBDXY +0.1) will be adding pressure, while yields are little changed. Bullion rallied on Wednesday after US President Trump called for Fed Governor Cook to resign. She was a Biden appointee.

- Currently there is around an 80% chance of a Fed cut at its next meeting on 17 September. Markets are waiting for Fed Chair Powell’s Jackson Hole speech on Friday to read his thinking regarding the timing of a resumption of easing. The July minutes showed that inflation worries persist.

- Fitch Solutions is forecasting gold to move between $3200-3600/oz over the rest of the year, according to Bloomberg.

- Silver is little changed at $37.928 after falling to $37.826 and then reaching $37.974.

- Equities are mixed with the Nikkei down 0.6%, CSI 300 up 0.7% and the S&P e-mini flat. Oil prices have continued higher with WTI +0.5% to $63.03/bbl. Copper is 0.2% lower.

- Later the Fed’s Bostic appears. US preliminary August S&P Global PMIs, August Philly Fed, July lead index, July existing home sales and jobless claims print. There are also European preliminary PMIs and UK July public sector net borrowing.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 21/08/2025 | 0600/0700 | *** | Public Sector Finances | |

| 21/08/2025 | 0600/0800 | Q2 GDP | ||

| 21/08/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 21/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 21/08/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 21/08/2025 | 0900/1100 | ** | Construction Production | |

| 21/08/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 21/08/2025 | 1130/0730 | Atlanta Fed's Raphael Bostic | ||

| 21/08/2025 | 1230/0830 | *** | Jobless Claims | |

| 21/08/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 21/08/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 21/08/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 21/08/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 21/08/2025 | 1400/1000 | *** | NAR existing home sales | |

| 21/08/2025 | 1400/1000 | * | Services Revenues | |

| 21/08/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 21/08/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 21/08/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 21/08/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 21/08/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 30 Year Bond | |

| 22/08/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 22/08/2025 | 2330/0830 | *** | CPI | |

| 22/08/2025 | 0600/0800 | ** | Unemployment | |

| 22/08/2025 | 0600/0800 | *** | GDP (f) | |

| 22/08/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 22/08/2025 | 0900/1100 | Q2 Negotiated Wage Growth | ||

| 22/08/2025 | 1230/0830 | ** | Retail Trade | |

| 22/08/2025 | 1230/0830 | ** | Retail Trade |