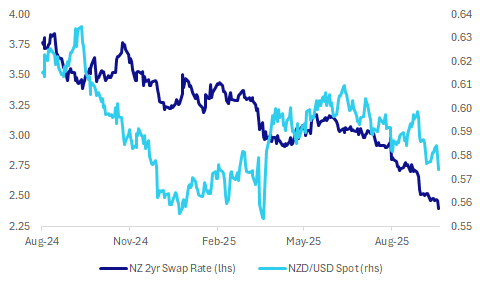

MNI EUROPEAN OPEN: NZD & Local Yields Slump On RBNZ 50bps Cut

EXECUTIVE SUMMARY

- MIRAN SAYS WON’T PLAY A PART IN FED CHAIR SEARCH - MNI BRIEF

- FORMER BOJ CHIEF ECONOMIST ON THE POLICY RATE OUTLOOK - MNI INTERVIEW

- JAPAN AUG REAL WAGES NEGATIVE FOR EIGHTH MONTH - MNI BRIEF

- US LAWMAKERS CALL FOR BROADER BANS ON CHIPMAKING TOOL SALES TO CHINA - RTRS

- RBNZ CUTS OCR 50BP TO 2.50% - MNI BRIEF

Fig 1: NZD/USD and Local Yields Slump Post RBNZ 50bps Cut

Source: Bloomberg Finance L.P./MNI

UK

POLITICS (BBC): “Sir Keir Starmer has said the UK will not relax visa rules for India ahead of a visit to the country to tout the benefits of a recent trade agreement. The prime minister is leading a delegation of more than 100 entrepreneurs, cultural leaders and university vice chancellors, as he attempts to boost UK investment and improve sluggish economic growth.”

TRADE (BBC): “The EU has announced plans to hike tariffs on imported steel in a move the UK's steel industry has said could be "perhaps the biggest crisis" it has ever faced. The EU is the UK's most important export destination for steel, worth nearly £3bn and representing 78% of steel products made in the UK for overseas markets.”

POLITICS (BBC): “The UK's most senior prosecutor has said a case involving two men accused of spying for China collapsed because he could not obtain evidence from the government referring to China as a national security threat.”

EU

EUR (MNI BRIEF): The international role of the euro can no longer remain a secondary issue in the context of trade tensions and global fragmentation, European Central Bank President Christine Lagarde said Tuesday, noting it was crucial to move from being a safe-haven currency to being a truly global one.

TARIFFS (MNI BRIEF): The European Commission has proposed tariff-rate-quotas to protect its steel industry from imports from China and other Asian countries as well as the problem of global overcapacity in the sector.

FRANCE (POLITICO): “With President Emmanuel Macron expected to reveal his next big move on Wednesday or shortly after, he’s still keeping everyone guessing on how he plans to pull France out of a deepening political and economic crisis. The French president is increasingly isolated, with three of his former centrist prime ministers now publicly piling pressure on him.”

ITALY (BBG): “Prime Minister Giorgia Meloni said banks will once again have to contribute to Italy’s budget.”

US

FED (MNI BRIEF): Federal Reserve Governor Stephen Miran emphasized the importance of an independent U.S. central bank Tuesday, and said he will not be playing a part in the search for the next Fed chair.

FED (MNI BRIEF): Federal Reserve Governor Stephen Miran said Tuesday the central bank needs to lower interest rates and that stable long term interest rates flow from success in achieving the central bank's dual mandate goals.

INFLATION (MNI BRIEF): The New York Fed's median measures of consumer inflation expectations at the one-year and five-year-ahead horizons ticked higher in September, according to the bank's monthly survey. Labor market expectations also continued to deteriorate.

OTHER

JAPAN (MNI BRIEF): Japan’s inflation-adjusted real wages, a key gauge of households’ purchasing power, fell 1.4% year-on-year in August, marking the eighth consecutive month of decline, preliminary data from the Ministry of Health, Labour and Welfare showed Wednesday. The drop followed a 0.2% fall in July.

JAPAN (MNI INTERVIEW): A former BOJ chief economist shares his policy rate outlook. On MNI Policy MainWire now, for more details please contact sales@marketnews.com

NEW ZEALAND (MNI BRIEF): The Reserve Bank of New Zealand’s Monetary Policy Committee cut the Official Cash Rate by 50 basis points to 2.5% on Wednesday, citing prolonged spare capacity and associated downside risks to medium-term activity and inflation.

CHINA

US/CHINA (RTRS): "U.S. lawmakers are calling for broader bans on chipmaking equipment to China after a bipartisan investigation found that Chinese chipmakers had purchased $38 billion of sophisticated gear last year."

MARKET DATA

JAPAN AUG. LABOR CASH EARNINGS +1.5% Y/Y; EST. +2.7%; JUL. +3.4%

JAPAN AUG. REAL CASH EARNINGS -1.4% Y/Y; EST. -0.5%; JUL. -0.2%

JAPAN AUG. SAME SAMPLE REGULAR FULL TIME PAY +2.4% Y/Y; EST. +2.5%; JUL. +2.4%

JAPAN AUG. CASH WAGES FROM SAME SAMPLE +1.9% Y/Y; EST. +2.7%; JUL. +3.1%

JAPAN AUG. TRADE SURPLUS Y105.9B YEN; EST. -Y111.5B; JUL. –Y189.4B

JAPAN AUG. CURRENT ACCOUNT SURPLUS Y3.776T; EST. +Y3.507T; JUL. +Y2.684T

JAPAN AUG. ADJUSTED CURRENT ACCOUNT SURPLUS Y2.464T; EST. +Y2.443T; JUL. +Y1.883T

MARKETS

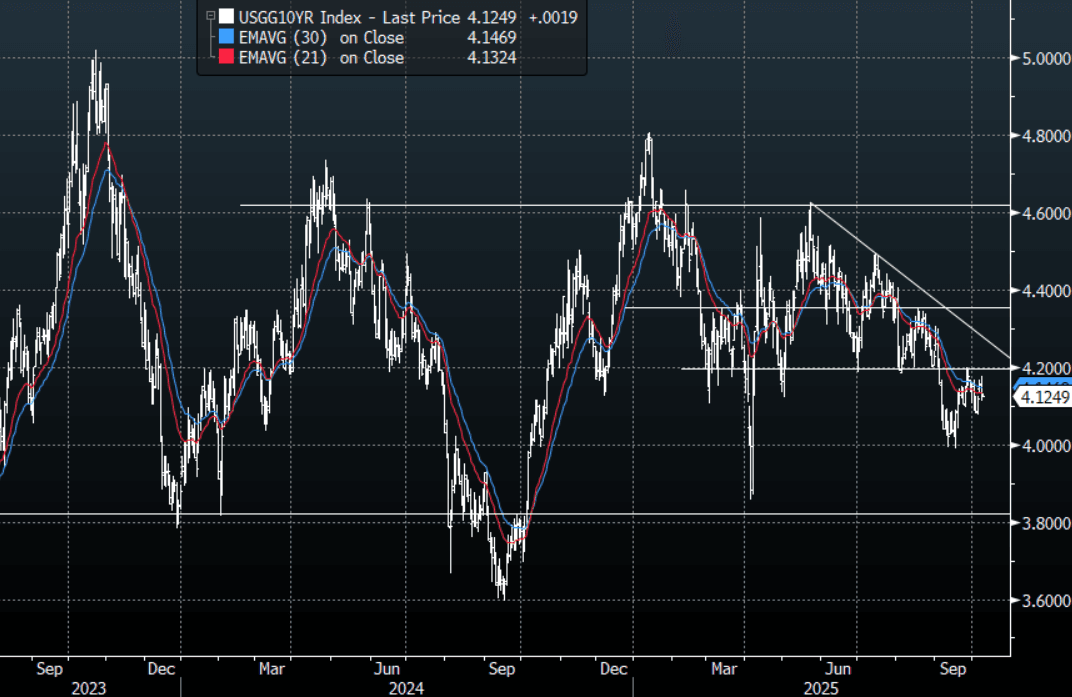

US TSYS: Asia-Pac: Yields Slightly Higher In A Quiet Session

The TYZ5 range has been 112-19+ to 112-22 during the Asia-Pacific session. It last changed hands at 112-21+, unchanged from the previous close.

- 10-Year yields bounced to start the week on the back of global politics but remains subdued below 4.20% as the market works through the US shutdown. I suspect buyers continue to be around 4.20% initially and look to fade bounces higher looking for a move back towards 4%.

- The US 10-year yield is trading around 4.125%.

- The US 2-year yield is trading around 3.568%.

- MNI Brief - Stephen Miran emphasized the importance of an independent U.S. central bank, and said he will not be playing a part in the search for the next Fed chair.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Twist-Flattener As Long-End Unwinds Politically Induced Sell-Off

JGB futures are weaker, -20 compared to settlement levels, but off session lows.

- August's labour earnings data today was comfortably below market expectations. This likely reinforces expectations that the BoJ will likely remain on hold at the Oct policy meeting. Japan's new political regime had already noted that October is too soon for a rate hike. BoJ Governor Ueda also noted recently that the risk was low for the central bank to fall behind the inflation/policy curve (with today's data supporting this theme).

- Nevertheless, cash JGBs out to the 10-year part of the curve have seen moderately higher yields today. In large part because the market already had only a 25% chance of a 25bp hike in October priced.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally.

- Cash JGBs beyond the 10-year are, however, richer as it continues to unwind the yield overshoot associated with the change in political leadership over the weekend. The benchmark 30-year yield is 2.6bps lower at 3.272% versus the cycle high of 3.351% set before yesterday’s auction result.

- The swap curve has twist-flattened, pivoting at the 20-year, with rates 2bps higher to 3bps lower.

- Tomorrow, the local calendar will see Weekly International Investment Flows, Tokyo Avg Office Vacancies and Machine Orders alongside 5-year supply.

AUSSIE BONDS: Data-Light Session, YM Biased Lower, AU-US 10YY Near Top Of Range

ACGBs (YM flat & XM +2.0) are modestly stronger in today's data-light session but off session bests.

- According to MNI’s technicals team, Aussie 3-yr futures (YM) have traded lower, and the contract has cleared the Sep 3 low of 96.435. A break of this level negates the recent short-term bullish theme. This breach signals scope for an extension towards 96.280, the May 15 low on the continuation chart. The short-term resistance to watch is 96.615, the Sep 12 high. Clearance of this level is required to reinstate a bullish theme.

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's modest rally.

- Cash ACGBs are 1-3bps richer with the AU-US 10-year yield differential at +23bps. At 23bps, the differential is approaching the top of the +/- 30bp range it has traded in since late 2022.

- The bills strip is flat to +2 across contracts.

- RRBA-dated OIS pricing is largely unchanged across meetings today. Markets now assign a 40% probability to a 25bp rate cut in November, with a total of 14bps of easing priced by year-end. This marks a notable shift from late September, when markets had fully priced a 25bp cut ahead of the August CPI release.

- Tomorrow, the local calendar will see Consumer Inflation Expectation data.

BONDS: Bull-Steepener After RBNZ Cuts By 50bp

NZGBs closed 4-7bps richer after the RBNZ cut 50bps to 2.50%.

- The MPC discussed cutting the OCR by 25bp or 50bp and all members agreed the latter was appropriate given material spare capacity in the economy. Given that this is likely to persist for some time and that while the economy has begun to recover it remains lacklustre, further cuts bringing policy into stimulatory territory are likely. In line with this it said that “the Committee remains open to further reductions in the OCR”.

- The MPC’s inflation concern appeared to shift this month. In August, it said it could ease policy further “if medium-term inflation pressures continued to ease as expected”, whereas this month it seemed more concerned with undershooting the target mid-point, stating it “remains open to further reductions … for inflation to settle sustainably” near the 2% mid-point over the medium-term.

- Swap rates closed 4-6bps lower on the day.

- RBNZ dated OIS pricing closed 9-15bps softer across meetings. 34bps of easing had been priced for this meeting. A cumulative 62bps of easing had been priced by November 2025 versus 75bps now (including today’s move).

- Tomorrow, the local calendar will see the NZ Government 12-Month Financial Statements.

- The NZ Treasury also plans to sell NZ$275mn of the 1.50% May-31 bond and NZ$175mn of the 4.25% May-34 bond.

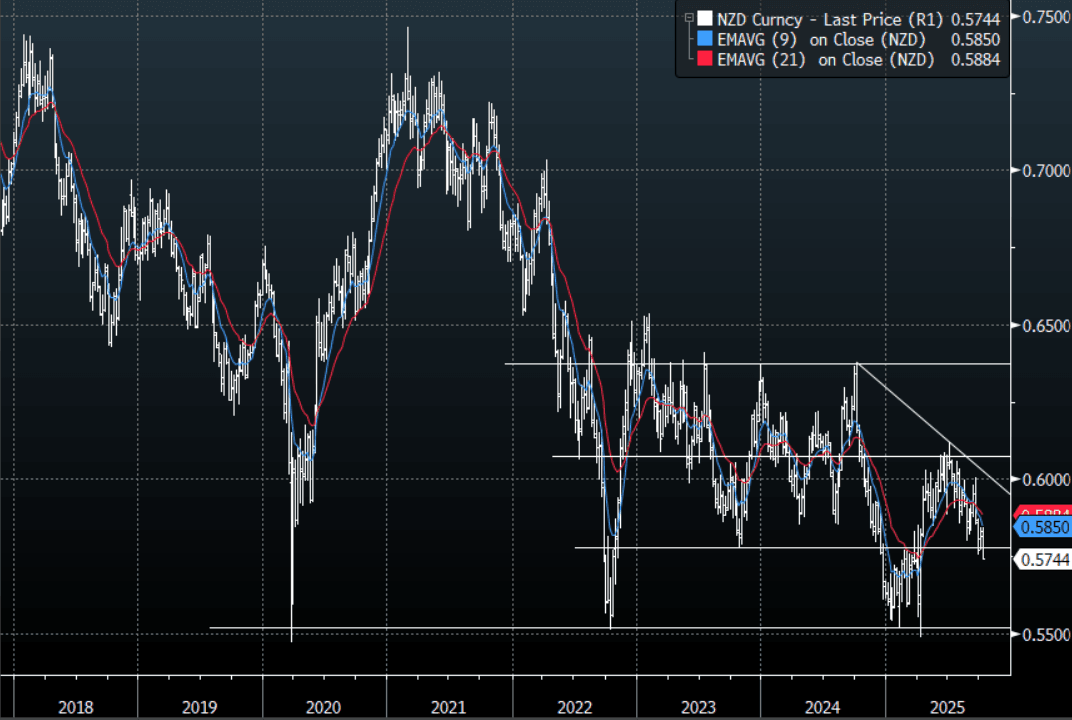

NZD: Asia-Pac: NZD/USD Breaks Lower As RBNZ Surprises Market With 50bps Cut

The NZD/USD had a range of 0.5739 - 0.5802 in the Asia-Pac session, going into the London open trading around 0.5745, -0.95%. A dovish surprise 50bps cut by the RBNZ has given the NZD/USD the momentum to extend below 0.5800 and is currently pressing the 0.5750 area. The market has already had a decent move on the day but rallies should now be faded. Should NZD/USD sustain the break through this support the focus will turn toward the multiple bottoms toward the 0.5500 area.

- MNI - RBNZ: Larger Cut Gives Sluggish Economic Recovery Extra Boost, Easing Bias. The MPC discussed cutting the OCR by 25bp or 50bp and all members agreed the latter was appropriate given material spare capacity in the economy. Given that this is likely to persist for some time and that while the economy has begun to recover it remains lacklustre, further cuts bringing policy into stimulatory territory are likely. In line with this it said that “the Committee remains open to further reductions in the OCR”

- RBNZ dated OIS pricing closed 9-15bps softer across meetings. 34bps of easing had been priced for this meeting. A cumulative 62bps of easing had been priced by November 2025 versus 75bps now (including today's move).

- "ANZ BANK NOW SEES RBNZ CUTTING CASH RATE TO 2.25% IN NOVEMBER" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5820(NZD305m). Upcoming Close Strikes : none - BBG

- AUD/NZD range for the session has been 1.1342 - 1.1446, currently trading around 1.1425. The Cross has surged back above 1.1400 on the surprise 50bps cut. I continue to feel the cross should do some work towards the 1.1500 area. A clear sustained break above 1.15/1.16 resistance and the market will begin to think about levels back towards 1.2000 and above.

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

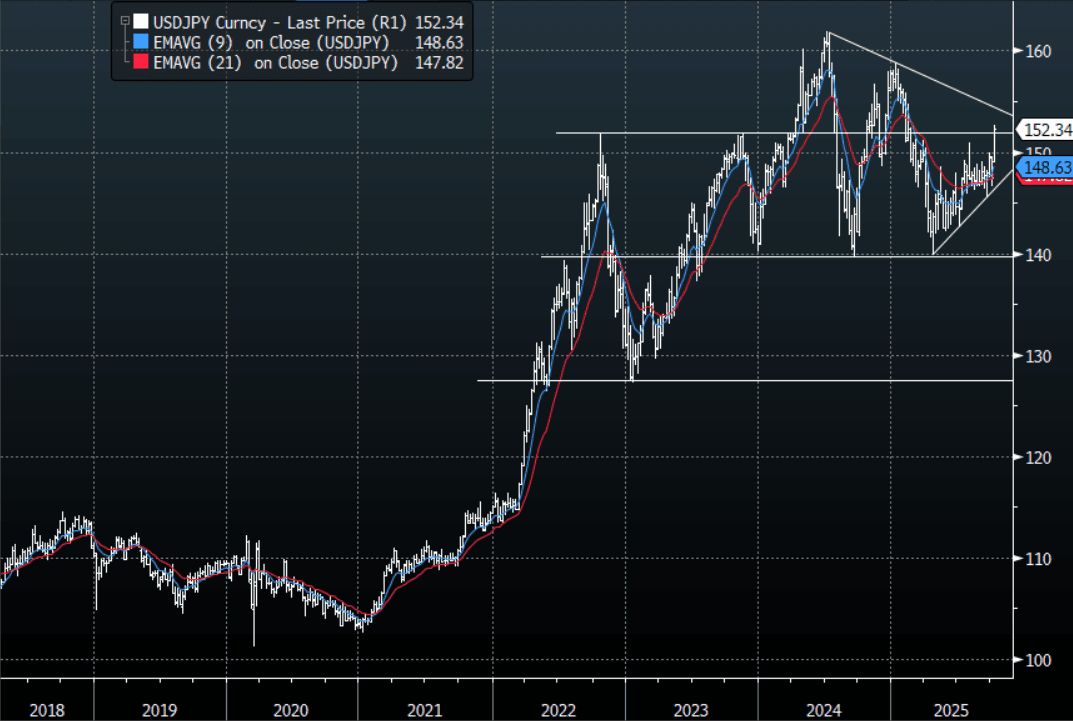

JPY: Asia-Pac: USD/JPY Breaking Above 152.00 If Sustained Targets 155-160 Area

The USD/JPY range has been 151.74 - 152.65 in the Asia-Pac session, it is currently trading around 152.35, +0.30%. The pair has extended its move higher in Asia and is attempting to break above the pivotal 152.00 area, if this break is confirmed it will turn the focus back to the 155-160 area. The last CFTC data available showed Asset Managers remained notably long JPY, should these moves begin to gather momentum, they could be forced to first pare back their longs and then if these significant levels are broken begin to rebuild JPY shorts. Many crosses are breaking through some pivotal areas(CNH/JPY Above 21.00) as well and unless the government says something to contradict the markets thinking these could begin to gather momentum. Expect dips to now find support unless there is push back on the market's views of Takaichi’s policies.

- MNI - Aug Labor Earnings Notably Sub Forecasts, BoJ Likely Holding In Oct: August labour earnings data in Japan was comfortably below market expectations. Headline earnings rose 1.5%y/y (against a 2.7 forecast and 3.4% July outcome), while real earnings dipped back to -1.4%y/y (-0.5%) was forecast. Real earnings have not been in positive territory (in y/y terms) so far in 2025. This will reinforce expectations of the BoJ likely remaining on hold at the Oct policy meeting.

- “JAPAN RULING BLOC TO DELAY DIET SESSION TO OCT. 20 OR LATER:FNN" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 147.00($1.47b). Upcoming Close Strikes : 150.00($778m Oct 9), 150.15($1.08b Oct 9) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

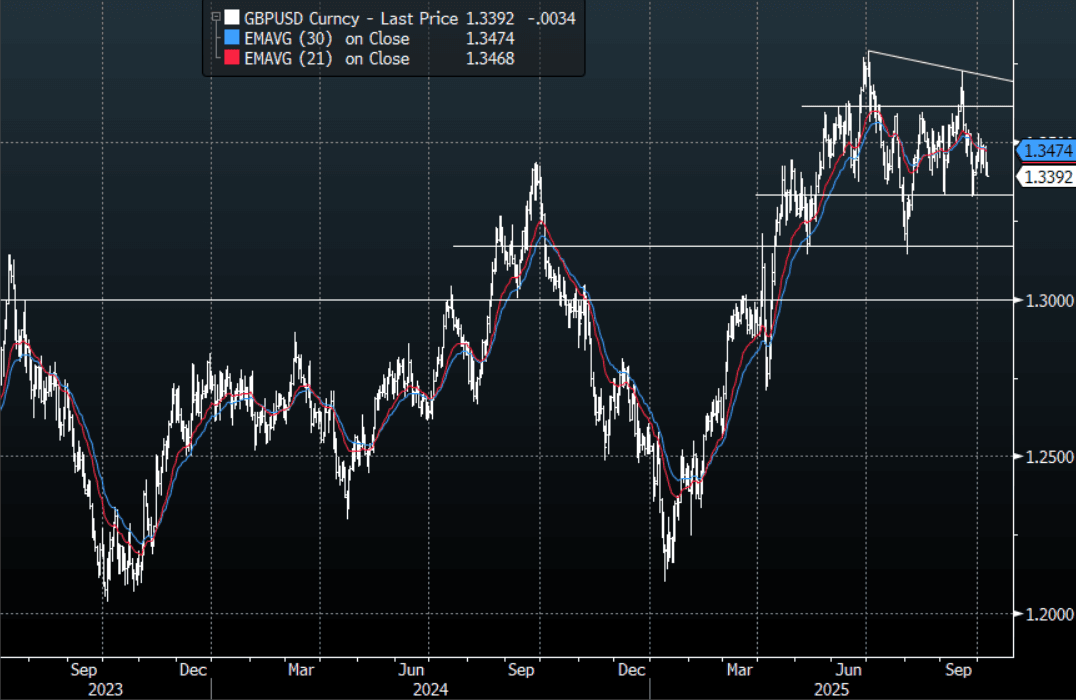

FOREX: Asia-Pac Wrap: The USD Builds On Its Overnight Gains

The BBDXY has had a range of 1208.46 - 1211.73 in the Asia-Pac session; it is currently trading around 1211, +0.15%. The USD has got a welcome reprieve from the surge in USD/JPY after failing to build any downward momentum below 1200 last week. This move extended overnight and again in our session as the USD continues to build on this pullback. The 1215-1225 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the USD shorts, but the weaker hands are definitely beginning to fold.

- EUR/USD - Asian range 1.1617 - 1.1661, Asia is currently trading 1.1620. The pair has begun to turn lower albeit still within its range as the USD bounce becomes more constructive. First support is back towards the 1.1550 area; a break through here could signal a deeper correction towards the more important 1.12001.1300 support.

- GBP/USD - Asian range 1.3391 - 1.3435, Asia is currently dealing around 1.3395. The pair continues to be capped on any move back towards the 1.3500 area. Cable needs a sustained break of the 1.3300 support to potentially signal a deeper move lower. Should this support give way the next support is around 1.3150 and it could signal a potential interim top in the pair.

- USD/CNH - Asian range 7.1443 - 7.1535, Asia is currently dealing around 7.1460. The area around 7.1500/1600 has proved to be solid resistance for now, it looks likely we could consolidate 7.09-7.16 for the moment. A break above here could signal a deeper pullback towards 7.20/22.

- Cross asset : SPX +0.15%, Gold $4025, US 10-Year 4.123%, BBDXY 1211, Crude Oil $62.23

- Data/Events : Germany Industrial Production SA

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

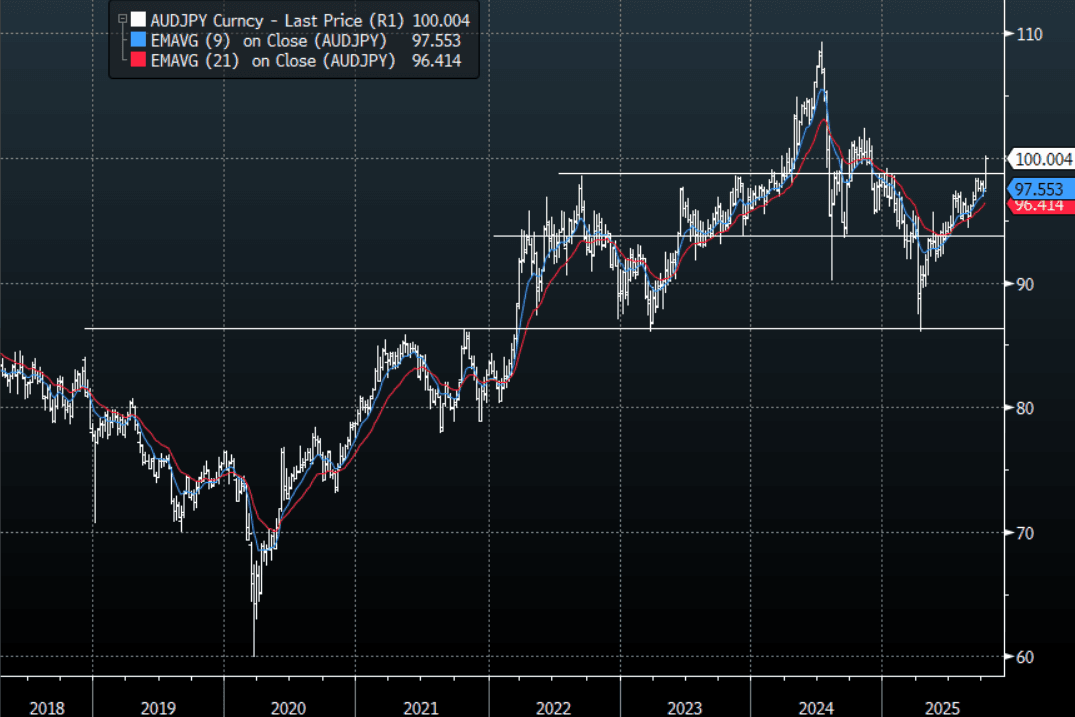

AUD: Asia-Pac: AUD/USD Drifts Lower In Sympathy With The NZD

The AUD/USD has had a range of 0.6558 - 0.6586 in the Asia- Pac session, it is currently trading around 0.6560, -0.30%. The AUD has continued to drift lower after topping out above 0.6600, this is in sympathy to the move in the NZD and the general bid tone of the USD. This puts the AUD firmly back within its recent range, and if the USD pullback continues to build the risk is skewed towards further losses, first support lies back toward the 0.6475 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6300(AUD899m), 0.6725(AUD 398m). Upcoming Close Strikes : 0.6545(AUD607m Oct 10) - BBG

- AUD/JPY - Asia-Pac range 99.89 - 100.20, Asia is trading around 100.05. The pair has surged higher breaking some pivotal resistance. The move extended higher overnight even with risk wobbling. Dips should now continue to be supported as the focus turns toward trying to break above 100 and then beyond.

Fig 1: AUD/JPY spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Tech Rally Takes A Breather

Asia Pac equities are mixed, with some caution coming through in tech/AI related space. Hong Kong markets have returned weaker, with the HSI down over 1%, tracking lower for third straight session. The tech sub index off over 1.1%. We did see US tech related bourses underperform in US Tuesday's trade, while the Golden Dragon index lost 2.24%. Note onshore China markets return tomorrow.

- Reuters also noted: "U.S. lawmakers are calling for broader bans on chipmaking equipment to China after a bipartisan investigation found that Chinese chipmakers had purchased $38 billion of sophisticated gear last year." This has potentially weighed on China tech related plays in Hong Kong.

- BBG also notes Citigroup analysts who stated that Golden Week box office results were below expectations (hurting sentiment in this space).

- Taiwan's Taiex is off around 0.50%, but still 2700, so close to recent record highs. Even with this recent run higher, offshore investors have only added modestly to local stocks, (but regional holidays, with China and South Korea still out may be a factor).

- In South East Asia, trends are mixed. Indonesia went to a fresh record high, but is now tracking modestly lower. Onshore government bond yields continue to fall, amid the dovish BI outlook, while consumer sentiment data for Sep fell to fresh lows since 2022.

- Thailand stocks are up ahead of an expected BoT cut later (last 0.55%). We also stimulus measures (0.3-0.4ppts of GDP) announced yesterday to boost consumption (via BBG).

- NZ stocks are outperforming Australia, after the 50bps RBNZ cut surprised the market.

OIL: Crude Continues Trending Higher Ahead Of EIA Data & Fedspeak

Oil prices continued trending higher during today’s APAC session with little news to give them direction. US industry-based data showed product drawdowns and the market continues to monitor strikes on Russian energy infrastructure which are impacting refining rates. For now the US EIA’s forecast of higher non-OPEC output and lower prices has been looked through but the IEA’s report is not until 14 October.

- WTI is up 0.9% to $62.28/bbl after rising to $62.36 and Brent is 0.8% higher at $65.95/bbl following a peak of $66.04. Both benchmarks are up around 2.2% since the weekend’s cautious OPEC decision.

- Official EIA oil data will still be released Wednesday as the agency is continuing to publish for now despite the US government shutdown. Bloomberg reported mixed industry-based data with oil inventories building but falling at key hub Cushing last week, according to people familiar with the API data. The reported product drawdown has likely provided support to prices today ahead of the EIA data.

- A soft outlook was reflected in the EIA’s October report as it is forecasting global oil inventories to build through next year pushing Brent down to $52/bbl from $62 in Q4 2025. Global output rises across its forecast horizon driven by non-OPEC. It doesn’t believe OPEC will be able to achieve its higher production targets helping to support prices.

- Later the Fed’s Musalem, Barr, Goolsbee, Kashkari and the ECB’s Lagarde, Elderson, Buch, Tuominen and BoE’s Pill speak. The September FOMC meeting minutes will also be published.

Gold Clears $4000 As Global Uncertainties Mount, More Fed Comments Later

Gold has tested psychological round number resistance at $4000 and decisively breached it reaching a record high of $4014.62 driven by political instability in the G7 that may not be resolved imminently. Issues in heavily indebted US, France and Japan are driving safe-haven flows, but ETF and central bank buying are providing structural support and geopolitics, US rate cuts and threats to Fed independence have also driven buying of gold. The US dollar (BBDXY +0.2%) has strengthened again today and yields are little changed, but gold’s rally is immune.

- Bullion is currently up 0.7% to around $4012.0/oz. Given it has rallied 4% so far this month and over 16% since 1 September, the risk of a pause in the uptrend is growing.

- The US shutdown is not just an issue for political stability but it also weighs on growth and government-issued data is being delayed making it difficult to gauge the economic situation ahead of the 29 October Fed decision. The OIS market has almost a full 25bp rate cut priced in for the meeting, despite a lack of data.

- Silver is outperforming gold after Tuesday’s underperformance. It is up 1.2% to $48.40, after a high of $48.46. It will also be benefiting from flight-to-quality flows as well as a tight physical market.

- Later the Fed’s Musalem, Barr, Goolsbee, Kashkari and the ECB’s Lagarde, Elderson, Buch, Tuominen and BoE’s Pill speak. The September FOMC meeting minutes will also be published.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 08/10/2025 | 0500/1400 | Economy Watcher's Survey | ||

| 08/10/2025 | 0600/0800 | ** | Industrial Production | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 08/10/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 08/10/2025 | 1030/1230 | ECB Elderson In Panel at Finance Conference | ||

| 08/10/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 08/10/2025 | 1320/0920 | St. Louis Fed's Alberto Musalem | ||

| 08/10/2025 | 1330/0930 | Fed Governor Michael Barr | ||

| 08/10/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 08/10/2025 | 1430/1030 | ** | US DOE Petroleum Supply | |

| 08/10/2025 | 1500/1600 | BOE Pill Speech at University of Birmingham | ||

| 08/10/2025 | 1600/1800 | ECB Lagarde Video Message at Werner Report Event | ||

| 08/10/2025 | 1700/1300 | ** | US Note 10 Year Treasury Auction Result | |

| 08/10/2025 | 1800/1400 | *** | FOMC Minutes | |

| 08/10/2025 | 1915/1515 | Minneapolis Fed's Neel Kashkari | ||

| 08/10/2025 | 2145/1745 | Fed Governor Michael Barr | ||

| 09/10/2025 | 0600/0800 | ** | Trade Balance | |

| 09/10/2025 | 0830/0930 | BOE Mann Keynote at Resolution Foundation Event | ||

| 09/10/2025 | 1145/0745 | BOC Sr Deputy Gov Rogers speaks in Toronto (time TBC) | ||

| 09/10/2025 | - | ECB Lagarde & Cipollone at Eurogroup Meeting | ||

| 09/10/2025 | 1230/0830 | *** | Jobless Claims | |

| 09/10/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 09/10/2025 | 1230/0830 | Fed Chair Jerome Powell | ||

| 09/10/2025 | 1235/0835 | Fed's Miki Bowman | ||

| 09/10/2025 | 1245/0845 | Fed's Miki Bowman |