AUD: Asia-Pac: AUD/USD Drifts Lower In Sympathy With The NZD

The AUD/USD has had a range of 0.6558 - 0.6586 in the Asia- Pac session, it is currently trading around 0.6560, -0.30%. The AUD has continued to drift lower after topping out above 0.6600, this is in sympathy to the move in the NZD and the general bid tone of the USD. This puts the AUD firmly back within its recent range, and if the USD pullback continues to build the risk is skewed towards further losses, first support lies back toward the 0.6475 area.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6300(AUD899m), 0.6725(AUD 398m). Upcoming Close Strikes : 0.6545(AUD607m Oct 10) - BBG

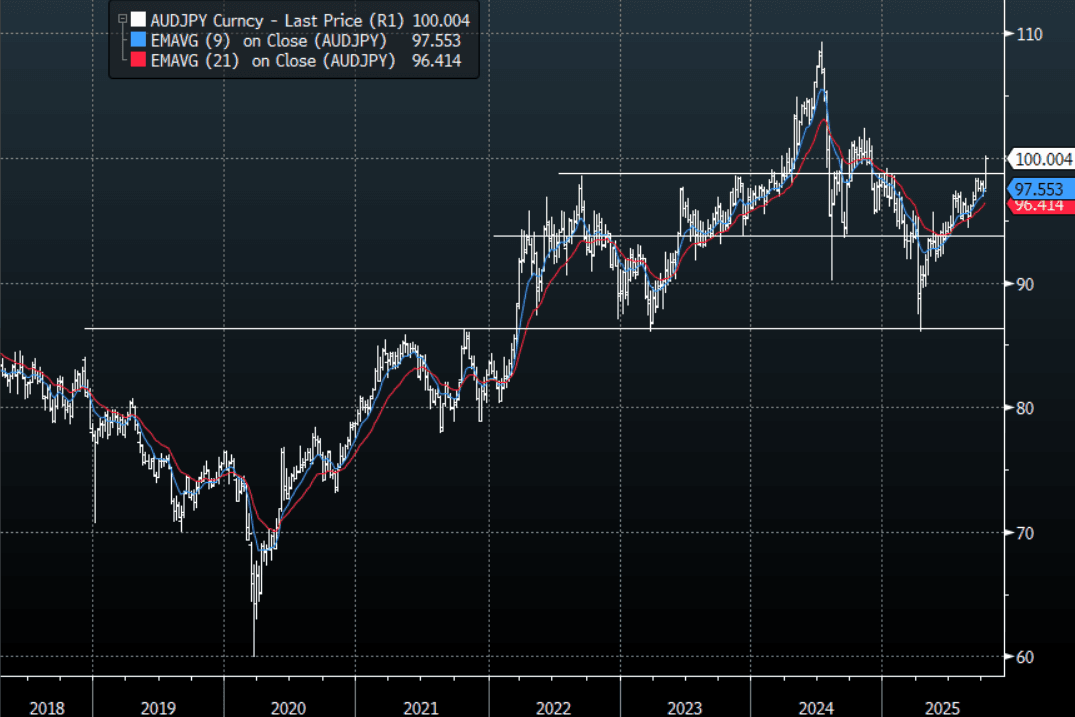

- AUD/JPY - Asia-Pac range 99.89 - 100.20, Asia is trading around 100.05. The pair has surged higher breaking some pivotal resistance. The move extended higher overnight even with risk wobbling. Dips should now continue to be supported as the focus turns toward trying to break above 100 and then beyond.

Fig 1: AUD/JPY spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

NZD: Asia Wrap - NZD/USD Consolidates Around 0.5900

The NZD/USD had a range of 0.5883 - 0.5904 in the Asia-Pac session, going into the London open trading around 0.5900, +0.12%. The NZD pushed higher in reaction to the NFP but found good selling above 0.5900 capping the move for now. This 0.5900-0.5950 area presents a good opportunity to fade for those who are bearish the NZD, but the caveat to this trade remains the USD’s ability to not break down. CFTC Data shows light positioning in a market that is struggling for a strong trend.

- Q2 manufacturing data print Tuesday including volumes. Manufacturing volumes rose 2.4% q/q in Q1. Q2 GDP prints on September 18, which the RBNZ expected to fall 0.3% q/q in its August projections.

- Bloomberg - “Dollar Vulnerability Turns to Downtrend on Payroll Miss. Further dollar weakness looks inevitable, with soft jobs data and falling rate expectations reinforcing the case for sustained downside. Together, easier Fed policy and the potential return of passive hedging flows create a feedback loop that makes sustained dollar strength increasingly difficult to justify.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5800(NZD515m Sept 10), 0.5870(NZD320m Sept 10) - BBG

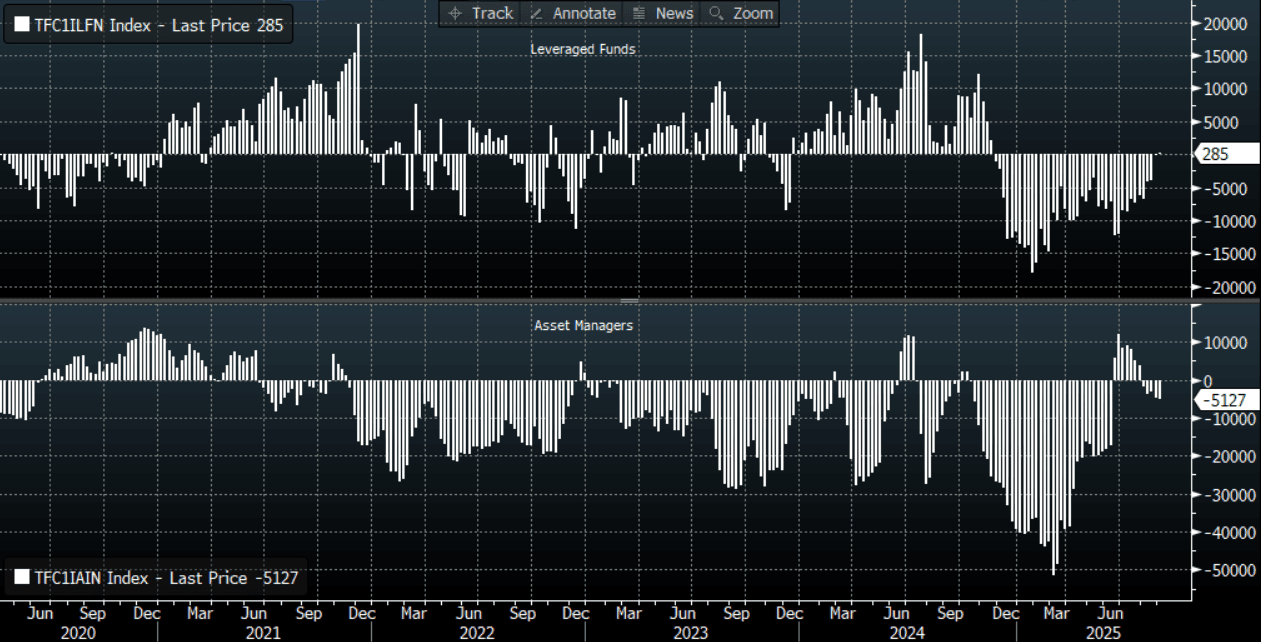

- CFTC Data of last week shows Asset Managers added slightly to their new short position in the NZD -5127(Last -4743), the Leveraged community have completely exited their short and have turned a fraction long +285(Last -225).

- AUD/NZD range for the session has been 1.1115 - 1.1133, currently trading 1.1120. The Cross is consolidating above 1.1100, dips back towards 1.1000/1.1050 should be supported now.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Futures Off Friday Highs, Swap Rates Higher For 20-40 Yr

JGB futures sit at 137.98, +.02 versus settlement levels in latest dealings. We are away from Friday highs (138.37), but dips under 138.00 have been support so far today.

- Focus remains on who will be the new PM, after Ishiba decided to step down over the weekend. Local media report that the leadership election may be held on Oct 4 (per TBS via BBG). An official announcement is expected tomorrow. A number candidates are likely to put their names forward.

- When Ishiba secured the PM position last Oct, the runner up was Sanae Takaichi. Via ABC news: "A Nikkei survey held at the end of August put Ms Takaichi as the most "fitting" successor to Ishiba." Takaichi could arguably generate the most significant market reaction if she is successful becoming the new PM, as she has been outspoken in terms of being more dovish in terms of the BoJ outlook and looking to boost fiscal spending. Former Minister, Toshimitsu Motegi, will reportedly run.

- Earlier on the data front, we had Q2 GDP revisions, which were firmer than market expectations. Stronger private consumption offset weaker capital investment the data showed.

- The cash JGB 2/30s curve is steeper, but away from session highs (+245bps) We were last +243bps. The outright 10yr yield is little changed, last near 1.575%.

- In the swap space, the move in 20-40yr rates has been larger than the cash JGB yield move. The 30yr is up around 5bps, last near 2.52%.

- Tomorrow on the data front, we have August money stock figures and August machine tool orders.

JPY: USD/JPY - Ishiba Gives Leveraged JPY Shorts A Reprieve

The Asia-Pac USD/JPY range has been 147.93-148.58, Asia is currently trading around 148.20, +0.50%. USD/JPY collapsed lower with US yields on Friday in reaction to the NFP, again challenging its support on a 146 handle. This support looked destined to be challenged to start this week but news of Ishiba stepping down has given the JPY bears another reprieve as the market has gapped higher on the open in response. CFTC data shows leveraged funds again added a decent clip to their short JPY position last week so this morning's move will have taken some pressure off them to start the week. Is this news enough to turn USD/JPY higher ? I suspect not but time will tell.

- MNI BRIEF: Japan Q2 GDP Revised Up On Consumption. Japan’s economy expanded faster in April-June than initially estimated, as stronger private consumption offset weaker capital investment, second preliminary GDP data from the Cabinet Office showed Monday.

- Focus will now turn to the LDP leadership race. When Ishiba secured the PM position last Oct, the runner up was Sanae Takaichi. Via ABC news: "A Nikkei survey held at the end of August put Ms Takaichi as the most "fitting" successor to Ishiba."

- Takaichi could arguably generate the most significant market reaction if she is successful becoming the new PM, as she has been outspoken in terms of being more dovish in terms of the BoJ outlook and looking to boost fiscal spending.

- "JAPAN LDP'S AIZAWA: WILL SET LEADERSHIP ELECTION DATE TUESDAY" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.00($1.1b), 149.00($882m), 145.75($792m).Upcoming Close Strikes : 145.75($1.12b Sept 11), 150.00($1.1b Sept 9) - BBG.

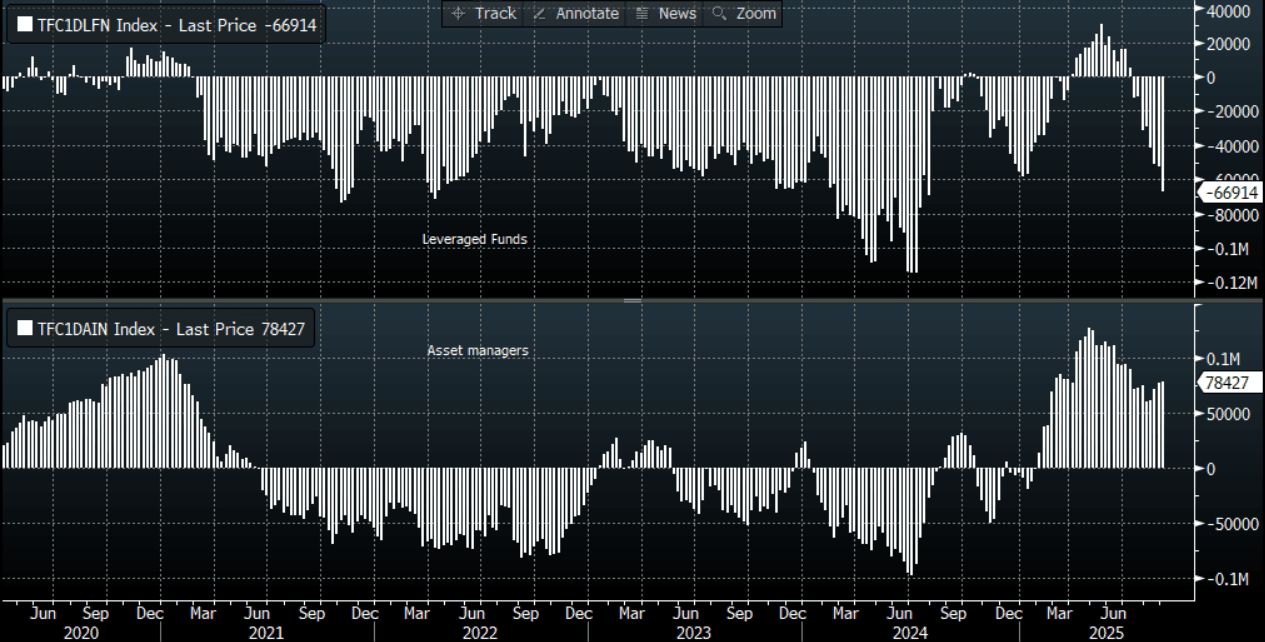

- CFTC data shows last week asset managers again added to their JPY longs after a consistent period of reduction +78427( Last +76761), leveraged funds though again used the dip to add a decent clip to their newly built short JPY position -66914(Last -52275). One of them is going to be wrong.

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P