MNI EUROPEAN OPEN: Mixed Jobs Data Weighs On NZD/Local Yields

EXECUTIVE SUMMARY

- TRUMP SAYS US TALKS WITH IRAN ONGOING AFTER DRONE SHOOTDOWN - BBG

- FED GOVERNOR MIRAN RESIGNS WHITE HOUSE POST - MNI BRIEF

- EU TO OFFER US CRITICAL MINERALS PARTNERSHIP TO CHECK CHINA - BBG

- UK UNEMPLOYMENT WILL PEAK AT 5.4% - NIESR

- NZ Q4 UNEMPLOYMENT RISES TO 5.4% - MNI BRIEF

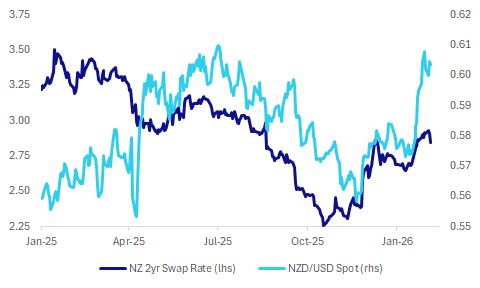

Fig 1: NZD/USD & NZ 2yr Swap Rate

Source: Bloomberg Finance L.P./MNI

UK

BOE (MNI BOE WATCH): The Bank of England is widely expected to leave Bank Rate on hold at 3.75% on Feb 5, with attention on forward guidance and its 2026 pay survey. Analysts anticipate a seven-two or six-three vote for a hold, after two consecutive five-four votes. Divisions within the Monetary Policy Committee have already been highlighted by a change in the statement format to include separate paragraphs written by each individual member

INFLATION (MNI INTERVIEW): UK food prices would increase by only 0.5% even if farmers pass on to consumers all of the cost of the government's Net Zero targets, which encourage them to use less fertiliser and reduce livestock numbers, a report by the Resolution Foundation think tank said on Wednesday.

UNEMPLOYMENT (MNI BRIEF): UK unemployment will peak at 5.4%, the National Institute of Economic and Social Research said in its quarterly forecast on Wednesday, as it expects 50 basis points of further cuts to Bank Rate this year.

UK-US (BBG): "Prime Minister Keir Starmer and President Donald Trump discussed the joint UK-US military base on Diego Garcia, a point of contention between the two countries after the president reversed his previous support for a plan to return sovereignty of the island to Mauritius."

EU

EU-US (MNI BRIEF): The European Parliament's negotiating team is continuing to discuss how to “Trump-proof” an EU-U.S. trade deal - which stalled following the clash over Greenland - ahead of an official vote on whether to resume work on the deal.

EU-US (BBG): “ The European Union will pitch the US on a critical minerals partnership to curb China’s influence, looking to shape the Trump administration’s push to strike global agreements this week.”

SPAIN (BBG): " Banco Santander SA agreed to acquire Webster Financial Corp. in a $12 billion deal that will allow Spain’s largest bank to bet big on the US."

FRANCE (BBG): "French far-right leader Marine Le Pen should stay banned from the 2027 presidential race, according to a prosecutor who also sought a confirmation of her conviction for embezzling European Union funds."

US

FED (MNI BRIEF): Federal Reserve Governor Stephen Miran has stepped down from his position as chair of the White House Council of Economic Advisers, MNI confirmed. Miran joined the Trump administration’s Council of Economic Advisers in January 2025. He had been on leave from this post since September 2025, when he became a member of the Federal Reserve Board of Governors. (See: MNI INTERVIEW: Fed’s Miran Sees Substantial Rate Cuts In 2026).

IRAN (BBG): "President Donald Trump reiterated that the US and Iran are maintaining diplomatic talks, even after an earlier skirmish in the Arabian Sea spooked oil markets amid heightened tensions between the two countries."

ECONOMY (MNI BRIEF): College graduates and higher income households continue to outspend their poorer counterparts in evidence of a bifurcated economy that raised concerns about the fragility of the expansion, New York Fed data published Tuesday showed.

FED (MNI BRIEF): The Federal Reserve should be ready to respond if labor market conditions deteriorate further but for now have taken some insurance against such deterioration, and data suggest a resilient economy and more inflation progress to come, Richmond Fed President Thomas Barkin said Tuesday.

OTHER

NEW ZEALAND (MNI BRIEF): New Zealand’s unemployment rate rose 10 basis points to 5.4% in the fourth quarter, up from 5.3% in Q3, data released by Stats NZ on Wednesday showed. The underutilisation rate was unchanged at 13.0%, while the employment rate edged up to 66.7% from 66.6% in the previous quarter.

SHIPPING (BBG): ' Tankers moving crude from the Middle East to China charged the highest fees in more than two months this week, after tensions over Iran combined with tight vessel supply to drive up prices."

CHINA

YUAN (BBG): "Bank of America Corp. boosted its forecast for the yuan, joining other Wall Street banks in raising their estimates on bets that China’s central bank will tolerate further gains in the currency."

HOUSING (SECURITIES DAILY): "More cities are expected to carry out the acquisition of second-hand homes for affordable housing, after Shanghai kicked off the campaign, Securities Daily reported citing analysts."

MNI: PBOC Net Drains CNY302.5 Bln via OMO Wednesday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY75 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net drain of CNY302.5 billion after offsetting the maturity of CNY377.5 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4000% at 09:43 am local time from the close of 1.4972% on Tuesday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 50 on Tuesday, compared with the close of 49 on Monday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 6.9533 Weds; +5.36% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 6.9533 on Wednesday, compared with 6.9608 set on Tuesday. The fixing was estimated at 6.9363 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND Q4 EMPLOYMENT CHANGE Q/Q 0.5%; MEDIAN 0.3%; PRIOR 0.0%

NEW ZEALAND Q4 EMPLOYMENT CHANGE Y/Y 0.2%; MEDIAN -0.1%; PRIOR -0.7%

NEW ZEALAND Q4 UNEMPLOYMENT RATE 5.4%; MEDIAN 5.3%; PRIOR 5.3%

NEW ZEALAND Q4 PARTICIPATION RATE 70.5%; MEDIAN 70.3%; PRIOR 70.3%

NEW ZEALAND Q4 PVT WAGES INC OVERTIME Q/Q 0.5%; MEDIAN 0.5%; PRIOR 0.4%

NEW ZEALAND Q4 AVERAGE HOURLY EARNIGNS Q/Q 0.7%; PRIOR 0.7%

AUSTRALIA JAN F S&P GLOBAL PMI SERVICES 56.3; PRIOR 56.0

AUSTRALIA JAN F S&P GLOBAL PMI COMPOSITE 53.1; PRIOR 52.8

JAPAN JAN F S&P GLOBAL PMI SERVICES 53.7; PRIOR 53.4

JAPAN JAN F S&P GLOBAL PMI COMPOSITE 53.1; PRIOR 52.8

CHINA JAN RATING DOG PMI SERVICES 52.3; MEDIAN 52.0; PRIOR 52.0

CHINA JAN RATING DOG PMI COMPOSITE 51.6; PRIOR 51.3

SOUTH KOREA JAN FX RESERVES $425.91BN; PRIOR $428.05BN

MARKETS

US TSYS: Neutral Bias Remains, Despite Yields Near 1 Month Highs

The US 10-Yr future traded in a 111-17+ to 111-21+ range today, treading water for much of the day even as many major equity bourses weakened. The 10-Yr moved lower initially but stabilized at 111-19+, just below its opening level of 111-20

Front end cash was flat with longer dated USTs only modestly higher in yield, having on a weak tone but with some modest improvement as equities stalled.

- The 2-Yr up +0.2bps to 3.574%

- The 5-Yr is up +0.2bps to 3.837%

- The 10-Yr up +0.6bps to 4.274%

- The 30-Yr up +0.6bps to 4.902%

US equity futures are point pointing to a mixed start at this stage, and with Friday's NFP delayed, focus turns to the treasury refunding announcement, though not markets not expecting any surprises. There will be a US$17bn 17-week auction.

Investors remain sensitive to shifts in the "Fed regime" as the transition toward Warsh approaches. Bostic speaks Wednesday and markets will look for guidance on how the committee views the recent bounce in manufacturing activity .

ADP Employment change is key, with private sector employment is expected to show an increase of 45k for January, up from December's gain of 41,000.

This ISM Services Index is forecast to drop to 53.5 (from 54.4 in December). Markets will closely watch the Prices sub-index (forecast at 64.0) for signs of cooling inflationary pressure.

JGBS: Modest Rally Across Curve, 5Y Remains Vulnerable, 30Y Supply Tomorrow

JGB futures are stronger, +12 compared to settlement levels.

- Cash JGBs are 1-2bps richer across benchmarks, with the futures-linked 7-year outperforming.

- After Tuesday’s underwhelming 10-year auction, where the bid-to-cover ratio fell below its 12-month average, attention turns to tomorrow's 30-year supply.

- The yield curve remains near its steepest on record, although it has traded within a well-defined range since mid-2025.

- Since late last year, the 2s/5s segment has seen the most pronounced steepening, with the 5-year sitting in a relatively unfavoured part of the curve. Several factors continue to weigh on the 5-year sector:

- A potential fiscal boost under a Takaichi administration would imply increased debt supply, adding pressure to the sector.

- The threat that renewed yen weakness could bring forward BOJ rate hikes relative to current pricing.

- The 5-year has recently been, and is likely to remain, a preferred duration to short for more aggressive traders. In particular, the strategy of shorting 5-year versus 30-year bonds to express flattening themes appears to have further room to run as the BOJ moves closer to another hike.

- Swap rates are 1-2bps lower.

- Tomorrow, the local calendar will see Weekly International Investment Flow data.

Source: Bloomberg Finance LP

AUSSIE BONDS: Post-RBA Weakness Remains

ACGBs (YM -4.0 & XM -3.0) are weaker, having extended yesterday’s post-RBA sell-off. ACGB futures are 3-7bps weaker than yesterday’s pre-RBA levels, with a flatter curve. Nevertheless, futures remain above yesterday’s intraday lows

- See MNI RBA Review Hidden PDF.

- Cash US tsys are slightly cheaper in today’s Asia-Pac session.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at +59bps.

- Today’s auction result extended the trend of firm pricing for ACGBs, with the weighted average yield printing 0.16bps through prevailing mids, according to Yieldbroker. Moreover, demand was stronger, as reflected by a cover ratio of 3.7250x, up from the prior 3.1950x.

- The increase in demand came with the bond’s outright yield at its cycle high, ~15bps higher than the previous outing. However, the 3/10 yield curve was around its flattest level since late 2024, approximately 40bps flatter than at the time of its syndicated sale.

- The AOFM plans to sell A$800mn of the 1.00% 21 December 2030 bond on Friday.

- The bills strip has bear-steepened, with pricing -1 to -4 across contracts.

- RBA-dated OIS pricing is firmer again today across meetings, extending yesterday’s post-RBA decision sell-off. Currently, pricing is 6-10bps firmer across meetings than pre-RBA level.

- Tomorrow, the local calendar will see Trade Balance.

BONDS: NZGBS: Q4 Jobs Report Extends Rally

NZGBs closed 4-5bps richer after today’s Q4 Employment Report.

- NZ-US and NZ-AU 10-year differentials finished 3bps lower.

- The NZ Q4 jobs report was a mixed bag. On the positive side, the jobs growth picture was better than forecast, rising 0.5%q/q, versus 0.3% forecast and flat in Q3. This was the strongest q/q rise since Q2 2023. It also bought the y/y pace back to positive territory at 0.2% from a revised 0.7%y/y fall in Q3.

- The unemployment rate edged up to 5.4%, above both the market consensus and RBNZ forecast of 5.3%. The participation rate rose to 70.5%, versus 70.3% forecast. Arguably we would have needed to see a combination of stronger jobs growth and a lower unemployment rate to get the market more excited about a potentially earlier 2026 rate hike from the RBNZ.

- Swap rates closed 5-7bps lower, with a steeper 2s10s curve.

- RBNZ-dated OIS pricing closed softer for late 2026 meetings. No tightening is priced for February, while December 2026 assigns 46bps, 5bps softer than yesterday’s close.

- Tomorrow, the local calendar will see Cotality Home Value data.

- The NZ Treasury also plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

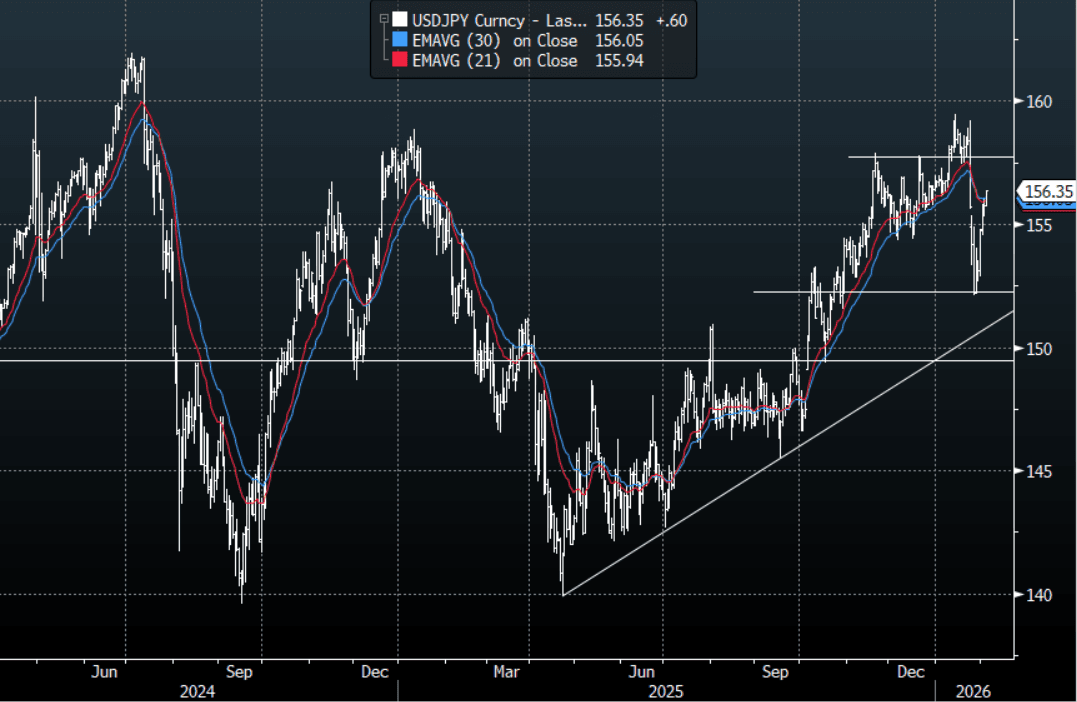

JPY: USD/JPY - Drifts Above 156.00 As The Election Looms

The USD/JPY range today has been 155.70 - 156.39 in the Asia-Pac session, it is currently trading around 156.35. USD/JPY continues to grind back up as we get closer to the weekend elections. A large portion of the leveraged short Yen positions being built up heading into the elections would have been washed out thanks to the Fed/MOF rate check after the BOJ rate decision. This large move lower was more down to overextended positioning than fundamentals and as we head toward this weekend's election all the reasons for the Yen short will come back to the fore. This should see USD/JPY which has lost its immediate upward momentum remain well supported on dips as the market looks toward the 160.00 area once again. Resistance on the day should be around 156.50-157.00 and support is back towards the 155.00 area.

- “Hedge funds are reviving bets against the yen and positioning for renewed weakness as Japan heads into a pivotal election.” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 153.25($801m), 159.50($769m). Upcoming Close Strikes : 153.00($1.59b Feb 5), 154.00($1.13b Feb 5) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 145 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: USD - Treading Water Around The 1190 Area In BBDXY

The BBDXY has had a range today of 1187.30 - 1188.85 in the Asia-Pac session; it is currently trading around 1188. Risk could not hold onto the ISM gains and has quickly given them up as the rotation out of Tech picks up pace. The USD is treading water around the 1190 area and it is still tough to have any strong conviction on its next medium term direction. I suspect that bounces will continue to find sellers in the short-term as the USD still has few friends, but the caveat being if we do have some sort of a correction in Stocks will the USD safe haven bid come back ? The market is not positioned for this. On the day, the first resistance is toward the 1193-1198 area and then more importantly back above 1200 where I suspect sellers could return.

- EUR/USD - Asian range 1.1809-1.1832, Asia is currently trading 1.1830. Price action has left an ugly bearish shadow on the weekly chart, but we are approaching levels that should start to see some buyers return. On the day, the support remains between the 1.1760-1.1790 area, a move through here could signal a deeper reversion back to the important 1.1700 area where I suspect buyers would again be around. I suspect a bounce back toward the 1.1870-1.1910 area would find sellers first up as the pair looks to consolidate as the market tries to get some conviction on how it thinks the USD will trade from here.

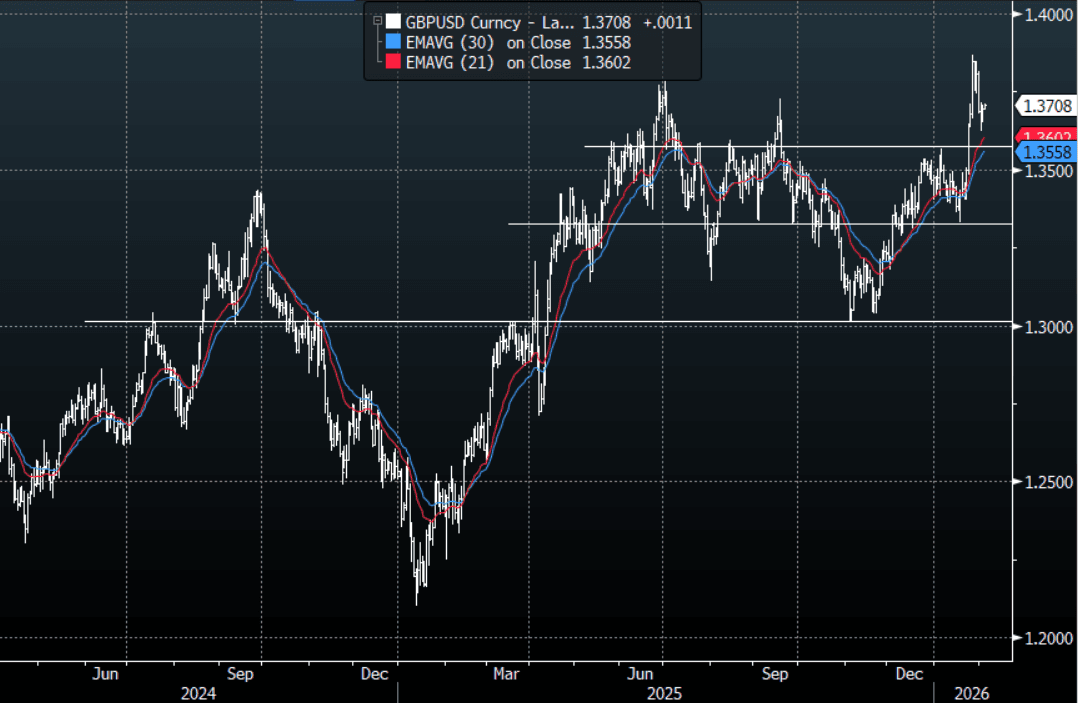

- GBP/USD - Asian range 1.3691-1.3713, Asia is currently dealing around 1.3710. The pair like everything else had an ugly weekly close leaving a clear rejection of the 1.3850 area. On the day, first support is 1.3600-1.3650 then the 1.3500 area.

- Cross asset : SPX +0.05%, Gold $5060, US 10-Year 4.27%, BBDXY 1188, Crude Oil $63.80

- Data/Events : Italy HCOB Italy Services PMI/CPI, Spain HCOB Spain Services PMI, France HCOB France Services PMI, Germany HCOB Germany Services PMI, EZ HCOB Eurozone Services PMI/PPI/CPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD/USD - Holding Above 0.7000

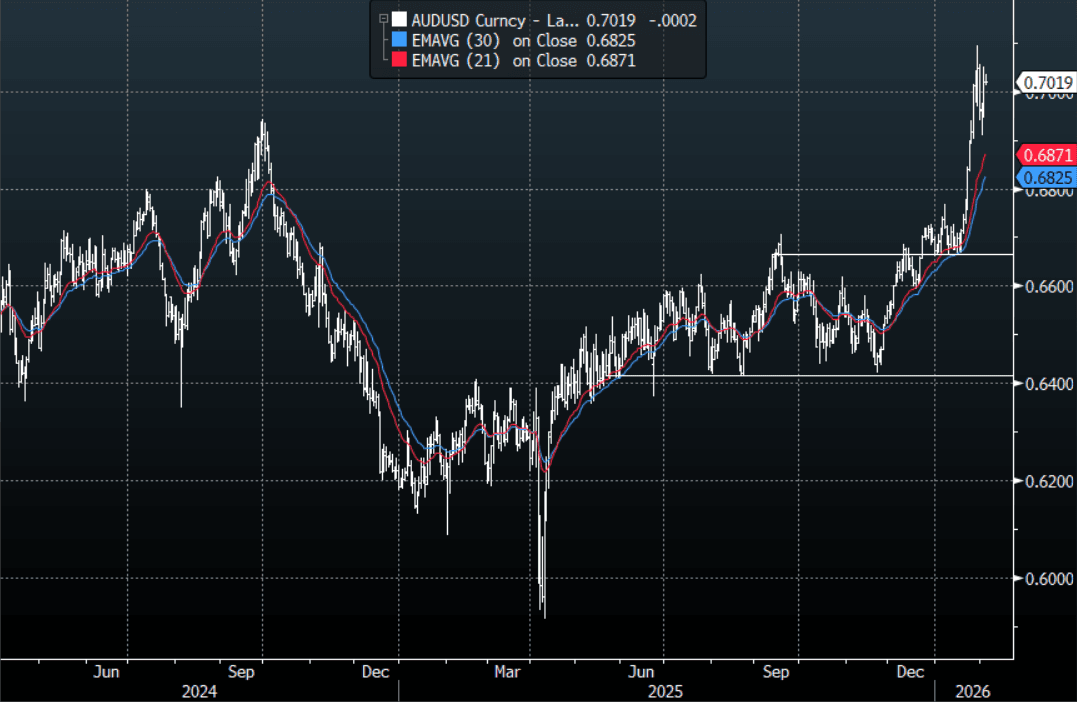

The AUD/USD has had a range today of 0.7013 - 7036 in the Asia- Pac session, it is currently trading around 0.7020. The AUD is holding above 0.7000 for now even as stocks have another pullback from their highs stalling the pairs upward momentum momentarily. The AUD has been outperforming across the board as leveraged funds increased their longs anticipating yesterday's hike, I suspect these trades will now begin to be added to as further hikes are priced in. On the day, the first buy-zone is toward the 0.6970-0.7000 area, if this does not hold we could see a deeper pullback toward 0.6900 where I suspect buyers could be lining up. The AUD is looking to regain its upward momentum to test the pivotal 0.7100-0.7200 and potentially extend higher from there.

- MNI RBA Review-Feb 2026: Further Tightening Likely Needed: The RBA raised the cash rate to 3.85%, as expected by the sell-side consensus and which was largely priced by the market. The decision was unanimous by the board. The risks appear skewed towards further action to ensure that inflation moves sustainably back into the target band of 2-3%.

- RBA-dated OIS pricing is firmer again today across meetings, extending yesterday's post-RBA decision sell-off. That leaves RBA-dated OIS showing tightening across all meetings, with the probability of a 25bp hike rising from 17% for March to 105% by June and 172% by December 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6950(AUD1.96b). Upcoming Close Strikes : 0.6860(AUD1.51b Feb 9), 0.6875(AUD913m Feb 6), 0.6900(AUD1.64b Feb 9) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 84 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

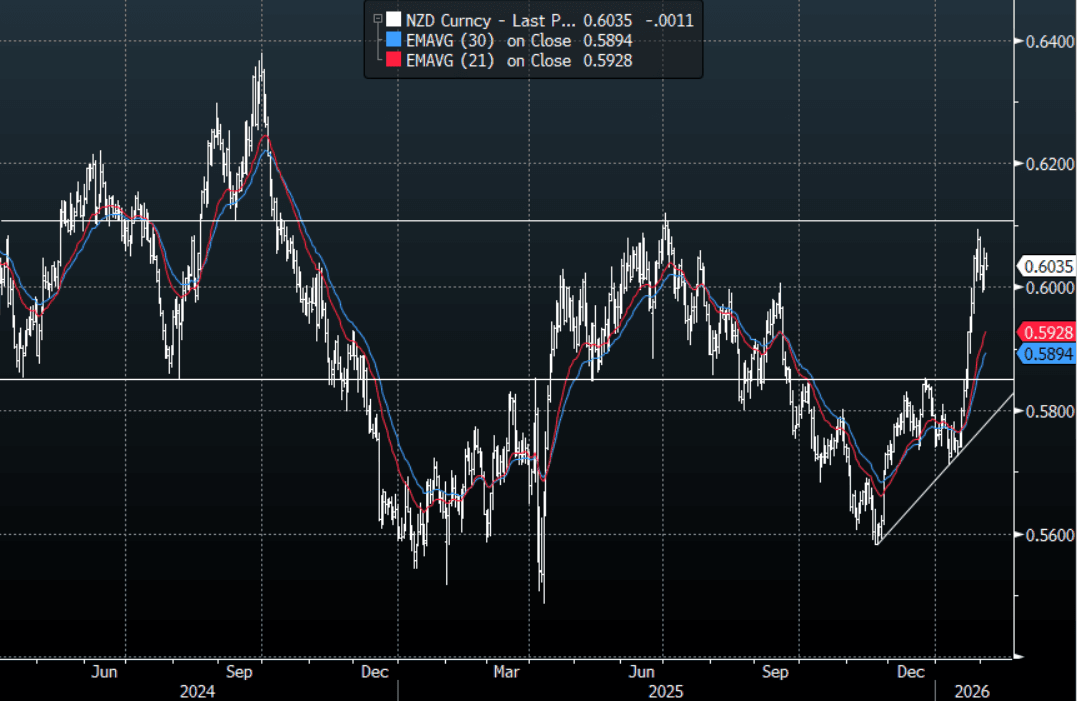

NZD/USD - Pulls Back From 0.6060 On Unemployment Data

The NZD/USD had a range today of 0.6028-0.6063 in the Asia-Pac session, it is currently trading around 0.6035, -0.20%. The NZD topped out above 0.6060 and moved lower as the unemployment rate is likely to keep the RBNZ on hold for now. On the day, the first support is around the 0.5985-0.6015 area as the market looks to regain its upward momentum. A break below here could signal a deeper pullback toward 0.5900 and put the test of 0.6100 off for a while.

- MNI AU - NZ Firmer Jobs Growth Offset By Higher U/E Rate, RBNZ Likely On Hold : The NZ Q4 jobs report was a mixed bag. On the positive side, the jobs growth picture was better than forecast. The unemployment rate though edged up to 5.4%, above both the market consensus and RBNZ forecast of 5.3%. Arguably we would have needed to see a combination of stronger jobs growth and a lower unemployment rate to get the market more excited about a potentially earlier 2026 rate hike from the RBNZ.

- “Less Hawkish RBNZ Pricing Better Reflects OCR Outlook, ANZ Says. “Markets had gotten well ahead of themselves in terms of the outlook” for rate hikes, says a senior strategist at ANZ Bank NZ.” - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5975(NZD746m). Upcoming Close Strikes : 0.5910(NZD399m Feb 5) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 62 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: US Lead Weighs on Japan and China, India's Momentum Builds

- Japanese stocks led the region lower today, unable to hold onto early gains and down -0.95%. Yesterday's run up in stocks with gains of almost 4% saw profit takers emerge Wednesday and some sector specific selling in tech following the US lead overnight. Downside looks capped for now as EMA's remain upward sloping and the NKY remains near to neutral on momentum indicators.

- The lead in from the US and Japan set China's major bourse on the back foot Wednesday, with major bourses down around -0.50%. Investors are likely positioning ahead of Chinese New Year and with the gold related volatility of last week still fresh in their minds, it seems likely that a more cautious approach will bias investors for now.

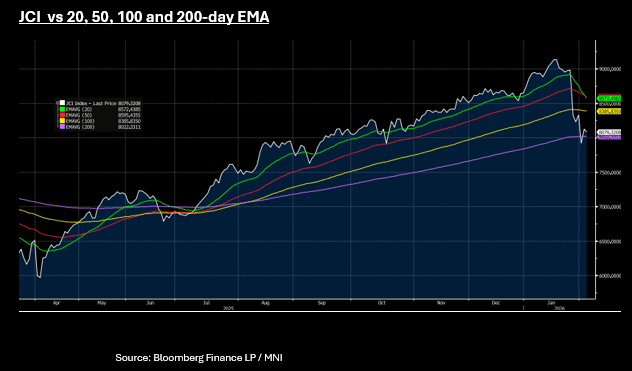

- Despite the Fin Mins assurances during a BBG TV interview, the JCI is down today, following a similar pattern to the NKY. Yesterday's gains of +2.5% has seen profit takers emerge, still cautious after the volatility of last week. The JCI is holding above 8,000, but as the 20-day EMA dips below the 50-day EMA, it suggests the short term negative momentum is outpacing the medium term trend. The JCI is holding above the 200-day EMA of 8,022, with last week's lows at 7,941.

The NIFTY 50 has opened modestly higher Wednesday, up over +3.5% since Sunday's close, having opened for the budget. The US tariff agreement continues to feed into an improved sentiment with the index above all moving averages, whilst largely neutral on momentum indicators, suggesting this positive momentum could continue.

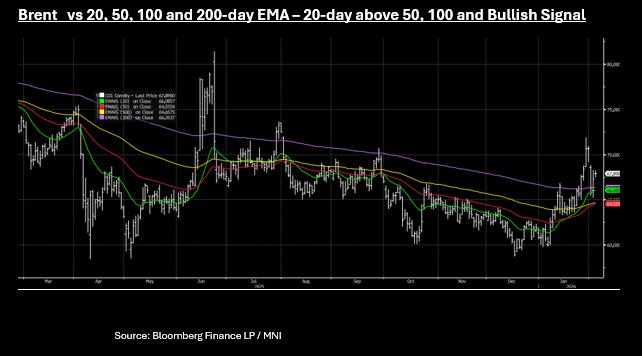

OIL: EMAs Point to Bullish Uptrend as Oil Rises Again

- Oil's overnight rally continued in Asia with WTI up 1%. WTI has traded in a range of $63.47 - $64.17 but was unable to hold above $64, settling back below at $63.83 bbl.

- The technical backdrop remains positive for WTI with a bullish crossover, where the 20-day trades above the 50 and 100-day EMAs signaling that the short term momentum is outpacing the medium term trend.

- Brent has traded in a $67.50- $68.26 context but could not hold above $68, slipping back below and settling at $67.87 bbl and a similar technical backdrop to WTI.

- News of a US warship shooting down an Iranian drone saw oil in a bullish reversal begin late Tuesday. US forces also intervened in the Strait of Hormuz after armed Iranian boats reportedly harassed a US-flagged merchant vessel. President Trump told reporters that "We are negotiating with them (Iran) right now" and "they'd like to do something." "They had a chance to do something a while ago and it didn't work out, and we did Midnight Hammer," he said, referring to the June US military strike in Iran and a likely reminder of the consequences for Iran.

- Official data out Wednesday will provide US crude inventories updates which are expected to fall, with BBG reporting that the drawdown could be the largest since June.

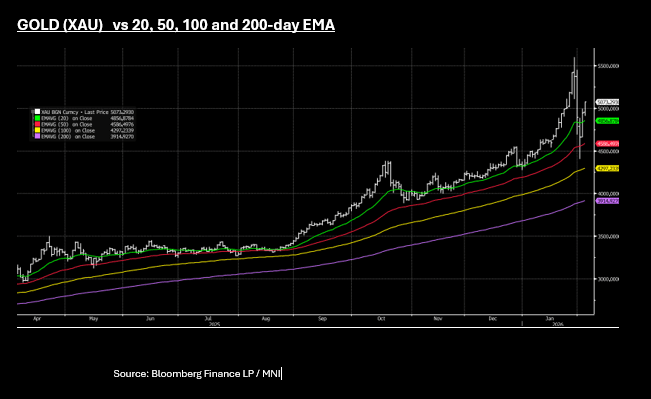

GOLD: $5,000 Poses No Challenge for Gold as Rally Resumes

- If gold's move overnight in the US looked like a technically driven relief rally, today's move looked increasingly like dip buyers taking charge.

- With the USD steady and risk sentiment strong, gold opened at US$4,952 and rallied from the outset, with the psychological level of $5,000 posing now resistance.

- Gold is currently up +2.45% at $5,068.37 and with momentum indicators remain fairly neutral and above all EMA's, the next key resistance is at $5,100.

- As a second retail focused gold trading platform in China signaled a funding shortfall following outflows last week, there may be an element of seasonality ahead of the Lunar New Year where demand from Chinese retail investors and households has provided a strong support historically,

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/02/2026 | 0815/0915 | ** | S&P Global Services & Composite PMI (f) | |

| 04/02/2026 | 0830/0930 | Riksbank Minutes | ||

| 04/02/2026 | 0845/0945 | ** | S&P Global Composite & Services PMI (f) | |

| 04/02/2026 | 0850/0950 | ** | S&P Global Composite & Services PMI (f) | |

| 04/02/2026 | 0855/0955 | ** | S&P Global Composite & Services PMI (f) | |

| 04/02/2026 | 0900/1000 | ** | S&P Global Composite & Services PMI (f) | |

| 04/02/2026 | 0930/0930 | ** | S&P Global Composite & Services PMI (Final) | |

| 04/02/2026 | 1000/1100 | ** | EZ PPI | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash | |

| 04/02/2026 | 1000/1100 | *** | EZ HICP Flash (2dp) | |

| 04/02/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 04/02/2026 | 1000/1100 | *** | HICP (p) | |

| 04/02/2026 | 1000/1100 | *** | Italy Flash Inflation | |

| 04/02/2026 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 04/02/2026 | 1315/0815 | *** | ADP Employment Report | |

| 04/02/2026 | 1330/0830 | *** | Treasury Quarterly Refunding | |

| 04/02/2026 | 1445/0945 | *** | S&P Global Composite & Services Index (final) | |

| 04/02/2026 | 1500/1000 | *** | ISM Non-Manufacturing Index | |

| 04/02/2026 | 1500/1000 | Treasury Secretary Scott Bessent | ||

| 04/02/2026 | 1530/1030 | ** | US DOE Petroleum Supply | |

| 04/02/2026 | 1530/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 04/02/2026 | 1700/1200 | Richmond Fed's Tom Barkin | ||

| 04/02/2026 | 2330/1830 | Fed Governor Lisa Cook | ||

| 05/02/2026 | 0030/1130 | ** | Trade Balance | |

| 05/02/2026 | 0700/0800 | ** | Manufacturing Orders | |

| 05/02/2026 | 0745/0845 | * | Industrial Production | |

| 05/02/2026 | 0830/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 05/02/2026 | 0900/1000 | * | Retail Sales | |

| 05/02/2026 | 0930/0930 | ** | S&P Global/CIPS Construction PMI | |

| 05/02/2026 | 1000/1100 | ** | EZ Retail Sales | |

| 05/02/2026 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 05/02/2026 | 1200/1200 | *** | Bank Of England Interest Rate | |

| 05/02/2026 | 1230/1230 | BOE Press Conference | ||

| 05/02/2026 | - | European Central Bank Meeting | ||

| 05/02/2026 | 1315/1415 | *** | ECB Deposit Rate | |

| 05/02/2026 | 1315/1415 | *** | ECB Main Refi Rate | |

| 05/02/2026 | 1315/1415 | *** | ECB Marginal Lending Rate | |

| 05/02/2026 | 1330/0830 | *** | Jobless Claims | |

| 05/02/2026 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 05/02/2026 | 1345/1445 | ECB Press Conference |