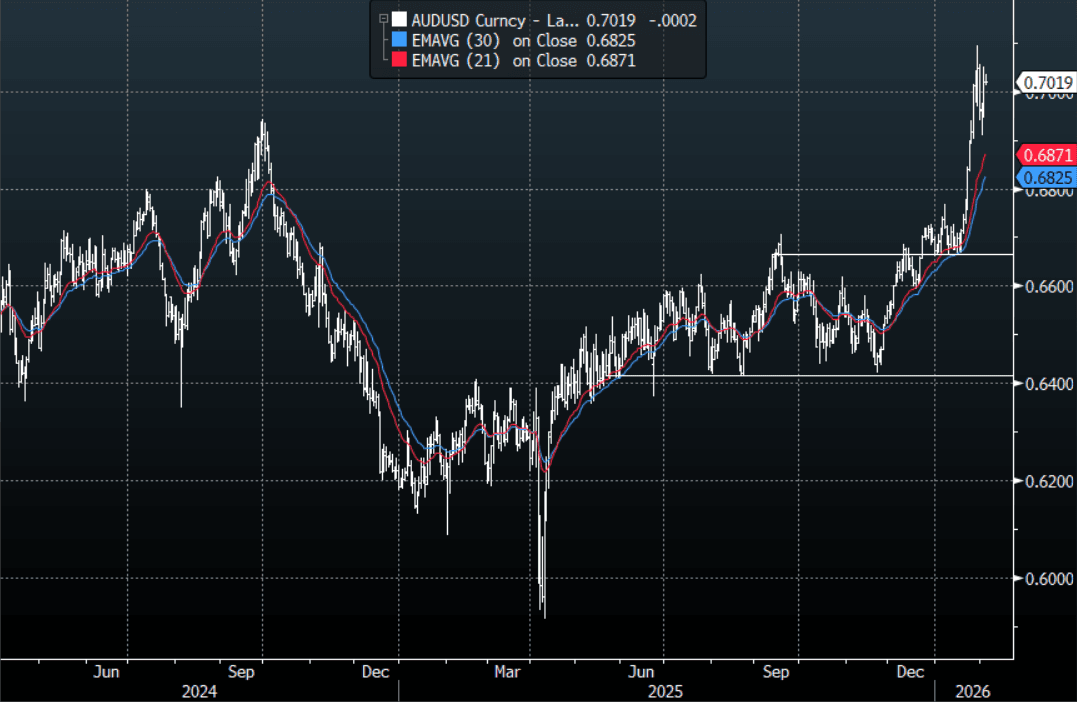

AUD: AUD/USD - Holding Above 0.7000

The AUD/USD has had a range today of 0.7013 - 7036 in the Asia- Pac session, it is currently trading around 0.7020. The AUD is holding above 0.7000 for now even as stocks have another pullback from their highs stalling the pairs upward momentum momentarily. The AUD has been outperforming across the board as leveraged funds increased their longs anticipating yesterday's hike, I suspect these trades will now begin to be added to as further hikes are priced in. On the day, the first buy-zone is toward the 0.6970-0.7000 area, if this does not hold we could see a deeper pullback toward 0.6900 where I suspect buyers could be lining up. The AUD is looking to regain its upward momentum to test the pivotal 0.7100-0.7200 and potentially extend higher from there.

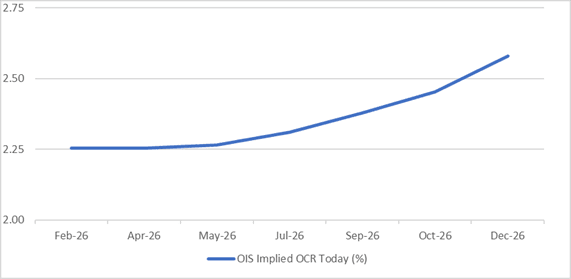

- MNI RBA Review-Feb 2026: Further Tightening Likely Needed: The RBA raised the cash rate to 3.85%, as expected by the sell-side consensus and which was largely priced by the market. The decision was unanimous by the board. The risks appear skewed towards further action to ensure that inflation moves sustainably back into the target band of 2-3%.

- RBA-dated OIS pricing is firmer again today across meetings, extending yesterday's post-RBA decision sell-off. That leaves RBA-dated OIS showing tightening across all meetings, with the probability of a 25bp hike rising from 17% for March to 105% by June and 172% by December 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6950(AUD1.96b). Upcoming Close Strikes : 0.6860(AUD1.51b Feb 9), 0.6875(AUD913m Feb 6), 0.6900(AUD1.64b Feb 9) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 84 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BONDS: NZGBS: Bear-Steepener On First Trading day Of Year

NZGBs closed showing a bear-steepener, with benchmark yields flat to 4bps higher, as trading resumed after the extended New Year’s break.

- The NZ-US 10-year yield differential closed at +35bps. For context, the differential was dealing around flat in mid-November.

- Cash US tsys are slightly richer in today's Asia-Pac session after Friday's modest bear-steepener. Focus in the first two full weeks of the year will be on nonfarm payrolls (Friday) and CPI reports (Jan 13) for December, with those two key reports back on their original schedules having been prioritized by the BLS. Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7. No scheduled Fed speakers today.

- The local data calendar is very light this week, with just Dec Cotality home value figures out later this evening. Next week we get Nov filled jobs, along with food prices as well.

- RBNZ-dated OIS pricing closed slightly softer across meetings. No tightening is priced for February, while October 2026 assigns 20bps.

Bloomberg Finance LP / MNI

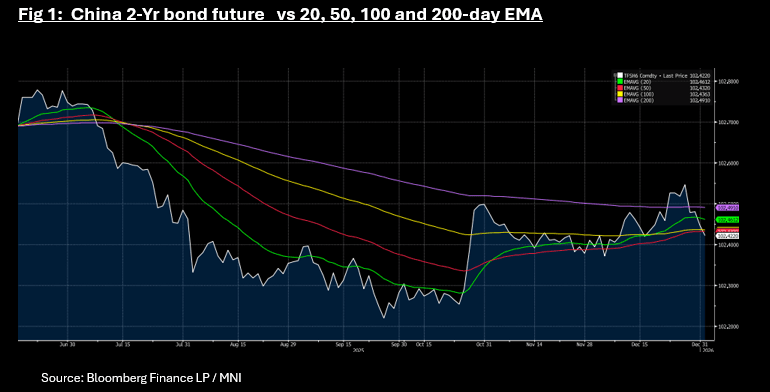

CHINA: 2-Yr Bond Future Dips Below Key Tech Levels

- China's bond futures are mixed today, following a sizeable withdrawal of liquidity during the OMO this morning.

- The 10-Yr is up +0.02 to 107.845, yet remains below all major moving averages. Upside resistance is via the 20-day EMA of 108.01.

- The 2-Yr is down -0.02 to 102.422, to dip below all major moving averages. If it is able to consolidate below, it is the first break below since early December. Each time it has broken below all moving averages in recent months, it has bounced back above within 1-2 trading days.

- Cash is quiet with the 2-Yr at 1.36% and the 10-Yr at 1.85%

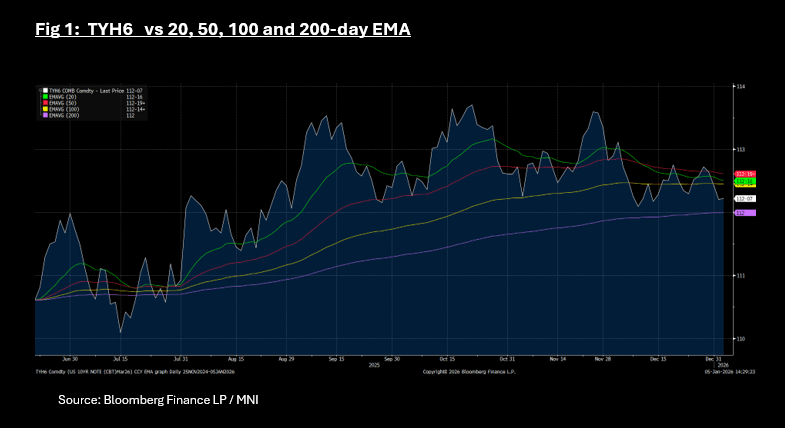

US TSYS: Cash Grinds Lower; TYH5 Wedged Between Key Tech Levels

US treasury futures have done nothing today with the 10-Yr up only marginally. At 112-07+ it remains wedged between the 100-day EMA as topside resistance and the downside resistance via the 200-day EMA of 112.

Cash is doing better with yields down -0.2bps to -0.9bps across the curve with the long end underperforming.

- The US 2-Yr is at 3.475% - flat today.

- The US 5-Yr is at 3.736%, down -0.9bps today.

- The US 10-yr is at 4.185%, down -0.6bps today.

- The US 30-Yr is at 4.869%, down -0.2bps.

Equity markets were key today but have seemingly brushed off the geopolitical risks, with strong rallies.

Whilst January is typically a busy month for issuance, Monday kicks off with just a US$86bn 13-week bill auction and a US$77bn 26-week bill auction.

Data wise ISM releases are the focus with the ISM Manufacturing forecast to remain in contraction and ISM Prices paid to remain elevated