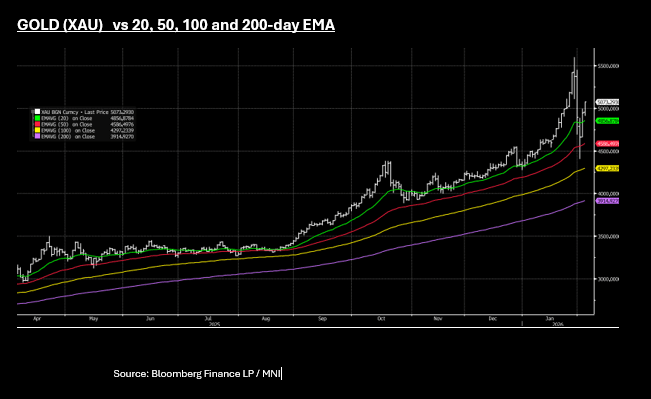

GOLD: $5,000 Poses No Challenge for Gold as Rally Resumes

- If gold's move overnight in the US looked like a technically driven relief rally, today's move looked increasingly like dip buyers taking charge.

- With the USD steady and risk sentiment strong, gold opened at US$4,952 and rallied from the outset, with the psychological level of $5,000 posing now resistance.

- Gold is currently up +2.45% at $5,068.37 and with momentum indicators remain fairly neutral and above all EMA's, the next key resistance is at $5,100.

- As a second retail focused gold trading platform in China signaled a funding shortfall following outflows last week, there may be an element of seasonality ahead of the Lunar New Year where demand from Chinese retail investors and households has provided a strong support historically,

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Venezuelan Oil Unlikely To Have Material Impact On Global Market

Venezuela is not a major player in the oil market despite having the largest known reserves, as years of sanctions and dictatorship have resulted in its crude production trending lower. The industry has been neglected and significant private investment will be needed to increase output as well as the lifting of sanctions. Low oil prices could discourage the needed capex. President Trump has said that the US needs full access to Venezuelan oil to rebuild the country.

- In the 1990s, Venezuela produced over 3mbd and OPEC reported that recently it was 1mbd which is above its 2020 trough. According to the IEA it was the 17th largest oil exporter globally and second in South America in 2023 as sanctions and a related-lack of investment in the sector drove output down 73% since 2000.

- Venezuela sells at a discount to benchmarks and most of its oil exports go to China.

- Even if it can return to producing 3mbd, Venezuela would still only be the 10th largest oil exporter and 15th largest producer, assuming other countries are unchanged.

OIL: Uncertainty Drives Minimal Change In Oil Prices

Oil prices fell around a percent on opening following the US’ removal of Venezuelan President Maduro, which in theory should allow for an easing of sanctions on its energy exports. Prices soon rebounded driven by significant uncertainty over Venezuela’s oil production capability, the situation in the country and stronger risk appetite in markets generally. At this stage markets don’t seem concerned that the action has set a destabilising precedent.

- WTI fell to $56.56/bbl on today’s open but soon began trending higher reaching $57.73. It is currently around $57.10 to be 0.4% down on the day. Brent declined to $60.00 before rising to $61.24 and is currently -0.2% at $60.61.

- With a record surplus widely projected for 2026, any extra Venezuelan supplies on global markets could add to current downward pressure on oil prices. OPEC’s decision on Sunday to stick with its plan of unchanged Q1 quotas should provide a short-term floor though.

- Venezuela’s oil producing region appears to have seen minimal impact from the weekend’s events. The US blockade had already caused a pause in production, which was not a major concern, as storage facilities filled.

- The industry needs significant investment after an extended period of neglect which will be a long process and so there is unlikely to be an increase in Venezuelan oil exacerbating the 2026 market surplus.

- Morgan Stanley expects global oil supply to peak in mid-2026 and so has cut its Brent forecasts for Q1, Q2 and Q3 with the trough at $55 in Q2, according to Bloomberg.

- Later US December manufacturing ISM and UK November lending data are released.

BONDS: NZGBS: Bear-Steepener On First Trading day Of Year

NZGBs closed showing a bear-steepener, with benchmark yields flat to 4bps higher, as trading resumed after the extended New Year’s break.

- The NZ-US 10-year yield differential closed at +35bps. For context, the differential was dealing around flat in mid-November.

- Cash US tsys are slightly richer in today's Asia-Pac session after Friday's modest bear-steepener. Focus in the first two full weeks of the year will be on nonfarm payrolls (Friday) and CPI reports (Jan 13) for December, with those two key reports back on their original schedules having been prioritized by the BLS. Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7. No scheduled Fed speakers today.

- The local data calendar is very light this week, with just Dec Cotality home value figures out later this evening. Next week we get Nov filled jobs, along with food prices as well.

- RBNZ-dated OIS pricing closed slightly softer across meetings. No tightening is priced for February, while October 2026 assigns 20bps.

Bloomberg Finance LP / MNI