US TSYS: Neutral Bias Remains, Despite Yields Near 1 Month Highs

The US 10-Yr future traded in a 111-17+ to 111-21+ range today, treading water for much of the day even as many major equity bourses weakened. The 10-Yr moved lower initially but stabilized at 111-19+, just below its opening level of 111-20

Front end cash was flat with longer dated USTs only modestly higher in yield, having on a weak tone but with some modest improvement as equities stalled.

- The 2-Yr up +0.2bps to 3.574%

- The 5-Yr is up +0.2bps to 3.837%

- The 10-Yr up +0.6bps to 4.274%

- The 30-Yr up +0.6bps to 4.902%

US equity futures are point pointing to a mixed start at this stage, and with Friday's NFP delayed, focus turns to the treasury refunding announcement, though not markets not expecting any surprises. There will be a US$17bn 17-week auction.

Investors remain sensitive to shifts in the "Fed regime" as the transition toward Warsh approaches. Bostic speaks Wednesday and markets will look for guidance on how the committee views the recent bounce in manufacturing activity .

ADP Employment change is key, with private sector employment is expected to show an increase of 45k for January, up from December's gain of 41,000.

This ISM Services Index is forecast to drop to 53.5 (from 54.4 in December). Markets will closely watch the Prices sub-index (forecast at 64.0) for signs of cooling inflationary pressure.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

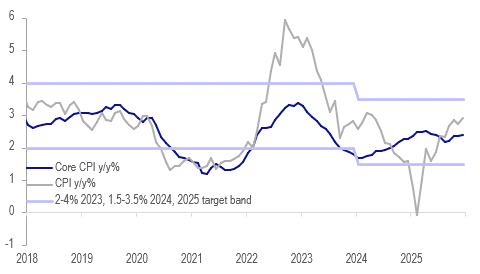

INDONESIA: Headline Up But Core Stable, IDR May Continue To Keep BI On Hold

Headline inflation rose more than expected in December printing at 2.9% y/y up from 2.7% but in line with the October outcome. There was a pickup in both fresh food and administered price inflation. Core was stable at 2.4% y/y for the third straight month and below 2025’s high of 2.5%. Both measures remain well with Bank Indonesia’s 1.5-3.5% corridor but with USDIDR higher than the last meeting and BI’s focus returning to FX stability, it could again be on hold at its next decision on 21 January.

- USDIDR strengthened to around 16700 on 31 December but is trending higher again and today is at 16755.

- Base effects from 2025’s energy discounts will drop out of the year-on-year comparison in Q1 and will temporarily boost headline inflation at the start of this year.

- Volatile food inflation rose to 6.2% y/y in December up from 5.5% due to chilis, chickens, shallots and fresh fish.

- Personal items rose 13.3% y/y up from 12.5% driven by jewellery as global gold prices rose 5.6% m/m on average in December to be up 63.4% y/y. Higher petrol prices boosted the transport component to 1.2% y/y from 0.7%.

Indonesia CPI y/y%

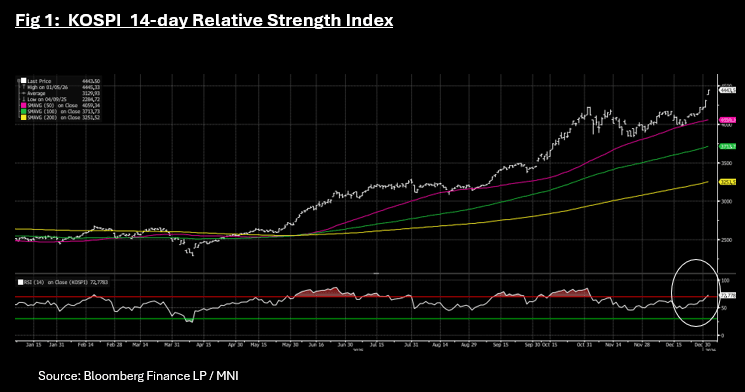

ASIA STOCKS: KOSPI Reaches Overbought as AI/Tech Rallies Again

The AI / tech rally continued today with key stocks like Samsung in Korea up +5.6%, TSMC in Taiwan +6.3% and Softbank in Tokyo +4% to help their respective bourses post strong gains. However the theme of China's key AI / tech stocks underperforming regional peers continues with Tencent in Hong Kong up just +0.15% today. Whilst the US ousting of Venezuela's president initially caused oil price volatility, Asian markets largely brushed off these tensions, maintaining their positivity throughout the day.

- The NIKKEI is gaining 3% today to 51,849 to be within 1% of the October high whilst the KOSPI jumped 3.10% to 4,442 and trend above the overbought line on the 14-day relative strength index. Joining in the AI / tech led party was the TAIEX which jumped +2.7% to a new high of 30,153 as it too reached overbought. There are growing calls from market observers as to the heated valuations from AI / tech stocks. SK Hynix in Korea for example is now up over 300% since its lows of April 2025.

- China's bourses were more subdued with the Hang Seng down -0.08% whilst the CSI 300 rose +1.5%, Shanghai +1.07% and Shenzhen +1.66%. For the Shanghai Comp, the rise above 4,000 to 4,011 brings the November high of 4,029 into its sights.

- SE Asia's major bourses all posted gains with the SE Thai outperforming following a much stronger than expected December PMI manufacturing. The SE Thai is up +1.7%, whilst the Jakarta Composite is up +0.65% and the FTSE Malay +0.34%

- India's NIFTY 50 continues to exhibit lower volatility relative to regional peers as it resets new highs. At 26,360 it remains up almost 20% from the March lows with gains of +0.15% Monday . The NIFTY 50 finished 2025 marginally below the 5-Year high of 23.50x, but is above the full year 2026 forecast. This suggests that from a valuation perspective, any near-term pressures on equities may not come from valuations though with the equity dividend yield at 1.26%, equity valuations relative to bonds look expensive.

FOREX: Early Risk Off Gives Way To Broader USD Gains, MXN Underperforms

USD gains have been fairly uniform against the G10 as Monday's Asia Pac session unfolded. Initial risk off drove AUD and NZD underperformance but this wasn't sustained. USD/JPY got to lows of 156.66, but now sits close to session highs, last 157.25/30, up around 0.30%. This keeps the recent uptrend intact, with upside focus likely to rest near the 158.00 (where we got to late last year post the Dec BoJ rate hike and where FX intervention rhetoric picked up from Japan officials).

- Despite the firmer US equity futures, and regional equity tone (albeit mainly focused in the tech/AI space), along with higher metal prices, the A$ has struggled to recovery ground. The pair was last around 0.6670/75. This is back close to the 20-day EMA support point, near 0.6660, which also coincides with recent lows. The 50-day EMA is further south near 0.6610.

- NZD/USD is off by a similar amount, last near 0.5750. This is close to recent lows in the pair around 0.5740, with a clean break lower potentially bringing 0.5700 back into focus.

- EUR/USD is softer as well, last 1.1680/85, levels last seen in the first half of Dec 2025. We are right around the 50-day EMA currently. GBP/USD is down 0.20% to 1.1325/30 right on the 20-day EMA support point.

- USD/MXN has risen close to 0.70%, up to 18.02/03. This keeps us close to highs from the second half of the Dec. Broader USD trends have aided the move, while remarks from US President Trump around needing to do something to curb drug flows from Mexico has likely weighed on sentiment as well. The weekend military action in Venezuela may leave the market not ruling out the possibility of US military action in Mexico to curb drug related activity.