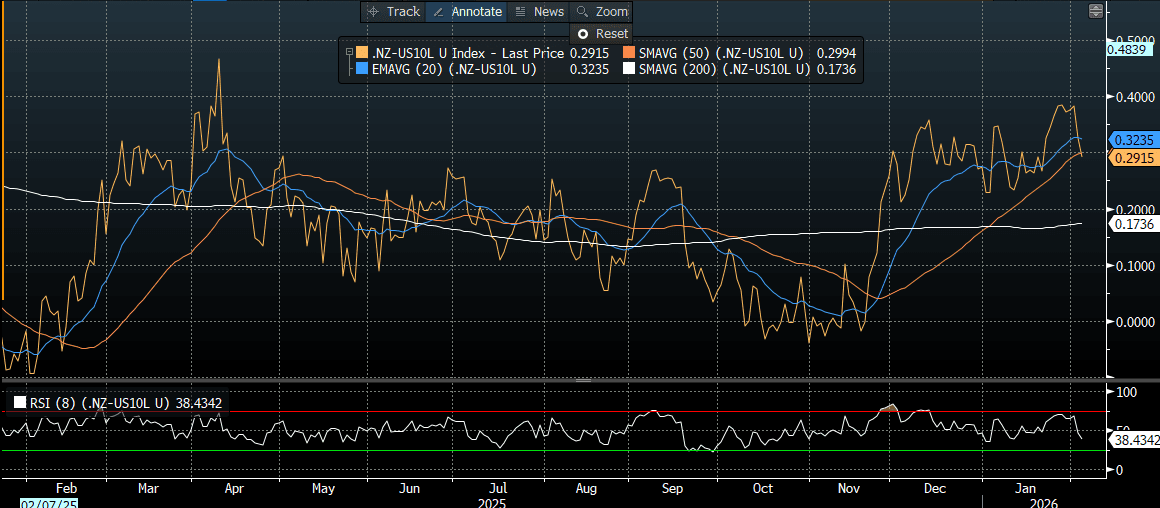

BONDS: NZGBS: Q4 Jobs Report Extends Rally

NZGBs closed 4-5bps richer after today’s Q4 Employment Report.

- NZ-US and NZ-AU 10-year differentials finished 3bps lower.

- The NZ Q4 jobs report was a mixed bag. On the positive side, the jobs growth picture was better than forecast, rising 0.5%q/q, versus 0.3% forecast and flat in Q3. This was the strongest q/q rise since Q2 2023. It also bought the y/y pace back to positive territory at 0.2% from a revised 0.7%y/y fall in Q3.

- The unemployment rate edged up to 5.4%, above both the market consensus and RBNZ forecast of 5.3%. The participation rate rose to 70.5%, versus 70.3% forecast. Arguably we would have needed to see a combination of stronger jobs growth and a lower unemployment rate to get the market more excited about a potentially earlier 2026 rate hike from the RBNZ.

- Swap rates closed 5-7bps lower, with a steeper 2s10s curve.

- RBNZ-dated OIS pricing closed softer for late 2026 meetings. No tightening is priced for February, while December 2026 assigns 46bps, 5bps softer than yesterday’s close.

- Tomorrow, the local calendar will see Cotality Home Value data.

- The NZ Treasury also plans to sell NZ$225mn of the 4.50% May-30 bond, NZ$175mn of the 4.25% May-34 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

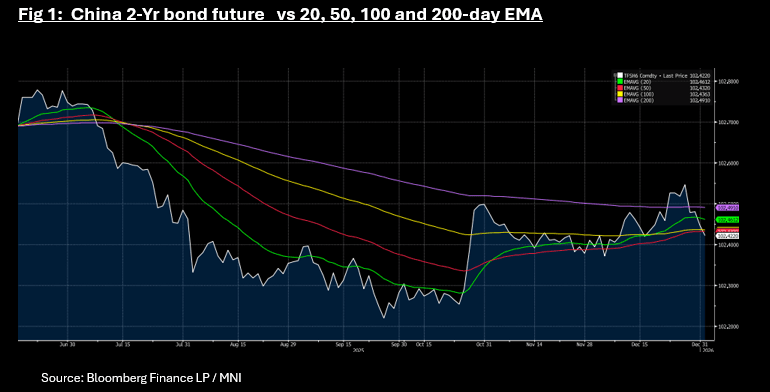

CHINA: 2-Yr Bond Future Dips Below Key Tech Levels

- China's bond futures are mixed today, following a sizeable withdrawal of liquidity during the OMO this morning.

- The 10-Yr is up +0.02 to 107.845, yet remains below all major moving averages. Upside resistance is via the 20-day EMA of 108.01.

- The 2-Yr is down -0.02 to 102.422, to dip below all major moving averages. If it is able to consolidate below, it is the first break below since early December. Each time it has broken below all moving averages in recent months, it has bounced back above within 1-2 trading days.

- Cash is quiet with the 2-Yr at 1.36% and the 10-Yr at 1.85%

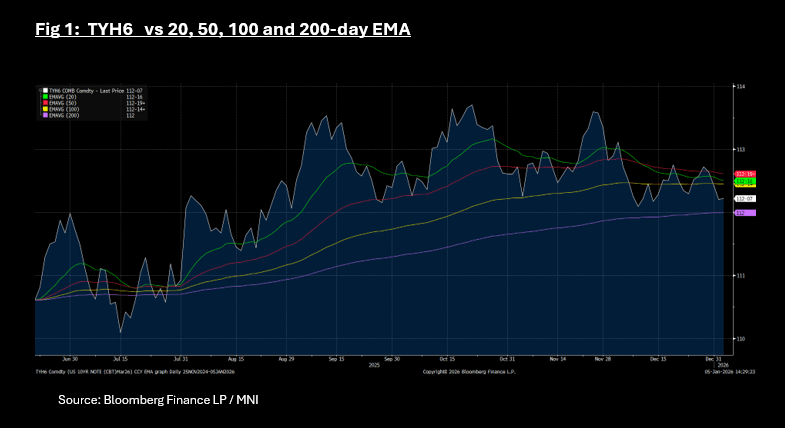

US TSYS: Cash Grinds Lower; TYH5 Wedged Between Key Tech Levels

US treasury futures have done nothing today with the 10-Yr up only marginally. At 112-07+ it remains wedged between the 100-day EMA as topside resistance and the downside resistance via the 200-day EMA of 112.

Cash is doing better with yields down -0.2bps to -0.9bps across the curve with the long end underperforming.

- The US 2-Yr is at 3.475% - flat today.

- The US 5-Yr is at 3.736%, down -0.9bps today.

- The US 10-yr is at 4.185%, down -0.6bps today.

- The US 30-Yr is at 4.869%, down -0.2bps.

Equity markets were key today but have seemingly brushed off the geopolitical risks, with strong rallies.

Whilst January is typically a busy month for issuance, Monday kicks off with just a US$86bn 13-week bill auction and a US$77bn 26-week bill auction.

Data wise ISM releases are the focus with the ISM Manufacturing forecast to remain in contraction and ISM Prices paid to remain elevated

JGBS: At Session Cheaps At Lunch

At the Tokyo lunch break, after the extended NY break, JGB futures are weaker and at a fresh cycle low, -41 compared to settlement levels (see chart).

- Cash US tsys are slightly richer in today's Asia-Pac session after Friday's modest bear-steepener. Focus in the first two full weeks of the year will be on nonfarm payrolls (Friday) and CPI reports (Jan 13) for December, with those two key reports back on their original schedules having been prioritized by the BLS. Private sector reports meanwhile are highlighted by ISM manufacturing and services reports Jan 5 and 7. No scheduled Fed speakers today.

- Cash JGBs are 1-6bps cheaper across benchmarks, led by the futures-linked 7-year. The benchmark 10-year yield is 5.4bps higher at 2.12%, a fresh cycle high.

- (Bloomberg) " Long-term JGB yields may continue to face upward pressure due to concerns about the Bank of Japan's efforts to rein in inflation and the government's "reflationary" policy intentions.”

- Swap rates are 2-5bps higher, with a steepener curve.

Source: Bloomberg Finance LP