MNI EUROPEAN OPEN: JPY & Yields Can't Rally With Tokyo CPI

EXECUTIVE SUMMARY

- TRUMP CALLS ON REPUBLICANS TO USE ‘NUCLEAR OPTION’ AND GET RID OF SENATE FILIBUSTER - THE HILL

- ECB HOLDS AGAIN AMID NARROWING RISKS - MNI ECB WATCH

- JAPAN OCT TOKYO CORE CPI RISES 2.8% VS. SEPT 2.5% - MNI BRIEF

- CHINA OCT MANUFACTURING PMI HIT SIX-MONTH LOW - MNI BRIEF

- RBNZ’S GAI SAYS GLOBAL SHOCKS HAVE OFFSET SOME POLICY EASING - BBG

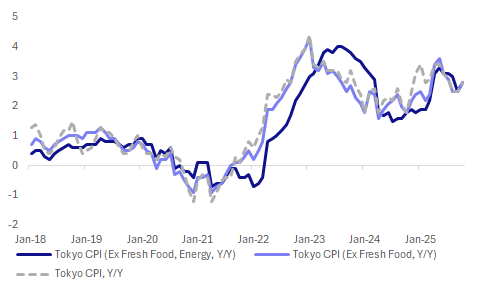

Fig 1: Tokyo CPI Y/Y Rebounds In Oct

Source: Bloomberg Finance L.P./MNI

UK

POLITICS (BBG): "UK Chancellor of the Exchequer Rachel Reeves’ estate agent apologized and took responsibility after it emerged she’d rented out her family home without a license, as Prime Minister Keir Starmer backed her to stay in her post following the furor."

EU

ECB (MNI ECB WATCH): The European Central Bank as expected held the deposit rate at 2% for a third consecutive meeting on Thursday, with President Christine Lagarde saying some risks to growth have abated and pointing to progress in trade talks involving the EU and China, the U.S. and China, and a peace-fire in Gaza.

GERMANY (BBG): "Germany is considering using public funds to pay Deutsche Telekom AG and other telecom operators to replace Huawei Technologies Co. equipment, people familiar with the matter said."

SWITZERLAND (BBG): "The Swiss National Bank won’t shy away from stepping into currency markets if required, while interest rates are the key tool, according one its top officials."

US

GOVERNMENT (THE HILL): “President Trump on Thursday called on Senate Republicans to initiate the “nuclear option” and get rid of the filibuster, which would allow them to end the government shutdown and pass legislation with a simple majority.”

US/CHINA (BBG): " The US will proceed with an investigation that opens the door to new tariffs on goods from China, despite the two nations’ fresh truce, President Donald Trump’s top trade negotiator said."

TECH (BBG): "Amazon.com Inc.’s cloud unit posted the strongest growth rate in almost three years, reassuring investors who were concerned that the largest seller of rented computing power was losing ground to rivals."

TECH (BBG): "Apple Inc. predicted a major sales surge during the holiday season after releasing new iPhones, helping assure investors that its flagship product remains a growth engine. "

OTHER

JAPAN (MNI BRIEF): The year-on-year rise in Tokyo’s core consumer price index accelerated to 2.8% in October from 2.5% in September, marking the 12th consecutive month above the Bank of Japan’s 2% target, data from the Ministry of Internal Affairs and Communications showed Friday.

JAPAN (MNI BRIEF): Japan’s industrial production rose 2.2% m/m in September, the first increase in three months following August’s 1.5% decline, led by higher output of production machinery, though automobile production growth slowed, data from the Ministry of Economy, Trade and Industry showed Friday.

NEW ZEALAND (BBG): “ Reserve Bank of New Zealand Monetary Policy Committee external member Prasanna Gai speaks on a policy panel Friday in Melbourne, according to speaking notes published on RBNZ website. “For a small open economy like New Zealand, the US tariffs have acted as negative demand shock”

CHINA

MANUFACTURING (MNI BRIEF): “China's Manufacturing Purchasing Managers Index fell by 0.8 points to 49.0 in October from September, hitting a six-month low and staying below the breakeven 50 mark for the seventh month, data from the National Bureau of Statistics showed Friday.”

CONSTRUCTION (MNI BRIEF): China’s construction business activity index, a key sub-index of the non-manufacturing Purchasing Managers’ Index (PMI), fell to 49.1% in October, down 0.2 percentage points from September, the National Bureau of Statistics (NBS) said Friday.

CONSUMPTION (YICAI): "Authorities will expand the product categories offered by duty-free shops to mobile phones, micro drones, sporting goods, health supplements, over-the-counter drugs, and pet food, to boost consumption, according to a document released by the Ministry of Finance and four other departments, Yicai.com reported."

MNI: PBOC Net Injects CNY187.1 Bln via OMO Friday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY355.1 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY187.1 billion after offsetting maturities of CNY168 billion today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) fell to 1.4260% at 09:58 am local time from the close of 1.5018% on Thursday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 48 on Thursday, the same as the close on Wednesday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Higher At 7.0880 Fri; +0.70% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate higher at 7.0880 on Friday, compared with 7.0864 set on Thursday. The fixing was estimated at 7.1190 by Bloomberg survey today.

MARKET DATA

NEW ZEALAND OCT ANZ CONSUMER CONFIDENC 92.4; PRIOR 94.6

AUSTRALIA Q3 PPI Y/Y 3.5%; PRIOR 3.4%

AUSTRALIA SEP PRIVATE CREDIT Y/Y 7.3%; PRIOR 7.3%

JAPAN SEP JOBLESS RATE 2.6%; MEDIAN 2.5%; PRIOR 2.6%

JAPAN SEP JOB-TO-APPLICANT RATIO 1.2; MEDIAN 1.2; PRIOR 1.2

JAPAN OCT TOKYO CPI Y/Y 2.8%; MEDIAN 2.4%; PRIOR 2.5%

JAPAN OCT TOKYO CPI, EX FRESH FOOD Y/Y 2.8%; MEDIAN 2.6%; PRIOR 2.5%

JAPAN OCT TOKYO CPI, EX FRESH FOOD, ENERGY Y/Y 2.8%; MEDIAN 2.6%; PRIOR 2.5%

JAPAN SEP RETAIL SALES Y/Y0.5%; MEDIAN 0.7%; PRIOR -0.9%

JAPAN SEP INDUSTRIAL PRODUCTION Y/Y 3.4%; MEDIAN 1.8%; PRIOR -1.6%

JAPAN SEP HOUSING STARTS Y/Y -7.3%; MEDIAN -7.8%; PRIOR -9.8%

CHINA OCT MANUFACTURING PMI 49.0; MEDIAN 49.6; PRIOR 49.8

CHINA OCT NON-MANUFACTURING PMI 50.1; MEDIAN 50.1: PRIOR 50.0

CHINA OCT COMPOSITE PMI 50.0; PRIOR 50.6

MARKETS

US TSYS: Futures Caught in Technical Range, 10-Yr Back Above 4.10%

Month end flows were not evident in Asia today with futures doing very little. TYZ5 barely troubled the scorers down just -01 at 112-21+. TYZ5 is currently at the mid-point below the 50-day EMA of 112-26+ and the 100-day EMA of 112-11+.

Cash was quiet also with many maturities failing to hold earlier gains, remaining unchanged Friday.

- The US 2-Yr is at 3.61 (-0.2bps today)

- The US 5-Yr is unchanged at 3.72%

- The US 10-Yr has edged back below the 4.10% earlier but is back to unchanged on the day at 4.101%

- The US 30-Yr is up is unchanged at 4.657%.

With PCE not set to be released tonight due to the government shutdown, focus is on MNI Chicago PMI (40.6 prior, 42.0 estimate) and speeches from Cleveland Fed Hammack & Atlanta Fed Bostic.

Auction wise focus tonight is US$110bn 4-week bills and US$95bn 8-week bills.

JGBS: 2yr JGB Yield Weaker Post Solid Auction, Futures Supported Post Tokyo CPI Dip

JGB futures are up from earlier lows, last 136.13, -.08 versus settlement levels. There was an early dip, aided by the firmer Tokyo CPI print, but there was no follow through. Recent ranges still hold for JGB futures. In the cash JGB space, yield losses have been move evident at the front end, aided by a solid 2yr debt auction (bid to cover of 4.35 versus 2.814 prior). The 2yr yield is down close to 2bps to 0.915%. The broader uptrend in the yield since April of this year remains intact (the 2/30s curve is a touch steeper at +213bps). The 10yr JGB is steady at 1.65%.

- The Tokyo CPI print showed strong m/m momentum across most key categories and a pick up in the y/y to 2.8%. Still, the central bank is likely to want to see further m/m gains before shifting its broader inflation expectations (i.e. its confidence in achieving its inflation target).

- Wages is also the other key focus point, with earlier data some softening in the labour market via a higher unemployment rate, but we remain with recent ranges. IP growth was stronger than forecast but a government official noted that there remains caution around the outlook.

- Looking ahead to next week, the main focus will be on the Sep labour cash earnings data, out on Thursday. This data was softer in recent months and remains a key watch point for the BOJ.

- Market pricing for the Dec meeting, per OIS, is around a 0.59% implied rate, little changed since the end of last week. A full 25bps hike is close to fully priced for the March meeting (using an effective rate of 0.476%).

- The FinMin maintained FX jawboning, but FX intervention risks don't look imminent (based off past language used by officials relative to today's comments).

- In the debt auction space, we have the 10yr, next Wednesday as the next major focus point.

AUSSIE BONDS: 3yr Yield Near Cash Rate, +25bps Firmer This Week, RBA Next Tues

Aussie bond futures have traded a tight range so far today, the 3yr (YM) at 96.37 currently and 10yr (XM) 95.675. These levels are largely holding losses seen this week, as the Q3 CPI beat saw easing risks for this year significantly curtailed. The 3yr ACGB yield is up close to 25bps so far this week, the biggest weekly rise since 2024. We were last near 3.61% so around the RBA cash rate, while the 10yr is a little higher above 4.30%.

- Focus going forward will be around easing risks into 2026. Our policy team interviewed a senior ex RBA Economist this week who stated: "Stronger-than-expected Q3 inflation data has almost eliminated any chance of further easing by the Reserve Bank of Australia this year and could even force rate hikes in H1 2026 if Q4 and Q1 CPI results come in hot, a former RBA senior economist told MNI."

- Market pricing for the Nov meeting is close to flat, while only 5bps of easing risk is priced for Dec. A full cut next year is priced by around the August meeting, although for May we have 23bps of easing priced in.

- The AU-US 10yr spread is around +21bps, little changed, but the moved higher has slowed since the hawkish Fed cut earlier this week.

- The AU 3/10s curve is slightly steeper at +70bps, but holding the bulk of this week's down move from +77bps.

- On the data front today we just had Q3 PPI, which rose to 3.5%y/y, from 3.4%, while the Sep credit figures were +0.6%m/m, in line with market forecasts.

- Next week, we have the RBA meeting outcome on Tuesday with no change expected, but focus will be on the updated forecast projections and how that shapes the outlook into 2026.

BONDS: NZGBS: A False Break Higher For Yields? Next Week Q3 Jobs Data

NZGB yields are finishing the weak on a softer note, down around 2-4bps across the curve, with the back end leading. The 2yr and the 10yr benchmarks are back under 20-day EMA resistance points, which were tested earlier this week. In yield terms, this is underperforming the US and Australian market trends. The NZ-US spread is back close to -4bps, near recent lows. Obviously catalysts today haven't that apparent for the yield losses seen. Still, we did have a softer ANZ NZ consumer sentiment print earlier, while RBNZ Monetary Policy Committee (MPC) external member Prasanna Gai noted the negative demand impact of tariffs, which has offset some the easing the central bank has done.

- The 2yr swap rate is also drifting lower, last down close to 2bps and near 2.38% (which is also back under the 20-day EMA resistance area).

- The implication from this is potentially more work for the RBNZ to do (this is our bias, not Gai's). We already have close to 25bps priced for the Nov meeting. Terminal rate pricing is around 2.14/15% for mid 2026, little changed.

- The consumer sentiment reading suggested that the recovery backdrop still remains challenging.

- Note next week we get the Q3 jobs report on Wednesday.

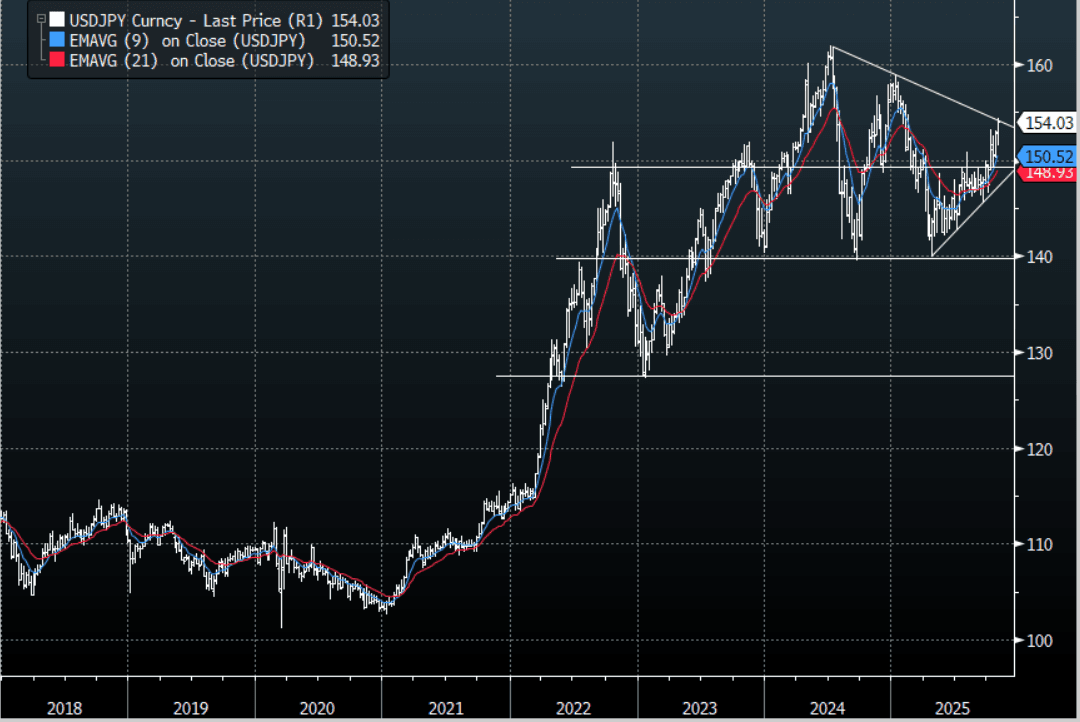

JPY: Asia-Pac: USD/JPY Tries Lower On CPI And MOF Jaw-Boning

The USD/JPY range has been 153.65 - 154.17 in the Asia-Pac session, it is currently trading around 154.00, -0.10%. The pair fell away thanks to a combination of a strong CPI print and some jaw-boning from the MOF. The pair remains a buy on dips though thanks to a combination of a hawkish FED and a BOJ that is still unsure about when it will raise rates. We are approaching some tough resistance back toward the 154/155 area and I would expect we might to do some work around here initially before moving higher. A break back above 155 could potentially see the move begin to accelerate and with that the potential for further intervention, though personally I think they will wait for levels closer to 160 to get involved.

- MNI BRIEF: Japan Oct Tokyo Core CPI Rises 2.8% Vs. Sept 2.5%. The year-on-year rise in Tokyo’s core consumer price index accelerated to 2.8% in October from 2.5% in September. The BOJ expects underlying CPI inflation to remain subdued temporarily as economic momentum weakens, before moving toward the 2% target. Officials are watching closely whether food prices excluding fresh items (+6.7% vs +6.9%) continue to moderate as projected.

- "JAPAN FINMIN KATAYAMA: CLOSELY WATCHING FX MOVES WITH A HIGH SENSE OF URGENCY RECENTLY SEEING ONE-SIDED, RAPID MOVES, IMPORTANT FOR CURRENCIES TO MOVE IN STABLE MANNER REFLECTING FUNDAMENTALS" RTRS"

- “KATAYAMA: CURRENCY MOVED PARTLY DUE TO MARKET VIEW ON BOJ, FED. BOJ'S DECISION WAS VERY REASONABLE" - BBG

- Bloomberg is reporting that Hedge funds are betting the yen will weaken to as low as 160 per dollar by the end of the year.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.50($1.42b). Upcoming Close Strikes : 150.00($1.13b Nov 3) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

FOREX: Asia-Pac FX: The USD Consolidates Overnight Gains, BBDXY Eyes 1220-1230

The BBDXY has had a range of 1217.20 - 1218.39 in the Asia-Pac session; it is currently trading around 1218, -0.05%. The USD accelerated higher overnight helped by the move in US yields which had a significant bounce. The 1220-30 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the USD shorts. The price action though is starting to look more constructive as higher lows are being made on the Daily chart through October. A move back above 1230 would potentially signal a medium term low is in place and deeper pullback is on the cards. We do have month-end tonight so there could be some further portfolio adjustments to get through.

- EUR/USD - Asian range 1.1565 - 1.1577, Asia is currently trading 1.1570. The pair has moved back toward its support just above 1.1500. A break under this support could signal a deeper correction.

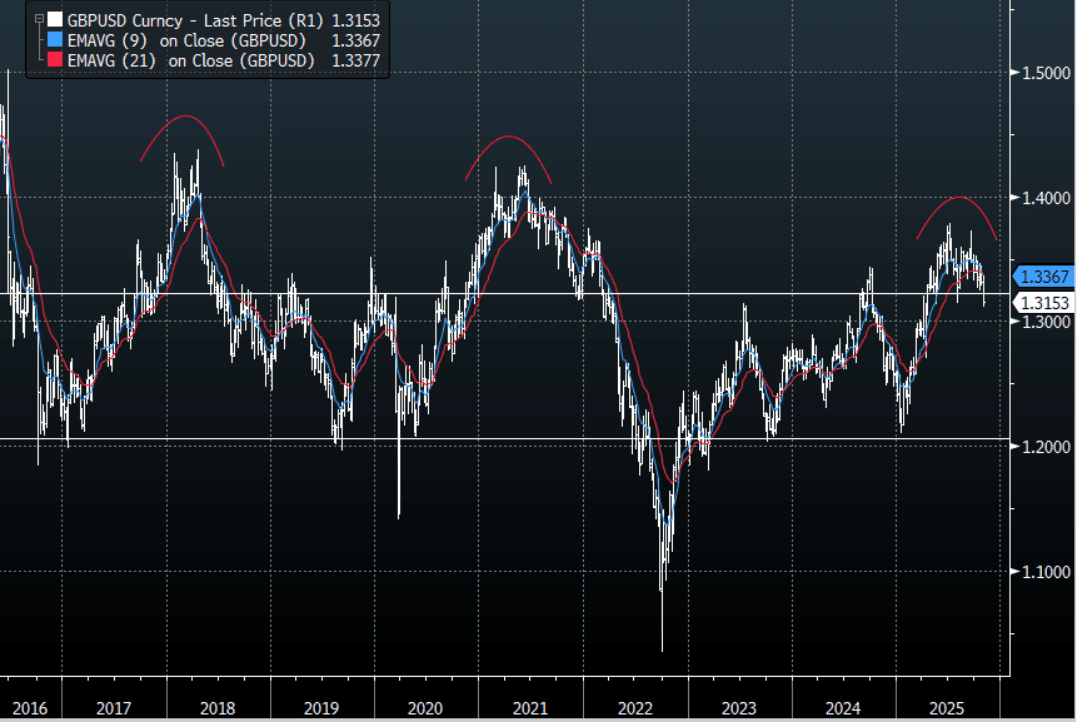

- GBP/USD - Asian range 1.3150 - 1.3165, Asia is currently dealing around 1.3155. The pair looks to be building some downward momentum. This 1.3150 area has proved to be supportive on more than 1 occasion this year so some work around this level could be expected. I continue to favor fading rallies though as GBP attempts to put in a medium term top.

- USD/CNH - Asian range 7.1082 - 7.1130, the USD/CNY fix printed at 7.0880, Asia is currently dealing around 7.1100. The support below 7.1000 looks to be pretty solid for now as USD/Asia moves in sympathy with a higher USD/JPY. The range of 7.08-7.16 looks set to continue for now.

- Cross asset : SPX +0.65%, Gold $3990, US 10-Year 4.0970%, BBDXY 1218, Crude Oil $60.14

- Data/Events : Italy CPI, Germany Retail Sales, EZ ECB Survey of Professional Forecasters/CPI, France Bloomberg Oct. France CPI, Spain Bloomberg Oct. Spain Current Account Balance

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia-Pac: AUD/USD Quiet Session, Ignores Bounce In US Stocks

The AUD/USD has had a range of 0.6547 - 0.6560 in the Asia- Pac session, it is currently trading around 0.6550, -0.10%. The AUD is consolidating around 0.6550, having shrugged off the bounce in US stocks. The AUD failed to extend above the 0.6600 area and has slipped lower as the USD continues its attempt to build a base from which to move higher. The AUD/USD is back within its recent 0.6400-0.6600 range with the pivot being around its current level around 0.6550.

- "AUSTRALIA 3Q PRODUCER PRICES RISE 1.0% Q/Q, AUSTRALIA 3Q PRODUCER PRICES RISE 3.5% Y/Y” - BBG (note there is no forecast for PPI, the Q2 rise was 0.7%q/q)

- “AUSTRALIA SEPT. PRIVATE CREDIT RISES 0.6% M/M; EST. +0.6%, AUSTRALIA SEPT. PRIVATE CREDIT RISES 7.3% Y/Y" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD 888m). Upcoming Close Strikes : 0.6625(AUD944m Nov 4), 0.6300(AUD600m Nov 4) - BBG

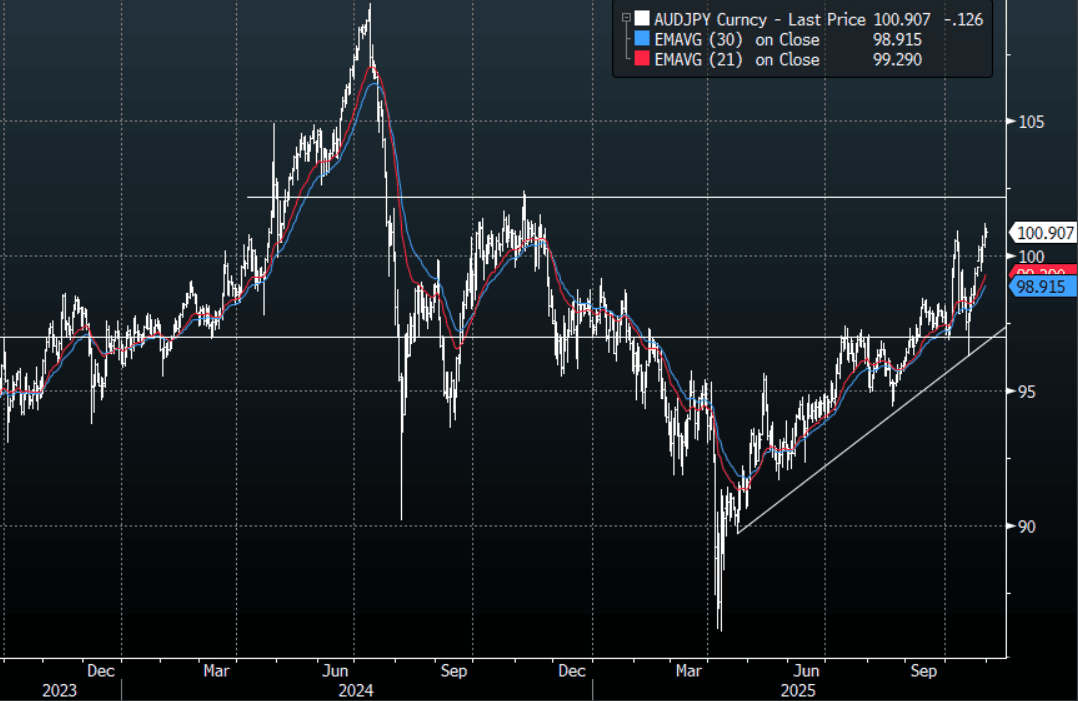

- AUD/JPY - Asia-Pac range 100.67 - 101.03, Asia is trading around 100.80. The pair is consolidating around 101.00 at the moment as it looks to build on its recent move back above 100.00. Suspect dips will continue to be supported for now with the first target 102.50 and then beyond.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

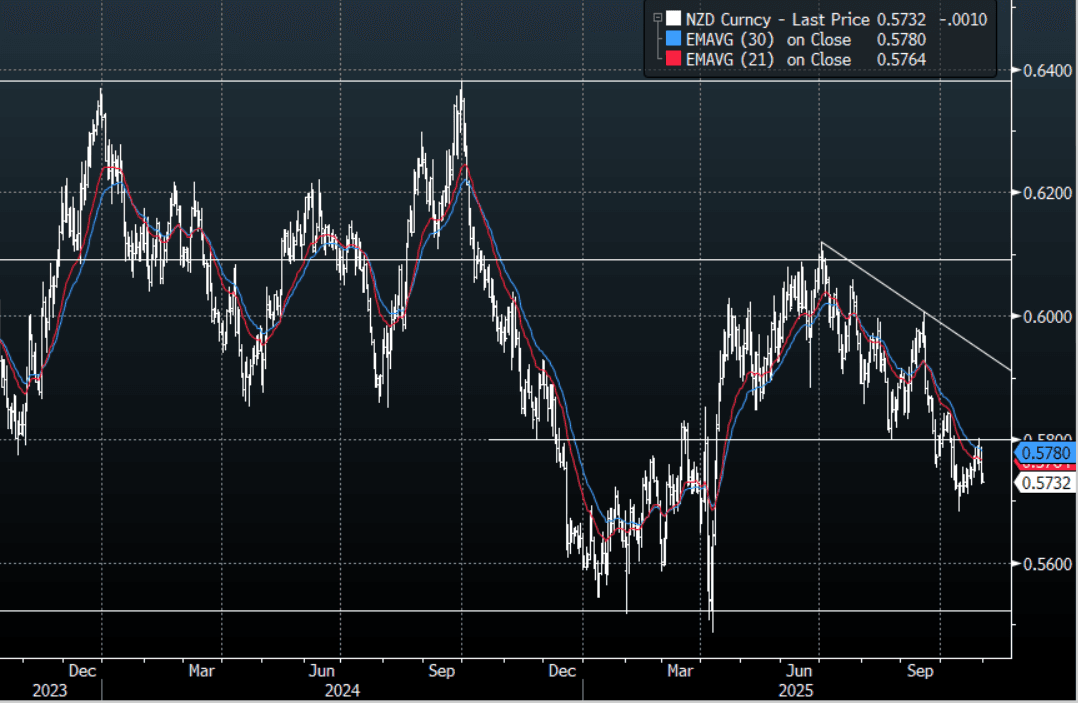

NZD: Asia-Pac: NZD/USD Moves Back To Overnight Lows On Gai Comments

The NZD/USD had a range of 0.5728 - 0.5745 in the Asia-Pac session, going into the London open trading around 0.5730, -0.20%. RBNZ committee member Prassanna Gai made some comments that saw the NZD move back to its overnight lows in our session. The NZD has run into solid resistance towards the 0.5800 area, this is the kind of price action the shorts would appreciate. While price remains below the 0.5800/50 area I suspect rallies will continue to be faded looking for a potential move back towards the 0.5500/0.5600 area. NZD continues to stand out as a short against a resurgent USD but it is worth noting that because of the size of the market traders can very quickly become all positioned the same way, so I think the USD will need to build on its challenge higher for the NZD to test those lows.

- Bloomberg reported on the comments made by Prassana Gai in her speech today: RBNZ’s Gai Says Global Shocks Have Offset Some Policy Easing. “For a small open economy like New Zealand, the US tariffs have acted as a negative demand shock. Compounding this has been a much broader uncertainty shock as the weaponization of trade and finance have profoundly changed widely accepted norms and international rules of the game. Together, these shocks appear to have offset some of the monetary easing that has taken place since August 2024.”

- "New Zealand Job Ads See First Annual Gain in 3 Years: Ministry, Job ads index rises 3.5% y/y" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD1.05b Nov 4), 0.5675(NZD1b Nov 5), 0.5750(NZD604m Nov 5) - BBG

- AUD/NZD range for the session has been 1.1409 - 1.1434, currently trading around 1.1430. The Cross has bounced hard after finding solid demand back toward 1.1300. This 1.1400/1.1500 remains tough resistance but the price action suggests it might be tested. Above 1.15/16 and the markets focus will start to turn toward 1.2000 and beyond.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

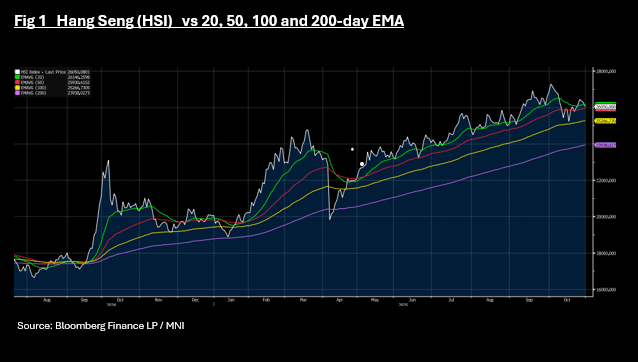

ASIA STOCKS: KOSPI + NIKKEI Lead Whilst China's Bourses Stumble into Month End

Weaker than expected Official PMIs may have been the catalyst for significant falls in the HSI today, dragging China's major bourses with it. Opening the trading day with modest gains, the falls in Hong Kong began just after the release that showed that state owned enterprises remain in contraction. Elsewhere the post Trump / XI meeting response continues to be broadly positive with the NIKKEI and the KOSPI continuing to lead the gainers in the region. Despite solid Apple Inc results at the start of the Asia trading day, tech stocks weren't the key driver for China, whilst in Korea and Taiwan, Samsung and TSMC reached yet new highs.

- The NIIKKEI's good run continued today with gains of +1.6% and weekly gains of +5.8%. The NIKKEI is at new highs of 52,206, up over 66% from the 2025 lows in April.

- The KOSPI is up +0.52% today and +4.2% for the week. Since the depths of trade war worries in April, the KOSPI has now risen over 78% year to date.

- The HSI in Hong Kong fell by -0.88% today and is barely holding on to a weekly gain. The CSI 300 is down by over 1% and back to flat on the week whilst the Shanghai and Shenzhen bourses are down, whilst retaining their slightly positive gains for the week. For the month of October, the divergence in onshore offshore is evident with the Hang Seng down -3.00% whilst the CSI 300 is up +0.45% and Shanghai +2%. The HSI has broken below the 20-day EMA again and is at 26,050 with the 50-day EMA below at 25,930.

- In Malaysia, the market awaits the decision from the Central Bank next week and continued it's lackluster period remaining where it started the week.

- In Jakarta, volatility returned after a period of strength and with further falls again the JCI is on track for a weekly loss of over 1%.

- The FTSE Straits Times in Singapore is flat on the week, whilst the PSEi in the Philippines is down over 2%, despite much stronger than expected export numbers for September being released.

India's NIFTY 50 hit new highs Wednesday of 26,053 but fell yesterday into the close on profit taking. Opening up +0.20% Friday sees week to date gains of 0.50%

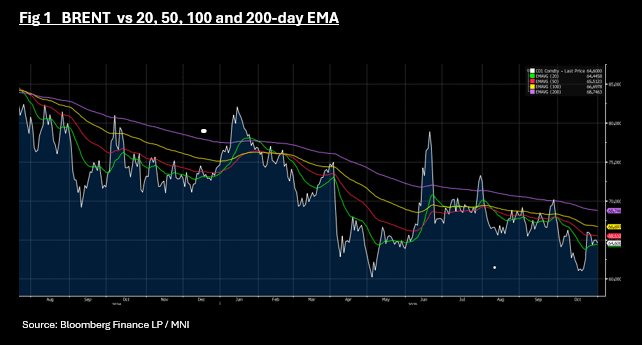

Oil in Weekly Decline as Brent Challenges Key Technical

- If current trends remain, oil will register it's fourth week in October of declines, locking in over -2% this week.

- WTI has weakened further Friday paring back the modest gains of Wednesday and Thursday, to be down -0.70% in the Asia trading day.

- Mid week gains had pushed WTI above the 20-day EMA of US$60.36 bbl, which it has given back today as it falls back to US$60.14.

- Brent is lower by -0.62% today at US$64.60 bbl, and down just over 2% for the week. Brent has fallen back near to the 20-day EMA of $64.44 and further falls tonight could see it consolidate below with near term lows of US$61.10 below.

- With no new news on further Russian sanctions or discussions with India on their Russian purchases although earlier in the week India Oil Corp stated clearly of their intent to stop buying oil under the sanctions. Other refiners have followed suit pausing all purchases.

- Similarly the mid week change in tact from the FED weighed heavy on oil just as the International Energy Agency has warned that the surplus in 2026 will be a record, though Saudi Aramco has struck a more positive tone. Oversupply in 2026 is a "highly credible scenario," Shell Plc CEO Wael Sawan said in an earnings call Thursday. (per BBG)

- The CEO of Europe's largest refiner TotalEnergies said overnight that " am more bullish than what we wrote a few days ago because I begin to realize that these sanctions will have a real impact in this market and that markets are underestimate what that mean."

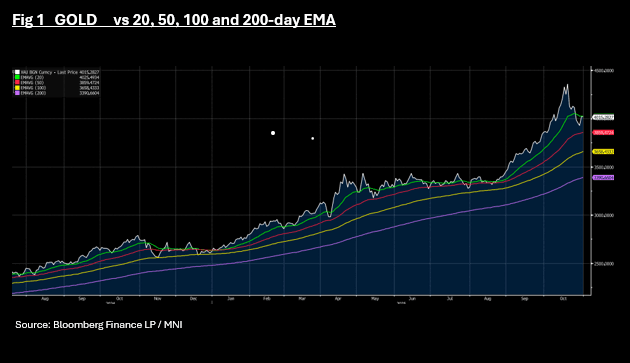

Gold Fails to Break 20-day EMA, Moves Lower

- After four days of strong losses, gold rebounded overnight to finish higher in the US trading session by +2.40%. Starting the Asia trading day near to the 20-day EMA of US$4,025.33, gold opened strongly from $4,024. However it was unable to break above the 20-day EMA, giving back early gains to lower at $4,014.78.

- For the week, gold remains lower by -2.3%, with successive weeks of losses to finish October.

- Overnight a report from the World Gold Council showed that Central Bank buying continues to underpin gold's rally with the July to September period seeing 220 tons of gold purchased by them, an increase of 28%.

- In China commercial bank's have been forced to raise their minimum purchase amount of gold from CNY900 to CNY1,100 as accumulation plans by investors are up 20% according to Ping An (source BBG).

- Moves in gold in the coming weeks will be watched eagerly, assuming trade tensions ease. Investors will watch closely to assess whether the more than 50% rise in gold was due to the 'safe haven bid' or the material change in markets, driven by Central Bank investment behaviour.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 31/10/2025 | 0700/0800 | ** | Import/Export Prices | |

| 31/10/2025 | 0700/0800 | ** | Retail Sales | |

| 31/10/2025 | 0730/0830 | ** | Retail Sales | |

| 31/10/2025 | 0745/0845 | *** | HICP (p) | |

| 31/10/2025 | 0745/0845 | ** | PPI | |

| 31/10/2025 | 0930/0930 | Blue Book / Pink Book | ||

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1000/1100 | *** | Italy Flash Inflation | |

| 31/10/2025 | 1000/1100 | *** | EZ HICP Flash | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 31/10/2025 | 1230/0830 | *** | Employment Cost Index | |

| 31/10/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 31/10/2025 | 1330/0930 | Dallas Fed's Lorie Logan | ||

| 31/10/2025 | 1342/0942 | *** | MNI Chicago PMI | |

| 31/10/2025 | 1500/1100 | Finance Dept monthly Fiscal Monitor (expected) | ||

| 31/10/2025 | 1600/1200 | Fed's Beth Hammack, Raphael Bostic | ||

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 31/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |