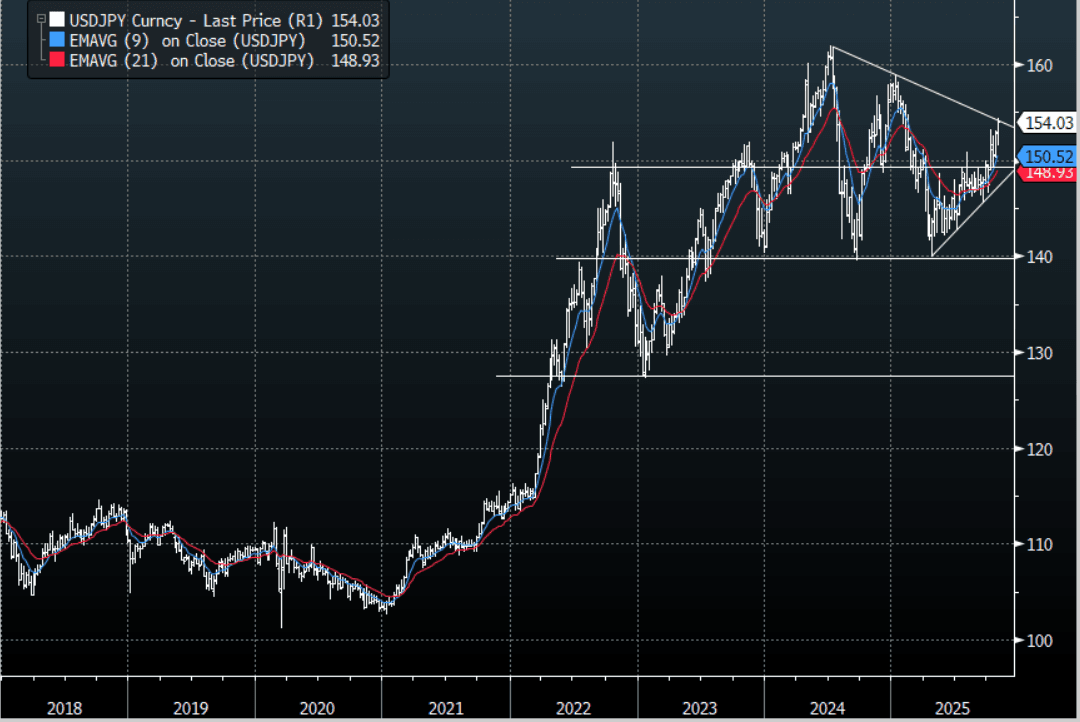

JPY: Asia-Pac: USD/JPY Tries Lower On CPI And MOF Jaw-Boning

The USD/JPY range has been 153.65 - 154.17 in the Asia-Pac session, it is currently trading around 154.00, -0.10%. The pair fell away thanks to a combination of a strong CPI print and some jaw-boning from the MOF. The pair remains a buy on dips though thanks to a combination of a hawkish FED and a BOJ that is still unsure about when it will raise rates. We are approaching some tough resistance back toward the 154/155 area and I would expect we might to do some work around here initially before moving higher. A break back above 155 could potentially see the move begin to accelerate and with that the potential for further intervention, though personally I think they will wait for levels closer to 160 to get involved.

- MNI BRIEF: Japan Oct Tokyo Core CPI Rises 2.8% Vs. Sept 2.5%. The year-on-year rise in Tokyo’s core consumer price index accelerated to 2.8% in October from 2.5% in September. The BOJ expects underlying CPI inflation to remain subdued temporarily as economic momentum weakens, before moving toward the 2% target. Officials are watching closely whether food prices excluding fresh items (+6.7% vs +6.9%) continue to moderate as projected.

- "JAPAN FINMIN KATAYAMA: CLOSELY WATCHING FX MOVES WITH A HIGH SENSE OF URGENCY RECENTLY SEEING ONE-SIDED, RAPID MOVES, IMPORTANT FOR CURRENCIES TO MOVE IN STABLE MANNER REFLECTING FUNDAMENTALS" RTRS"

- “KATAYAMA: CURRENCY MOVED PARTLY DUE TO MARKET VIEW ON BOJ, FED. BOJ'S DECISION WAS VERY REASONABLE" - BBG

- Bloomberg is reporting that Hedge funds are betting the yen will weaken to as low as 160 per dollar by the end of the year.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.50($1.42b). Upcoming Close Strikes : 150.00($1.13b Nov 3) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

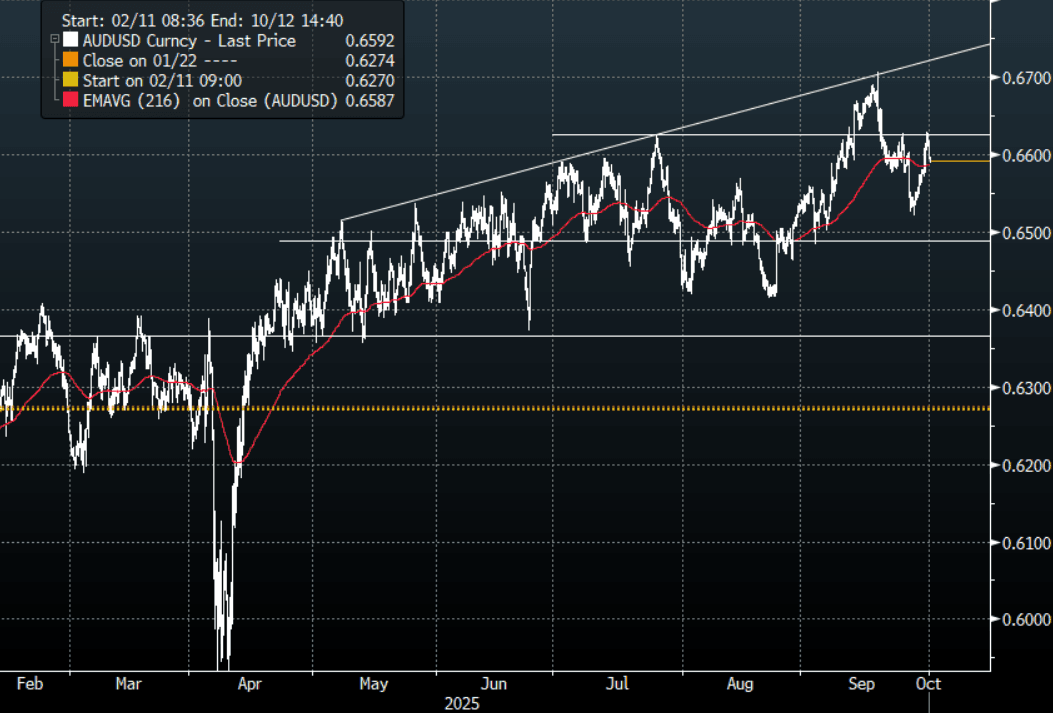

AUD: Asia Wrap - AUD/USD Gives Back Overnight Gains As Shutdown Begins

The AUD/USD has had a range of 0.6589- 0.6618 in the Asia- Pac session, it is currently trading around 0.6590, -0.32%. The AUD drifted lower in Asia in sympathy with US Equity futures which traded lower as the US Shutdown begins to be executed. Price action has stalled towards 0.6625 initially, the fate of the USD will determine if this move higher can regain the momentum to have another look toward the pivotal 0.6700 area. The Payrolls data this week was to be critical so should we not get it due to a shutdown the ADP print tonight could take on larger significance.

- MNI RBA WATCH: Bullock Declines To Confirm Easing Bias. Governor Michele Bullock declined to say whether the Reserve Bank of Australia retains an easing bias after the Board held the cash rate at 3.6% on Tuesday, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive.

- Bloomberg - “China Bans New BHP Orin Ore Cargoes Ad Pricing Dispute Grows. China’s state-run iron ore buyer has told major steelmakers and traders to temporarily halt purchases of all new BHP Group cargoes, escalating a pricing dispute that risks upending one of the mining giants most important trading partnerships.”

- "ALBANESE SAYS CHINA'S BAN ON BHP ORE CARGOES IS `DISAPPOINTING"

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD742m), 0.6600(AUD983m), 0.6700(AUD1.64b). Upcoming Close Strikes : 0.6600(AUD1.55b Oct 3), 0.6600(AUD1.74b Oct 2), 0.6700(AUD1.06b Oct 6) - BBG

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

- AUD/JPY - Asia-Pac range 97.49 - 97.92, Asia is trading around 97.50. The pair has struggled to gain any traction above 98.00 with the upward momentum stalling. A break sub 97.00 could signal a deeper correction.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

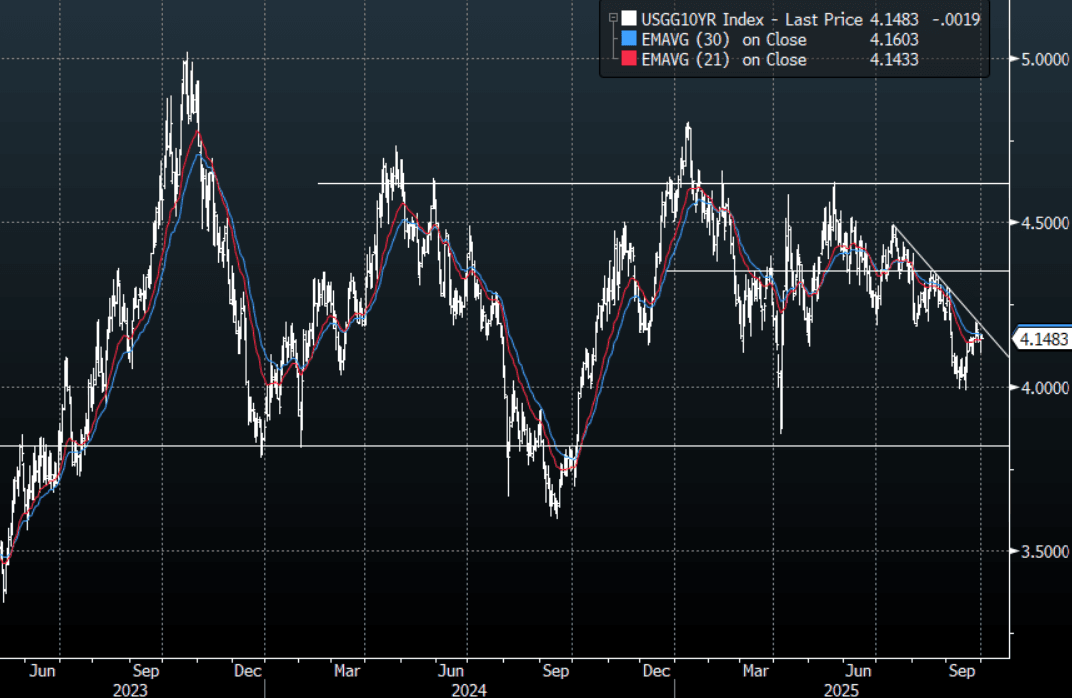

US TSYS: Asia Wrap - Yields A Little Lower As Shutdown Begins

The TYZ5 range has been 112-13 to 112-16+ during the Asia-Pacific session. It last changed hands at 112-16, unchanged from the previous close.

- The US 2-year yield has edged lower trading 3.605%.

- The US 10-year yield is trading around 4.148%.

- 10-Year yields remain subdued below 4.20% as the market prices in a US shutdown, I suspect buyers continue to be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week and if not then the ADP tonight starts to take on a lot more relevance.

- MNI: Fed’s Logan Cautious On Cuts Given Still-High Inflation. “I will be cautious about further rate cuts,” Logan said. "Even setting aside temporary effects of this year's increases in tariff rates, inflation is not convincingly on track to return all the way to 2%.”

- Brian Sullivan on X: “It can be an uncomfortable thing because so many people and families are worried about their paychecks, but markets tend to go UP in government shutdowns. It's because shutdowns 1) don't involve all of the government and 2) tend to be short and 3) the economy actually tends to keep growing. Weird but true.”

- Data/Events: MBA Mortgage Applications, ADP Employment Change, S&P Global US Manufacturing PMI, ISM Manufacturing, Construction Spending

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JGBS: Cash Bonds Little Changed At Lunch

At the Tokyo lunch break, JGB futures are stronger, +11 compared to settlement levels.

- The Q3 Tankan survey printed in line with expectations and Q2 but FY25 capex intentions increased 1pp to 12.5%. Large company business conditions have been moving sideways at a solid level since the start of last year, especially for the non-manufacturing sector.

- The large manufacturers' index rose 1 point to 14 in Q3 while the outlook for Q4 is forecast to deteriorate 2 points. The series has not been affected by new US tariffs and the 2025 average is slightly higher than 2024's.

- Non-manufacturers' conditions were steady at 34, well above the series average of +7.3, with the outlook at 28.

- Small non-manufacturers are also outperforming manufacturers with the index at 14 (down 1 point) compared to +1 (stable). The outlook for both sectors improved 1 point.

- The September BoJ summary of opinions showed a bias towards a resumption of tightening.

- (Bloomberg) Japan will get its second prime minister in just over a year when the ruling Liberal Democratic Party holds a leadership election on Oct. 4.

- Cash US tsys are slightly mixed, with a steepening bias, in today's Asia-Pac session after yesterday's modest twist-steepener.

- Cash JGBs are little changed across benchmarks.

- Swap rates are flat to 1bp lower, with a steepening bias. Swap spreads are mixed.