AUSSIE BONDS: 3yr Yield Near Cash Rate, +25bps Firmer This Week, RBA Next Tues

Aussie bond futures have traded a tight range so far today, the 3yr (YM) at 96.37 currently and 10yr (XM) 95.675. These levels are largely holding losses seen this week, as the Q3 CPI beat saw easing risks for this year significantly curtailed. The 3yr ACGB yield is up close to 25bps so far this week, the biggest weekly rise since 2024. We were last near 3.61% so around the RBA cash rate, while the 10yr is a little higher above 4.30%.

- Focus going forward will be around easing risks into 2026. Our policy team interviewed a senior ex RBA Economist this week who stated: "Stronger-than-expected Q3 inflation data has almost eliminated any chance of further easing by the Reserve Bank of Australia this year and could even force rate hikes in H1 2026 if Q4 and Q1 CPI results come in hot, a former RBA senior economist told MNI."

- Market pricing for the Nov meeting is close to flat, while only 5bps of easing risk is priced for Dec. A full cut next year is priced by around the August meeting, although for May we have 23bps of easing priced in.

- The AU-US 10yr spread is around +21bps, little changed, but the moved higher has slowed since the hawkish Fed cut earlier this week.

- The AU 3/10s curve is slightly steeper at +70bps, but holding the bulk of this week's down move from +77bps.

- On the data front today we just had Q3 PPI, which rose to 3.5%y/y, from 3.4%, while the Sep credit figures were +0.6%m/m, in line with market forecasts.

- Next week, we have the RBA meeting outcome on Tuesday with no change expected, but focus will be on the updated forecast projections and how that shapes the outlook into 2026.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GOLD: Gold Off Earlier High After Senate Vote Fails, Shutdown Has Begun

Gold prices spiked to a new record at $3878.53/oz during Wednesday after a vote in the US senate failed to break the debt ceiling impasse. It has benefited from significant safe haven flows driven by related concerns. The government shutdown began at midnight ET but bullion remains below the earlier high up 0.1% to $3860.8 as the risk had been priced in. The US dollar index is slightly higher and yields are little changed.

- September US payrolls scheduled for Friday were widely anticipated to gauge the Fed outlook but at this stage they look they will be delayed. Fed views continue to diverge with 2026’s FOMC member Logan saying that easing should proceed cautiously.

- President Trump has said that the shutdown is likely to result in job losses.

- Silver reached a high of $47.56, breaking above initial resistance at $47.251, earlier in the APAC session but is now up 0.9% today at around $47.04. It has also benefited from US concerns but also physical tightness given its use in solar panels.

- Equities are mixed with the S&P e-mini down 0.4% and Nikkei -1.0% but KOSPI up 0.8%. Oil prices are slightly higher with WTI +0.3% to $62.57/bbl. Copper is down 0.3%.

- With the government shutdown, some US data may be delayed. September ADP employment, final September S&P Global manufacturing PMI & ISM and August construction are scheduled for Wednesday. European September manufacturing PMIs and euro area September CPI print. The Fed’s Barkin and Goolsbee and ECB’s Elderson & de Guindos speak.

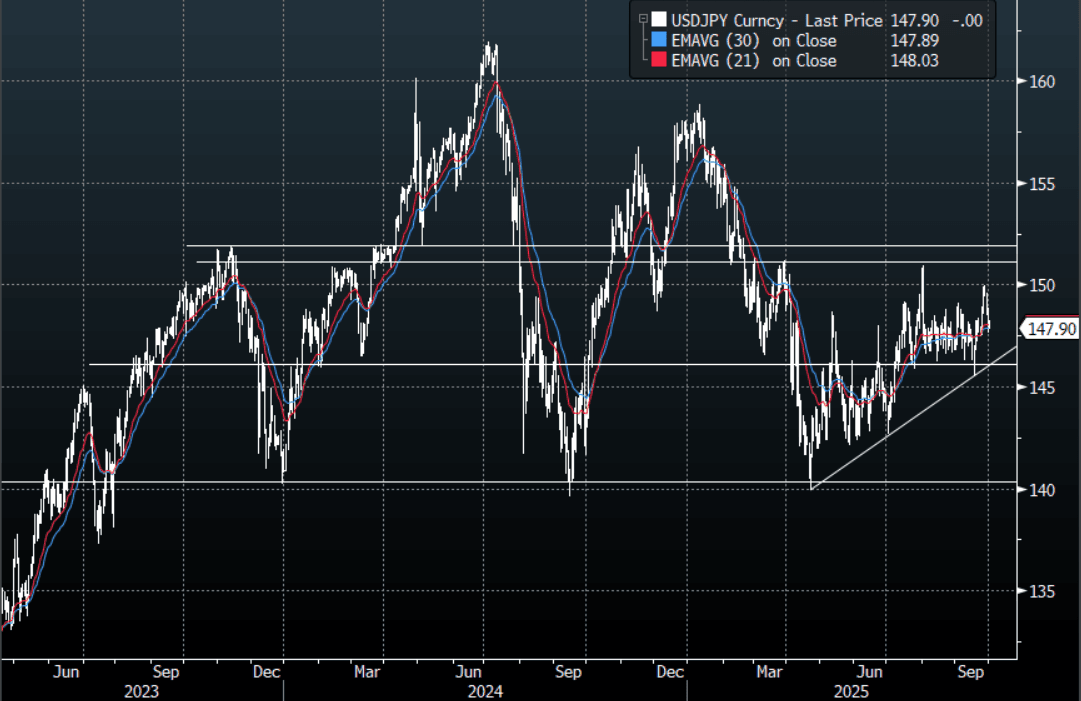

JPY: Asia Wrap - USD/JPY Tries And Fails Above 148.00 On The Tankan

The USD/JPY range has been 147.82 - 148.23 in the Asia-Pac session, it is currently trading around 147.90, -0.02%. The pair popped back above 148.00 on the Tankan survey but failed toward 148.25 and quickly reversed all of its gains. We are once again right back in the middle of very familiar ranges. The Payrolls data this week was to be critical, so a shutdown now makes the ADP print tonight take on larger significance. First support is seen around 147.50 then back toward the bottom of the range around 146.00.

- MNI - Tankan Steady, Capex Intentions Higher: The Q3 Tankan survey printed in line with expectations and Q2 but FY25 capex intentions increased 1pp to 12.5%. Large company business conditions have been moving sideways at a solid level since the start of last year, especially for the non-manufacturing sector. Respondents see USDJPY around 145.68 in FY25.

- Bloomberg - “Markets are focused on how Japan will finance $550 billion in investment it has agreed to make in the US as part of a trade deal with President Donald Trump. The readily available resources that meet Tokyo’s funding conditions don’t look sufficient — we see a $250 billion shortfall.”

- "AKAZAWA: WANT NEXT ADMINISTRATION TO CARRY OUT $550B FUND, US NOT INTERESTED IN BREAKDOWN OF INVESTMENT, LOANS, UP TO JAPAN TO DECIDE INVESTMENT AMOUNT WITHIN $550B, ILL USE $550B FUND IN WAYS THAT WON'T IMPACT FOREX" - BBG

- "KOIZUMI LEADS JAPAN LDP RACE AMONG LAWMAKERS: ASAHI POLL" - BBG

- "JAPAN DPP LEADER TAMAKI: ETF SALES COULD FUND GOVT SPENDING, BOJ SHOULD OFFLOAD ALL ETFS WITHIN 15 YEARS" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 146.15($864m), 146.50($1.09b), 147.50($650m). Upcoming Close Strikes : 147.00($1.21b Oct 6), 148.00($1.15b Oct 2) - BBG.

- CFTC data shows last week asset managers increased their JPY longs slightly +79262( Last +71162), leveraged funds though again used the dip to add to their short position as the support held, -634171(Last -58811). The diverging views amongst investors continue to build.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

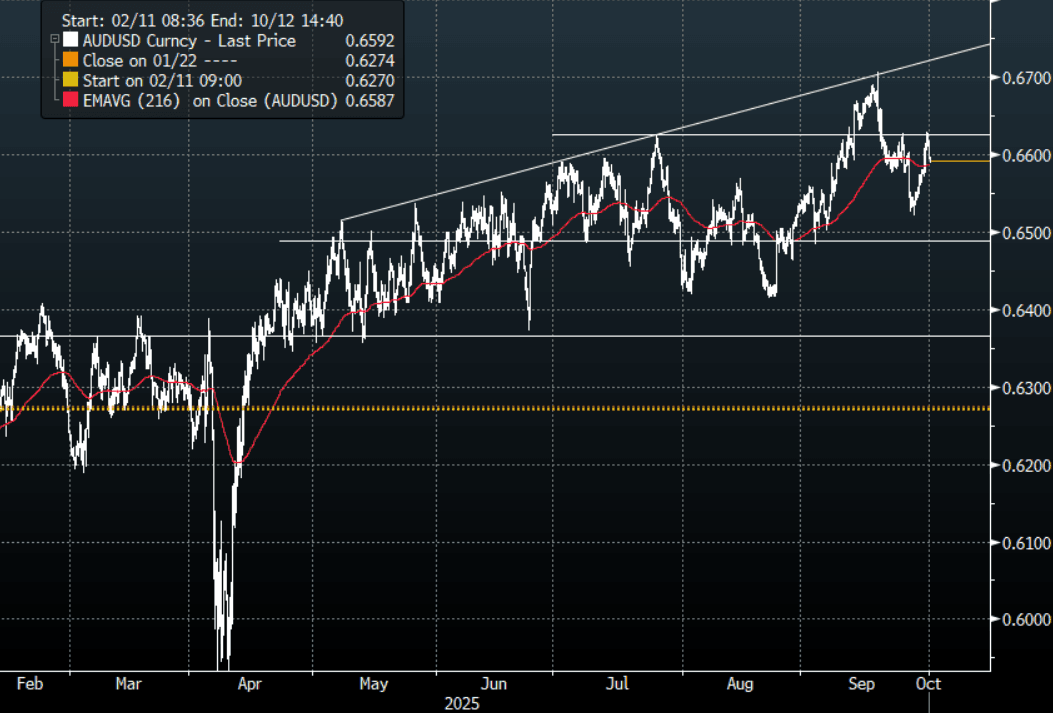

AUD: Asia Wrap - AUD/USD Gives Back Overnight Gains As Shutdown Begins

The AUD/USD has had a range of 0.6589- 0.6618 in the Asia- Pac session, it is currently trading around 0.6590, -0.32%. The AUD drifted lower in Asia in sympathy with US Equity futures which traded lower as the US Shutdown begins to be executed. Price action has stalled towards 0.6625 initially, the fate of the USD will determine if this move higher can regain the momentum to have another look toward the pivotal 0.6700 area. The Payrolls data this week was to be critical so should we not get it due to a shutdown the ADP print tonight could take on larger significance.

- MNI RBA WATCH: Bullock Declines To Confirm Easing Bias. Governor Michele Bullock declined to say whether the Reserve Bank of Australia retains an easing bias after the Board held the cash rate at 3.6% on Tuesday, stressing that future moves will depend on incoming data, with the current level still viewed as slightly restrictive.

- Bloomberg - “China Bans New BHP Orin Ore Cargoes Ad Pricing Dispute Grows. China’s state-run iron ore buyer has told major steelmakers and traders to temporarily halt purchases of all new BHP Group cargoes, escalating a pricing dispute that risks upending one of the mining giants most important trading partnerships.”

- "ALBANESE SAYS CHINA'S BAN ON BHP ORE CARGOES IS `DISAPPOINTING"

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD742m), 0.6600(AUD983m), 0.6700(AUD1.64b). Upcoming Close Strikes : 0.6600(AUD1.55b Oct 3), 0.6600(AUD1.74b Oct 2), 0.6700(AUD1.06b Oct 6) - BBG

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

- AUD/JPY - Asia-Pac range 97.49 - 97.92, Asia is trading around 97.50. The pair has struggled to gain any traction above 98.00 with the upward momentum stalling. A break sub 97.00 could signal a deeper correction.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P