MNI EUROPEAN OPEN: China Exports Up, Trade Conflict Escalates

EXECUTIVE SUMMARY

- TRUMP, VANCE OPEN DOOR TO CHINA DEAL AS TRADE SPAT DRAGS ON - BBG

- FRENCH PM LECORNU NAMES NEW GOVERNMENT BEFORE LOOMING BUDGET DEALINE - FRANCE 24

- KEEPING UK MANIFESTO PROMISES TOUGH, NOT IMPOSSIBLE - IFS - MNI

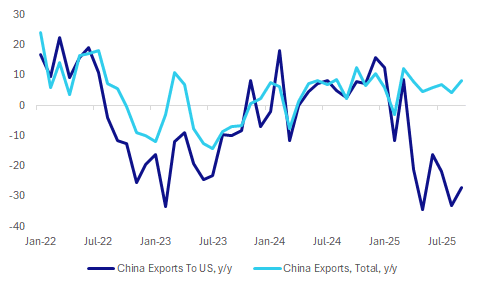

- CHINA'S SEP EXPORTS +8.3%, IMPORTS +7.4% - MNI BRIEF

- THE RBA BELIEVES ITS CASH RATE IS STILL RESTRICTIVE - MNI

Fig 1: China Aggregate Export Growth Holding Up - Y/Y

Source: MNI - Market News/Bloomberg/Refinitiv.

UK

FISCAL (MNI): Restoring the UK’s fiscal headroom will be “difficult, but not impossible” without breaking Labour’s manifesto pledges not to raise VAT, National Insurance, or income tax in the Nov 26 budget, the Institute for Fiscal Studies said in a report published on Monday.

BUDGET (TIMES): “Rachel Reeves could pass a one-off wealth tax to avoid “half-baked fixes” that risk breaking Labour’s manifesto pledge not to raise income tax, VAT or national insurance, leading economists have said. The Institute for Fiscal Studies has published a detailed list of options.”

POLITICS (TIMES): “The leader of Reform UK will promise not to reduce taxes before reducing spending, deep cuts to the civil service and a ban on borrowing to fund government expenditure in his first big speech on the economy next month.”

EU

FRANCE (FRANCE24): “Reinstated French Prime Minister Sebastien Lecornu named a new government Sunday after a meeting with President Emmanuel Macron, as he faces pressure to urgently produce a budget and quell the political turmoil engulfing France.”

UKRAINE (BBC): “In a statement, the leaders of the UK, France and Germany said the joint action would "increase pressure" on Russian President Vladimir Putin and "bring Russia to the negotiation table". It added the move would be taken "in close cooperation" with the US.”

DENMARK (BBC): “Denmark has announced $4.2bn (£3.2bn) of extra defence spending to boost security in the Arctic and North Atlantic regions, including Greenland. It will also spend $4.5bn buying 16 more F-35 fighter jets from the US.”

NETHERLANDS (POLITICO): “Dutch far-right leader Geert Wilders has put his campaign on hold “until further notice” after being informed that he was among several politicians in the crosshairs of a suspected terrorist group. Wilders, whose Party for Freedom is currently leading in the polls ahead of a snap parliamentary elections set for Oct. 29.”

PORTUGAL (POLITICO): “The top candidates to lead Lisbon and Porto remained neck and neck as the ballots deposited in Sunday’s nationwide local elections in Portugal continue to be counted early Monday morning. While the race is too close to call in the country’s largest cities, elsewhere official results indicate the far-right Chega party failed to conquer any major cities.”

ITALY (POLITICO): “Italian Prime Minister Giorgia Meloni appears to be edging closer to a politically viable tax on banks, with both sides more open to compromise after earlier attempts fizzled under pressure from financial elites.”

POLAND (POLITICO): “Poland’s centrist government is pushing to restore the rule of law undermined by the previous populist administration — but the country’s divided politics mean the chances of success are slim.”

ISRAEL (POLITICO): “Israel’s new ambassador to the EU tells POLITICO that Europe is not likely to get a seat on Trump’s “board of peace” unless it restores full cooperation with Netanyahu’s government.”

US

US/CHINA (BBG): “ President Donald Trump’s administration signaled openness Sunday to a deal with China to quell fresh trade tensions while also warning that recent export controls announced by Beijing were a major barrier to talks.”

FED (MNI): Federal Reserve Bank of St. Louis President Alberto Musalem said Friday the U.S. central bank should proceed with caution as it considers further interest rate cuts but he remains open-minded about easing.

UKRAINE/RUSSIA (POLITICO): “President Donald Trump said that he and Ukrainian President Volodymyr Zelenskyy discussed during a Sunday phone call the possibility of Ukraine obtaining long-range Tomahawk missiles. But Trump, speaking to reporters on board Air Force Once en route to Israel, said he might speak to Russian President Vladimir Putin about it first — because it would be a “step up” in the war.”

OTHER

AUSTRALIA (MNI POLICY): The RBA believes its cash rate is still restrictive. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

MIDDLE EAST (BBG): "President Donald Trump will look to seal the biggest diplomatic achievement of his second term when he travels to the Middle East to herald a deal ending the Israel-Hamas war and greet hostages emerging from two years of subjugation."

CHINA

TRADE (MNI BRIEF): China's exports increased 8.3% y/y in September, while imports rose 7.4%, data released by China Customs showed on Monday. Exports in September rose 8.3% y/y to USD 328.6 billion, accelerating from 4.4% in August and exceeding expectations for 6.5% growth. Imports climbed 7.4% y/y, up sharply from 1.3% in August and well above the 1.8% market consensus.

COMMODITIES (MNI BRIEF): China’s imports of iron-ore reached 116 million metric tonnes in September, up 10.5% m/m, according to customs statistics released on Monday. Beijing’s inbound shipments of iron-ore now total 918 million metric tonnes during the first nine months of the year, down 0.1% y/y, improving from the -1.6% during the first eight months.

AUTOS (RTRS): "China's car sales accelerated in September, the traditional peak season for the auto market, as dealers and consumers took advantage of trade-in subsidies before more local governments suspended the incentives."

MNI: PBOC Net Injects CNY137.8 Bln via OMO Monday

MNI (BEIJING) - The People's Bank of China (PBOC) conducted CNY137.8 billion via 7-day reverse repos, with the rate unchanged at 1.40%. The operation led to a net injection of CNY137.8 billion as no reverse matures today, according to Wind Information.

- The seven-day weighted average interbank repo rate for depository institutions (DR007) rose to 1.4404% at 09:50 am local time from the close of 1.3945% on Friday.

- The CFETS-NEX money-market sentiment index, measuring interbank money-market liquidity, closed at 46 on Monday, compared with the close of 47 on Saturday. A higher reading points to tighter liquidity condition, with 50 representing an equilibrium.

MNI: PBOC Sets Yuan Parity Lower At 7.1007 Mon; -0.28% Y/Y

MNI (BEIJING) - The People's Bank of China (PBOC) set the dollar-yuan central parity rate lower at 7.1007 on Monday, compared with 7.1048 set on Friday. The fixing was estimated at 7.1234 by Bloomberg survey today.

MNI: China CFETS Yuan Index Up 0.55% In Week of Oct 10

The CFETS Weekly RMB Index was 97.32 on Oct 10, up 0.55% from 96.77 on Sep 30.

MARKET DATA

NEW ZEALAND BNZ SEPT. SERVICES PSI 48.3; AUG. 47.6

NEW ZEALAND AUG. NET MIGRATION ESTIMATE +460; JUL. +1770

SOUTH KOREA OCT. 1-10 EXPORTS -15.2% Y/Y; PRIOR +3.8%

SOUTH KOREA OCT. 1-10 IMPORTS -22.8% Y/Y; PRIOR +11.1%

CHINA'S SEPT. TRADE BALANCE CNY645.5 BLN; AUG. CNY 730.0B

CHINA SEPT. IMPORTS IN YUAN TERMS +7.5% Y/Y; AUG. +1.7%

CHINA SEPT. EXPORTS IN YUAN TERMS +8.4% Y/Y; AUG. +4.8%

CHINA SEPT. IMPORTS IN USD TERMS +7.4% Y/Y; EST. +1.8%; AUG. +1.3%

CHINA SEPT. EXPORTS IN USD TERMS +8.3% Y/Y; EST. +6.6%; AUG. +4.4%

CHINA SEPT. TRADE SURPLUS $90.45B; EST. +$98.05B; AUG. $102.33B

MARKETS

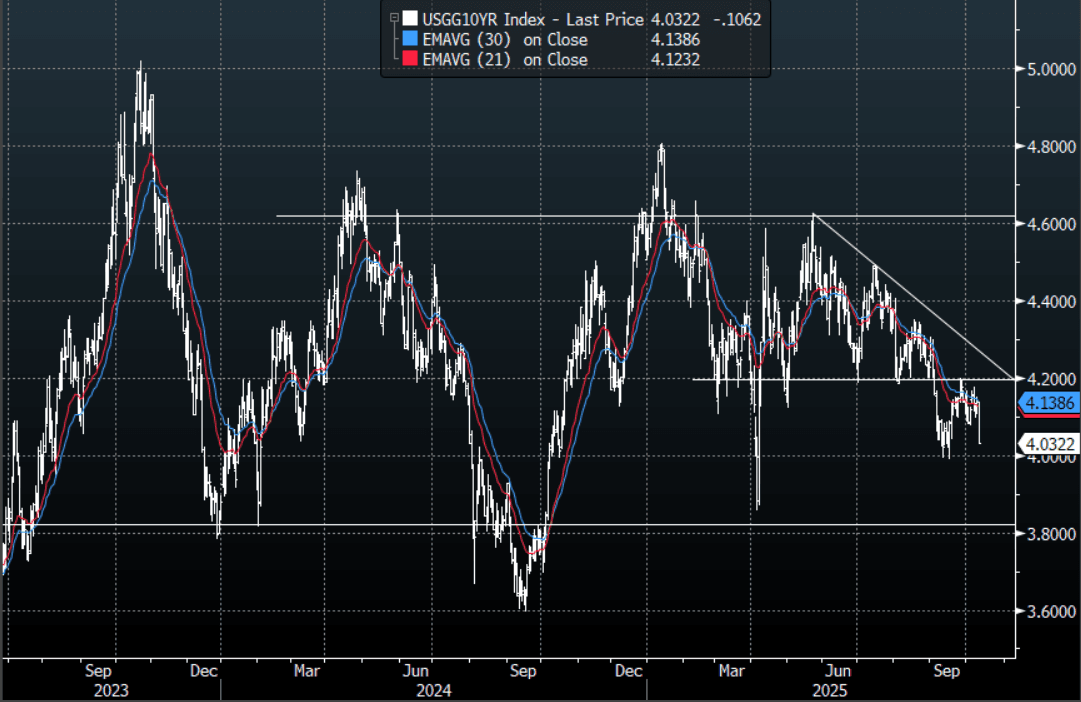

US TSYS: Futures Move Lower As Flare Up Is Trying To Be Walked Back

The TYZ5 range has been 112-30 to 113-03+ during the Asia-Pacific session. It last changed hands at 113-00, down 0-04+ from the previous close.

- 10-Year yields accelerated lower on Friday on the back of China/US Escalation. Some clarification from China over the weekend on their new rare earth export controls has seen the US walk back its aggressive stance and a more conciliatory tone is being set. I suspect a lot of Friday's moves will see some decent pullbacks on this, but how long it lasts is anybody's guess.

- The Cash Market was closed in Asia due to a Japanese Holiday.

- Robin Brooks wrote a substack expanding on how he thought markets might play out if the situation escalates again: “If the China-US trade war escalates and China devalues, there'll be lots of collateral damage: (i) US Treasury market will go "yippy" like in April; (ii) high-debt countries like Japan and France will suffer; (iii) $-pegs in Argentina and Turkey will blow.” https://t.co/Sh4nlrKDWC

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUSSIE BONDS: Key Resistance For Futures Remains Intact, RBA Mins Tomorrow

Aussie bond futures are holding higher, but away from best levels. Important key resistance points remain intact. 3yr futures were last 96.47 (+7bps), while 10yr futures were at 95.685 (+7bps). Earlier highs were at 96.505 for the 3yr and 95.7050 for the 10yr. Some cap for futures has come from the softer US Tsy futures tone and better risk appetite trends more broadly, with US official comments showing reduced recent rhetoric around US-China trade issues (albeit still with the threat of higher tariff levels come Nov 1, per remarks by US President Trump).

- Short term resistance points for futures are as follows. For 3yr: RES 1: 96.615 - High Sep 12 , while for 10yr: RES 1: 96.615 - High Sep 12.

- Cash ACGB yields are around 6-7bps lower across the curve, with the front end slightly weaker in yield terms. The 33yr benchmark last 3.50%, while the 10yr was at 4.29%, with little change in the Au3/10s curve.

- The bias is likely to be fade this yield move in Aussie, given RBA comfort around the current macro backdrop. A risk remains from higher US tariff levels on China, export controls etc, which could see negative spill over to the Australian economic outlook. For the 3yr Aussie bond, moves under 3.45% may be faded.

- At this stage, per Polymarket, 100% tariff odds by Nov 1 sit at 17%.

- Looking ahead to tomorrow, the publication of the September 30 decision minutes will be important given the Board’s more cautious tone and Bullock avoiding to state what the current stance is. She also noted that Board is concerned about certain CPI components including market services. NAB’s September business survey also prints on Tuesday.

BONDS: NZGBS: Yields Up From Lows, But Bearish Bias Intact Given Data

NZGB yields have pared losses as Monday's session has unfolded, consistent with improved risk appetite amid higher US equity futures and lower US Tsy futures. We were last 2-4.5bps weaker, led by the backend. Near term focus will remain on US-China tensions, as markets look for an off ramp to higher US tariff level and export controls. Comments from US officials up to President Trump hint at an openness to negotiate. Still, for NZGBs the risks remain for lower levels in yield terms, so long as domestic growth remains soft, something reinforced by today's data.

- The 2yr was last at 2.60% (today's low near 2.55%), the 10yr at 4.08% (today's low was under 4.04%). The 2/10s curve is around +148, flatter versus recent highs of +154bps.

- The 2yr swap rate got to lows of 2.355%, but we sit back at 2.38% in latest dealings, off close to 2bps for the session. In yield terms the 2yr swap rate is oversold, but upticks, particularly back towards 2.50% may be used as fresh entry points to express lower yield risks. Longer term trends still look for move into the 2.00-2.25% region, without a broader shift in the macro backdrop.

- On the data front, the BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. The manufacturing sector stagnated in August/September, while services continued to contract but at a slower rate with September. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

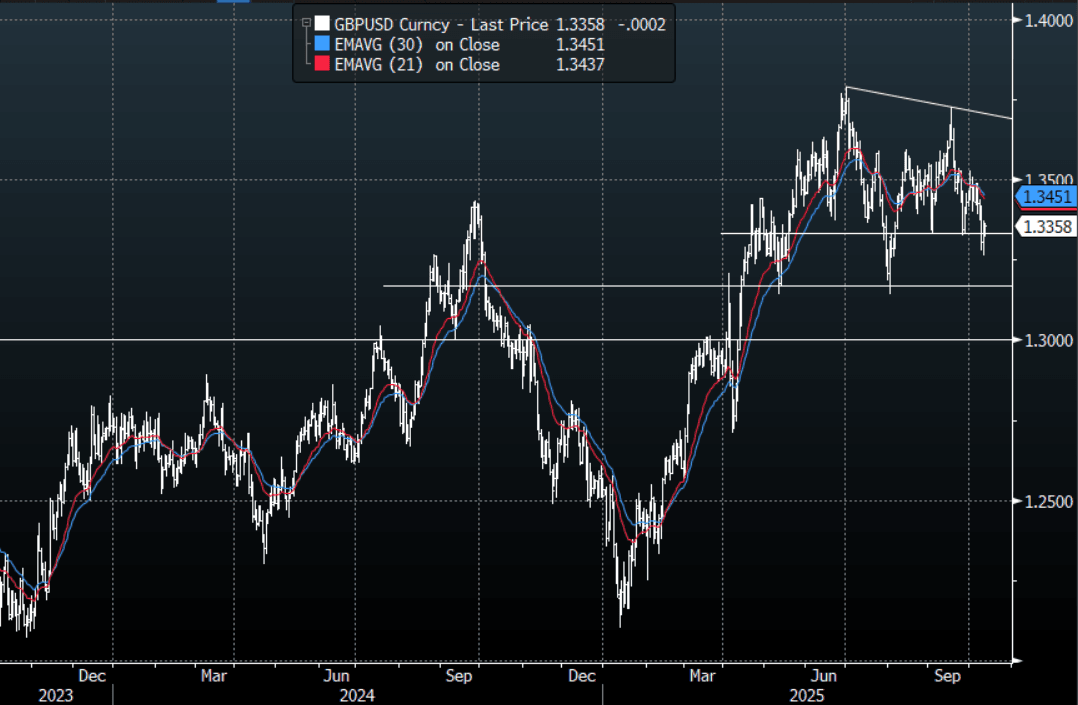

FOREX: Asia-Pac: USD Drifts Lower

The BBDXY has had a range of 1211.98 - 1214.25 in the Asia-Pac session; it is currently trading around 1212, -0.10%. The USD correction higher stalled just as it began to probe its longer-term resistance. The 1215-1225 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the USD shorts. The weaker hands may be folding but I suspect we would need to do some work before the market can call a low for the USD as longer term accounts potentially look to fade this squeeze as they increase hedging ratios.

- EUR/USD - Asian range 1.1592 - 1.1628, Asia is currently trading 1.1620. Price found some decent demand towards its first support around the 1.1550 area; a break through here is needed to signal a deeper correction towards the more important 1.1200-1.1300 support. Expect sellers back towards the 1.1700 area first up.

- GBP/USD - Asian range 1.3333 - 1.3363, Asia is currently dealing around 1.3360. The pair looks to have had a false break below the 1.3300 area. I suspect sellers should reemerge on any bounce back toward the 1.3450/1.3500 area.

- USD/CNH - Asian range 7.1320 - 7.1455, the USD/CNY fix printed lower at 7.1007, Asia is currently dealing around 7.1380. The area around 7.1500/1600 has proved to be solid resistance and with the PBOC managing the fix lower, it looks likely we could consolidate 7.09-7.16 for the moment.

- Cross asset : SPX +1.25%, Gold $4055, US TYZ5 112-31+, BBDXY 1212, Crude Oil $59.74

- Data/Events : Italy Bloomberg Oct. Italy Economic Survey, Germany Wholesale Price Index/Bloomberg Oct. Germany Economic Survey/Current Account Balance, EZ Bloomberg Oct. Eurozone Economic Survey, France Bloomberg Oct. France Economic Survey, Spain Bloomberg Oct. Spain Economic Survey

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

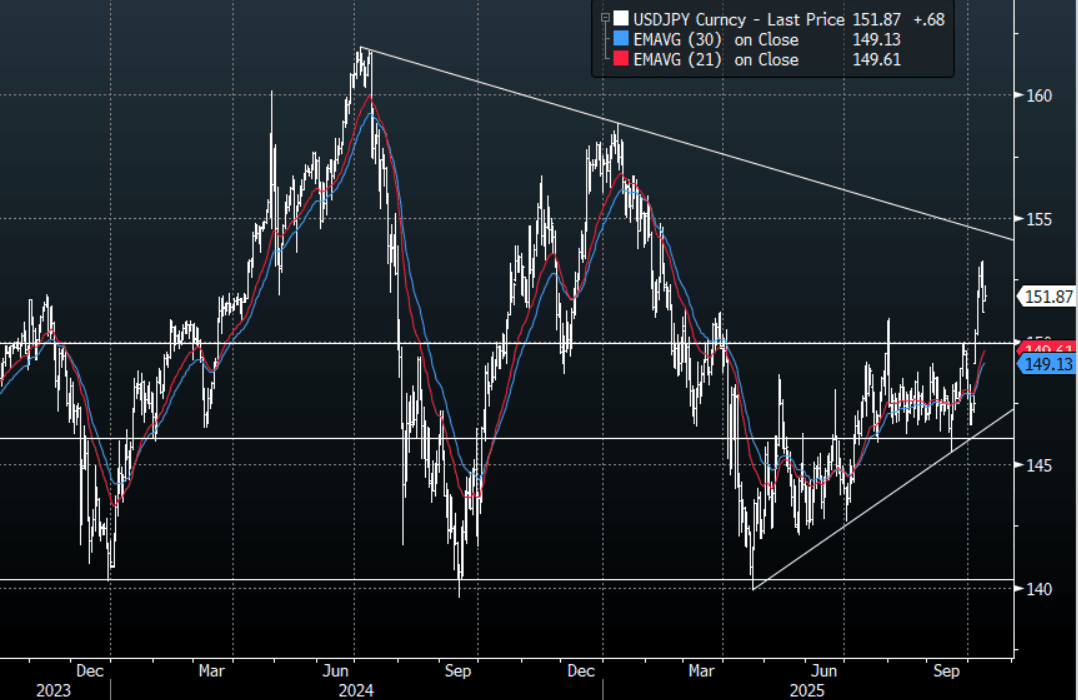

JPY: Asia-Pac: USD/JPY Consolidates Around 152.00

The USD/JPY range has been 151.74 - 152.28 in the Asia-Pac session, it is currently trading around 151.90, +0.45%. The pair collapsed with risk and US yields, and I am a little surprised the bounce this morning has not been bigger on the more conciliatory tone now being used. The Crypto market has led the retracement in risk higher over the weekend as the temperature was lowered, but the huge deleveraging of positions and the first crack in the markets conviction will be hard to just shake off. The JPY crosses in particular took the brunt of it on Friday and the rejections some pairs had look ugly. It will be interesting to see how the week starts and how much faith the markets have in those in charge to sort this mess out amicably. Technically dips back toward the 150/151 area should now find support first up.

- The FT is reporting the Dutch Government is taking control of the Chinese-owned chipmaker Nexperia, which could further inflame the situation. Arnaud Bertrand wrote a thread on X: “It invites retaliation from China, which is almost systematic. I wouldn't want to be a Dutch company with Chinese operations right now.”

- "KOMEITO DOESN'T RULE OUT OPPOSITION PARTY COOPERATION: KYODO" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 150.00($340m), 151.00($856m). Upcoming Close Strikes : 150.00($986m Oct 15) - BBG.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

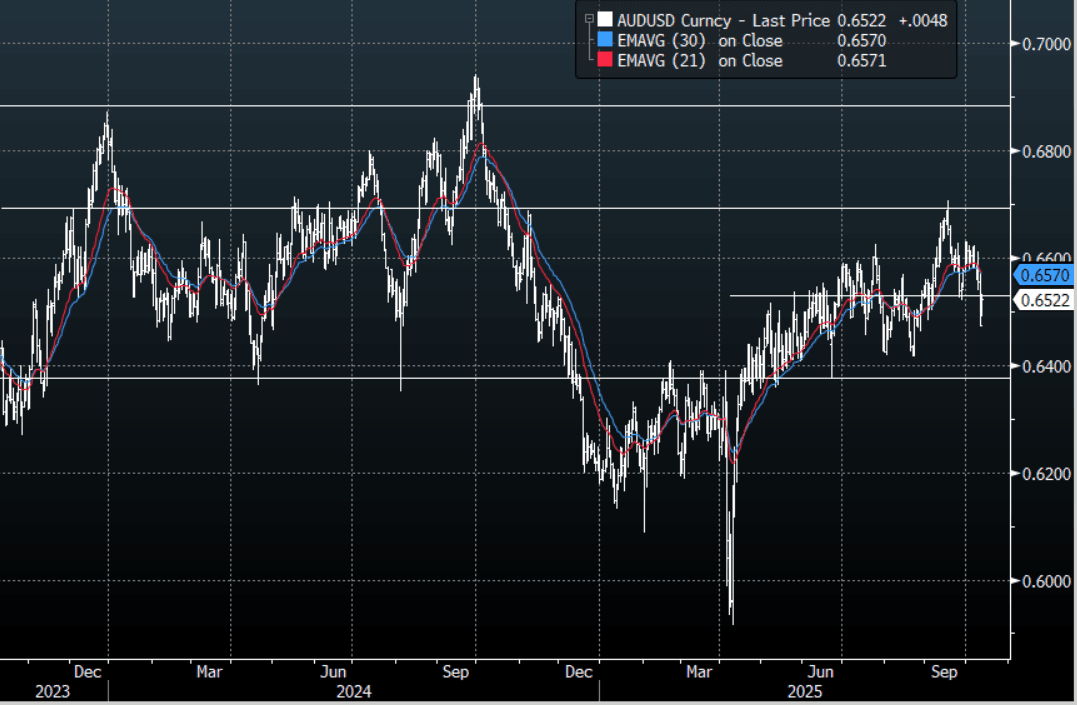

AUD: Asia-Pac: AUD/USD Bounces With Risk & A Lower CNY Fix

The AUD/USD has had a range of 0.6491 - 0.6533 in the Asia- Pac session, it is currently trading around 0.6520, +0.75%. Some clarification from China over the weekend on their new rare earth export controls has seen the US walk back its aggressive stance and a more conciliatory tone is being set. I suspect a lot of Friday's moves will see some decent pullbacks on this, but how long it lasts is anybody's guess. The AUD has gapped higher on the open and another very low CNY fix from the PBOC has underpinned the move for now. A lot of leverage would have been taken out last week and it's very hard for the market to just regain the conviction it previously had so I suspect the rally will stall at some point as those still overweight risk use the opportunity to pare back.

- The FT is reporting the Dutch Government is taking control of the Chinese-owned chipmaker Nexperia, which could further inflame the situation. Arnaud Bertrand wrote a thread on X: “It invites retaliation from China, which is almost systematic. I wouldn't want to be a Dutch company with Chinese operations right now.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AD403m), 0.6555(AUD529m). Upcoming Close Strikes : 0.6500(AUD1.01b Oct 14), 0.6600(AUD948m Oct 14), 0.6650(AUD880m Oct 14) - BBG

- AUD/JPY - Asia-Pac range 98.57 - 99.23, Asia is trading around 99.05. The pair had an ugly rejection above 100. This morning the pair has bounced in sympathy with risk rallying, but it will need this move in risk to get back to the previous highs for it to look at breaking above 100 again.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia-Pac: NZD/USD Drifts Higher In Sympathy & Lower CNY Fix

The NZD/USD had a range of 0.5722 - 0.5745 in the Asia-Pac session, going into the London open trading around 0.5740, +0.30%. Some clarification from China over the weekend on their new rare earth export controls has seen the US walk back its aggressive stance and a more conciliatory tone is being set. I suspect a lot of Friday's moves will see some decent pullbacks on this, but how long it lasts is anybody's guess. The NZD has drifted higher from the open in sympathy to moves elsewhere and another very low CNY fix from the PBOC which has underpinned the move for now. The NZD had a poor weekly close though and technically remains a sell on rallies now for those looking for a currency to be short of in their basket. The sell zone remains back toward the 0.5800 area with the market looking for a potential move back towards the 0.5500/0.5600 area.

- MNI - Services & Manufacturing Indices Signal Ongoing Weak Q3 Activity. The BNZ services and manufacturing PMIs for September were consistent with the RBNZ’s assessment in its October statement that “economic activity recovered modestly in the September quarter”. Continued weak activity, including employment, at the end of the quarter is consistent with further RBNZ easing with policy likely to become stimulatory.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5850(NZD300m Oct 14), 0.5950(NZD312m Oct 16) - BBG

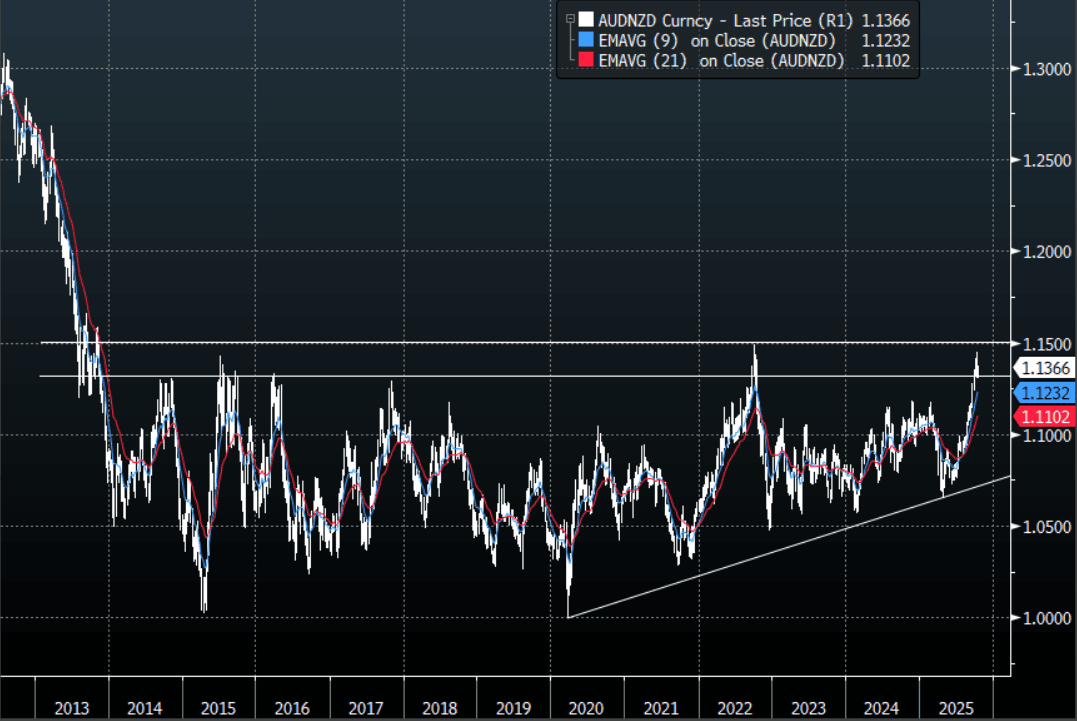

- AUD/NZD range for the session has been 1.1321 - 1.1373, currently trading around 1.1365. The Cross failed again above the 1.1400 area where I suspect initial paring back of longs. A clear sustained break above 1.15/1.16 resistance and the market will begin to think about levels back towards 1.2000 and above. Dips back toward 1.1200 should be a good place to start buying again if seen.

Fig 1: AUD/NZD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: As Trade War Intensifies, Equities Suffer (amended)

- With Japan out today, it was left to China's major bourses to guide sentiment as the trade war rhetoric ramps up. Having declined over -1.9% Friday, the CSI 300 started the week on the back foot, dragging the other key bourses with it. Down -1.7% today, it was the biggest two days of consecutive falls since April when the trade war began first ratcheted up. The Hang Seng fell sharply, down -3.3% as it traded through the key 20-day and 50-day EMA's and now is approaching the 100-day EMA which it last traded below in April. There was little positives to find as Shanghai Comp fell -1.30% and Shenzhen down -2.2%. The retail expansion of equity accounts over recent months has been a key contributor to the performance of stocks and comes on the back of a multi year decline in housing. The authorities will be loathe to see significant stock losses for investors and news agencies over the weekend were keen to spell out that the outlook for the CSI 300 should be little impact by the threats coming from Washington.

- Unsurprisingly the KOSPI followed China's lead and is down -1.6%. As always with market, context is key and the KPSPI hit new all time highs recently and any move lower is as much driven by the locking in of profits by investors, rather than a sea change in sentiment at this stage.

- With the JCI doing very little, South East Asia's other major bourse the FTSE Malay KLCI is down just over -0.50%. It has consistently underperformed the run up in equities in the recent period of strength and naturally its downside seems less pronounced.

- The focus on China arguably gives India a short respite having been in the sights of the US recently. The NIFTY 50 delivered a positive though modest week of gains last week, yet is giving some of those gains back in Monday morning trade.

OIL: Partial Recovery On Hopes Of US-China Trade De-escalation

Oil prices are 1.3% higher on Monday with some payback for Friday’s fall of around 5% plus also some relief from US/China comments on the weekend that the current trade issues can be resolved. Since President Trump’s announcement of tariffs at the start of the year, oil markets have been concerned about the impact of increased protectionism on energy demand at a time of excess supply.

- WTI is up 1.3% to $59.65/bbl off the intraday high of $60.01. Brent is 1.3% higher at $63.56 after reaching $63.84. The USD index is slightly lower also helping dollar-denominated crude.

- Trump sounded confident before flying to the Middle East that the trade issues with China can be resolved when he speaks with President Xi at the end of October. Xi stated that China will retaliate if the US imposes 100% tariffs on November 1.

- Risks remain around Ukraine-Russia with strikes continuing and Ukraine hitting a major Russian refinery on the weekend. President Zelenskyy also discussed longer-range Tomahawk missiles with Trump, which Russia sees as an escalation.

- Later the Fed’s Paulson speaks. The US bond market is shut but equities are open. IMF/World Bank meetings are taking place. The ECB’s Buch and BoE’s Mann and Greene speak. Germany’s September WPI prints.

GOLD: Trade Jitters Drive Safe-Haven Flows, New Highs For Gold & Silver

Gold fell early in the APAC session to $4006.48/oz on comments from US President Trump suggesting that the US-China trade situation may not be as severe as implied on Friday. However, it didn’t last and concerns that the trade war could be reignited as well as a lower US dollar drove gold just above last Wednesday’s record to $4060.01, opening resistance at $4074.5, a Fibonacci projection. It is currently 1.0% higher at $4057.4.

- Silver has rallied strongly with prices up 2.3% to $51.47, close to the intraday high and above resistance and all-time high at $51.235. It is also above a Fibonacci projection at $51.405 opening round number resistance at $52.00. It has been boosted not just by trade-related safe-haven flows but also by constrained liquidity in London. In addition, it remains unclear if it will be excluded from US import duties.

- Regional equities have sold off with the Hang Seng down 3.5% and ASX -1.0% but S&P e-mini up 1.2%. Oil prices are higher with WTI +1.4% to $59.73/bbl. Copper is up 2.0%.

- Later the Fed’s Paulson speaks. The US bond market is shut but equities are open. IMF/World Bank meetings are taking place. The ECB’s Buch and BoE’s Mann and Greene speak. Germany’s September WPI prints.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 13/10/2025 | 1105/1205 | BOE Greene at Society of Professional Economists Conference | ||

| 13/10/2025 | - | *** | Money Supply | |

| 13/10/2025 | - | *** | New Loans | |

| 13/10/2025 | - | *** | Social Financing | |

| 13/10/2025 | - | ECB Lagarde and Cipollone at IMF/World Bank Meetings | ||

| 13/10/2025 | 1655/1255 | Philly Fed's Anna Paulson | ||

| 13/10/2025 | 1910/2010 | BOE Mann in MonPol Panel, National Association of Business Economists | ||

| 14/10/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - AWE & Unemployment | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0700 | *** | Labour Market - Payrolls & Claimants | |

| 14/10/2025 | 0600/0800 | *** | Germany CPI (f) | |

| 14/10/2025 | 0750/0950 | ECB Cipollone Speech on Digital Euro | ||

| 14/10/2025 | 0900/1100 | *** | ZEW Current Expectations Index | |

| 14/10/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 14/10/2025 | - | ECB Lagarde and Cipollone at G20 Meeting | ||

| 14/10/2025 | 1200/1300 | BOE Taylor Remarks and Fireside Chat at University of Cambridge | ||

| 14/10/2025 | 1230/0830 | * | Building Permits | |

| 14/10/2025 | 1245/0845 | Fed Governor Michelle Bowman | ||

| 14/10/2025 | 1255/0855 | ** | Redbook Retail Sales Index |