MNI EUROPEAN OPEN: China Assessing Possibility of Trade Talks

EXECUTIVE SUMMARY

- CHINA SAYS US EAGER TO NEGOTIATE ON TARIFFS, BEIJING’S DOOR IS ‘OPEN’ - RTRS

- TRUMP TO PROPOSE SLASHING $163 BILLION IN GOVERNMENT PROGRAMS IN BUDGET BLUEPRINT - WSJ

- JAPAN SAYS ITS $1 TRILLION IN US TREASURIES IS AMONG TOOLS FOR TRADE TALKS - RTRS

- MNI DISCUSSES THE RBA CASH RATE STRATEGY - MNI

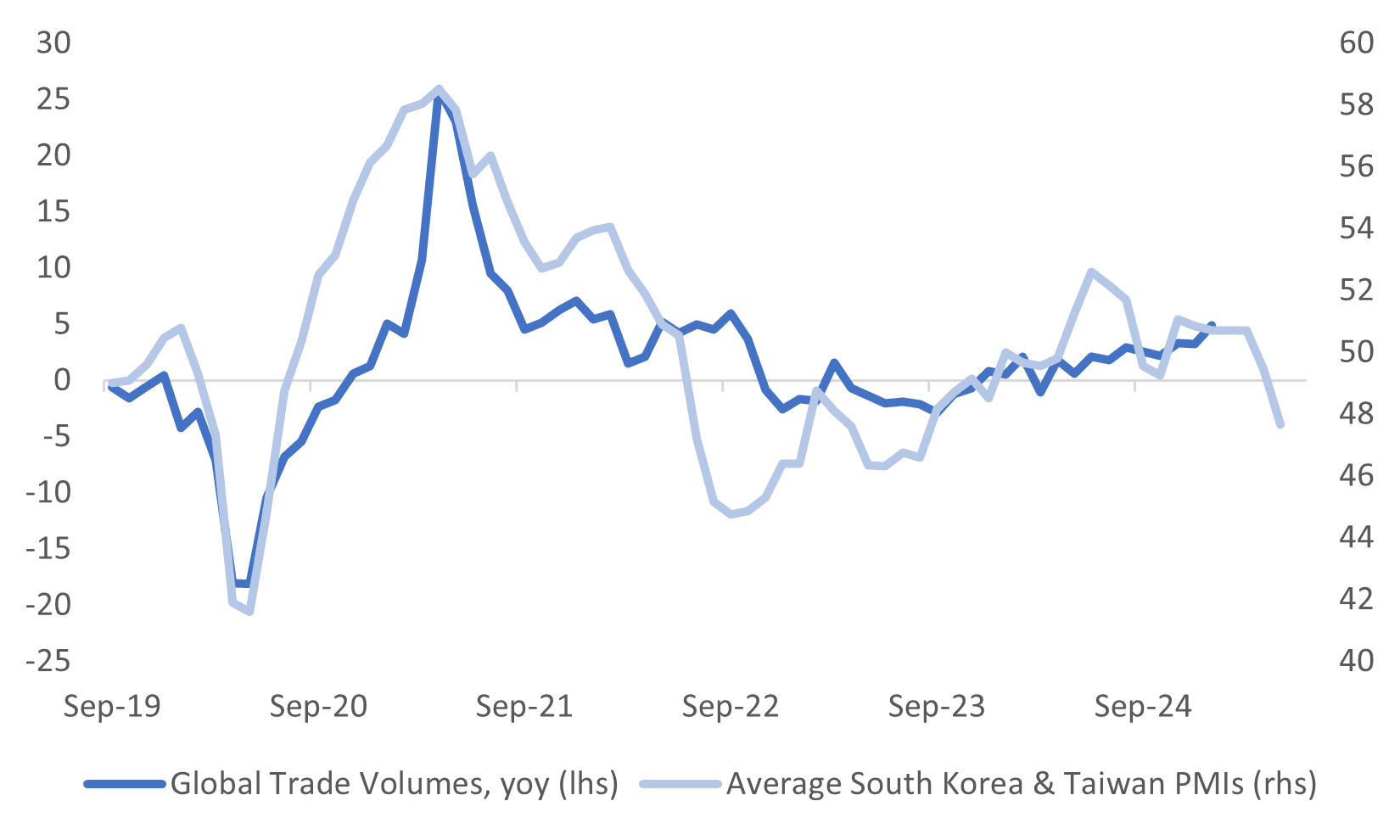

Fig 1: South Korea, Taiwan PMIs Point To Slower Global Trade Growth

Source: MNI - Market News/Bloomberg

UK

POLITICS (RTRS): "Britain's right-wing Reform UK party made early gains in local election results on Friday and was ahead by just four votes in a battle for a seat in parliament in the first major electoral test since last year's general election."

EU

US/EU (BBG): “The Trump administration sees its resource deal with Ukraine as a model for further international agreements, reflecting the president’s strategy of using Washington’s foreign policy heft to secure assets and investment returns overseas.”

ROMANIA (BBG): "Romania faces a prolonged period of elevated funding costs as a contentious presidential election risks further delaying steps to curb the European Union’s widest budget deficit."

US

FX (MNI INTERVIEW): Policies such as a potential Mar-a-Lago currency accord between the U.S. and China or forcing foreign holders of Treasuries to extend the maturity of their holdings are expressly not on the Trump administration’s agenda, Stephen Miran, Chair of the White House Council of Economic Advisers, told MNI Thursday.

ECONOMY (MNI INTERVIEW): The U.S. economy is unlikely to slip into recession this year and trade deals should soon rekindle animal spirits, though some volatility in growth and inflation figures is to be expected given President Donald Trump’s expansive policy agenda, Stephen Miran, Chair of the White House Council of Economic Advisers, told MNI.

ISM (MNI INTERVIEW): Unreliable Trump Stings US Factories, ISM Says

NATIONAL SECURITY (RTRS): “U.S. President Donald Trump ousted his national security adviser Mike Waltz on Thursday and named Secretary of State Marco Rubio as his interim replacement in the first major shakeup of Trump's inner circle since he took office in January.”

FISCAL (WSJ): “President Trump is expected to propose far-reaching cuts to federal environmental, renewable energy, education and foreign-aid programs in a budget blueprint that slashes nondefense discretionary spending by more than $160 billion, according to administration officials.”

IRAN (BBG): “ President Donald Trump said he would impose secondary sanctions on nations or companies buying Iranian oil, ratcheting up pressure on Tehran as nuclear talks with the US hit a snag.”

APPLE (RTRS): “Apple on Thursday trimmed its share buyback program by $10 billion, with CEO Tim Cook telling analysts that tariffs could add about $900 million in costs this quarter as the iPhone maker shifts its vast supply chain to minimize the impact of President Donald Trump's trade war.”

OTHER

JAPAN (RTRS): “Japan's huge $1 trillion-plus in U.S. Treasury holdings are among the tools available for Tokyo to use in trade negotiations with the United States, Japanese Finance Minister Katsunobu Kato said on Friday.”

JAPAN (BBG): “Japan aims to achieve a trade agreement with the US in June, with the high-stakes bilateral discussions expected to gain momentum in mid-May, Tokyo’s chief negotiator said after concluding the latest round of talks in Washington.”

CANADA (MNI INTERVIEW): Carney Quebec Gain Boosts Pipeline Odds- Surkes

AUSTRALIA (MNI): MNI discusses the RBA cash rate strategy. On MNI Policy MainWire now, for more details please contact sales@marketnews.com.

SOUTH KOREA (RTRS): “South Korea's former acting President Han Duck-soo said on Friday he would join the race to become the country's next president after resigning the day before.”

CHINA

CHINA/US (RTRS): “The United States has approached China to seek talks over President Donald Trump's 145% tariffs and Beijing's door is open for discussions, China's Commerce Ministry said on Friday, signalling a potential de-escalation in the trade war. The U.S. should be prepared to take action in correcting "erroneous" practices and cancel unilateral tariffs, the commerce ministry said in a statement, adding that Washington needs to show "sincerity" in negotiations.”

MARKET DATA

NEW ZEALAND MAR BUILDING PERMITS M/M 9.6%; PRIOR 0.7%

AUSTRALIA MAR RETAIL SALES 0.3%; MEDIAN 0.4%; PRIOR 0.2%

AUSTRALIA Q1 RETAIL SALES VOLUMES Q/Q 0.0%; MEDIAN 0.3%; PRIOR 0.8%

AUSTRALIA Q1 PPI Q/Q 0.9%; PRIOR 0.8%

AUSTRALIA Q1 PPI Y/Y 3.7%; PRIOR 3.7%

JAPAN MAR JOBLESS RATE 2.5%; MEDIAN 2.4%; PRIOR 2.4%

JAPAN MAR JOB-TO-APPLICANT RATE 1.26; MEDIAN 1.25; PRIOR 1.24

JAPAN APR MONETARY BASE Y/Y-4.8; PRIOR -3.1%

SOUTH KOREA APR CPI M/M 0.1%; MEDIAN 0.1%; PRIOR 0.2%

SOUTH KOREA APR CPI Y/Y 2.1%; MEDIAN 2.0%; PRIOR 2.1%

SOUTH KOREA APR CPI EX FOOD AND ENERGY Y/Y 2.1%; MEDIAN 1.9%; PRIOR 1.9%

SOUTH KOREA APR S&P PMI MFG 47.5; PRIOR 49.1

MARKETS

US TSYS: Asia Wrap - Yields A Little Higher

TYM5 has traded a little lower within a range of 111-23+ to 112-01 during the Asia-Pacific session. It last changed hands at 111-26, down 0-01 from the previous close.

- The US 10-year yield is a little higher, dealing around 4.23%, up from its close around 4.21%.

- The US 2-year yield is a little higher, dealing around 3.71%, up from its close around 3.698%

- “Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials including Treasury Secretary Scott Bessent was “positive and constructive.”(per BBG)

- BBG noted: "China's Commerce Ministry said in a Friday statement that it had noted senior US officials repeatedly expressing their willingness to talk to Beijing about tariffs.

- NFP tonight will dictate price action further, with a wide distribution in the survey. There are calls for as low as 50k and some as high as 170k. The consensus seems to be around 138k.

- The 10-year Yield has bounced nicely off its first support around 4.10%. Resistance is seen towards 4.30% and we should see buyers remerge there initially. Range seems to be 4.10% - 4.45%, with the pivot the 4.25/30 area for now.

- Data/Events : US NFP

JGBS: Cheaper, Trade Deal HLs In Focus, Market Closed On Mon & Tues

JGB futures are slightly higher, +5 compared to settlement levels.

- While the domestic calendar delivered labour market, monetary base and international investment flow data, it was news on trade deals that appeared to dominate the market’s attention.

- "Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials, including Treasury Secretary Scott Bessent, were "positive and constructive."(per BBG).

- There was also positive US-China trade news, with headlines that China is considering trade talks with the US (which came from the China Ministry of Commerce).

- Cash US tsys are 1-2bps cheaper in today’s Asia-Pac session. US NFP will dictate price action tonight.

- Cash JGBs are 1bp richer to 5bps cheaper across benchmarks, with a steepening bias.

- Swap rates are 1bp lower to 2bps higher. Swap spreads are mixed.

- The local market is closed on Monday and Tuesday.

AUSSIE BONDS: Cheaper After Some Positive Trade Deal HLs, US NFP Due

ACGBs (YM -3.0 & XM -4.0) are cheaper but near session bests.

- While PPI and retail sales offered some domestic insights, it was offshore developments that dominated local market attention.

- In addition to positive US-China trade headlines, there were some positive trade deal comments from Japan, "Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials, including Treasury Secretary Scott Bessent, were "positive and constructive."(per BBG).

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session. US NFP will dictate price action tonight.

- Cash ACGBs are 3bps cheaper with the AU-US 10-year yield differential at -1bp.

- The bills strip -2 to -5 across contracts, with a steepening bias

- RBA-dated OIS pricing is flat to 3bps firmer across meetings today, with late 2025 leading. A 50bp rate cut in May is given a 3% probability, with a cumulative 110bps of easing priced by year-end.

- On Monday, the local calendar will see S&P Global PMI Composite & Services, Melbourne Institute Inflation and ANZ-Indeed Job Advertisements.

- Next week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 3.75% 21 April 2037 bond on Wednesday and A$700mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: NZGBS: Closed With A Twist-Flattener After Trade HL-Induced Volatility

NZGBs closed showing a twist-flattener, with benchmark yields 1bp higher to 2bps lower, after a volatile pre-US payrolls session. NZGBs had 7-8bp ranges.

- The Asian session has seen risk trade well as the market attempts to look through the negative earnings of Apple and Amazon to concentrate on some positive US-China trade headlines. As well as some positive trade deal comments from Japan, "Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials, including Treasury Secretary Scott Bessent, were "positive and constructive."(per BBG).

- Cash US tsys are 1-3bps cheaper in today’s Asia-Pac session. US NFP will dictate price action tonight.

- Swap rates closed 1-2bps higher.

- RBNZ dated OIS pricing closed flat to 4bps firmer across meetings, with early-2026 leading. 26bps of easing is priced for May, with a cumulative 78bps by November 2025.

- The local calendar will be on Monday, ahead of ANZ commodity prices on Tuesday. The data highlight, however, is likely to be the Q1 Employment Report.

FOREX: G10 Wrap - Can The USD follow through?

The BBDXY has had an Asian range of 1225.86 - 1231.01, Asia is currently trading around 1226. The USD has given back some overnight gains as China made comments interpreted as being open to potentially explore trade talks with the US. Bloomberg - “The EU may buy more gas and agricultural products from the US to address the trade imbalance, the FT reported, citing the bloc’s Trade Commissioner Maros Sefcovic.” Reuters - “ Ryanair threatens to cancel huge Boeing order if tariffs raise prices.”

- EUR/USD - Asian range 1.1274 - 1.1316, Asia is currently trading 1.1305. Intra-day support is around the 1.1250 area, should this area not hold demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3274 - 1.3314, Asia is currently dealing around 1.3305. Intra-day support is around the 1.3250 area, then the pivotal 1.30/31 support is next.

- USD/JPY - Asian range 145.15 - 145.92, has drifted sideways for most of the Asia session. USD/JPY broke the 144.00 resistance yesterday and has quickly moved to the next level of resistance. The 145.50/1.4700 area should be tough to get through initially, watch price action around this crucial area as the bears try to wrest control back once more.

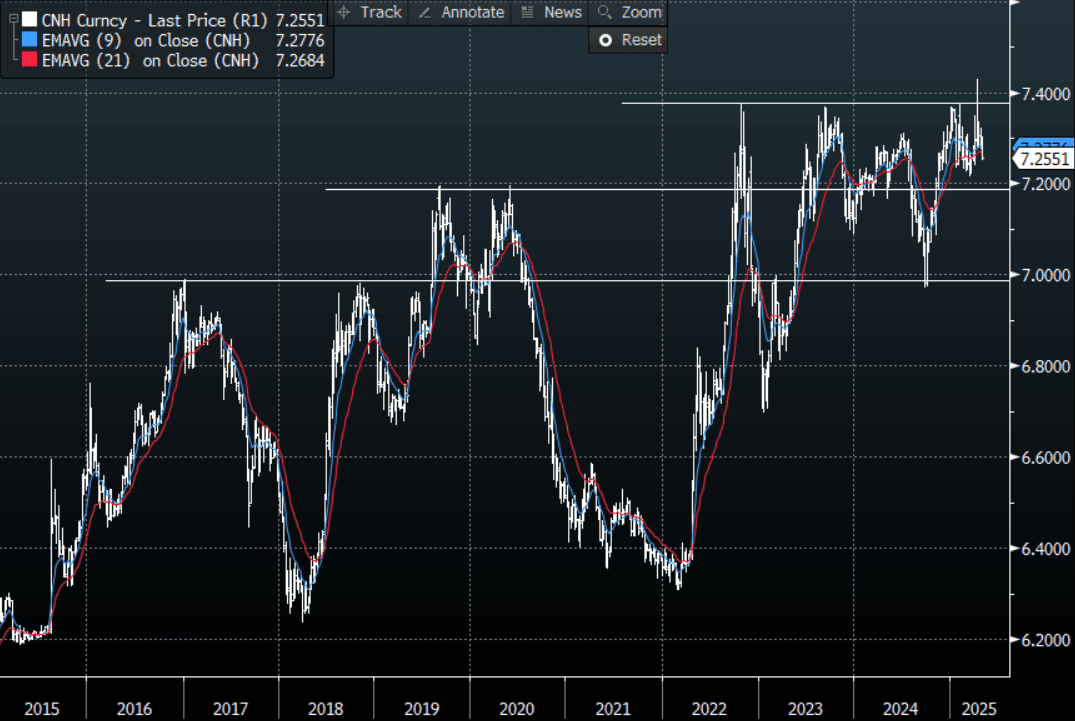

- USD/CNH - Asian range 7.2518 - 7.2808, Chinese stock markets are shut for a holiday. The longs in Usd/Asia are starting to be pared back, this was perceived to be the cleanest expression of the Tariff trade but this move lower in the USD is now starting to bite.

- Cross asset : SPX +0.81%, Gold $3254, US 10-Year yield 4.23%, BBDXY 1226, Crude oil $59.69.

- Data/Events : Dutch CPI, IT Unemployment, US NFP

Fig 1: USD/CNH Spot Weekly Chart

Source: MNI - Market News/Bloomberg

FOREX: Antipodean Wrap - AUD & NZD Continue To Outperform

The Asian session has seen risk trade well this morning as the market attempts to look through the negative earnings of Apple and Amazon to concentrate on some positive US-China trade headlines. As well as some positive trade deal comments from Japan, “Japanese Prime Minister Shigeru Ishiba says he was told the second round of tariff talks between his chief negotiator Ryosei Akazawa and US officials including Treasury Secretary Scott Bessent was “positive and constructive.”(per BBG). NFP will dictate price action tonight.

- AUD/USD - Asian range 0.6375 - 0.6420, the AUD is currently dealing around 0.6415. While the support around 0.6350 holds the focus will be on building upward momentum. The AUD looks to be building a solid base from which to move higher again, first target the 0.6600 area.

- AUD/JPY - Asian range 92.64 - 93.48, price goes into London trading around 93.20. AUD/JPY broke the resistance around 92.00 yesterday and has had a powerful extension as shorts are pared back, short term this move could have more to go. Weekly resistance seen between 94.00/96.00 should see sellers remerge.

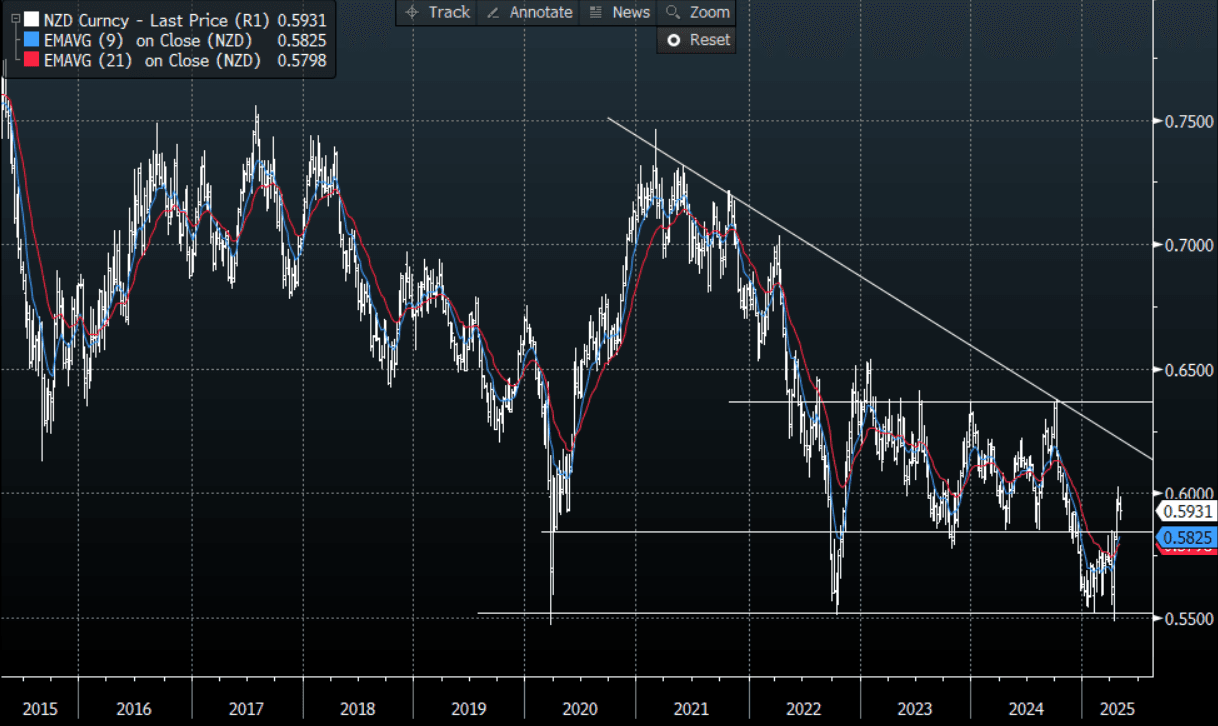

- NZDUSD - Asian range 0.5894 - 0.5938, going into London trading around 0.5930. With support having held once more around 0.5900, a move above 0.5950 could see the move higher build momentum again.

- AUD/NZD - Asian range 1.0785 - 1.0823, the Asian session currently trading 1.0810. Sellers could be expected again back towards the 1.0850 area.

Fig 1 : NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Strong Day as Trade Agreements Rumours Evolve

With China out today, equity markets remained quiet despite the ongoing headlines that China's Commerce Ministry said it is evaluating the possibility of trade talks with the US, after senior US officials expressed willingness to talk to Beijing about tariffs. Despite the comments the ministry was still demanding that the US show sincerity towards China and its wrong practices; suggesting that the chances of Beijing bowing to Washington’s pressure remains low.

Markets were buoyed by the news and mainly green could be viewed across trading screens with gains in all major markets.

- Taiwan’s TAIEX was the best performer up +2.2% and on track to finish over 4% higher for the week, an 18% gain since the low on 09 April.

- The KOSPI had a positive day, rising +0.32% to take back yesterday’s losses and remain on track to finish the shortened week with a +0.75% gain.

- As Malaysia prepares for a rate decision next week, weaker PMIs weighed heavy on the FTSE Bursa Malay KLCI which was one of the few markets to fall. Down -0.15% for the day, it remains over +1.5% higher for the week.

- In Indonesia the Jakarta Composite has been on a tear of late and despite weak PMIs is up +0.35% today and over +1.5% for the week to deliver its third successive positive week and be 13% higher than the lows of 09 April.

- Singapore’s Straits Times gained +0.30% and the PSEi in the Philippines over 1% gain.

- India’s NIFTY 50 is up +0.88% today as news circulates that India could be one of the first to finalize their trade deal. The index is on track to deliver a 2% gain this week for three successive weeks of gains.

Oil Set for Another Big Weekly Drop (UPDATED)

- Oil had its strongest day of the week as WTI rose as further threats of Iranian sanctions permeated through oil markets.

- Trump stated clearly that the US will sanction any nation or person who buys oil or petrochemicals from Iran in breach of sanctions driving prices higher.

- Additionally, a prominent US Senator and known supporter of Trump has stated publicly that he has the commitment of 72 colleagues on a bill to further sanction Russia and those countries that continue to source their oil from the Kremlin.

- These threats added to the news overnight that April OPEC+ production fell by 200,000 barrels a day due to the winding down of operations in Venezuela by US producers as the threat of increased sanctions gets closer.

- US crude inventories declined by 2.7 million barrels, the biggest fall in more than a month, to around 440.4 million barrels. Refineries processed the most crude since 2019 for this time of year, with oil processing improving in all regions except the Midwest. Gasoline inventories saw a 4 million-barrel decline, driven by a large drawdown in the Midwest, to the lowest since late December.

- In a move that would add more supply to the global outlook, House Republicans plan to raise more than $15 billion in revenue through increasing US oil, gas and coal lease sales, as well as other measures, to help pay for President Donald Trump’s massive tax cut package, according BBG

- WTI finished the US trading session at US58.98 bbl yet has opened in the Asia trading day lower initially before rallying back in the afternoon to be +1.1% better

- Despite today’s gains, WTI is set for a decline of over 5% for the week.

- Brent had opened in the Asia trading session at $61.82 and climbed steadily throughout the trading day to reach $62.52, a gain of 1%.

- Despite the gain, Brent is on track for a loss of over 6% for the week.

Gold Set for Biggest Drop Since February

- Gold’s overnight fall tempered in Asia as markets assessed the latest headlines on trade negotiations.

- Having exhibited ‘safe-haven’ status in recent months as tariff headlines buffeted markets, gold had risen at one point 27% year to date.

- It is now more than 5% off its April high of US$3,423.98 and opened the Asia trading data at $3,239.21 having lost -1.50% yesterday.

- Gold managed gains today up +0.51 yet is down over 1.9% for the week at $3,255.91.

- The move overnight sees gold trade below the 20-day EMA of $3,246.90 with the next key technical level the 50-day EMA at $3,115.31

- Gold remains up over 20% this year on trade war concerns and renewed support by Central Banks.

- For gold, the key focus now will likely return to interest rates and the next FED decision as tonight sees the release of the Non-Farm Payrolls.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 02/05/2025 | 0630/0730 | DMO to announce details of long syndication for W/C 19 May | ||

| 02/05/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0745/0945 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0750/0950 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0755/0955 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (f) | |

| 02/05/2025 | 0900/1100 | *** | HICP (p) | |

| 02/05/2025 | 0900/1100 | ** | Unemployment | |

| 02/05/2025 | 1230/0830 | *** | Employment Report | |

| 02/05/2025 | 1400/1000 | ** | Factory New Orders | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 02/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |