MNI EUROPEAN MARKETS ANALYSIS: Yen Aided By Equity Dip

- The RBA kept rates on hold, as expected, and sounded cautious on the rate cutting outlook, with the policy rate close to neutral.

- AUD/USD is still weaker, although outperforming NZD marginally. US equity futures are striking a risk off tone, which is helping yen rally. We also had fresh FX jawboning from the FinMin in Japan. US Tsy futures have drifted higher.

- Later the Fed’s Bowman speaks on supervision and monetary policy, ECB President Lagarde and BoE’s Breeden also appear. US data releases scheduled for today are likely to be delayed by the ongoing government shutdown.

MARKETS

US TSYS: Treasuries Look to QTRLY Borrowing Estimates for Next Catalyst

US bond futures didn't get out of bed today, with the 10-Yr where it started at 112-21+ to remain at the mid-point of the 50-day EMA and the 100-day EMA. With economic data releases still constrained by the government shutdown, bonds will look to the release this week of the maturity breakdown for funding going forward into 2026. Current expectations are for a significant increase in bill issuance that should create increased demand for longer bonds, thus bring yields down and lowering the interest cost for the government.

Cash was quiet from the open also inching lower in yield after last night's rise with all maturities around 0.5bps lower in yield.

- The 2-Yr is marginally lower at 3.60%.

- The 5-Yr is at 3.71%

- The 10-Yr is steady at 4.10%

- The 30-Yr is -0.5bps lower at 4.68%

Tonight's focus for issuance will continue to come from corporates, where the blockbuster start to the month is set to continue. For USTs the focus will be US$95bn 6-week bills

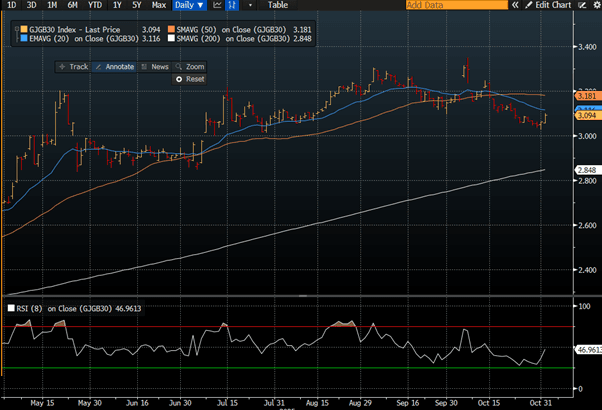

JGBS: Curve Steepens Ahead Of Tomorrow's 10Y Supply

JGB futures are weaker and at session lows, -20 compared to the settlement levels.

- “Japanese Prime Minister Sanae Takaichi will put together the nation’s new growth strategy by next summer, while pledging to boost tax revenues without increasing taxation rates." - BBG

- MNI Brief: Japan’s economy is expected to have contracted for the first time in six quarters in the July-September period, as weaker private consumption and capital investment offset earlier front-loaded gains, according to private economists. Preliminary estimates suggest GDP fell 0.7% quarter-on-quarter, or an annualised 2.7%, reversing from a 0.5% q/q (annualised 2.2%) expansion in the April-June quarter.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off.

- Cash JGBs are flat to 3bps cheaper across benchmarks, with the 30-year underperforming. The benchmark 30-year yield is at 3.094% versus the cycle high of 3.35%. The near-term technical bias, however, appears lower. (see chart)

- Swap rates are 1-4bps higher, with a steepening bias.

- Following last week's policy decision, BoJ-dated OIS pricing is softer across late 2025/early 2026 meetings compared to early August levels, but slightly firmer for mid to late 2026 meetings.

- Tomorrow, the local calendar will see BOJ Minutes (Sep MPM) and Monetary base data alongside 10-year supply.

Source: Bloomberg Finance LP

RBA: Keeping Options Open, Main Concern To Get Inflation Back In Band

The Board only considered keeping rates at 3.6% at its November meeting as well as discussing its strategy going forward. Governor Bullock observed that the Board thinks it is “pretty close to neutral”, which makes it difficult to assess the level of policy restrictiveness, and thus it doesn’t have a bias, which is consistent with its discussion around holding. She said that data will continue to drive its outlook and the Board will decide policy on a “meeting-by-meeting basis” with all directions in rates possible.

- The jump in underlying inflation in Q3 was partly due to temporary factors, such as council rates, travel & fuel, but also because of more persistent items, such as dwelling costs & market services, which may be signalling that demand is exceeding supply. While the trimmed mean is expected to remain above 3% over the next year, the RBA is forecasting the quarterly increases to moderate.

- Both inflation and unemployment rose more than the bank expected, and as there is information in both, the Board remains cautious and a bit more concerned about getting inflation back in the band.

- Bullock noted that labour market forward indicators suggest that conditions are more stable than the September unemployment rate suggested and for now are likely to stay steady. ULC growth is also rising quickly. The Board is alert to risks in both directions.

- She reiterated that rates didn’t rise as much in Australia as in other countries, therefore it is likely that it won’t need to cut as much either. For now, the Board believes it is where it needs to be and is in a position to respond to both upside and downside risks.

RBA: Inflation Persistence Needs To Abate, Only One Cut Assumed In Forecasts

The RBA left rates at 3.6% as was widely expected but it revised up its trimmed mean forecasts to a peak of 3.2% in both Q4 2025 and Q2 2026 up from 2.6% in August. The main change to the statement was also around the “materially higher” Q3 inflation print and “recent evidence of more persistent inflation” but risks were said to be “in both directions”. The Board didn’t seem concerned about softness in the September labour market data. While inflation is assessed as “persistent” and expected to be above the top of the band, rates are likely on hold.

- Underlying inflation is projected to return to the band by Q4 2026 but the 2.5% mid-point is no longer in the forecast but as Governor Bullock previously said the further out a forecast is, the greater the uncertainty. Headline was revised up 0.3pp to 3.3% for Q4 and 0.6pp to 3.7% in Q2 2026 and is within the band in 2027.

- Inflation returns to the band using a higher rate assumption that has only one 25bp cut for H1 2026 down from 75bp assumed in August. Another sign that for now policy is on hold at “a little restrictive”.

- In September, labour market conditions were overall “stable”, whereas this month they appeared “a little tight” at the statement end, despite the 0.2pp rise in the last unemployment read. It also noted that surveys and liaison suggest “a significant share of firms are experiencing difficulty sourcing labour”. While the unemployment rate path was revised up 0.1pp to 4.4%, the Board doesn’t sound concerned.

- The growth outlook is little changed with Q4 2025 revised up 0.3pp to 2% but the rest of the path similar to August. Q4 consumption is 0.3pp higher at 2.1% supported by a lower savings rate and slightly stronger wage growth but higher inflation reduces real disposable income gains.

AUSSIE BONDS: Market Cheapens As Gov Bullock Delivers A Hawkish Tone

ACGBs (YM -4.5 & XM -2.5) cheapen during RBA Gov Bullock’s presser.

- RBA Governor Michele Bullock said the labour market remains slightly tight relative to full employment and that the Board did not consider cutting or raising rates at its latest meeting, opting instead to hold and review its strategy. She noted that while both inflation and unemployment have risen, the Board is more concerned about inflation, with core inflation above 3% considered “not ideal.”

- Bullock added that the RBA may not need to cut rates much further.

- She dismissed concerns about stagflation.

- Overall, her comments carried a slightly hawkish tone.

- Cash US tsys are slightly richer in today's Asia-Pac session after yesterday's modest sell-off

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +25bps.

- The bills strip is -3 to -6 across contracts.

- RBA-dated OIS pricing had implied just a 3% probability of a move today. As it currently stands, the OIS market has a 75% chance of a 25bp cut by mid-2026.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Wednesday and A$800mn of the 3.00% 21 November 2033 bond on Friday.

- Tomorrow, the local calendar will see S&P Global Composite & Services PMIs.

BONDS: NZGBS: Steady Ahead Of Labour Mkt & Wages Data

NZGBs closed little changed across benchmarks after a subdued session.

- Tomorrow sees the key event of the week’s calendar with the release of Q3 labour market and wages data.

- Filled jobs for the quarter signal a stabilisation, but employment is likely to have remained weak, with consensus forecasting it to rise only 0.1% q/q to be still down 0.2% y/y. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ's August projections. Soft labour demand is likely to weigh on private wage growth, which is forecast to rise around 0.4% q/q after 0.6%.

- Swap rates are little changed. The 2-year rate is holding its recent rise, bouncing off channel support, after reaching extreme overbought conditions. (see chart)

- RBNZ dated OIS pricing is little changed across meetings. 24bps of easing is priced for November, with a cumulative 31bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 5.00% May-54 bond.

Bloomberg Finance LP

NEW ZEALAND: Significantly Weaker Jobs Data Could Increase Easing Expectations

Q3 jobs and wages data are released Wednesday and with spare capacity an important driver of monetary easing, will be monitored closely as there has been excess supply in the labour market. Monthly data in the quarter signal there was a stabilization but employment is likely to have remained soft. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ’s August projections. A 25bp cut on 26 November is generally expected but if the labour data print significantly weaker, then expectations of 50bp may increase.

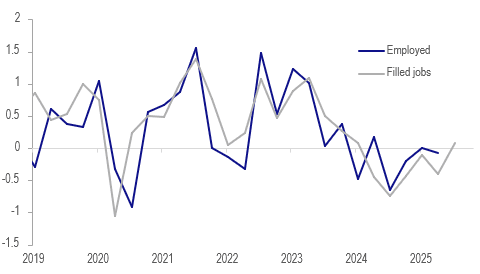

- Q3 filled jobs, vacancy and survey data all point to a stabilisation in NZ’s labour market. Average filled jobs rose 0.1% q/q after falling 0.4% in Q2.

NZ filled jobs vs employment q/q%

Source: MNI - Market News/Statistics NZ/LSEG

- In its August projections, the RBNZ forecast flat Q3 employment growth leaving the annual rate down 0.3%. It also expected private wage growth to moderate to 0.4% q/q from Q2’s 0.6%.

- Bloomberg consensus is forecasting employment to rise only 0.1% q/q and still be down 0.2% y/y with expectations in a fairly narrow range of -0.1% to +0.3% q/q. ASB, Kiwibank and Westpac are below consensus but in line with the RBNZ projecting flat jobs growth in Q3, while BNZ is at +0.1% q/q and ANZ +0.2% q/q.

- Forecasts for the unemployment rate are between 5.2% and 5.4% with ANZ, BNZ, Kiwibank and Westpac all expecting 5.3% but ASB is steady at 5.2%.

- Soft labour demand is likely weighing on private wage growth which is forecast to rise around 0.4% q/q after 0.6%. ASB, BNZ and Kiwibank are all in line with consensus, while ANZ and Westpac expect 0.5%.

FOREX: Asia-Pac FX: The USD Continues To Grind Higher, Testing Resistance

The BBDXY has had a range today of 1221.38 - 1223.25 in the Asia-Pac session; it is currently trading around 1222, +0.10%. The USD continues to build on its recent gains eking out new highs every day. The 1220-30 area remains tough resistance, only a sustained close back above 1230 would start to challenge the conviction of the longer-term USD shorts. Risk/Reward does still favour fading this moving initially but the price action is starting to look more constructive as higher lows are being made on the Daily chart through October. A sustained move back above 1230 would potentially signal a medium term low is in place and a deeper pullback is on the cards.

- EUR/USD - Asian range 1.1498 - 1.1523, Asia is currently trading 1.1515. The pair has moved back toward its support just above 1.1500. A break under this support could signal a deeper correction, first target 1.1400 and then the 1.1100/1.1200 area.

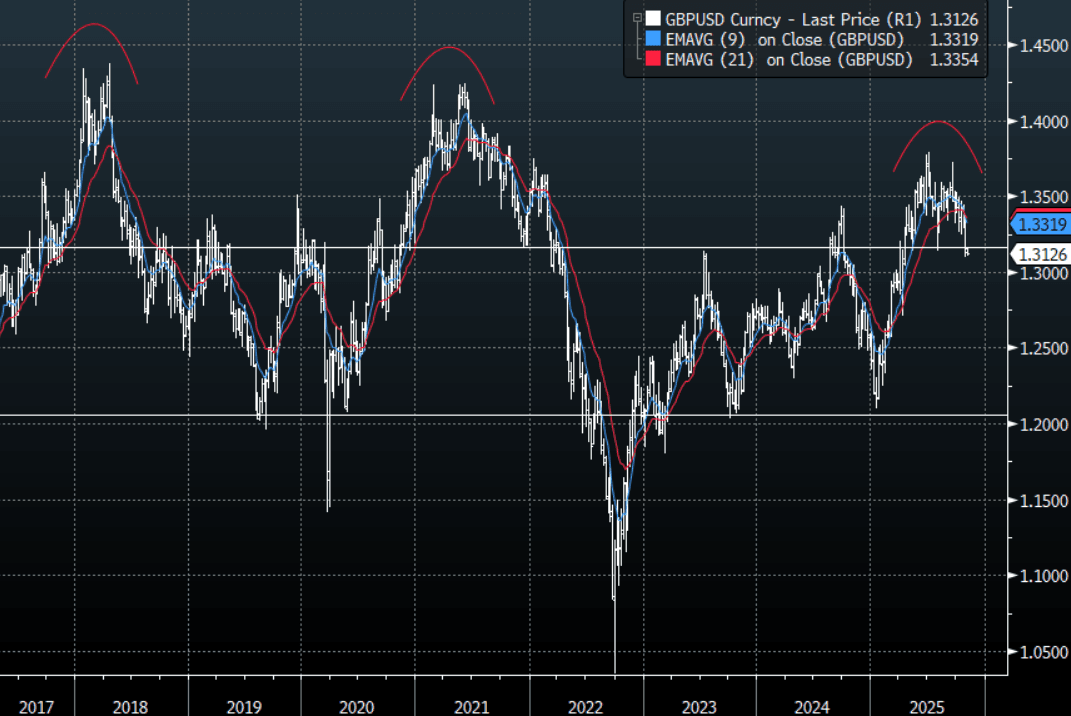

- GBP/USD - Asian range 1.3118 - 1.3162, Asia is currently dealing around 1.3125. The pair looks to be building some downward momentum. This 1.3100/1.3150 area has proved to be supportive on more than 1 occasion this year so some work around this level could be expected. I continue to favor fading rallies though as GBP attempts to put in a medium term top.

- Cross asset : SPX -0.45%, Gold $3988, US 10-Year 4.1050%, BBDXY 1222, Crude Oil $60.90

- Data/Events : Italy New Car Registrations YoY, France Budget Balance YTD, Spain Unemployment Change

Fig 1: GBP/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

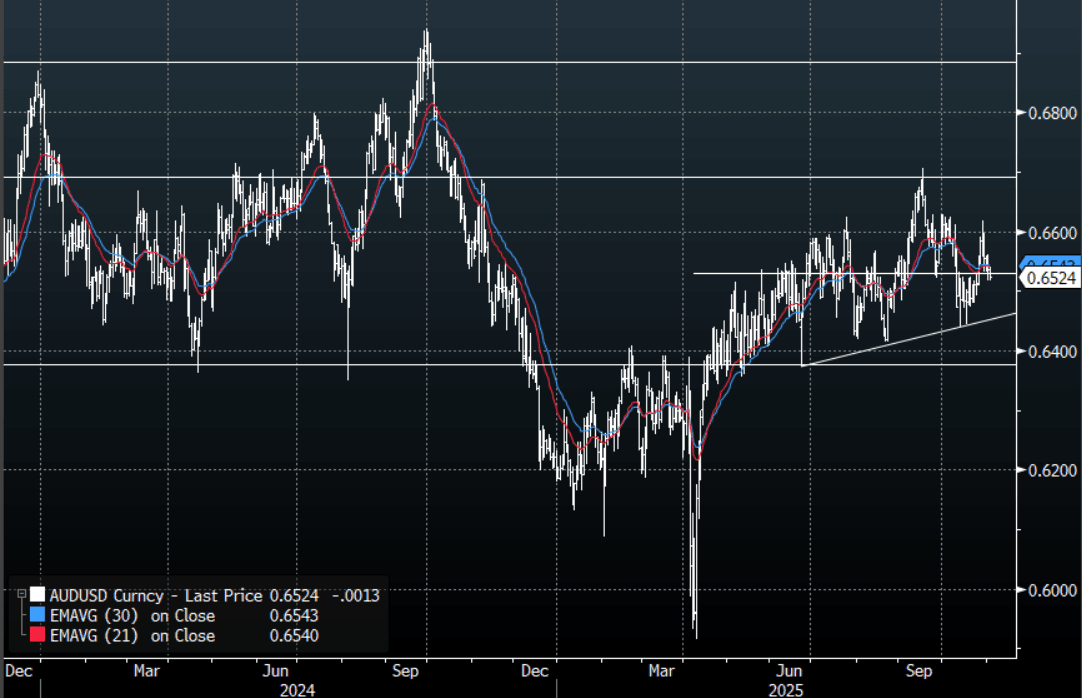

AUD: Asia-Pac - AUD/USD Drifts Lower After RBA

The AUD/USD has had a range today of 0.6518 - 0.6541 in the Asia- Pac session, it is currently trading around 0.6525, -0.20%. The RBA held rates and the AUD/USD slipped a few spreads lower with the market perhaps looking for a more hawkish RBA. The AUD/USD is firmly back within its recent 0.6400-0.6650 range with the pivot between 0.6500-0.6550 finding some demand first up.

- The RBA is clearly still concerned with inflation and the data going forward now will be critical as this line in the statement suggests. "Given this, and the recent evidence of more persistent inflation, the Board judged that it was appropriate to remain cautious, updating its view of the outlook as the data evolve."

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6625(AUD 944m). Upcoming Close Strikes : 0.6500(AUD822m Nov 7), 0.6600(AUD682m Nov 7) - BBG

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

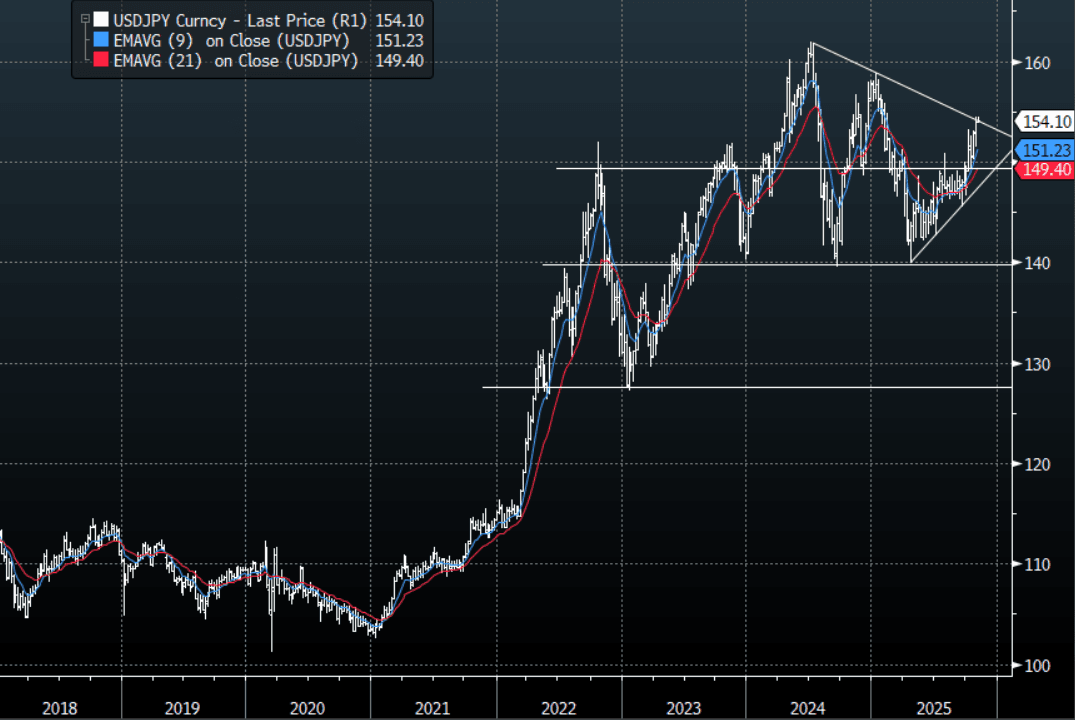

JPY: Asia-Pac: USD/JPY - Official Jaw-Boning Sees It Pull Back To 154.00

The USD/JPY range today has been 154.06 - 154.48 in the Asia-Pac session, it is currently trading around 154.10, +0.05%. The pair remains well supported thanks to a combination of a hawkish FED and a BOJ that is still unsure about when it will raise rates. We are testing some resistance around the 154/155 area and I would expect we might to do some work around here initially. A sustained break back above 155 could see the move begin to accelerate and with that the potential for a new round of intervention, though personally I think they will wait for levels closer to 160 to get involved. Look for dips to continue to be supported while above 149-150, the first buy zone is back toward the 152.00 area.

- Yen comments by the FinMin today show FX remains a close watch point for the authorities. Still, based on historical remarks, the comments suggest concern, but not yet suggesting intervention is imminent.

- Options : Close significant option expiries for NY cut, based on DTCC data: 152.50($1.42b). Upcoming Close Strikes : 150.00($1.13b Nov 3) - BBG.

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

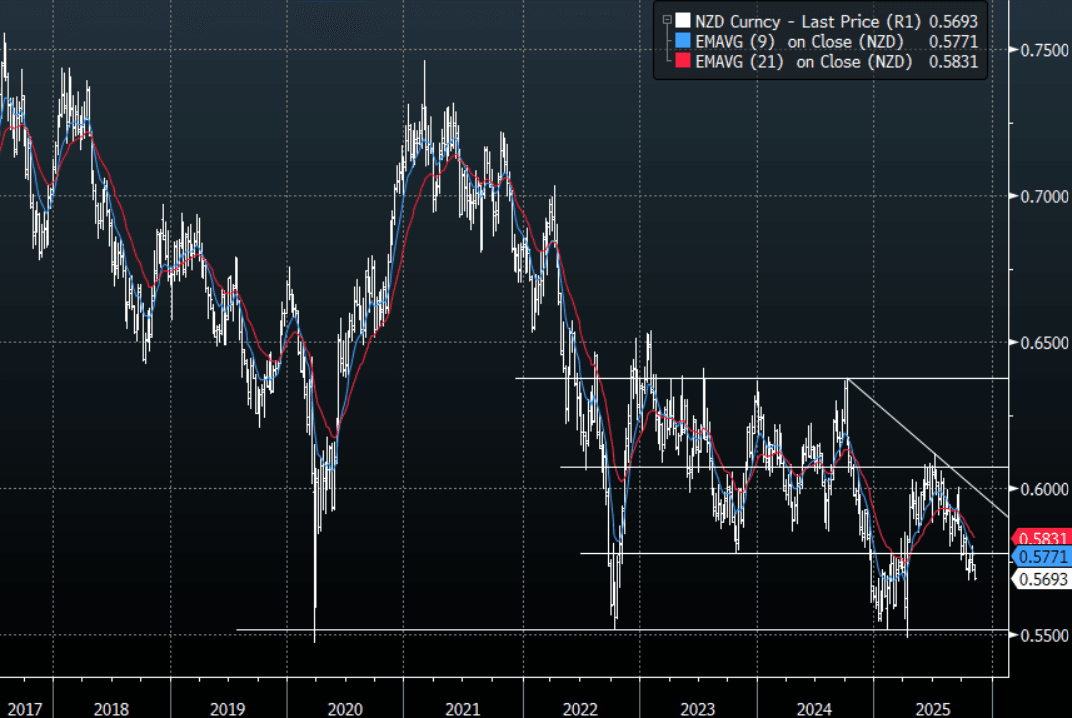

NZD: Asia-Pac: NZD/USD Trades Heavy Breaking Below Overnight Lows

The NZD/USD had a range of 0.5686 - 0.5710 in the Asia-Pac session, going into the London open trading around 0.5695, -0.25%. The NZD has slipped lower and remained under pressure for most of our session. While price remains below the 0.5800/50 area I suspect rallies continue to be faded looking for a potential move back towards the 0.5500/0.5600 area. NZD continues to stand out as a short against a resurgent USD but it is worth noting that because of the size of the market the market can very quickly become all positioned the same way, so I think the USD will need to break above its pivotal resistance for the NZD to test those lows. That being said, a poor unemployment print tomorrow in New Zealand would certainly give it another nudge.

- MNI AU - Significantly Weaker Jobs Data Could Increase Easing Expectations: Q3 jobs and wages data are released Wednesday and with spare capacity an important driver of monetary easing, will be monitored closely as there has been excess supply in the labour market. Monthly data in the quarter signal there was a stabilization but employment is likely to have remained soft. The unemployment rate is expected to rise 0.1pp to 5.3%, in line with the RBNZ’s August projections. A 25bp cut on 26 November is generally expected but if the labour data print significantly weaker, then expectations of 50bp may increase.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5650(NZD1.1b Nov 5), 0.5675(NZD1.05b Nov 5), 0.5750(NZD604m Nov 5) - BBG

Fig 1: NZD/USD Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

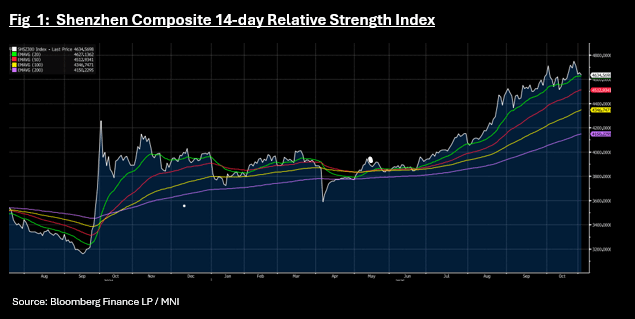

ASIA STOCKS: Nikkei / KOSPI in Rare Down Day as CSI Approaches Key Tech Level

In a day where stock specific news was muted, a pull back occurred for major bourses which for some was the first in several days. Whilst tech stocks are still underwriting the positive momentum in Asia, a minor pullback was due. The DOW finished modestly down and with futures pointing down also, most major bourses opened on the back foot. The KOSPI's fall can also be attributed to the unusual occurrence that occurred overnight with the Korea Exchange issuing an 'investment caution' over SK Hynix shares. SK Hynix are up over 280% from their lows this year. The warning sees the company's shares down 6% today, with Samsung down -3.5%.

- The KOSPI was the biggest faller today, with losses of -1.90%, the biggest one day fall since September. It does little to change the technical backdrop with the KOSPI remaining above all major moving averages, and overbought on the 14-day Relative Strength Index.

- The NIKKEI's fall of -0.50% does little to impact the technical backdrop for the index. All major moving averages are steep in their upward slope, an indicator that the positive momentum remains.

- China's major bourses are again inversely correlated with the Hang Seng up modestly by +0.20%, whilst the CSI 300 is down -0.40%, Shanghai down -0.19% and Shenzhen down -1.09%. Shenzhen's technical pullback mirrors that of the CSI 300 as they both near their 20-day EMA.

- SE Asia's major bourses are mixed with the JCI up +0.27%, FTSE Malay up +0.15% whilst the SE Thai is down -0.38% for its fourth day of falls as it nears its 20-day EMA.

OIL: Crude In Narrow Range As Looks For Direction, US Stock Data Out Tuesday

Oil prices have trended lower during today’s session consistent with their recent tendency to range trade. Geopolitical factors, such as sanctions & Ukrainian strikes, have supported them, while reports of elevated levels of oil at sea are fuelling excess supply concerns. OPEC’s decision to pause output increases in Q1 was welcome as a result. However, the EIA is forecasting a 4mbd surplus in 2026.

- WTI is off its intraday low of $60.78/bbl to be down 0.3% to $60.85. It breached $61.00 at the start of Tuesday’s session. Brent is 0.3% lower at $64.70/bbl after falling to $64.61. Both benchmarks are holding above initial support levels.

- With attention firmly on supply/demand fundamentals, US inventory data will continue to be monitored. Industry-based figures are released Tuesday followed by the official EIA’s on Wednesday. November monthly reports from the EIA, IEA and OPEC are scheduled for next week.

- Later the Fed’s Bowman speaks on supervision and monetary policy, ECB President Lagarde and BoE’s Breeden also appear. US data releases scheduled for today are likely to be delayed by the ongoing government shutdown.

GOLD: Bullion Lower On Stronger US$ & Uncertainty Over December Fed Cut

Gold prices have trended lower through today’s APAC trading pressured by the continued uptrend in the US dollar (BBDXY +0.1%). They are down 0.3% to $3988.5/oz, off the intraday low of $3976.01, having spent most of the session below $4000. While Monday’s Fed speakers reiterated that policy is “not on a predetermined path”, they didn’t say that a December rate cut was a likely outcome, which has made bullion more cautious. Chair Powell said last week that further easing in December was not a given.

- Fed Governor Cook said that she supported the October cut as she believed the risks to the labour market outweighed inflation. She also said that “every meeting, including December’s, is a live meeting”. Monetary easing is supportive of non-interest bearing gold and the market has about a 70% chance of a December cut.

- SF Fed President Daly noted that the FOMC should “keep an open mind” about easing next month and that 50bp of cumulative easing would leave the Fed “better positioned”.

- Silver is 0.5% lower at $47.86, after an intraday low at $47.64 but well above the 50-day EMA at $45.963. It reached $48.181 earlier.

- Equities are mixed with the S&P e-mini down 0.3% but Hang Seng up 0.2%. Oil prices are lower with WTI -0.4% to $60.82/bbl. Copper is down 1%.

- Later the Fed’s Bowman speaks on supervision and monetary policy, ECB President Lagarde and BoE’s Breeden also appear. US data releases scheduled for today are likely to be delayed by the ongoing government shutdown.

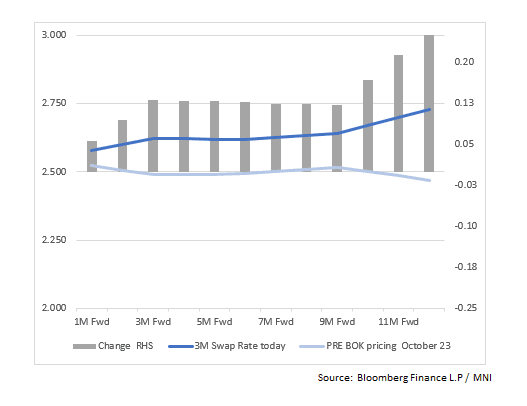

SOUTH KOREA: Could KRW Swap Moves Point to Next Rate Move for BOK?

- The recent BOK decision driven by concerns from the housing sector, when coupled with today's CPI, will likely see the BOK on hold for some time.

- However as witnessed in many developed nations globally, deflating a housing bubble cannot be done quickly, nor without the help of monetary policy.

- Up until recently, the Korean swaps curve had a mid year 2026 cut priced in, but no longer does.

- Moves in recent days have now resulted in a greater than 50% chance of a hike towards the end of next year.

- The swaps curves have 2-6bps of increases factored in over the next six months, before rising to 17bps in 12 months time.

- The MIPR function on BBG has +9bps of rate rises priced in over a 12 month time horizon.

- The key for the BOK and the bond market remains the focus by the government on the housing market. Additional attempts to cool the overheated Seoul property markets have been announced recently.

- The BOK now finds itself with time on its side but with up to -0.50% forecast to be shaved off GDP growth next year due to tariffs, decisions on monetary policy are going to be difficult.

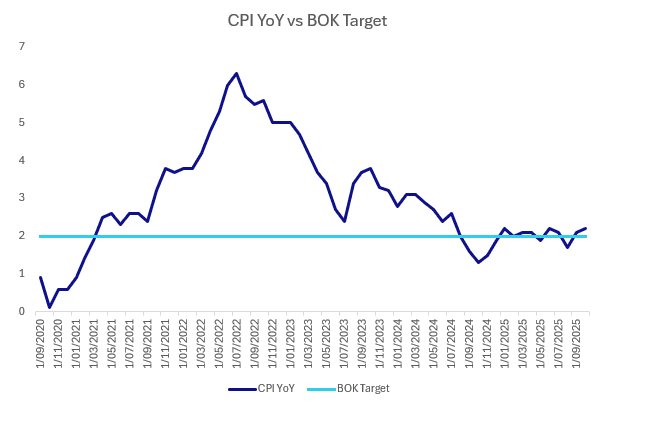

SOUTH KOREA: CPI Puts BOK on Sidelines for Some Time

- The October CPI in Korea topped forecasts and prior month result, giving the BOK yet another reason to hold.

- At the October 23 meeting, the monetary policy committee voted to hold rates citing the housing sector and with today's PMI slipping above target, provides ample room now for an extended hold.

- Core was also ahead of expectations and prior at +2.2% in what will be welcome signs that the deflationary pressures have receded.

- Within core, food prices rose +3.5% YoY as the largest gainer with transport +3.4% YoY the next biggest.

- CPI MoM prices were ahead also, up +0.3% MoM

- The window to remain on hold is limited for the BOK with estimates for 2026 that GDP growth will be trimmed by around 0.50%

- Our swaps model has seen rate cuts that were priced a short period ago, priced out and the BBG MIPR model has very littel priced in also.

- Today's CPI has the potential to be the catalyst for an extended hold.

ASIA FX: Broader USD Gains, USD/KRW Testing 1440, PHP Bucks Broader Trends

USD/Asia pairs are higher, except for USD/PHP and USD/INR. USD/CNH is testing above 7.1300, amid broader USD gains and is giving back recent gains against the yen. USD/KRW is probing selling interest around 1440, while USD/IDR is through 16700. A generally supportive USD backdrop remains in play (outside of modest yen gains), with AUD and NZD weaker, while regional equity sentiment is mostly on the backfoot.

- USD/CNH is testing above 7.1300, not too far from the 50-day EMA resistance (7.1335). We had the CNY fixing earlier, which stayed sub 7.0900. CNH/JPY is weaker, back under 21.5700, so off recent highs, but CNY is outperforming most other majors.

- USD/KRW spot has tested above 1440 today but hasn't been able to sustain the break higher. Recent highs were at 1441.45, while beyond this area interest is likely to focus on a test of 1450. The authorities may pick up FX jawboning on a break above this level though. The Kospi is down over 2%, with likely offshore selling a KRW headwind.

- Spot USD/TWD is firmer as well, closing in on 30.90, but only up 0.20%, versus USD/KRW's +0.60% rise. We may see some resistance around the 31.00 figure level. We are already through all the key EMAs though.

- USD/IDR has risen above 16700 and is back eyeing a test near 16800. Broader USD sentiment appears to be driving gains in the pair, with IDR seeing greater losses during periods of USD gains as opposed to greater IDR gains when the dollar is on the backfoot.

- USD/PHP sits off recent highs, last in the 58.65/70 region, down around 0.25%. USD/PHP is showing a fairly low beta to overall USD moves at this stage. The turn of the month may be helping marginally from a seasonal point of view.

- USD/INR is softer, on suspected intervention flows. We were last 88.60/65.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/11/2025 | 0740/0840 | ECB Lagarde Keynote Speech At Bulgarian National Bank | ||

| 04/11/2025 | 0745/0845 | Budget Balance | ||

| 04/11/2025 | 0945/1045 | ECB Lagarde At Bulgarian National Bank Press Conference | ||

| 04/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 04/11/2025 | 1130/1130 | Chancellor Reeves at House of Commons | ||

| 04/11/2025 | 1135/0635 | Fed Vice Chair Michelle Bowman | ||

| 04/11/2025 | 1140/1140 | BOE Breeden at International Banking Conference | ||

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1330/0830 | ** | Trade Balance | |

| 04/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 1500/1000 | *** | JOLTS jobs opening level | |

| 04/11/2025 | 1500/1000 | *** | JOLTS quits Rate | |

| 04/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 04/11/2025 | 2100/1600 | Canada federal budget, release expected just after 4pm EST | ||

| 05/11/2025 | 2200/0900 | * | S&P Global Final Australia Services PMI | |

| 05/11/2025 | 2200/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/11/2025 | - | Riksbank Meeting | ||

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/11/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/11/2025 | 0700/0800 | ** | Manufacturing Orders | |

| 05/11/2025 | 0745/0845 | * | Industrial Production | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0815/0915 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0830/0930 | *** | Riksbank Interest Rate Decison | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0845/0945 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0850/0950 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0855/0955 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0900/1000 | * | Retail Sales | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Services PMI (f) | |

| 05/11/2025 | 0900/1000 | ** | S&P Global Composite PMI (final) | |

| 05/11/2025 | 0930/0930 | ** | S&P Global Services PMI (Final) | |

| 05/11/2025 | 0930/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/11/2025 | 1000/1100 | ** | EZ PPI | |

| 05/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 05/11/2025 | 1315/0815 | *** | ADP Employment Report | |

| 05/11/2025 | 1330/0830 | *** | Treasury Quarterly Refunding |