RBA: Keeping Options Open, Main Concern To Get Inflation Back In Band

The Board only considered keeping rates at 3.6% at its November meeting as well as discussing its strategy going forward. Governor Bullock observed that the Board thinks it is “pretty close to neutral”, which makes it difficult to assess the level of policy restrictiveness, and thus it doesn’t have a bias, which is consistent with its discussion around holding. She said that data will continue to drive its outlook and the Board will decide policy on a “meeting-by-meeting basis” with all directions in rates possible.

- The jump in underlying inflation in Q3 was partly due to temporary factors, such as council rates, travel & fuel, but also because of more persistent items, such as dwelling costs & market services, which may be signalling that demand is exceeding supply. While the trimmed mean is expected to remain above 3% over the next year, the RBA is forecasting the quarterly increases to moderate.

- Both inflation and unemployment rose more than the bank expected, and as there is information in both, the Board remains cautious and a bit more concerned about getting inflation back in the band.

- Bullock noted that labour market forward indicators suggest that conditions are more stable than the September unemployment rate suggested and for now are likely to stay steady. ULC growth is also rising quickly. The Board is alert to risks in both directions.

- She reiterated that rates didn’t rise as much in Australia as in other countries, therefore it is likely that it won’t need to cut as much either. For now, the Board believes it is where it needs to be and is in a position to respond to both upside and downside risks.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Fresh Cycle High

- RES 4: 1.4111 High Apr 10

- RES 3: 1.4045 3.0% Upper Bollinger Band

- RES 2: 1.4019 38.2% retracement of the Feb 3 - Jun 16 bear leg

- RES 1: 1.3989 200-dma

- PRICE: 1.3953 @ 16:02 BST Oct 3

- SUP 1: 1.3897/3825 Low Sep 30 / 50-day EMA

- SUP 2: 1.3727 Low Aug 29 and a bear trigger

- SUP 3: 1.3689 Low Jul 28

- SUP 4: 1.3637 Low Jul 25

A bull cycle in USDCAD remains intact and yesterday’s break above the late September’s high, firms the bullish theme. This move higher also maintains the bullish price sequence of higher highs and higher lows. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. Sights are on 1.4019, a Fibonacci retracement point. On the downside, first key support lies at 1.3825, the 50-day EMA.

AUDUSD TECHS: Support Remains Intact For Now

- RES 4: 0.6763 1.382 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 3: 0.6726 1.236 proj of the Jun 23 - Jul 24 - Aug 21 price swing

- RES 2: 0.6660/6707 High Sep 18 / 17 and key resistance

- RES 1: 0.6629 High Sep 30 & Oct 01

- PRICE: 0.6603 @ 16:01 BST Oct 3

- SUP 1: 0.6527/21 61.8% of the Aug 21 - Sep 17 bull leg / Low Sep 26

- SUP 2: 0.6484 76.4% retracement of the Aug 21 - Sep 17 bull leg

- SUP 3: 0.6463/6415 Low Aug 27 / Low Aug 21 / 22 and a bear trigger

- SUP 4: 0.6373 Low Jun 23

The AUDUSD uptrend remains intact and recent weakness appears to have been a correction. Support to watch lies at the 50-day EMA, at 0.6558. A clear break of this average would signal scope for a deeper retracement and expose 0.6527 once again, a Fibonacci retracement. For bulls, a stronger reversal higher would refocus attention on 0.6707, the Sep 17 high. Initial resistance to watch is 0.6629, the Sep 30 and Oct 1 high.

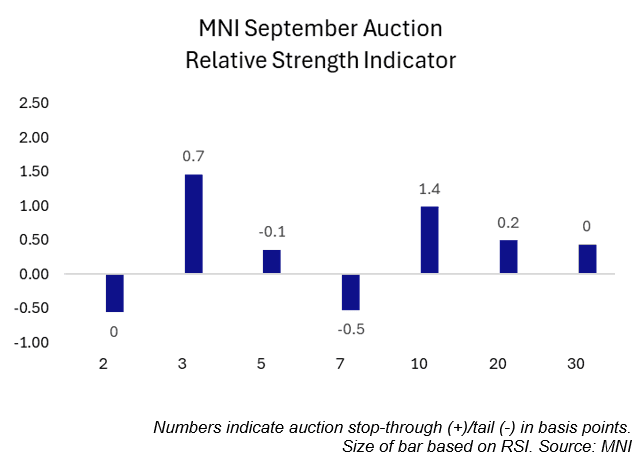

US TSYS/SUPPLY: September's Coupon Auctions Were Generally Solid (2/2)

September’s coupon auctions were generally solid, with three lines trading through, two coming out on the screws and two tailing slightly.

- Looking through the lens of MNI’s Relative Strength Indicator (RSI), five lines saw positive readings while two saw negative readings.

- The 3-year sale was the strongest auction of the month according to MNI’s RSI. The 3-year line traded through 0.7bps, the largest stop through in seven months. Meanwhile, the primary dealer take-up was just 8.4%, the lowest on record (data going back to 2003).

- The weakest sale of the month was the last – the 7-year line. This line saw the second consecutive 0.5bp tail, with the 12.0% primary dealer take-up above August’s 9.8% and July’s record low 4.1%.

September Auction Review:

- 2Y Note on-the-screws: 3.571% vs. 3.571% WI.

- 2Y FRN: 0.200% high margin vs. 0.195% prior

- 3Y Note trade-through: 3.485% vs. 3.492% WI.

- 5Y Note tail: 3.710% vs 3.709% WI.

- 7Y Note tail: 3.953% vs. 3.948% WI.

- 10Y Note trade-through: 4.033% vs. 4.047% WI.

- 10Y TIPS: 1.734% high yield vs. 1.985% prior

- 20Y Bond trade-through: 4.613% vs 4.615% WI.

- 30Y Bond on-the-screws: 4.651% vs. 4.651% WI.