MNI EUROPEAN MARKETS ANALYSIS: USD Weakness Continues

- President Trump has indicated that the US will levy tariffs in a range of 15-50% according to reports.

- Asia's FX markets had a strong day as broad based USD softness prevailed.

- Japan stocks continue to shine post announcement of trade deal with the US.

- Bullard says that Powell's removal could upend long rates.

MARKETS

US TSYS: Asia Wrap - Yields Edge Higher

The TYU5 range has been 110-30 to 111-02 during the Asia-Pacific session. It last changed hands at 110-31+, down 0-01 from the previous close.

- The US 2-year yield has edged higher trading around 3.886%, up 0.01 from its close.

- The US 10-year yield has moved higher trading around 4.392%, up 0.01 from its close.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, expect supply around 4.30/35% first up. A close back below 4.30% would begin to get the bulls excited once more and the chopfest within the range will continue.

- Wei Li(CIS BlackRock) on LinkedIn - “Credit is the dog that didn’t bark this year. It navigated wild swings in headlines and markets with a lot less vol - just a boring (boring is good!) carry story. In fact carry is back across FI: more than 80% of global FI yields >4%, compared to less than 20% (chart). Find quality carry - even US HY, its default is about half of long term average - and barbell with high conviction risky calls in equities.” See Graph Below.

- (Bloomberg) - Investors are pricing about 76 bps of Fed rate cuts in 2026 on growing speculation that Jerome Powell’s successor will deliver the easier monetary policy that Trump demands. Lutnick told Fox News rates need to be lower and called for the replacement of the Fed chair.

- Data/Events: Initial Jobless Claims, Chicago Fed Activity Index, S&P Global US PMI’s, Building Permits, New Home Sales, Kansas City Fed Manf. Activity.

Fig 1: Fixed Income Assets With Yields Above 4%

Source: MNI/BlackRock

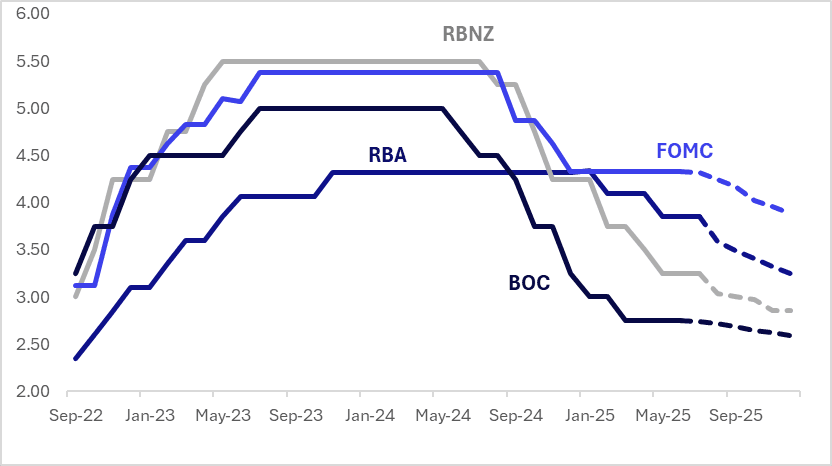

STIR: $-Bloc Markets Relatively Stable Over Past Week

Interest rate expectations across dollar-bloc economies were relatively stable over the past week, with Australia and New Zealand standing out. Australian rates moved 5bps higher, while New Zealand saw a 7bps decline. U.S. and Canadian rates were little changed.

- In New Zealand, Q2 CPI rose less than expected. Headline inflation increased 0.5% q/q and 2.7% y/y, slightly below the consensus forecasts of 0.6% and 2.8%, respectively. Tradeables inflation came in softer at 0.3% q/q, while non-tradeables matched expectations at 0.7% q/q.

- The RBNZ’s sectoral factor model—a key gauge of core inflation—also signalled subdued price pressures. It eased 0.1pp to 2.8% y/y in Q2, the lowest since Q2 2021, and now sits just 0.1pp above the headline rate. With domestic activity indicators still weak, the data reinforce expectations for a 25bp rate cut at the August 20 meeting, which coincides with the next update of the RBNZ’s staff forecasts.

- The next key regional events are the FOMC and BoC policy decisions on July 30, with markets assigning just a 4% and 8% probability, respectively, to a 25bp rate cut at either meeting.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.89%, -44bps; Canada (BOC): 2.59%, -16bps; Australia (RBA): 3.22%, -63bps; and New Zealand (RBNZ): 2.86%, -39bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

JGBS: Twist-Flattener, Tokyo CPI Tomorrow

JGB futures are slightly weaker and off session lows, -11 compared to settlement levels.

- Heading into this week, BoJ watchers largely expected the central bank to raise its benchmark interest rate at either the October or January meeting. The key debate was whether the anticipated fiscal expansion would bring that timing forward. Opinions were divided: some argued it would accelerate a hike, others said it could delay it, while many viewed the impact as neutral or difficult to assess.

- While there appears to be little immediate pressure to raise rates, this week’s announcement of a trade deal between Japan and the U.S. may nudge the BoJ closer to a hike by improving the outlook for economic conditions. This view is supported by recent comments from BoJ Deputy Governor Shinichi Uchida, who said that "uncertainty has receded, and this of course means that the likelihood has risen" for the Bank’s forecasts to be met.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's sell-off.

- Cash JGBs are 2bps cheaper to 3bps richer across benchmarks, with a flattening bias. The benchmark 10-year yield is 1.6bps higher at 1.603% versus the cycle high of 1.616%.

- Swap rates are 1bp higher to 2bps lower. Swap spreads are tighter.

- Tomorrow, the local calendar will see Tokyo CPI, PPI Services, Coincident/Leading Index, Nationwide Dept Sales and Weekly International Investment Flow data.

AUSSIE BONDS: Cheaper & Near Session Lows After RBA Gov Discusses Mon Pol

ACGBs (YM -7.5 & XM -6.5) are weaker and hovering just above lows.

- "RESERVE BANK OF AUSTRALIA GOV BULLOCK: MEASURED, GRADUAL APPROACH TO MONETARY POLICY EASING IS APPROPRIATE, LABOUR MARKET HAS EASED ONLY GRADUALLY, UNEMPLOYMENT RATE RELATIVELY LOW, RISE IN UNEMPLOYMENT IN JUNE WAS IN LINE WITH OUR FORECASTS, NOT A "SHOCK", JUNE DATA SUGGESTS LABOUR MARKET MOVED A LITTLE FURTHER TOWARDS BALANCE." – RTRS

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session after yesterday's modest sell-off. Today’s US calendar will see: Initial Jobless Claims, Chicago Fed Activity Index, S&P Global US PMI's, Building Permits, New Home Sales, Kansas City Fed Manf. Activity

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at -5bps.

- The bills strip is cheaper, with pricing -3 to -4.

- RBA-dated OIS pricing is firmer across meetings today. A 25bp rate cut in August is given a 100% probability, with a cumulative 62ps of easing priced by year-end.

- The local calendar will be empty until next Wednesday’s Q2 CPI data.

BONDS: NZGBS: Closed Cheaper With A Mixed Performance Versus $-Bloc 10Y

NZGBs closed 3-4bps cheaper, with the NZ-US 10-year yield differential 2bps wider and the NZ-AU 2bps tighter.

- RBNZ Chief Economist Paul Conway has delivered a speech earlier today in Wellington. It focused on the impact of tariffs. The key takeaway from a monetary policy standpoint is that Conway reiterated the recent monetary policy stance: "As outlined in the July Monetary Policy Review, the Committee sees scope to lower the OCR further if medium-term inflation pressures continue to ease as projected, Mr Conway says."

- "Global tariffs and economic uncertainty are likely to mean less inflation pressures in New Zealand and a pullback in business investment and household spending, RBNZ Chief Economist Paul Conway says. However, the economy is currently supported by high export prices and lower interest rates, he says."

- Today’s weekly supply showed strong demand metrics with cover ratios ranging from 2.78x (Apr-37) to 3.89x (Apr-29).

- Swap rates closed 2-5bps higher, with the 2s10s curve steeper.

- RBNZ dated OIS pricing closed little changed across meetings. 21bps of easing is priced for August, with a cumulative 37bps by November 2025.

- Tomorrow, the local calendar will be empty.

RBNZ: Conway - Tariffs To Dampen Medium Ter Inflation, RBNZ Ready To Act

RBNZ Chief Economist Pail Conway has delivered a speech earlier today in Wellington NZ. It focused on the impact of tariffs. Some key snippets from the speech are outlined below. The key take away from a monetary policy standpoint is that Conway reiterated the recent monetary policy stance: "As outlined in the July Monetary Policy Review, the Committee sees scope to lower the OCR further if medium-term inflation pressures continue to ease as projected, Mr Conway says." (see the full speech at this link).

- "Global tariffs and economic uncertainty are likely to mean less inflation pressures in New Zealand and a pullback in business investment and household spending, RBNZ Chief Economist Paul Conway says. However, the economy is currently supported by high export prices and lower interest rates, he says."

- "Tariffs may make global supply chains less efficient and could nudge up the cost of imports. This is why tariffs are expected to add to inflation pressures in the US. But for New Zealand, the main impact is likely to be weaker global growth, which could reduce demand for our exports and lower import prices. Import prices could fall further as other countries redirect their exports away from the US. This is expected to reduce inflation pressures here.

- At the same time, uncertainty is elevated, making it harder for households and businesses to plan. “When businesses aren’t sure what’s coming, they hold off hiring and delay big investments. Households tend to respond to increased uncertainty by putting off big spends or job moves,” Mr Conway says.

- “There’s a whole lot of ‘wait and see’ going on out there right now.”

- “On net, these developments are expected to slow New Zealand’s economic recovery over mid-2026 and reduce medium-term inflation pressures. This is against a backdrop of strong export prices, especially for dairy and beef, and lower interest rates. "

FOREX: Asia FX Wrap - The USD Trades Poorly

The BBDXY has had a range of 1191.55 - 1193.53 in the Asia-Pac session, it is currently trading around 1192, -0.10%. The USD again slipped lower overnight, and this time in the face of US yields moving higher. The market is much more comfortable selling USD’s, while below 1220 rallies should continue to find supply. The price action for the USD is really beginning to stink and you can see why most of the market wants to express a short. There is lots of event risk coming up next week and we are heading into month-end so caution is warranted.

- EUR/USD - Asian range 1.1762 - 1.1780, Asia is currently trading 1.1775. The pair bounced off its first support around the 1.1600 area. The price still looks a little stretched in the short term, but the USD is trading extremely poorly and the EUR will continue to be the main beneficiary.

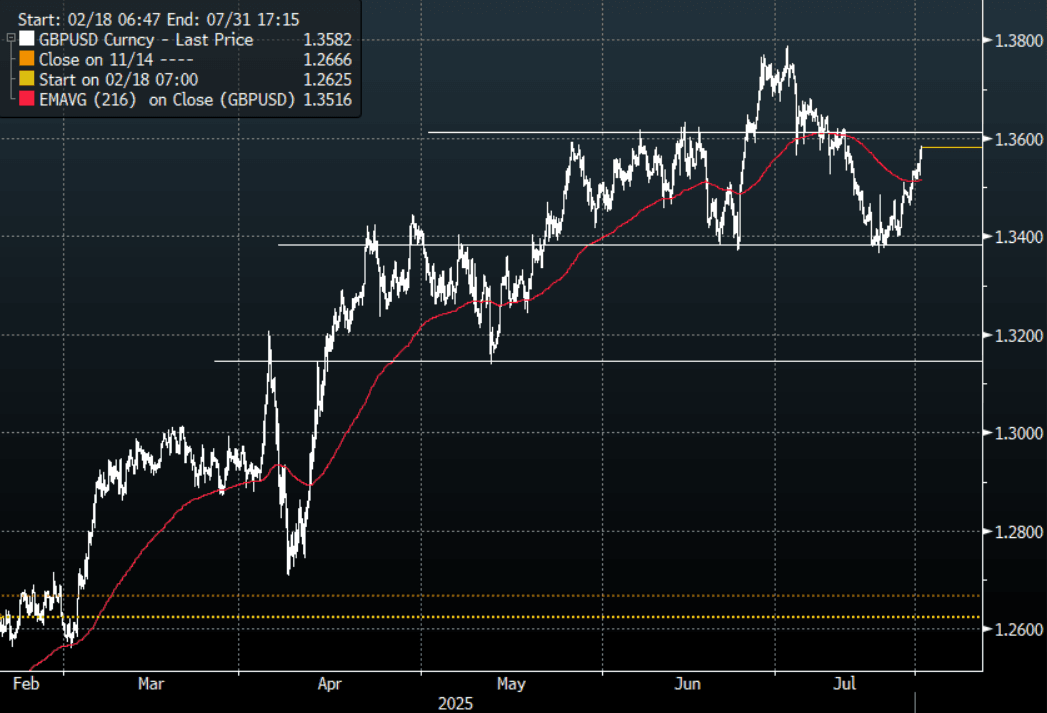

- GBP/USD - Asian range 1.3571 - 1.3589, Asia is currently dealing around 1.3580. The support around 1.3350/1.3400 has proved to be solid first up. The pair has cleared its resistance around 1.3550 and focus will now turn back to the 1.3650 area and beyond. While the support holds the market will be encouraged to continue to play from the long side.

- USD/CNH - Asian range 7.1441 - 7.1524, the USD/CNY fix printed 7.1385, Asia is currently dealing around 7.1480. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.05%, Gold $3382, US 10-Year 4.39%, BBDXY 1192, Crude oil $65.56

- Data/Events : France Business & Manufacturing Confidence/HCOB PMI’s, EZ HCOB PMI’s & ECB Decision, Germany GfK Consumer Confidence & HCOB PMI’s

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA FX: USD Biased Weaker In SEA, PHP Outperforms

In South East Asia FX markets, the bias is for weaker USD levels. PHP is the best performer so far today, up around 0.40% in spot terms. Elsewhere, gains are modest, in the 0.15-0.25% range.

- USD/PHP sits close to 56.65 in latest dealings. Outside of broader USD weakness and optimism on trade deal progress, there doesn't appear a fresh catalyst for PHP gains. We are well above earlier 2025 lows of 55.15, so we may be seeing some catch up to broader dollar trends. The Philippines hopes to negotiate a tariff rate of 15% its envoy to the US stated.

- USD/THB has slightly lagged these softer dollar trends, the pair last near 32.15, little changed for the session. Still, we got to fresh multi year lows of 32.11 in the first part of trade. A clean break lower will see the 32.00 figure level targeted. June trade figures were a little bit below forecasts in terms of export and import growth, but the trade surplus was above, over $1bn. The authorities noted the H2 outlook is very uncertain given US tariff levels. The other focus point will be on Thailand-Cambodia border clashes, which have escalated over the past 24 hours. Broader markets fallout appears limited at this stage.

- USD/MYR is down close to 0.25%, last under 4.2200. Focus will be a re-test sub 4.2000 for this pair. USD/IDR is down less than 0.10%, last near 16280, exhibiting a low beta with respect to lower USD moves at this stage.

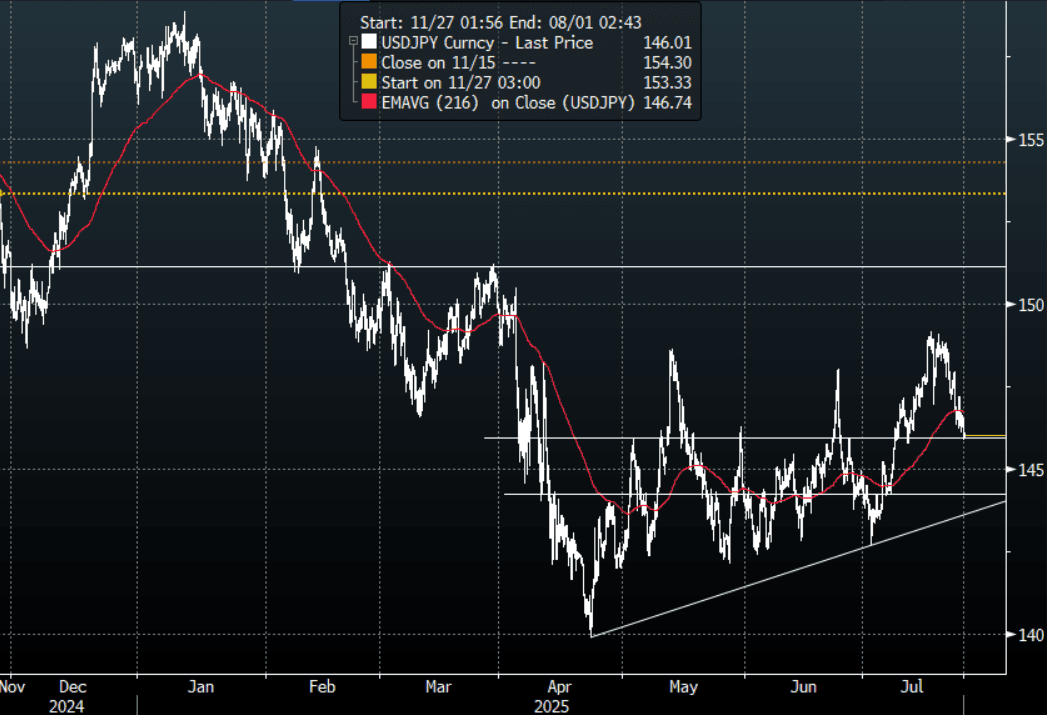

JPY: Asia Wrap - USD/JPY Has A Look Below 146.00 Testing First Support

The Asia-Pac USD/JPY range has been 145.86 - 146.51, Asia is currently trading around 146.00, -0.36%. USD/JPY continues to frustrate the market and has given back a lot of its recent gains which saw a big portion of the JPY longs capitulate. The move lower in USD/JPY might have a few traders scratching their heads but for the moment the USD seems to be floundering in all scenarios. The CFTC data showed the market is shifting its view on the JPY, with leverage funds just starting to build JPY shorts and Asset managers actively reducing their own. We are probing the first support around 146.00 where some demand could be seen, next support is the pivotal 144.00/145.00 area.

- JAPAN DATA July PMIs Mixed, Manufacturing Back Into Contraction, Services Rise: Japan preliminary July PMIs were mixed. notably manufacturing fell to 48.8 from 50.1 in June. Services rose though to 53.5 from 51.7. This left the composite index at 51.5, unchanged from the June read.

- (Bloomberg) Japanese government bonds may fall on growing speculation that the Bank of Japan will hike interest rates by the end of this year. The yen is steady against the dollar after Prime Minister Shigeru Ishiba tells reporters that there's no truth in reports that he will resign.

- "HAYASHI: TO BASE US DEFENSE BUYS ON EXISTING CAPABILITY PLAN” - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.50($751m),147.00($986m), 147.50($1.57b).Upcoming Close Strikes : 145.00($1.3b July 29), 145.00($1.15bm July 25) - BBG.

- CFTC data shows Asset managers starting to reduce JPY longs more aggressively +71610, while leveraged funds have started to build into a new short JPY position -12606.

Fig 1 : USD/JPY Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

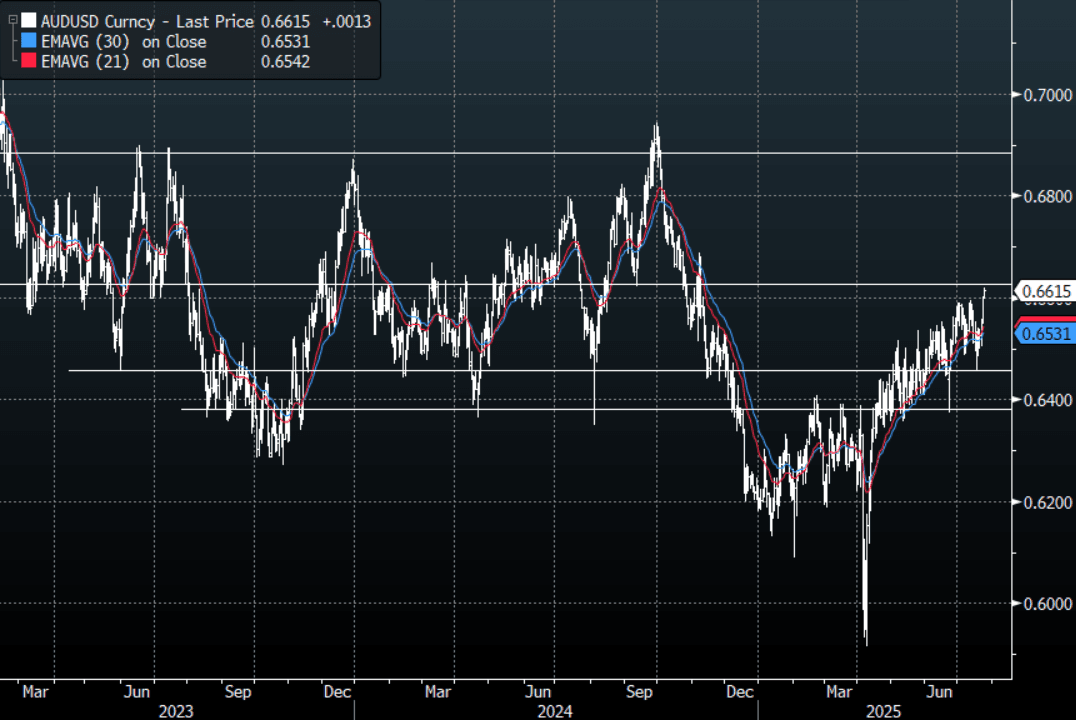

AUD: Asia Wrap - AUD/USD Has A Look Above 0.6600

The AUD/USD has had a range of 0.6597 - 0.6618 in the Asia- Pac session, it is currently trading around 0.6615, +0.23%.The pair extended higher once more as the USD continues to trade heavy even with US yields moving higher. The pair is now challenging the top of its recent range and a sustained move above 0.6600 could see it gain upward momentum, but there is lots of event risk coming up next week and we are heading into month-end so caution is warranted.

- "RESERVE BANK OF AUSTRALIA GOV BULLOCK: MEASURED, GRADUAL APPROACH TO MONETARY POLICY EASING IS APPROPRIATE, LABOUR MARKET HAS EASED ONLY GRADUALLY, UNEMPLOYMENT RATE RELATIVELY LOW, RISE IN UNEMPLOYMENT IN JUNE WAS IN LINE WITH OUR FORECASTS, NOT A "SHOCK", JUNE DATA SUGGESTS LABOUR MARKET MOVED A LITTLE FURTHER TOWARDS BALANCE.” - RTRS

- (Bloomberg) -- “Fortescue’s shipment of iron ore rose 4% from a year earlier in the fourth quarter to a record high. The Australian miner exported 55.2 million tons of the steelmaking material over the period, taking the full-year volume to 198.4 million tons.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD495m), 0.6600(AUD886m). Upcoming Close Strikes : 0.6600(AUD968m July29) - BBG

- CFTC Data shows Asset managers have maintained their shorts -38267, the Leveraged community added slightly to their shorts to -20048.

- AUD/JPY - Today's range 96.40 - 96.74, it is trading currently around 96.60, +0.13%. The pair consolidated trading sideways overnight. The support between 95.00 - 96.00 held as demand materialised first up, the pair is looking for some momentum to continue to build for a move higher.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

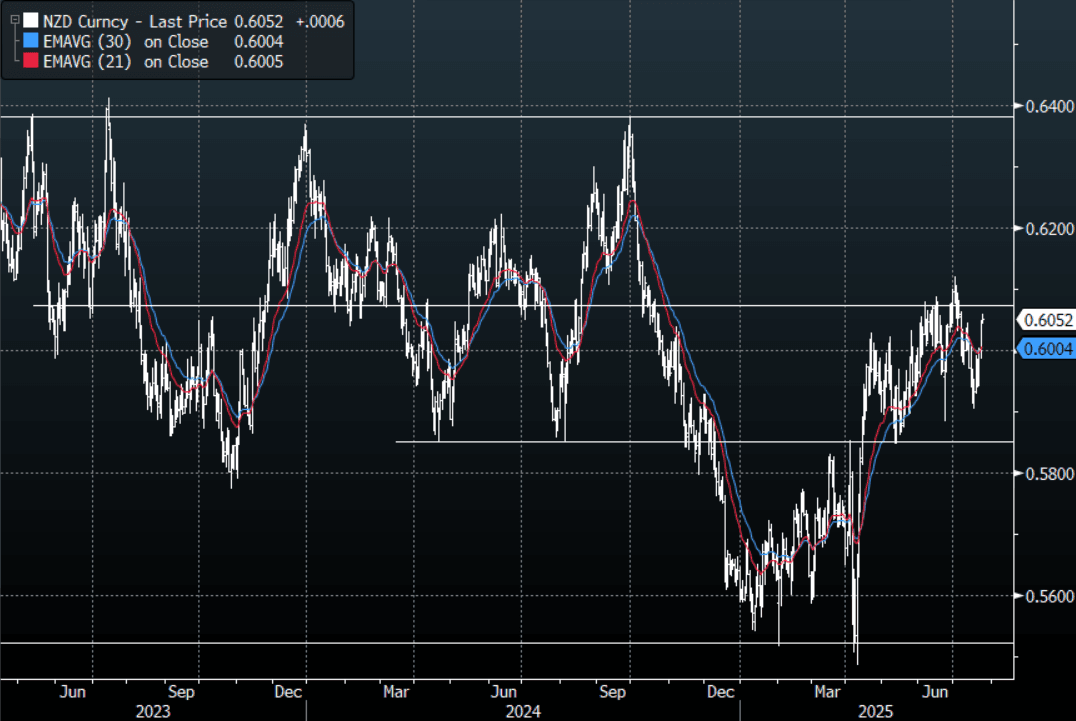

NZD: Asia Wrap - NZD/USD Extends Move Higher, Eyes 0.6100

The NZD/USD had a range of 0.6042 - 0.6059 in the Asia-Pac session, going into the London open trading around 0.6053, +0.12%. The pair extended higher once more as the USD continued to trade heavy even with US yields moving higher. Depending what your view is this 0.6050 area looks an attractive fade initially, the danger though is the USD which is looking sickly once more and should it capitulate the NZD could build momentum higher again. Price will need a sustained break back above the 0.6050/0.6100 area to signal a potential base might be in place. There is lots of event risk coming up next week and we are heading into month-end so caution is warranted.

- "RBNZ'S CONWAY: TARIFFS LIKELY TO MEAN A WEAKER EXPORT DEMAND, MPC EXPECTS INFLATION NEAR 3% THROUGH MID-2025, SEE INFLATION SETTLING AROUND 2% EARLY 2026, CPI WAS CONSISTENT WITH RBNZ EXPECTATIONS, INDICATORS SUGGEST 2Q GROWTH WAS A BIT WEAK " - BBG

- "China Newspaper Sees Yuan Resilience, Citing Policy Potentials: The strength of the yuan against the dollar this year is the result of a combination of internal and external factors, and the Chinese currency is expected to maintain its resilience, Shanghai Securities News reported, citing analysts." BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6010(NZD302m), 0.6050(NZD395m). Upcoming Close Strikes :none. - BBG

- CFTC Data shows Asset Managers slightly reduced their newly built longs in NZD +8192, the Leveraged community has continued to reduce their shorts last week -6744.

- AUD/NZD range for the session has been 1.0912 - 1.0928, currently trading 1.0925. The cross moved higher in response to the NZ CPI. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Most Markets Higher, Japan Still Outperforming

Regional Asia Pac equities are mostly tracking higher so far in Thursday trade, although continued outperformance from Japan stocks remain a highlight. These moves follow broad based cash gains in Wednesday US trade. US futures are up modestly so far, led by the tech side, while EU equity futures are showing a +1.3% gain at this stage. Positive tones around US-EU and US-China trade talks has aided broader sentiment over the past 24 hours (in the aftermath of the 15% tariff deal with Japan).

- Japan benchmark indices are up around 1.6% at this stage. This puts the Topix not too far from the 3000 level, and have already hit fresh record highs today. The auto sub index is up close to 1.10%, so lagging the broader market gain, but this follows a +10% rise yesterday. Bank stocks have risen today, the index up 3.3%, amid hopes the trade deal may enable the BoJ to tighten policy before year end.

- Elsewhere Hong Kong and China markets remain firmer. The CSI 300 is near 4140, just short of recent highs, the HSI was tracking towards 25690, fresh highs back to 2021.

- South Korean and Taiwan markets are up more modestly. Tsy Secretary Bessent won't attend the next round of trade talks with South Korea due to a scheduling conflict. Still other talks will happen, while onshore media in South Korea says the authorities will propose $100bn of investments into the US to achieve a trade deal. The Kospi is struggling above 3200, while the Taiex was last up 0.30%.

- In SEA, Indonesian stocks are outperforming, up over 1%, while Thailand's benchmark is down modestly, after strong gains yesterday.

ASIA STOCKS: Inflows Seen Across The Board, Thailand's Best Day Since Sep 2024

EM Asia equity inflows were positive across the board yesterday, while Indian inflows also rebounded, see the table below. Broader equity market gains helped fuel inflow momentum, with market sentiment buoyed by the US-Japan trade deal (along with positive spill over from the surge in Japan equities).

- Positive momentum was maintained for Taiwan inflows. July to date has now seen close to $7bn of net inflows into local stocks from offshore investors.

- Net inflows into South Korea also returned. This morning the Kospi is higher, above 3200, with focus on whether we can hold above this level. Local media (Chosun) reported: "South Korean government to raise ceiling on corporate tax to 25% from 24% and also increase stock transaction tax, Chosun Ilbo newspaper reports, without citing anyone." (via BBG, see this link). The plan also includes changes to taxes on dividend income.

- Thailand's +$139mn inflow was the strongest daily inflow since September last year. The SET index was up 2.34% yesterday, rising to 1220, near May highs for the index.

- Inflows were positive for other parts of SEA, but of smaller magnitude.

Fig 1: Asian Market Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 302 | 961 | -7158 |

| Taiwan (USDmn) | 300 | 1914 | 1029 |

| India (USDmn)* | 535 | 46 | -8395 |

| Indonesia (USDmn) | 41 | 51 | -3607 |

| Thailand (USDmn) | 139 | 335 | -1992 |

| Malaysia (USDmn) | 23 | 19 | -2836 |

| Philippines (USDmn) | 3 | -2 | -620 |

| Total (USDmn) | 1344 | 3323 | -23578 |

| * Data Up To July 22 |

Source: Bloomberg Finance L.P./MNI

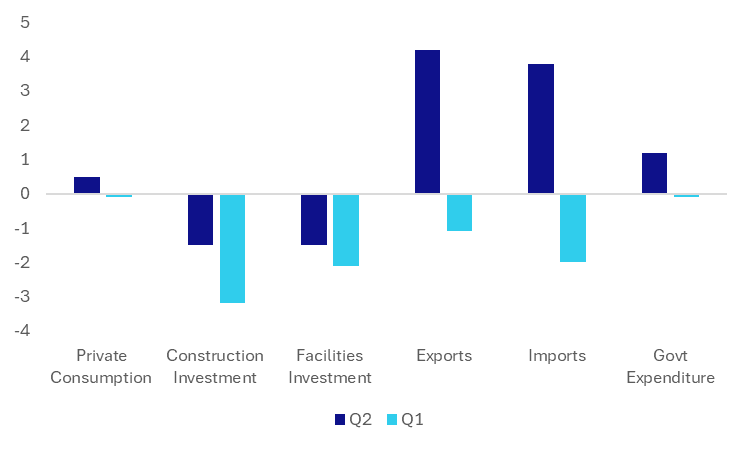

SOUTH KOREA: GDP Rebounds, Aided By Consumption/Exports, Investment Still Weak

South Korea's q/q growth of 0.6% was just above market forecasts (0.5%), but well above the Q1 contraction of -0.2%. Q2's rise was the strongest quarterly gain since Q1 2024. In y/y terms growth rose 0.5%, against a 0.4% forecast and flat outcome in Q1.

- In terms of the detail, Rtrs noted on the expenditure: "private consumption rose 0.5% over the quarter, while construction and facility investments each fell 1.5%, according to the Bank of Korea. Exports jumped 4.2%, led by semiconductors, after falling 0.6% in the previous quarter amid U.S. tariff uncertainty. It was the strongest quarterly performance since the third quarter of 2020."

- The chart below plots the various expenditure outcomes for Q2 versus Q1.

- Manufacturing rose 2.7%q/q after a 0.6% decline in Q1, but construction was down -4.4%q/q. Services rose 0.6%q/q, after falling 0.2% in Q1.

- The data is likely to add to the BoK's wait and see approach in terms of the rate outlook. The central bank has already revised down the growth outlook, while we also recently had fresh fiscal stimulus from the government.

- Earlier this week the consumer sentiment reading rebounded to multi year highs as well.

Fig 1: South Korean Q2 GDP Rebounds

Source: Bloomberg Finance L.P./MNI

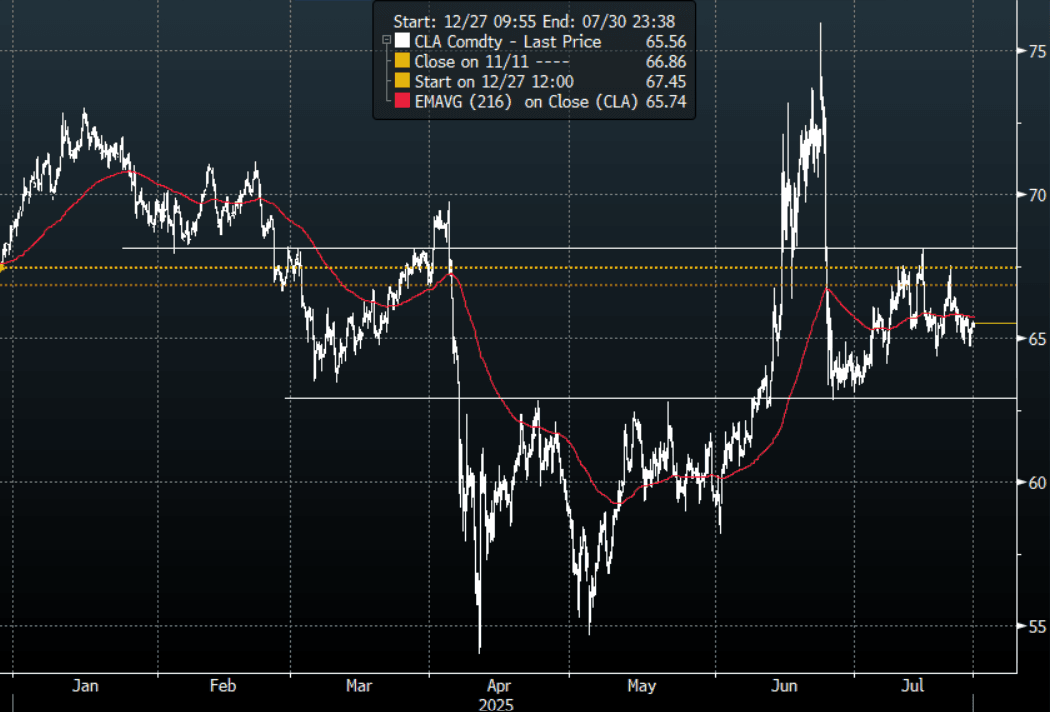

OIL: WTI Finds Demand Sub $65.00 On US Crude Stock Drawdown

The overnight range for the CLU5(WTI) contract was $64.71 - $65.52, it is currently trading around $65.55 in the Asia-Pac session, +0.48%. WTI found some demand below $65.00 but continues to consolidate within its recent $63 - $68 range. Oil prices continued to range trade and did not find support from the US-Japan deal during European trading as they trended lower. The larger-than-expected US crude stock drawdown though helped them to find a trough and they recovered to finish slightly higher on the day. US crude oil inventories fell by 3.17 million barrels, the EIA said.

- Brent for September settlement is trading at $68.70 a barrel in Asia, +042%.

- “Vishnu Varathan, head of macro for Asia at Mizuho Bank Ltd, said there may be mild buoyancy in crude from a less-dismal demand-side assumption as markets express relief on the worst-case tariff threats being averted.” - BBG

- “The oil-procurement patterns of India’s Reliance Industries Ltd. are coming under scrutiny after the European Union announced new restrictions on diesel made from Russian crude." - BBG

Fig 1: WTI Crude Future Hourly Chart

Source: MNI - Market News/Bloomberg Finance L.P

GOLD: Holding Lower After Wednesday's Dip, Safe Haven Flows Weighed By Equities

Gold prices are holding slightly weaker in the first part of Thursday trade. We were last near $3383.5/oz. This is off recent highs near $3439/oz. We have seen a generally positive tone to regional equity markets so far today, with Japan continuing to outperform. US equity futures are also a touch higher, led by Nasdaq futures. As we saw on Wednesday, the global equity bounce is reducing safe haven flows, which may be weighing on bullion demand. So far today, the generally softer tone for the USD is not providing positive impetus to gold prices, with reduced safe haven flows outweighing at this stage.

- Bullion is again below the 23 June high of $3395.1. It fell to a low of $3381.59 on Wednesday. Initial support is at $3350.8, 20-day EMA. Resistance is $3483.9 with the bull trigger at $3500.1.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 24/07/2025 | 0600/0800 | * | GFK Consumer Climate | |

| 24/07/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 24/07/2025 | 0700/0900 | ** | PPI | |

| 24/07/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/07/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 24/07/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 24/07/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/07/2025 | 1100/0700 | *** | Turkey Benchmark Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Deposit Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Main Refi Rate | |

| 24/07/2025 | 1215/1415 | *** | ECB Marginal Lending Rate | |

| 24/07/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/07/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1230/0830 | ** | Retail Trade | |

| 24/07/2025 | 1245/1445 | ECB Press Conference | ||

| 24/07/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/07/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/07/2025 | 1400/1000 | *** | New Home Sales | |

| 24/07/2025 | 1400/1000 | *** | New Home Sales | |

| 24/07/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/07/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/07/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/07/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/07/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 25/07/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 25/07/2025 | 2330/0830 | ** | Tokyo CPI | |

| 25/07/2025 | 0600/0800 | ** | PPI | |

| 25/07/2025 | 0600/0800 | ** | Unemployment | |

| 25/07/2025 | 0600/0700 | *** | Retail Sales | |

| 25/07/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 25/07/2025 | 0800/1000 | ** | M3 | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 25/07/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 25/07/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 25/07/2025 | 1300/1500 | ** | BNB Business Confidence |