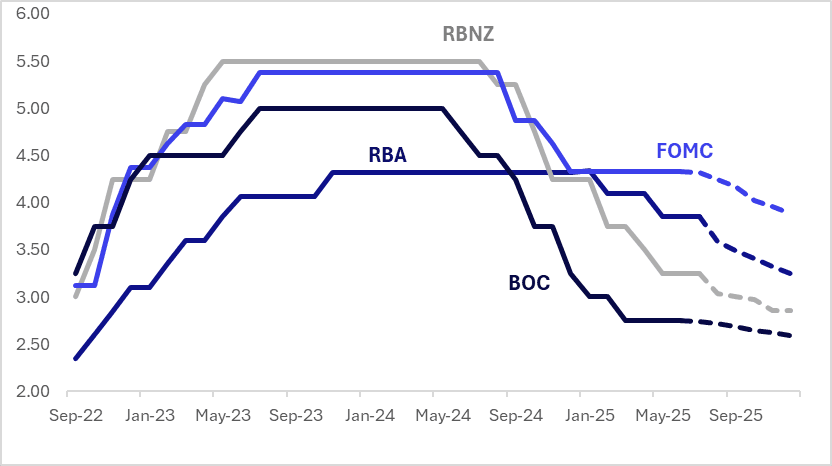

STIR: $-Bloc Markets Relatively Stable Over Past Week

Jul-24 03:49

Interest rate expectations across dollar-bloc economies were relatively stable over the past week, with Australia and New Zealand standing out. Australian rates moved 5bps higher, while New Zealand saw a 7bps decline. U.S. and Canadian rates were little changed.

- In New Zealand, Q2 CPI rose less than expected. Headline inflation increased 0.5% q/q and 2.7% y/y, slightly below the consensus forecasts of 0.6% and 2.8%, respectively. Tradeables inflation came in softer at 0.3% q/q, while non-tradeables matched expectations at 0.7% q/q.

- The RBNZ’s sectoral factor model—a key gauge of core inflation—also signalled subdued price pressures. It eased 0.1pp to 2.8% y/y in Q2, the lowest since Q2 2021, and now sits just 0.1pp above the headline rate. With domestic activity indicators still weak, the data reinforce expectations for a 25bp rate cut at the August 20 meeting, which coincides with the next update of the RBNZ’s staff forecasts.

- The next key regional events are the FOMC and BoC policy decisions on July 30, with markets assigning just a 4% and 8% probability, respectively, to a 25bp rate cut at either meeting.

- Looking ahead to December 2025, current market-implied policy rates and cumulative expected easing are as follows: US (FOMC): 3.89%, -44bps; Canada (BOC): 2.59%, -16bps; Australia (RBA): 3.22%, -63bps; and New Zealand (RBNZ): 2.86%, -39bps.

Figure 1: $-Bloc STIR (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS AUCTION: 20-Year JGB Auction Results

Jun-24 03:44

The Japanese Ministry of Finance (MOF) sells Y 758.6bn 20-Year JGBs:

- Average Yield: 2.364% (prev. 2.453%)

- Average Price: 100.48 (prev. 99.29)

- High Yield: 2.385% (prev. 2.540%)

- Low price: 100.20 (prev. 98.15)

- % Allotted At High Yield: 20.7575% (prev. 80.8791%)

- Bid/Cover: 3.1007x (prev. 2.5007x)

CHINA: Bond Futures Lower as Equity Rallies

Jun-24 03:15

- A decent bounce in risk sentiment sees major bourses strong and bond futures lower.

- The 10YR is lower by -0.06 at 109.08 and remains above the 20-day EMA of 108.99

- The 2YR is lower by -0.01 at 102.51 and sits just above the 50-day EMA of 102.50

- The CGB10YR is at 1.64%

JGBS: Modestly Weaker At Lunch Ahead Of 20Y Supply

Jun-24 03:01

At the Tokyo lunch break, JGB futures are weaker, -18 compared to the settlement levels.

- (Bloomberg) -- The Bank of Japan shrank its balance sheet by 2.3% to 716.1 trillion yen in the past 10 days.

- Impact of data

- Cash JGBs are little changed across benchmarks out to the 30-year and 1bp cheaper beyond. The benchmark 20-year yield is 0.6bp lower at 2.353% ahead of today's supply.

- Today’s 20-year JGB auction follows very poor results across key metrics at last month’s auction. The low price underperformed dealer forecasts, according to a Bloomberg poll. Moreover, the cover ratio decreased to 2.5007x from 2.9639x in the prior auction and the auction tail lengthened dramatically from 0.34 to 1.14 – the longest since 1987.

- Today’s 20-year JGB auction offers an outright yield approximately 10bps below last month’s level and 25bps below the cycle high.

- Moreover, the 10/20 yield curve remains near its recent high, its steepest since 1999.

- Today's auction also comes after a tentative ceasefire between Israel and Iran, diminishing any haven bid it potentially may have enjoyed.

- Swap rates are 1-2bps higher, with a steeper curve. Swap spreads are wider.