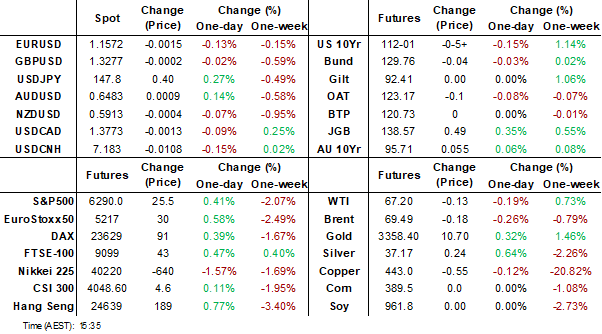

MNI EUROPEAN MARKETS ANALYSIS: USD Steady, Equity Futures Up

- US Tsy yields have retraced a small part of Friday's move lower. US President Trump stated he would nominate a new Fed Governor (for the outgoing Kugler) and new head of Labor Stats in the next few days.

- The USD is relatively steady, with broader risk appetite holding up ok. US equity futures are firmer, while regional markets are mostly higher (ex Japan).

- Oil prices are slightly lower today after falling around 3% on Friday driven by growth concerns and their potential impact on energy demand.

- Later final US June orders, Swiss July CPI and Spanish July unemployment print.

MARKETS

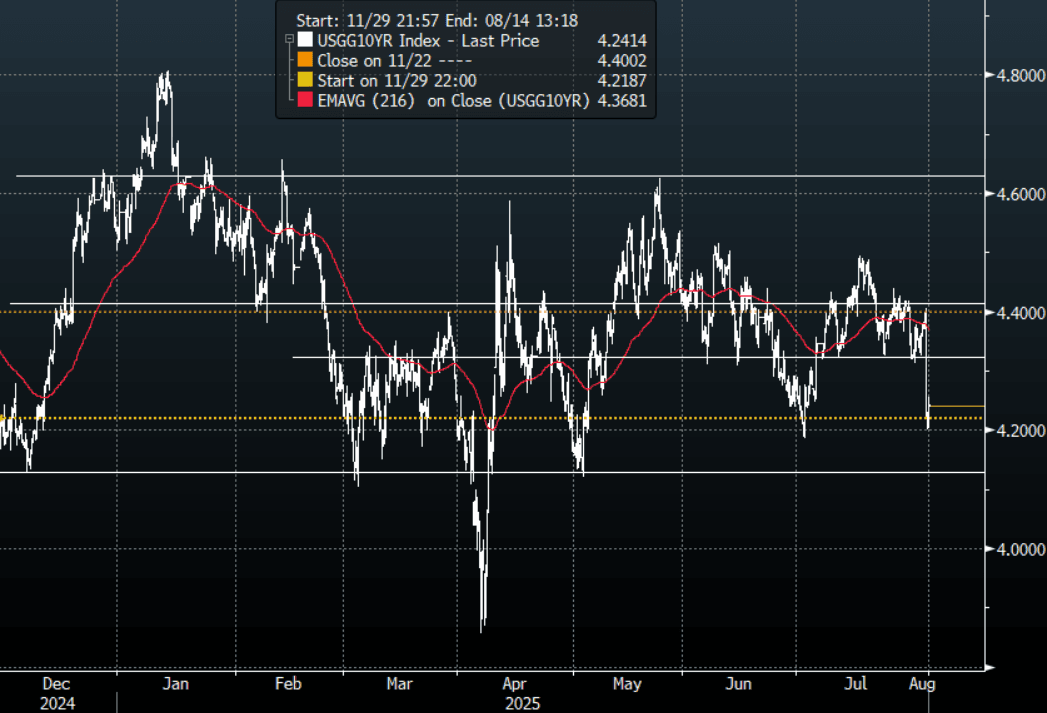

US TSYS: Asia Wrap - Yields Retrace Some Of Friday's Moves

The TYU5 range has been 112 to 112-12 during the Asia-Pacific session. It last changed hands at 112-03+, down 0-03 from the previous close.

- The US 2-year yield has bounced off Friday’s lows trading around 3.696%, up 0.01 from its close.

- The US 10-year yield has also bounced off Friday’s lows trading around 4.241%, up 0.03 from its close.

- (Bloomberg) -- “A block of 2,300 contracts in 10-year bond September futures traded at a price of 114-03 on CBOT. A total of 53,897 contracts traded so far in this session.” There were also multiple block trades executed in both the five-year and two-year contracts.

- The 10-year yield had a powerful move lower in reaction to the NFP data, breaking below its 4.30% pivot within the wider range 4.10% - 4.65%. This now turns momentum lower in yields and you could expect buyers of treasuries on bounces back towards 4.30/35% now looking to initially test the 4.10% area. The move was even more aggressive in the 2-year which has rejected the move back towards 4% and now looks to target the pivotal 3.50% area.

- Wei Li(CIS BlackRock) on LinkedIn: “I don’t envy Powell, the Fed challenge is real:

- Slower growth - we had expected tariffs to slow US growth to about HALF its potential, and now it looks like the economy is already there. 3-month average payroll gains of just 35k is below our breakeven estimate of 60-80k, that accounts for demographics and softening immigration flows. Tariffs and trade are distorting other data such as gdp, but it is less the case with labour data/nfp.”

- “Persistent inflation pressure - average hourly earnings rose on the month, puzzlingly strong given weak job creation, although partly attributable to slower immigration crimping labour supply. Furthermore, tariffs are starting to feed through and could further push up goods prices.”

- CrossBorder Capital on X: “US Treasuries looking pretty stable despite the noise!? Term premia decoupling favorably from RoW. Zero evidence of loss of safe haven quality.”

- Data/Events: Factory Orders, Durable Goods

Fig 1: 10-Year US Yield 120min Chart

JGBS: Futures Test Above 139.00 Before Retracing, 10yr Debt Auction Tomorrow

Japan Sep futures tested above 139.00 in early trade, but sit back at 138.68, +.60 in latest dealings. After spiking early in response to the US Tsy futures rise we have settled into a tight range for much of the session after dipping back under 138.80.

- In the cash JGB space, yields are holding lower, but are away from worst levels. The 10yr was last close to 1.505%, earlier we got to 1.472%. This was lows back to early July in yield terms. For the 2-7yr tenors we are 5-7bps off in yield terms. For the 20-40yr tenors we have seen a steadier backdrop.

- Focus remains on the fiscal backdrop, particularly as opposition parties continue to push for sales tax cuts. So far the LDP has resisted such moves as it is worried around what the market impact could be on further fiscal position deterioration.

- Note tomorrow we get the 10yr debt auction locally.

- On the data front today we just had the July monetary base data. Focus will be on Wednesday's June labor cash earnings figures.

AUSSIE BONDS: Futures Off Highs, Inflation Gauge Up But Mkt Following Tsys

Australian bond futures sit off earlier highs. The 3yr (YM) got above 96.70 in early dealings, but sits back near 96.65 currently, still +.105 for the session. The 10yr future (XM) got above 95.80, but is now back at 95.72, +.065 for the session.

- Like elsewhere news flow has been fairly light so far today. This has left market largely following US moves, which pared earlier gains. Broader risk appetite has held up ok, which has likely aided some yield retracement (albeit very modest with Friday's yield losses).

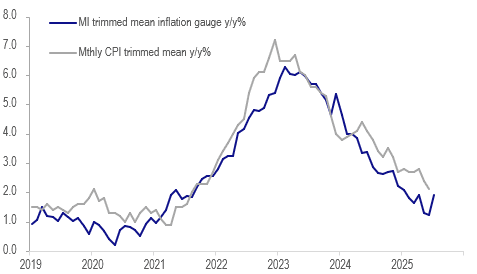

- On the data front, the Melbourne Institute headline inflation gauge for July showed a material increase to 2.9% y/y from 2.4% in June as it rose 0.9% m/m. Its trimmed mean measure rose 0.8% m/m to be up 1.9% y/y from 1.2%, the highest since January. This can lead the monthly CPI trimmed mean by up to 6 months and thus could be signalling that it troughed in June around the bottom of the RBA's 2-3% target band and may rise in coming months.

- In a week of second tier data, the focus is likely to be on Tuesday’s June household spending data which will now replace retail sales, which had its last print last week. The Q2 chain volume measure is also out. Bloomberg consensus expects June consumption values to rise 0.8% m/m to be up 4.9% y/y after 4.2% in May. The ABS noted that discounting in the month had boosted June retail sales.

AUSTRALIA DATA: MI Underlying Inflation Gauge Rises Signalling Possible Trough

The Melbourne Institute headline inflation gauge for July showed a material increase to 2.9% y/y from 2.4% in June as it rose 0.9% m/m. Its trimmed mean measure rose 0.8% m/m to be up 1.9% y/y from 1.2%, the highest since January. This can lead the monthly CPI trimmed mean by up to 6 months and thus could be signalling that it troughed in June around the bottom of the RBA’s 2-3% target band and may rise in coming months. The headline inflation gauge has less signal to it. Currently the RBA remains focussed on quarterly CPI data but a more complete monthly series will be released in November.

Australia trimmed mean inflation y/y%

BONDS: NZGB Yields Down But Away From Worst Levels, US Tsy Yields Edge Higher

NZGB yields sit lower, but are away from session lows. We are around 4-5.5bps lower across the benchmarks, with the 15-30yr tenors slightly lagging the other tenors. The 2yr yield is under 3.19%, while the 10yr is back to 4.45%. The 2yr is threatening multi month lows, while the 10yr is around mid range.

- The pick up in US Tsy yields (around +2-3bps across the curve), has helped pull NZGB yields up from session lows.

- In the swap space, the 2yr is holding under 3.00%, off 5bps so far today. The 10yr couldn't sustain an earlier move under 3.90%, last close to 3.92%, off around 4bps.

- The local news flow has been very light with no data out today. Market focus has been on spill over from the Tsy yield plunge on Friday. So far today risk appetite has held up ok, which has likely aided some yield retracement.

- The main data event this week will be Wednesday's Q2 labour market report. It is likely to show a contraction in employment and a further pickup in the unemployment rate and as a result further moderation in wage inflation. Q2 filled jobs fell 0.3% q/q after -0.1% signalling that there was job shedding in the quarter. The unemployment rate was stable in Q1 at 5.1%, helped by a 0.1pp fall in the participation rate, but this was up almost 2pp since the Q1 2022 trough. The economic recovery remains lacklustre despite 225bp of easing and thus given the lags the labour market is yet to pickup again.

Source: MNI - Market News/Bloomberg Finance L.P

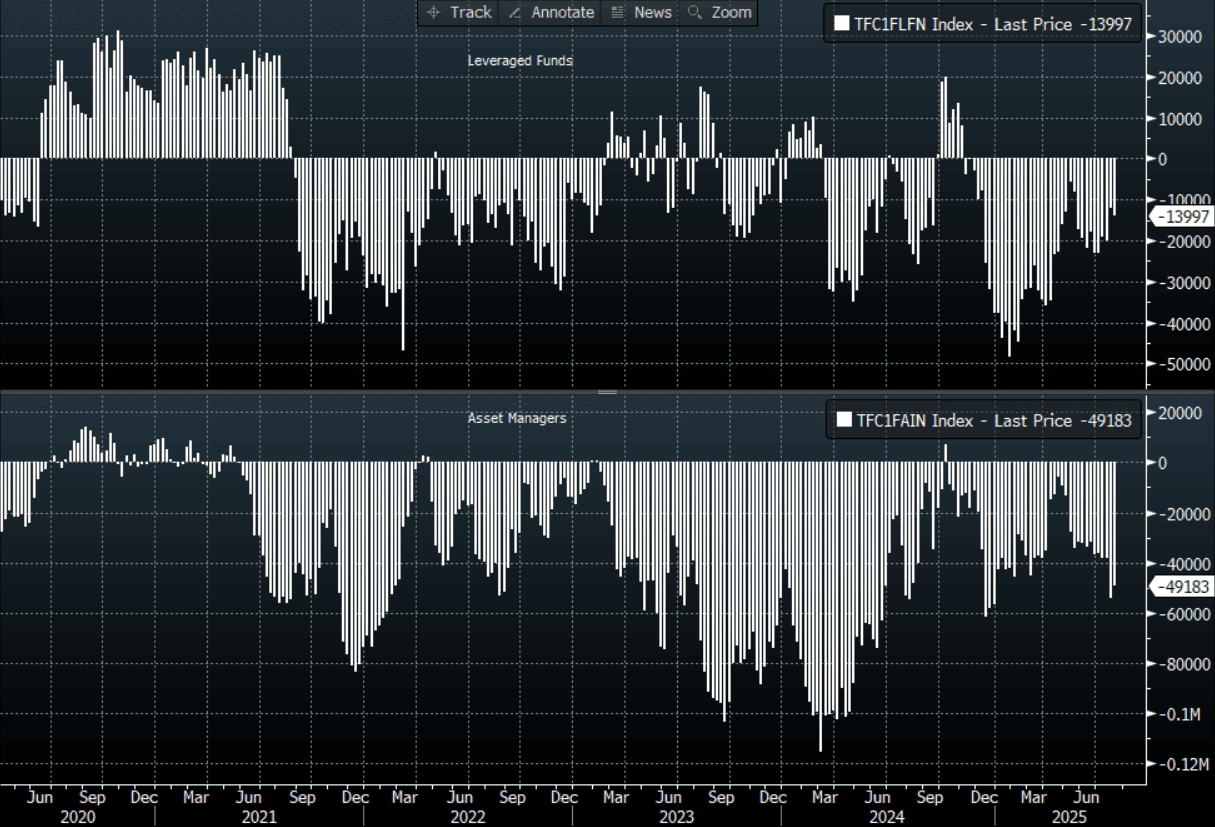

FOREX: Leveraged Investors Mostly Bought the USD In Week Ending July 29th

In the week ending Tuesday July 29th the bias from the leveraged investor base was in favor of the USD. For 6 out of the 8 currencies we saw net USD buying, with JPY and GBP the most prominent. Yen shorts were extended to -31k, the largest since Feb of this year. This in part helps explain Friday's price action, where the yen rebounded strongly in the aftermath of the weaker US NFP report. USD/JPY fell over 2.25% for Friday's session, as yen shorts were potentially cut back.

- GBP and EUR selling by this segment further trimmed net outright longs for these investors. Aggregate shifts elsewhere for leveraged investors were quite modest.

- In the asset manager space, trends were mixed. The largest shifts came via EUR and GBP selling, but the outright EUR long remains large.

- AUD shorts were curbed, but again this segment remains comfortably net short the A$.

Table 1: CFTC Positioning - Weekly Change & Outright Positions By Currency & Investor Type

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | -19709 | -31280 | 2793 | 75119 |

| EUR | -2427 | 4724 | -16883 | 382871 |

| GBP | -8125 | 45410 | -4981 | -63439 |

| AUD | -1987 | -13997 | 4776 | -49183 |

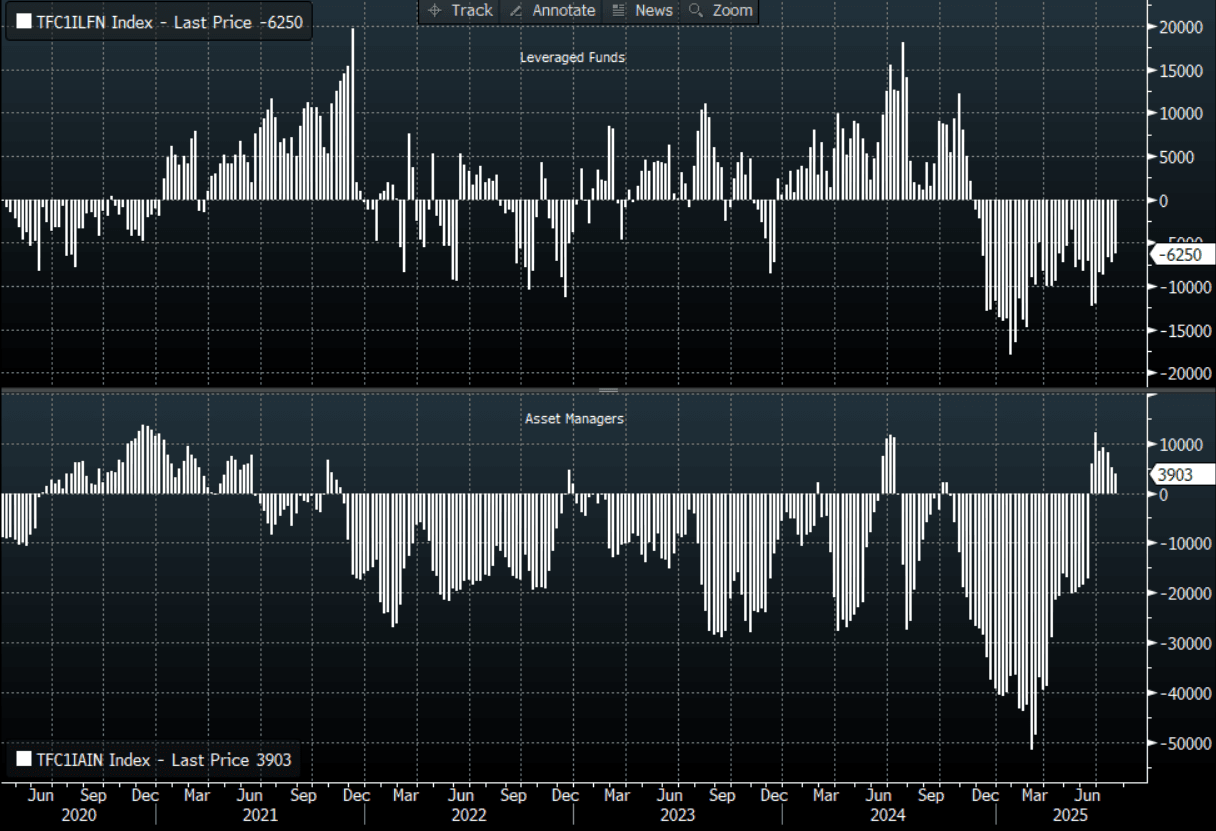

| NZD | 1078 | -6250 | -1131 | 3903 |

| CAD | -2445 | -32170 | -2377 | -50182 |

| CHF | 1176 | -1585 | -266 | -34034 |

| MXN | -2243 | 6907 | 4960 | 43333 |

Source: Bloomberg Finance L.P./MNI

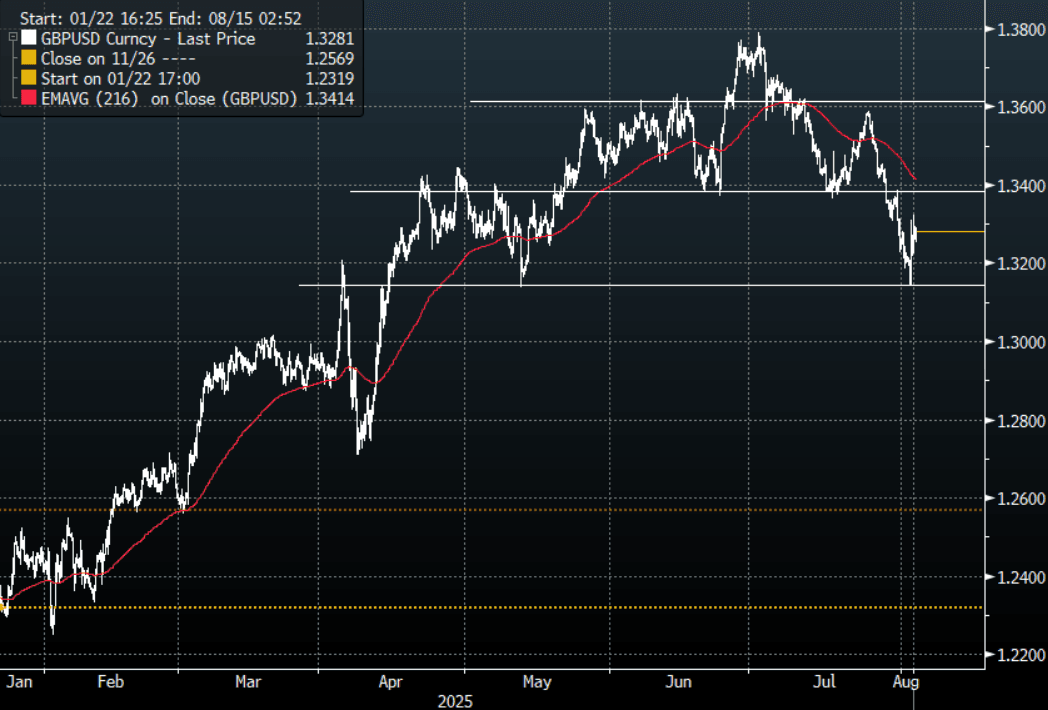

FOREX: Asia FX Wrap - Market Returns To Selling USD's

The BBDXY has had a range of 1209.26 - 1211.89 in the Asia-Pac session, it is currently trading around 1209, -0.11%. The USD, with a huge rejection of the 1220/1230 area on Friday, had a knee-jerk reaction lower to the huge move in US rates as the market's view on growth and interest rate cuts is re-evaluated. With US Equities now beginning to look vulnerable to a potential reappraisal of the growth outlook, the USD’s utilisation as a safe haven will again come back into the conversation. While the USD has fallen over 10% this year its role as a safe haven has come squarely into question, should the correction lower in risk begin to expand this premise will again be tested.

- EUR/USD - Asian range 1.1551 - 1.1596, Asia is currently trading 1.1579. The pair has bounced nicely off the important 1.1300/1.1400 area. There should be sellers initially towards 1.1650/1.1700 as the market decides how to trade the USD.

- GBP/USD - Asian range 1.3254 - 1.3293, Asia is currently dealing around 1.3285. This pair bounced nicely off the 1.3100/1.3200 support area. I would suspect sellers would be around on a bounce back towards 1.3400 initially.

- USD/CNH - Asian range 7.1801 - 7.1958, the USD/CNY fix printed 7.1395, Asia is currently dealing around 7.1800. Sellers should be around on bounces while price holds below the 7.2200/2500 area and the PBOC manages the fix lower. Above 7.2500 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.35%, Gold $3361, US 10-Year 4.243%, BBDXY 1209, Crude Oil $67.16

- Data/Events : Spain Unemployment, EZ Sentix Investor Confidence,

Fig 1: GBP/USD Spot 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Bounces Into The Fix, Demand Fails Towards 148.00

The Asia-Pac USD/JPY range has been 147.06 - 147.91, Asia is currently trading around 147.60, +0.12%. USD/JPY reacted to the capitulation in US yields and had a kneejerk move lower. The JPY got the double whammy of the move in rates and as a safe haven as risk wobbled off its highs. Price moved very quickly away from the pivotal 151/152 area much to the relief of Institutional JPY longs and the BOJ. The Pair opens in Asia testing its first support around 147.00, the more important level will be around 145.00. CFTC Data shows leveraged accounts had started to aggressively build Yen shorts last week so this quick move lower would be a bitter pill to swallow. A move sub 145.00 would turn momentum lower once more, until then the 145.00-151-00 range should dominate. USD/JPY moved higher into the Japanese fix, I suspect the price will find it tough back towards 148.50 initially.

- News flow has seen focus on the fiscal outlook, with the following headlines crossing. "ISHIBA: IMPLEMENTATION OF SUBSIDIES DEPENDS ON TALKS W PARTIES" - BBG, along with "*CDP'S NODA: TO DISCUSS SALES TAX CUT W OTHER OPPOSITION PARTIES, and "ISHIBA: MUST MULL HOW SALES TAX CUT MAY IMPACT YIELDS, TRUST" - BBG.

- Otavio Costa on X: “ The yen just recorded its biggest one-day gain against the US dollar since December 2022, when the BoJ loosened its yield curve control and allowed 10-year yields to rise. This isn’t just a one-off move, in my view, it’s part of a broader fiscal survival response. The reality is that both the US dollar and interest rates must come down, in my opinion. This kind of fiscal and monetary adjustment isn’t optional — it’s the last viable path to avoid the US economy hitting a debt wall.”

- Options : Close significant option expiries for NY cut, based on DTCC data: 149.50($752m), 150.00($1.16b), 150.50($967m).Upcoming Close Strikes : 147.65($1.14b Aug 7) - BBG.

- CFTC data shows asset managers surprisingly added slightly to their JPY longs +75119( Last +72326), while leveraged funds aggressively added to their newly built short JPY position -31280(Last -11571).

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Finds Some Demand As Risk Stabilises In Asia

The AUD/USD has had a range of 0.6462 - 0.6484 in the Asia- Pac session, it is currently trading around 0.6483, +0.14%. US Yields collapsed in response to the NFP data which sparked a kneejerk response lower in the USD. This was also a very bad day for US stocks which finally look to be pulling back from elevated levels. The question for the AUD going forward is does the USD see sellers quickly return in response to the move in rates, or can the USD rise from the ashes and return as a safe haven. The AUD bounced nicely off the 0.6400 area but I suspect sellers again back towards 0.6500/50 initially as risk wobbles and the market wrestles about what to do with the USD.

- AUSTRALIAN DATA: MI Underlying Inflation Gauge Rises Signalling Possible Trough. The Melbourne Institute headline inflation gauge for July showed a material increase to 2.9% y/y from 2.4% in June as it rose 0.9% m/m. Its trimmed mean measure rose 0.8% m/m to be up 1.9% y/y from 1.2%, the highest since January. This can lead the monthly CPI trimmed mean by up to 6 months and thus could be signalling that it troughed in June around the bottom of the RBA’s 2-3% target band and may rise in coming months. The headline inflation gauge has less signal to it. Currently the RBA remains focussed on quarterly CPI data but a more complete monthly series will be released in November.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6465(AUD727m), 0.6450(AUD402m). Upcoming Close Strikes : 0.6600(AUD1.97b Aug 7), 0.6800(AUD1.72b Aug 7) - BBG

- CFTC Data shows Asset managers reduced their shorts slightly -49183(Last -53959), the Leveraged community added to their own shorts -13997(Last -12010).

- AUD/JPY - Asia-Pac range 95.13 - 95.82, Asia is trading around 95.70. The pair failed on multiple attempts above 97.00 and has moved swiftly back to test its first support around the 95.50 area. With risk having a huge reversal lower last week the headwinds for JPY crosses are growing and should risk remain under pressure I suspect bounces will initially be met with supply.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap - NZD/USD Consolidates Just Above 0.5900

The NZD/USD had a range of 0.5903 - 0.5923 in the Asia-Pac session, going into the London open trading around 0.5920, +0.03%. US Yields collapsed in response to the NFP data which sparked a kneejerk response lower in the USD. This was also a very bad day for US stocks which finally look to be pulling back from elevated levels. The question for the NZD going forward is does the USD see sellers quickly return in response to the move in rates, or can the USD rise from the ashes and return as a safe haven. NZD/USD bounced nicely off its 0.5850 support but would suspect sellers would return on any bounce back toward 0.6000 initially as the market decides how best to trade the USD.

- “AUCKLAND JULY AVERAGE HOUSE PRICE FALLS 2.4% Y/Y: BARFOOT" - BBG

- NEW ZEALAND: Labour Market Data Likely Deteriorated In Q2. The focus of the week will be the Q2 labour market data published on Wednesday. It is expected to show that it weakened in the quarter after some signs of stabilisation in Q1. The unemployment rate is forecast to rise 0.2pp to 5.3% more than the RBNZ’s 5.2% May projection. If the data print is as weak as or weaker than the Bloomberg consensus, then a rate cut on August 20 is likely.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5970(NZD3496m Aug 7). - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +3903(Last +5034), the Leveraged community reduced their shorts slightly -6250(Last -7328).

- AUD/NZD range for the session has been 1.0930 - 1.0959, currently trading 1.0950. The Cross continues to consolidate on a 1.09 handle as the pair tries to build some momentum to move higher.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Equities Look Through Poor US Data

As the market digested the poor jobs report from the US, markets appeared to have found a silver lining and extrapolated rate cuts. China and the KOSPI ignored the falls in Japan to post modest gains as South East Asian markets. In Korea, the KOSPI received a boost on comments that the ruling Democratic Party is reviewing its position on capital gains tax whilst China's tech stocks got a boost from news that US chip exports may be delayed.

- China's Hang Seng has started the week on a positive footing, rising +0.50% whilst onshore bourses were mixed. The CSI 300 is unchanged on the day along with the Shenzhen Comp and the Shanghai Comp has had a mildly positive start, rising +0.20%.

- Taiwan's TAEIX is lower by -0.65%

- The KOSPI is one of the better regional performers, rising +0.95%.

- In Malaysia, the FTSE KLCI has a very strong finish to Friday but has given some of those gains back, falling -0.33%.

- The Jakarta Composite had a very strong July but is off -0.35% to start the week.

- The FTSE Straits Times in Singapore is up +0.80% whilst the PSEi in the Philippines is down -0.45%.

- India's NIFTY 50 finished down last week yet has seen well known EM investor Mark Mobius calling Indian stocks a 'buy' as the tariff battle continues.

ASIA STOCKS: Mostly Outflows At The End Of Last Week, Taiwan Still Positive

At the end of last week, only Taiwan saw positive inflows into local equities from offshore investors. South Korea saw a very sharp drop in the Kospi on Friday, down 3.88%. We are higher today, last around +1% for the index. Near term focus remains on local government tax shifts. The ruling party will reportedly make its position on capital gains tax known soon: "South Korea’s ruling Democratic Party chief Jung Chung-rae said the party will determine its position on capital gains tax as quickly as possible and inform the public." (via BBG a short while ago).

- More broadly inflow sentiment may be dictated by global equity trends. Friday's NFP report and ISM dip cast a shadow over the US equity market outlook. Futures are are higher in the first part of trade today, with Eminis up around 0.25%.

- Taiwan inflows remained positive, albeit with the 5-day rolling sum of inflows cooler that what we saw through parts of July.

- Indian outflow momentum remained strong to the end of last month. Higher tariff rates have likely weighed on sentiment. The Nifty is back at levels from mid June.

- Thailand also saw outflows on Friday, unwinding some of the recent positive inflows seen.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -549 | 931 | -5483 |

| Taiwan (USDmn) | 171 | 821 | 2516 |

| India (USDmn)* | -703 | -2000 | -11007 |

| Indonesia (USDmn) | -4 | -142 | -3753 |

| Thailand (USDmn) | -58 | 47 | -1837 |

| Malaysia (USDmn) | -3 | -89 | -2949 |

| Philippines (USDmn) | -1 | -8 | -623 |

| Total (USDmn) | -1148 | -441 | -23137 |

| * Data Up To July 31 |

Source: Bloombegr Finance L.P./MNI

OIL: Crude Slightly Lower Following OPEC Decision To Increase Output

Oil prices are slightly lower today after falling around 3% on Friday driven by growth concerns and their potential impact on energy demand. US July payrolls disappointed and showed sharp downward revisions to May/June, while a significant pickup in the US effective tariff was confirmed. In addition, OPEC increased its output target for September on the weekend. Excess supply fears have resurfaced after the market was concerned last week about the impact on supply if restrictions on Russia tightened.

- WTI is down 0.2% to $67.16/bbl today off the intraday low of $66.56 reached at the start of the session on the OPEC news. It had reached a high of $67.30. Brent is 0.3% lower at $67.84/bbl, close to today’s peak, after a trough of $67.39.

- OPEC agreed to increase output by 547kbd in September, above the 411k agreed for August. This unwinds the 2023 voluntary-cuts made as the group focuses on increasing its market share. There is still another 1.66mbd of reductions not due to be unwound until 2026 but OPEC says it is keeping its options open, according to Bloomberg.

- Goldman Sachs is not expecting any further OPEC production increases as the market is well supplied and as a result left its 2026 Brent forecast at $56/bbl and Q4 2025 at $64 (Bloomberg).

- Later final US June orders, Swiss July CPI and Spanish July unemployment print.

Gold Prices Hold Onto Post-Payroll Gains

Gold prices rose strongly on Friday as US yields and the US dollar fell following weaker-than-expected US payroll data. The increase in the US effective tariff is also adding risks to the growth outlook. Bullion started today trending lower reaching a trough of $3345.12/oz before beginning to recover. It is currently down 0.1% to $3359.6. The USD index is 0.1% lower but the 2-year yield slightly higher.

- Silver also trended down at the start of the session but after a low of $36.678 it has bounced back and is now up 0.2% to $37.108, close to the intraday high.

- Equities are mixed with the Nikkei down 1.5% but S&P e-mini up 0.4% and Hang Seng +0.5%. Oil prices are slightly lower with WTI -0.2% to $67.22/bbl. Copper is down 0.2%.

- Later final US June orders, Swiss July CPI and Spanish July unemployment print.

MNI RBI Preview - August 2025: On Hold

Hidden PDF

- We see the RBI pausing at their August meeting as the full extent of the policy changes at the June meeting are still to come.

- Inflation remains below target and is forecast to remain subdued.

- The focus turns to investments and the consumer with surveys showing both supportive.

- Uncertainty remains as to the final decision on US tariffs as the US negotiators head to India at the end of the month.

INDIA: Country Wrap: Mobius Says India a Buy

- Trump’s tariff shock is having a psychological impact on India’s market but any decline will be “a good opportunity to buy,” according to Mark Mobius of Mobius Investments. (source BBG)

- India's largest oil refiner, Indian Oil Corp., bought at least 5 million barrels of US crude and 2 million barrels of supplies from Abu Dhabi, according to traders. India's refiners have been under pressure from Washington and Europe over their purchases from Russia, with US President Donald Trump threatening to impose secondary tariffs on buyers of Russian oil. (source BBG)

- India's NIFTY 50 finished down last week yet has seen well known EM investor Mark Mobius calling Indian stocks a 'buy' as the tariff battle continues.

- The Rupee is modestly up today ahead of this week's central bank decision, rising +0.18% to 87.38

- Bonds are rallying with the 10yr at 6.33% (from Friday's close of 6.36%)

SOUTH KOREA: Country Wrap: CGT Decision Pending

- South Korea’s presidential policy chief said the country’s $350 billion investment pledge as part of the US trade deal is largely structured as loan guarantees rather than direct capital injections, seeking to ease domestic concerns over the scale and risks of the agreement. The most accurate way to understand the $350 billion is as a credit guarantee ceiling,” Kim said, referring to the role of state-backed Export-Import Bank of Korea and the Korea Trade Insurance Corp. in supporting Korean companies involved in US projects. “This isn’t about financing everything unconditionally, but about investing in projects that are commercially viable.” (source BBG)

- South Korea’s ruling Democratic Party chief Jung Chung-rae said the party will determine its position on capital gains tax as quickly as possible and inform the public. Jung said in a meeting on Monday that the debate over govt’s proposed capital gains tax reform is heating up but it’s not appropriate for lawmakers in the party to express different views openly. Jung asks lawmakers to refrain from making public statement on their views. (source BBG)

- The KOSPI is one of the better regional performers, rising +0.95%.

- The Won is up +0.46% taking it's 5-day total positive.

- Bonds have had one of their strongest days in some time, with yields up to 7bps lower on the curve. KTB 10yr at 2.76% (-7bps)

ASIA FX: MYR, THB & PHP All Up Over 1%

In South East Asia FX, we have seen decent USD losses across a number of pairs, with catch up to Friday's dollar losses in play. MYR, PHP and THB are all up over 1%, while IDR is around 0.65% firmer in the first part of Monday dealings. The move lower in US real yields on Friday has boosted sentiment, while risk appetite is also holding well with mixed equity trends throughout the region, along with higher US futures, are further supports.

- USD/THB was last near 32.45/50, which puts us back under all key EMAs. Highs on Friday were above 32.87. Recent lows in the pair were around 32.11.

- USD/PHP is back to 57.50/55, which is still above all key EMAs. The 20-day is back around 57.22. Recent highs in the pair were at 57.56.

- USD/MYR is near 4.2350, back under all key EMAs. Downside focus will be on a re-test under the 4.2000 level.

- USD/IDR was last around the 16380/85 level, against recent highs just above 16500. The 200-day is around 16233, which we haven't been able to sustain under on dips so far this year.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 04/08/2025 | 0630/0830 | *** | CPI | |

| 04/08/2025 | 0700/0300 | * | Turkey CPI | |

| 04/08/2025 | 1400/1000 | ** | Factory New Orders | |

| 04/08/2025 | 1400/1000 | ** | Factory New Orders | |

| 04/08/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 04/08/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 05/08/2025 | 2300/0900 | * | S&P Global Final Australia Services PMI | |

| 05/08/2025 | 2300/0900 | ** | S&P Global Final Australia Composite PMI | |

| 05/08/2025 | 0030/0930 | ** | S&P Global Final Japan Services PMI | |

| 05/08/2025 | 0030/0930 | ** | S&P Global Final Japan Composite PMI | |

| 05/08/2025 | 0145/0945 | ** | S&P Global Final China Services PMI | |

| 05/08/2025 | 0145/0945 | ** | S&P Global Final China Composite PMI | |

| 05/08/2025 | 0645/0845 | * | Industrial Production | |

| 05/08/2025 | 0700/0900 | ** | Industrial Production | |

| 05/08/2025 | 0715/0915 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0715/0915 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0745/0945 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0745/0945 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0750/0950 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0750/0950 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0755/0955 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0755/0955 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0800/1000 | ** | S&P Global Services PMI (f) | |

| 05/08/2025 | 0800/1000 | ** | S&P Global Composite PMI (final) | |

| 05/08/2025 | 0830/0930 | ** | S&P Global Services PMI (Final) | |

| 05/08/2025 | 0830/0930 | *** | S&P Global/ CIPS UK Final Composite PMI | |

| 05/08/2025 | 0900/1100 | ** | PPI | |

| 05/08/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1230/0830 | ** | International Merchandise Trade (Trade Balance) | |

| 05/08/2025 | 1230/0830 | ** | Trade Balance | |

| 05/08/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 05/08/2025 | 1345/0945 | *** | S&P Global Services Index (final) | |

| 05/08/2025 | 1345/0945 | *** | S&P Global US Final Composite PMI |