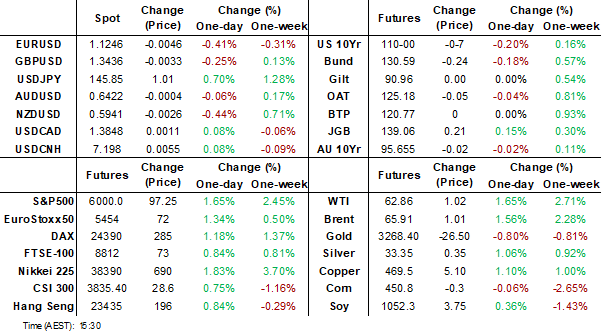

MNI EUROPEAN MARKETS ANALYSIS: USD Extends Recovery

- US equity futures are up strongly, buoyed by better Nvidia results and the US trade court ruling against Trump's reciprocal tariffs. The US Administration has already stated it will appeal the decision.

- The USD recovery has extended, while US Tsy yields are higher as well.

- The BoK cut rates as expected, with further easing likely.

- Later the Fed’s Barkin, Goolsbee, Kugler and Daly and BoE’s Bailey appear. Revised Q1 US GDP and jobless claims print.

MARKETS

US TSYS: Asia Wrap - Yields Extend Higher

The TYM5 range has been 109-27+ to 110-07+ during the Asia-Pacific session. It last changed hands at 110-01, down 0-06 from the previous close.

- The US 2-year yield has edged higher, dealing around 4.01%, up 0.02 from its close.

- The US 10-year yield has extended higher, dealing around 4.50%, up 0.02 from its close.

- (Bloomberg) - “The rallies in risk assets are gathering pace despite the US administration announcing it will appeal the decision, setting aside any concerns that the president might be determined to impose these measures in the longer term.”

- “This excitement is understandable in the short term, because the risk scenarios surrounding the situation are extremely unclear -- and could range from a modest hiccup for Trump’s tariffs to a serious confrontation between the administration and the judiciary. For today, investors will focus on the immediate story that tariffs are being switched off -- and worry about any fallout when that becomes apparent.”

- "The court gave the administration 10 days to "effectuate" its order, but didn't provide any specific directions of steps it must take to unwind the tariffs."(BBG)

- The 10-year looks likely to see supply on any dips in yield in the short-term, should yields hold above 4.35/40% the target looks to be the 4.75/80% area.

JGBS: Cheaper With US Tsys, Nvidia Beats & Trump Tariff Uncertainty

JGB futures are stronger, +12 compared to settlement levels, hovering near Tokyo session highs.

- Cash US tsys are 2-4bps cheaper in today's Asia-Pac session.

- Eminis and Nasdaq futures are stronger after Nvidia printed better-than-expected results, despite headwinds regarding chip curbs to China.

- Bloomberg - "There's an apparent irony that US stock futures, which were already higher than they were when Trump's 'Liberation Day' tariffs were announced, are now rallying on news that they've been blocked by a US court. The decision, for as long as it stands, is clearly good news for the US economy, though it doesn't say much about the state of US policymaking and it won't help businesses make decisions."

- Japan’s consumer confidence index rose to 32.8 in May, compared with the median estimate of 31.8.

- Cash JGBs are flat to 4bps cheaper across benchmarks, with a steeper curve. The benchmark 40-year yield is 3.4bps higher at 3.39% versus its high of 3.68%.

- Swap rates are 1bp lower to 4bps higher. Swap spreads are mixed.

- Tomorrow, the local calendar will see Jobless Rate, Job-To-Applicant Ratio, Tokyo CPI, Industrial Production, Housing Starts and Retail Sales data alongside 2-year supply.

JAPAN DATA: Local Investors Cool Offshore Bond Buys, Sell Equities

Offshore weekly investment trends were mixed for Japan in the week ending May 23, see the table below. Most notable was the slowdown in offshore bond purchases by local Japan investors. Whilst outflows for this segment were still positive, it was well down on the pace seen in the prior two weeks (with a combined ¥4.763trln in net purchases of offshore bonds). Local investors also sold overseas equities for the second consecutive week. Still, since mid March, outflows to overseas stocks are above ¥5.5trln, so it is only a small unwind in recent weeks.

- In terms of inflows into Japan markets from offshore investors, we saw net selling of local bonds. This marked the fourth straight week of such outflows. We would note though cumulative inflows since the start of 2025 are still quite strong for this segment.

- Offshore investors continued to buy local stocks, marking the eighth straight week of net buying for this segment.

Table 1: Japan Offshore Weekly Investment Flows

| Billion Yen | Week ending May 23 | Prior Week |

| Foreign Buying Japan Stocks | 309.3 | 715.3 |

| Foreign Buying Japan Bonds | -334.4 | -225 |

| Japan Buying Foreign Bonds | 92.0 | 2833.9 |

| Japan Buying Foreign Stocks | -524.7 | -241.4 |

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Holding Weaker Despite Weaker Capex, Trump Tariff HLs In Focus

ACGBs (YM -2.0 & XM -3.0) are holding in negative territory.

- Q1 private capital expenditure volumes were weaker than expected, falling 0.1% q/q to be down 0.5% y/y driven by a contraction in machinery & equipment investment. Q4 was revised up to +0.2% q/q, there appears to be a trend of upward revisions to the previous quarter as was also the case with construction. Q1 GDP prints on June 4, with the inventory and net export components released on June 3, but currently it is looking soft.

- Cash US tsys are 2-4bps cheaper in today's Asia-Pac session.

- (Reuters) - A U.S. federal court on Wednesday blocked President Donald Trump's "Liberation Day" tariffs from going into effect, ruling that the president overstepped his authority by imposing across-the-board taxes on imports from nations that sell more to the United States than they buy."

- Cash ACGBs are 2-3bps cheaper with the AU-US 10-year yield differential at -15bps.

- The bill strip has cheapened, with pricing -2 to -3.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in July is given a 54% probability, with a cumulative 68bps of easing priced by year-end.

- Tomorrow, the local calendar will see Retail Sales, Private Sector Credit and Building Approvals data.

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond tomorrow.

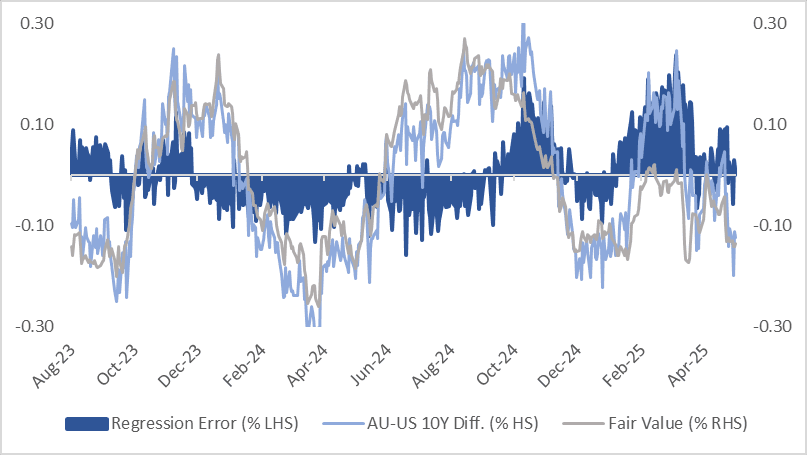

AUSSIE BONDS: AU-US 10Y Diff Sits In Bottom Half Of Range

The AU-US 10-year cash yield differential currently stands at -14bps, positioned in the bottom half of the +/- 30bps range that has largely held since November 2022.

- A simple regression of the 10-year yield differential against the AU-US 1-year forward 3-month swap rate (1Y3M) differential over the past year suggests the current spread is at fair value.

- The 1Y3M differential, a key gauge of expected relative policy trajectories over the next 12 months, has traded within a 40bp range this year and is currently near the bottom of the range at ~-27bps.

- In early February, the 1Y3M differential had declined approximately 95bps since mid-September 2024, falling from +60bps to -35bps.

Figure 1: AU-US Cash 10-Year Yield Differential Vs. Fair Value (%)

Source: MNI - Market News / Bloomberg

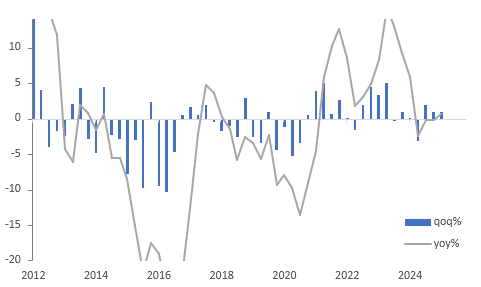

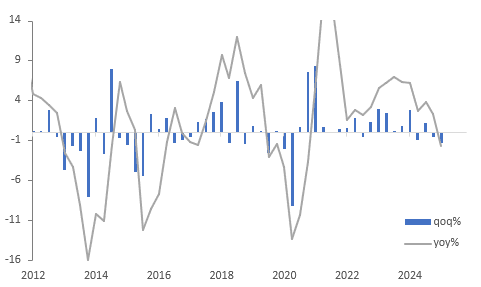

AUSTRALIA DATA: Weak Equipment Capex Drives Q1 Investment Lower

Q1 private capital expenditure volumes were weaker than expected falling 0.1% q/q to be down 0.5% y/y driven by a contraction in machinery & equipment investment. Q4 was revised up to +0.2% q/q, there appears to be a trend of upward revisions to the previous quarter as was also the case with construction. Q1 GDP prints on June 4 with the inventory and net export components released on June 3, but currently it is looking soft.

- Q1 building & structures investment rose 0.9% q/q, third consecutive quarterly increase, to be up 0.6% y/y after falling 0.2% y/y. It was driven by mining projects in oil & gas, gold, and other metal ores with capex up 1.7% q/q while non-mining was +0.4%.

- Plant & equipment fell 1.3% q/q after -0.6%q/q to be down 1.8% y/y after rising 2.3% y/y in Q4. The weakness was due to the non-mining sector (-2.0% q/q), while mining rose 2.4% q/q. In terms of non-mining, the ABS notes that services invested in less IT and vehicles.

- Investment intentions for FY25 were revised up 2.2% and for FY26 +5.6%.

Australia capex building & structures %

Source: MNI - Market News/ABS

BONDS: NZGBS: Closed With A Bear-Flattener But Off Worst Levels

NZGBs closed showing a bear-flattener, with yields 2-6bps higher. NZGBs did, however, finish off the session’s worst levels.

- Today’s supply saw solid demand, with cover ratios of 3.27x (May-36) to 3.54x (May-30).

- Swap rates closed 5-7bps higher.

- RBNZ Governor Hawkesby just spoke with Bloomberg today and reiterated that the message at yesterday’s press conference was not to assume that a July rate cut is programmed into the MPC’s thinking.

- Elevated uncertainty means that there could be many different paths from here, which is why the central bank presented different scenarios in its May Monetary Policy Statement.

- ANZ business confidence fell to 36.6 in May from 49.3, the lowest since July, while the outlook moderated to 34.8 from 47.7. The survey suggests a gradual, soft recovery with higher costs difficult to pass through, which ANZ believes will allow the RBNZ to cut rates to 2.5%.

- RBNZ-dated OIS pricing is 10-13bps higher across meetings compared to yesterday’s pre-RBNZ decision levels.

- Markets had fully priced in yesterday’s 25bp cut ahead of the decision, with a total of 64bps of easing expected by November 2025. That has now adjusted to 50bps, inclusive of yesterday’s move.

- Tomorrow, the local calendar will see ANZ Consumer Confidence data.

RBNZ: A July Rate Cut Not “Programmed In”

RBNZ Governor Hawkesby just spoke with Bloomberg and reiterated that the message at yesterday’s press conference was not to assume that a July rate cut is programmed into the MPC’s thinking. Elevated uncertainty means that there could be many different paths from here, which is why the central bank presented different scenarios in its May Monetary Policy Statement. For instance if current trade events result in higher costs and NZ price pressures rise then the OCR is unlikely to move much from where it is in the ‘neutral zone’ but if weaker global demand reduces inflation then there is room to cut. Thus he said that the MPC will make “considered, data dependent steps” and that markets should also follow developments closely.

NEW ZEALAND: Soft Economy But Outlook Improved Later In May

ANZ business confidence fell to 36.6 in May from 49.3, the lowest since July, while the outlook moderated to 34.8 from 47.7. ANZ notes though that the breakdown of responses indicates that the picture is not as soft as the month averages suggest as they improved in the latter part of the month with positive news on trade talks and are “well off their late-April lows”. Price/cost components generally fell in May. The survey suggests a gradual, soft recovery with higher costs difficult to pass through, which ANZ believes will allow the RBNZ to cut rates to 2.5%.

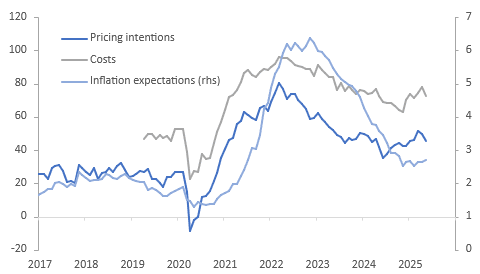

- Inflation expectations were stable in May at 2.7% but are 0.2pp higher than the recent trough. Pricing intentions fell 4 points to 45.4, the lowest since December, but retail posted its highest reading since March 2024. Costs 3-months out moderated 5 points to 72.8, with the decline across sectors except construction.

NZ ANZ business price/cost components

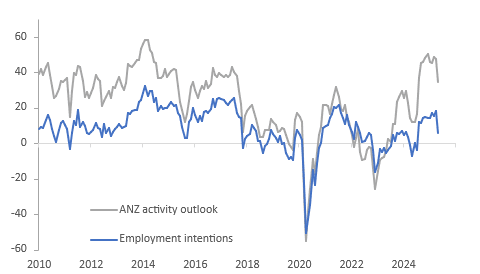

- Employment intentions remain positive consistent with a stabilisation in the labour market but fell 12 point to 6, the lowest since July, in line with little growth. Thus it is unsurprising that wage expectations 12-months ahead moderated 6 points.

- Activity compared to a year ago, which has a good correlation with GDP, fell 6 points with all sectors down signalling that Q2 was soft.

- Export & investment intentions, profit expectations and construction sentiment were all lower.

NZ ANZ business survey

Source: MNI - Market News/LSEG

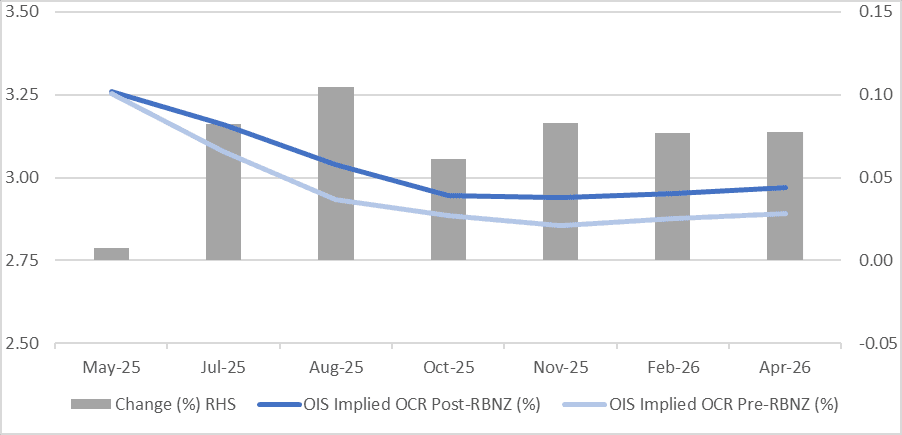

STIR: RBNZ-Dated OIS Extends Post-RBNZ Firming

RBNZ-dated OIS pricing is 10-13bps higher across meetings compared to yesterday’s pre-RBNZ decision levels.

- RBNZ Governor Hawkesby just spoke with Bloomberg today and reiterated that the message at yesterday’s press conference was not to assume that a July rate cut is programmed into the MPC’s thinking.

- Elevated uncertainty means that there could be many different paths from here, which is why the central bank presented different scenarios in its May Monetary Policy Statement.

- For instance, if current trade events result in higher costs and NZ price pressures rise, then the OCR is unlikely to move much from where it is in the ‘neutral zone’, but if weaker global demand reduces inflation, then there is room to cut. Thus, he said that the MPC will make “considered, data-dependent steps” and that markets should also follow developments closely.

- Markets had fully priced in yesterday’s 25bp cut ahead of the decision, with a total of 64bps of easing expected by November 2025. That has now adjusted to 50bps, inclusive of yesterday’s move.

Figure 1: RBNZ Dated OIS Today vs. Pre-RBNZ Levels (%)

Source: MNI - Market News / Bloomberg

FOREX: Asia FX Wrap - The USD Correction Extends In Asia

The BBDXY has had a range of 1219.81 - 1225.58 in the Asia-Pac session, it is currently trading around 1223. Ben Hunt on X: “The initial USD positive reaction to the tariff block is weird to me. Either the Supreme Court reverses the trade court ruling and we’re back to where we were (only worse) or they don’t reverse and Trump initiates the biggest constitutional crisis of the past 70 years. Both are intensely USD negative. https://x.com/EpsilonTheory/status/1927912996174549490

- EUR/USD - Asian range 1.1210 - 1.1297, Asia is currently trading 1.1250. EUR has had a big drop during the Asian session. The news this morning tipped the USD buying over the edge. Dips back to 1.1000/100 should continue to find support.

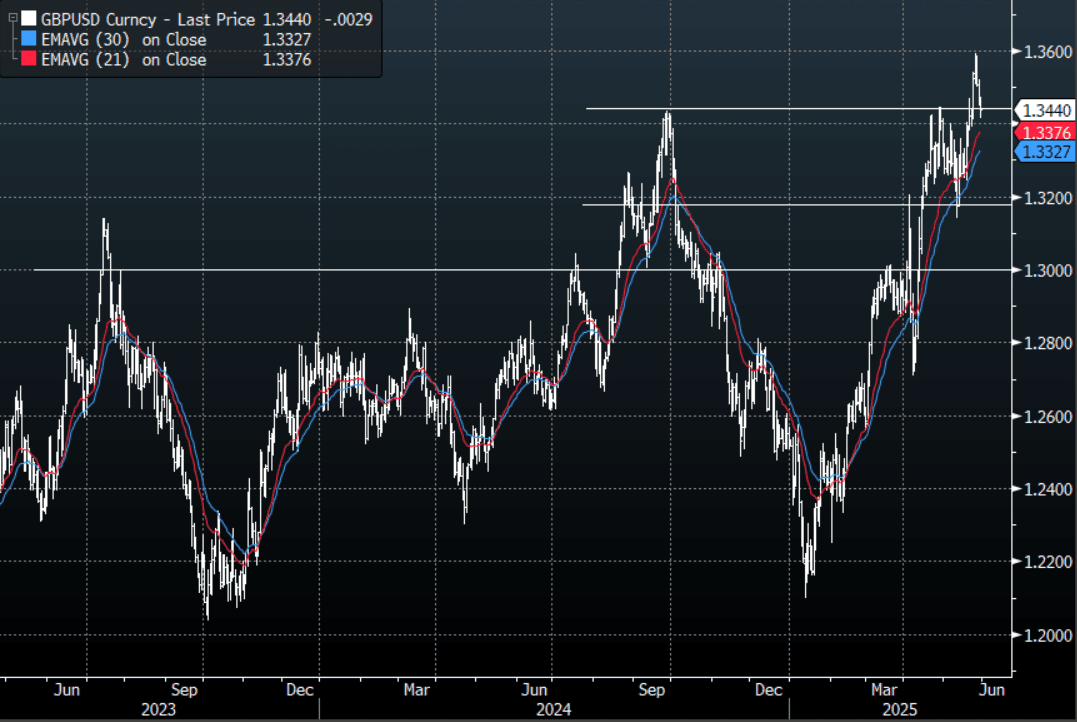

- GBP/USD - Asian range 1.3416 - 1.3472, Asia is currently dealing around 1.3445. The GBP could not hold above the pivotal 1.3500 area for now. Look for support to return back towards the 13300/3400 area.

- USD/CNH - Asian range 7.1908 - 7.2087, the USD/CNY fix printed 7.1907. Asia is currently dealing around 7.1975. Sellers should be found on a bounce back towards the 7.2200 area again. Andreas Steno Larsen on X : The elephant in the room. USDCNH needs to go to 6.80 at least. https://x.com/AndreasSteno/status/1926115935200440525

- Cross asset : SPX +1.60%, Gold $3270, US 10-Year 4.50%, BBDXY 1223, Crude oil $62.74

Data/Events : Spain Retail Sales, Italy Consumer Confidence & Industrial Sales

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

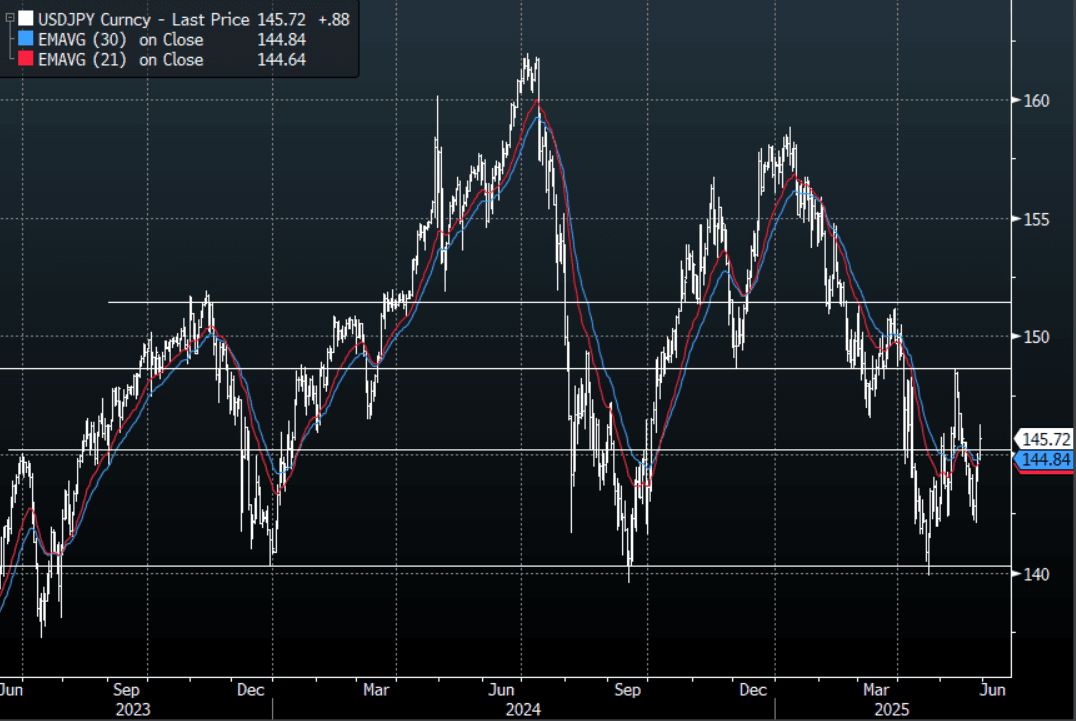

JPY: Asia Wrap - The Correction Testing The 146.00 Resistance

The Asia-Pac USD/JPY range has been 144.76 - 146.28, Asia is currently trading around 145.70. USD/JPY stayed well supported all through our day, what looks like overextended positioning is being challenged.

- (Bloomberg) - “There’s an apparent irony that US stock futures, which were already higher than they were when Trump’s ‘Liberation Day’ tariffs were announced, are now rallying on news that they’ve been blocked by a US court. The decision, for as long as it stands, is clearly good news for the US economy, though it doesn’t say much about the state of US policymaking and it won’t help businesses make decisions.”

- Ben Hunt on X: “ The initial USD positive reaction to the tariff block is weird to me. Either the Supreme Court reverses the trade court ruling and we’re back to where we were (only worse) or they don’t reverse and Trump initiates the biggest constitutional crisis of the past 70 years. Both are intensely USD negative. https://x.com/EpsilonTheory/status/1927912996174549490

- There was a definitive demand for USD’s all through our session. This has seen USD/JPY challenge its resistance around 146.00, the JPY bulls need this move to top out somewhere around here.

- The market has been very confident of a move lower in USD/JPY but with positioning quite large now the risk of pullbacks does increase. The market is currently testing the resistance around the 146.00 area, there should be sellers around these levels but a close back above 146.00/50 would signal the retracement could have further to go.

Options : Close significant option expiries for NY cut, based on DTCC data: 145.00($2.14b), 143.00($1.98b), 144.00($1.67b). Upcoming Close Strikes : 143.00($3.34b May 30), 140.00($2.78b May 30).

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

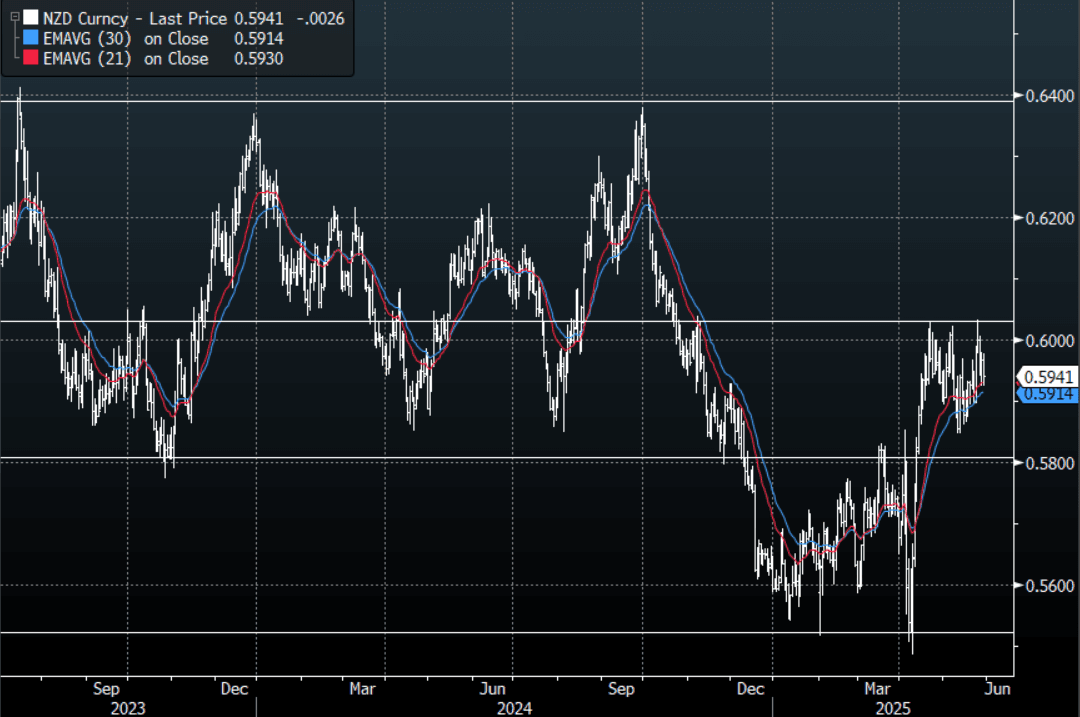

NZD: Asia Wrap - Can't Ignore The USD Strength

The NZD/USD had a range of 0.5925 - 0.5977 in the Asia-Pac session, going into the London open trading around 0.5940. The NZD has fallen pretty hard in our session as it seems to be catching up to the general USD move. It seemed to brush off the USD strength overnight but the extension this morning looked like risk moving higher was a bridge too far.

- NEW ZEALAND Data: Soft Economy But Outlook Improved Later In May. ANZ business confidence fell to 36.6 in May from 49.3, the lowest since July, while the outlook moderated to 34.8 from 47.7.

- RBNZ Governor Hawkesby spoke with Bloomberg today and reiterated that the message at yesterday's press conference was not to assume that a July rate cut is programmed into the MPC's thinking.

- Elevated uncertainty means that there could be many different paths from here, which is why the central bank presented different scenarios in its May Monetary Policy Statement.

- The NZD continues to trade in a 0.5850/0.6050 range, the hawkish slant from the RBNZ probably saw a portion of the new shorts added last week by leveraged accounts pared back overnight.

- The support back towards 0.5800 has held very well, and while this continues to hold expect buyers to be around on dips. A break above 0.6050 is needed to provide the spark for the next leg higher.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5975(NZD440m). Upcoming Close Strikes : 0.6100(NZD375m June 3)

AUD/NZD range for the session has been 1.0764 - 1.0821, currently trading 1.0815. NZD looks to have played catch up in Asia this morning. A top looks to have been put in place now just above 1.0900, the market will have been looking for a more dovish tone from the RBNZ yesterday and AUD/NZD should now see supply on bounces. The first target is around 1.0650.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

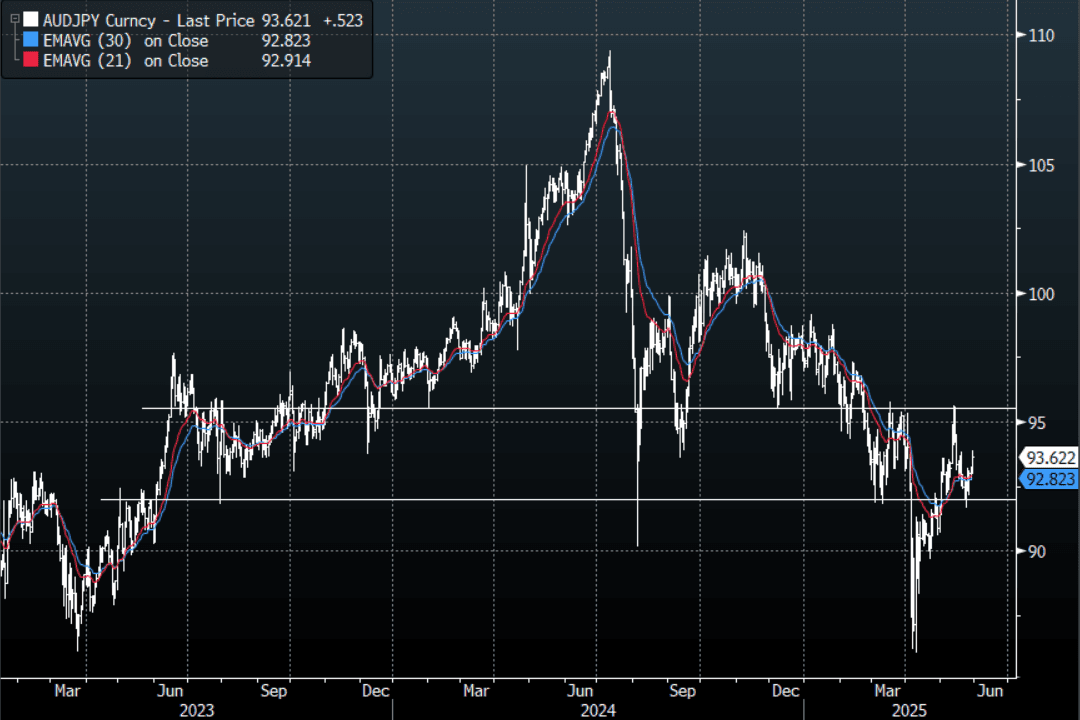

AUD: Asia Wrap - AUD Outperforms In The Crosses

The AUD/USD has had a range of 0.6407 - 0.6436 in the Asia- Pac session, it is currently trading around 0.6425. The AUD has outperformed in the crosses retracing some of its recent moves.

- AUSTRALIA DATA: Weak Equipment Capex Drives Q1 Investment Lower. Q1 private capital expenditure volumes were weaker than expected falling 0.1% q/q to be down 0.5% y/y driven by a contraction in machinery & equipment investment.

- (AFR) "Inflation is not a barrier to another cash rate cut as soon as the next Reserve Bank of Australia board meeting in July, as new figures showed price pressures remained within the central bank's target band last month."

- Most of the possible month end corporate USD buying would have been transacted overnight, but there could still be some residual to get done today.

- Expect buyers to continue to be around on dips while the support in the AUD holds, a close back below 0.6300/50 would start to challenge the newly formed uptrend. A break above 0.6550 and the move higher could begin to accelerate.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6555(AUD389m). Upcoming Close Strikes : 0.6400(AUD 786m June 2)

AUD/JPY - Today's range 92.98 - 93.87, it is trading currently around 93.60. The pair has surged this morning above the 93.00 area that has capped price in the last couple of days. If this break is sustained and risk holds onto its gains it implies this pair can once again head higher with the focus turning back towards the 96.00 area.

Fig 1: AUD/JPY spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Mostly Higher, Led By Tech Plays Post Nvidia & Tariff News

Regional Asia Pac equity markets are mostly tracking higher. Several positives are in play, with positive spill over evident from US equity futures. Late Wednesday in the US we had Nvidia results, which were better than expected and renewed tech/AI optimism. This helped US equity futures re-open higher. Not long after headlines crossed that the US trade court had ruled Trump's reciprocal tariffs were illegal.

- In latest dealings, Nasdaq futures are up around 1.9%, putting the index at fresh highs back to Feb. Eminis are up close to 1.55%. The Trump administration has already stated it will appeal the decision, but for the moment broader risk appetite is staying positive.

- South Korean stocks continue to outperform, the Kospi last up +1.75%. The tariff news, tech/AI sentiment (post Nvidia), along with corporate value up optimism, are all combining to drive these strong gains.

- The Taiex is also higher, up +0.55% at the time of writing, while Japan benchmarks are up +1.4% for the Topix and +1.6% for the NKY.

- Hong Kong and China markets are also firmer, albeit with gains of around 0.65% to the lunchtime break.

- US-China news flow has mostly been negative, with reports of further tech related curbs in the software space (related to semiconductor manufacturing), while the NYTs reported other export related restrictions. Visas for China students will also reportedly start to be revoked. These moves haven't weighed on aggregate share performance though.

- In SEA, market moves are more muted, with Singapore and Malaysian markets down modestly. Thailand shares are up close to 0.80%.

ASIA STOCKS: South Korean Inflows Firmer, Muted Trends Elsewhere

Asian equity flows saw positive momentum into South Korea yesterday, with nearly $500mn in net inflows from offshore investors. This brings the net inflows for the past 5 trading days back into positive territory. Outside of positive Indian inflows, flows elsewhere were fairly muted.

- For South Korea, the turnaround in global tech indices has certainly been a positive of late, while onshore there is growing optimism around fresh corporate reforms, which could boost undervalued companies. Value related stocks have performed well in recent sessions. The Kospi is up a further 1.75% so far today, with the dovish BoK rate cut and the tariff court ruling in the US other positives.

- Taiwan stocks inflows have certainly slowed this past week, but at over $8bn for May to date, we around record highs in terms of offshore inflows in a single month.

Table 1: Asian Offshore Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 461 | 274 | -11066 |

| Taiwan (USDmn) | 25 | 133 | -10317 |

| India (USDmn)* | 112 | -1 | -10279 |

| Indonesia (USDmn) | 84 | 165 | -2726 |

| Thailand (USDmn) | 10 | 6 | -1709 |

| Malaysia (USDmn) | -23 | -135 | -2259 |

| Philippines (USDmn) | 12 | 4.3 | -245 |

| Total (USDmn) | 681 | 446 | -38601 |

| * Data Up To May 27 |

Source: MNI - Market News/Bloomberg

OIL: US Court Tariff Ruling Eases Oil’s Demand Worries, EIA Data Out Later

Crude is up sharply during today’s APAC session following a rise of around 1.5% yesterday. News that the US Court of International Trade blocked most of the proposed tariffs saying that the President had overstepped his authority has boosted risk appetite and driven a relief rally in oil prices. The market had been concerned that increased protectionism would weigh on global energy demand. The USD index is up 0.2% after 0.3% on Wednesday.

- WTI is up 1.3% to $62.66/bbl, close to the intraday high of $62.72, and slightly above the 50-day EMA. A clear break above would open $64.19, 21 May high. The benchmark is up 1.8% this week and at its highest since May 21. But OPEC’s meeting on the weekend could push prices down again if another large output increase is decided for July.

- Brent is now 1.4% higher this week after rising 1.1% to $65.64 today, just short of resistance at $66.05, 50-day EMA.

- Most of the US tariffs have now been put on hold with the appeal possibly to be heard by the US Supreme Court. A lengthy national security review may be required for tariffs to go ahead. Either way there is likely to be an extended delay.

- Attention will be on the official EIA inventory data after Bloomberg reported that US crude inventories fell 4.24mn barrels last week, according to people familiar with the API data. But gasoline demand will also be a key part of the release.

- Later the Fed’s Barkin, Goolsbee, Kugler and Daly and BoE’s Bailey appear. Revised Q1 US GDP and jobless claims print.

Gold Breaks Below Support As Risk Sentiment Improves

Gold is down 0.4% to $3274/oz during Thursday’s APAC trading after falling 0.4% yesterday. It has been pressured by the stronger US dollar (USD BBDXY +0.3%), higher US yields and better risk appetite after robust Nvidia earnings and news that a US Court of International Trade blocked most of the proposed tariffs saying that the President had overstepped his authority. The administration has appealed the decision but for now it looks like tariffs may be on hold beyond July 8, which has reduced safe-haven interest in gold.

- Bullion fell to a low of $3245.50 following the US tariff news but has recovered somewhat since then. This is below initial support at $3284.6, 20-day EMA, which if sustained opens up $3202.9, 50-day EMA. Initial resistance is at $3365.9, 23 May high. The yellow metal is currently down 2.5% this week and 0.4% in May.

- Most of the US tariffs have now been put on hold with the appeal possibly to be heard by the US Supreme Court. There is the chance that duties already paid will have to be refunded and that a lengthy national security review will be required for tariffs to go ahead. Either way there is likely to be an extended delay which will reduce gold’s appeal as a safe-haven asset.

- Equities have rallied on the US tariff news with the S&P e-mini up 1.6% and Nikkei +1.6%. Commodity prices are also higher with WTI +1.3% to $62.63, copper +0.3% and silver +0.6% to $33.20.

- Later the Fed’s Barkin, Goolsbee, Kugler and Daly and BoE’s Bailey appear. Revised Q1 US GDP and jobless claims print.

BOK: Still In Easing Mode, Scope For Larger Cuts, But Outlook Uncertain

The BoK cut rates by 25bps, as widely expected, taking the policy rate to 2.50%. It maintained a clear easing bias noting in its statement: "the Board will maintain its rate cut stance to mitigate downside risks to economic growth and adjust the timing and pace of any further Base Rate cuts while closely monitoring changes in the domestic and external policy environments and examining the resulting impact on inflation and financial stability."

- This came after the central bank slashed its growth forecast for 2025 to 0.8%, versus the 1.5% projection made in February. The 2026 projection was also nudged down, while inflation forecasts were relatively steady and hold just under 2%.

- Governor Rhee in the press conference noted today's decision was unanimous, while stating that 4 out of 6 board members see lower rates in 3 months, while 2 board members see policy rates on hold over this period.

- Rhee noted that the 2025 GDP projection doesn't reflect fiscal pledges made by the Presidential candidates (with the election to be held on June 3). In the statement BOK noted: "The future economic growth trajectory is assessed to be subject to significant uncertainty, stemming from developments in trade negotiations, government stimulus measures, and monetary policies in major economies."

- Rhee stated there was scope for larger rate cuts in the future, but this would depend on how the growth outlook evolves given the new lower projection for 2025.

ASIA FX: NEA Weaker, KRW & TWD Fall By More Than CNH

In North East Asian FX markets, the USD is better bid, with KRW and TWD falling by more than CNH. Broader USD sentiment is positive, aided by the tariff court ruling against Trump's reciprocal tariffs. The better US equity futures tone, which has been aided by the tariff news, along with Nvidia's earnings results, have also likely aided the dollar.

- USD/CNH got to highs of 7.2087, but sits back at 7.1980 in latest dealings, only a touch weaker versus end Wednesday levels in the US. Once again CNH is exhibiting a low beta with respect to broader USD shifts. In the G10 space, both JPY and CHF are underperforming, off nearly 0.60% versus the USD. CNH/JPY got just above 20.30 before selling interest emerged. Outside of the tariff/Nvidia news, US-China headlines have been negative. There are reports of further tech related curbs in the software space (related to semiconductor manufacturing), while the NYTs reported other export related restrictions. Visas for China students will also reportedly start to be revoked.

- Spot USD/KRW got to highs of 1385.35. The continued rally in onshore equities overshadowed by broader USD gains. We also had a dovish BoK 25bps cut, with further policy easing likely although Governor Rhee stated that rates were unlikely to fall sub 2% in the near term. USD/KRW sits back at 1382 now, still 0.50% weaker in won terms for the session. Governor Rhee also mentioned Asian countries have discussed FX with the US, which helped curb earlier highs.

- Spot USD/TWD is higher, but is just under the 30.00 level in latest dealings, around 0.30% weaker in TWD terms.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 29/05/2025 | 0800/1000 | ** | ISTAT Consumer Confidence | |

| 29/05/2025 | 0800/1000 | ** | ISTAT Business Confidence | |

| 29/05/2025 | 0900/1000 | BOE's Breeden opening remarks at conference on non-bank financial sector and financial stability | ||

| 29/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 29/05/2025 | 1230/0830 | * | Current account | |

| 29/05/2025 | 1230/0830 | * | Payroll employment | |

| 29/05/2025 | 1230/0830 | *** | GDP | |

| 29/05/2025 | 1230/0830 | Richmond Fed's Tom Barkin | ||

| 29/05/2025 | 1400/1000 | ** | NAR Pending Home Sales | |

| 29/05/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 29/05/2025 | 1445/1545 | BOE's Saporta panellist on hedge funds' role in recent crises | ||

| 29/05/2025 | 1500/1100 | ** | DOE Weekly Crude Oil Stocks | |

| 29/05/2025 | 1500/1600 | BOE's Bailey speech and fireside chat at Irish IAIM Dinner | ||

| 29/05/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 29/05/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 29/05/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 29/05/2025 | 1800/1400 | Fed Governor Adriana Kugler | ||

| 29/05/2025 | 2000/1600 | San Francisco Fed's Mary Daly | ||

| 30/05/2025 | 2330/0830 | ** | Tokyo CPI | |

| 30/05/2025 | 2330/0830 | * | Labor Force Survey | |

| 30/05/2025 | 2350/0850 | ** | Industrial Production | |

| 30/05/2025 | 2350/0850 | * | Retail Sales (p) | |

| 29/05/2025 | 0025/2025 | Dallas Fed's Lorie Logan | ||

| 30/05/2025 | 0130/1130 | * | Building Approvals | |

| 30/05/2025 | 0130/1130 | ** | Retail Trade | |

| 30/05/2025 | 0600/0800 | *** | GDP | |

| 30/05/2025 | 0600/0800 | ** | Import/Export Prices | |

| 30/05/2025 | 0600/0800 | ** | Retail Sales | |

| 30/05/2025 | 0630/0730 | DMO to release FQ2 (Jul-Sep) issuance ops calendar | ||

| 30/05/2025 | 0700/0900 | *** | HICP (p) | |

| 30/05/2025 | 0700/0900 | ** | KOF Economic Barometer | |

| 30/05/2025 | 0800/1000 | ** | M3 | |

| 30/05/2025 | 0800/1000 | *** | GDP (f) | |

| 30/05/2025 | 0800/1000 | *** | Bavaria CPI | |

| 30/05/2025 | 0800/1000 | *** | North Rhine Westphalia CPI | |

| 30/05/2025 | 0800/1000 | *** | Baden Wuerttemberg CPI | |

| 30/05/2025 | 0900/1100 | *** | HICP (p) | |

| 30/05/2025 | 1000/1200 | ** | PPI | |

| 30/05/2025 | 1200/1400 | *** | HICP (p) | |

| 30/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 30/05/2025 | 1230/0830 | *** | Personal Income and Consumption | |

| 30/05/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 30/05/2025 | 1230/0830 | *** | GDP - Canadian Economic Accounts | |

| 30/05/2025 | 1230/0830 | *** | Gross Domestic Product by Industry | |

| 30/05/2025 | 1230/0830 | *** | CA GDP by Industry and GDP Canadian Economic Accounts Combined | |

| 30/05/2025 | 1342/0942 | *** | MNI Chicago PMI |