MNI EUROPEAN MARKETS ANALYSIS: US Yields Lower, USD Steady

- Trump remarks were in early focus, with the President stating new tariff levels for China could be announced in 2-3 weeks. Trump reiterated his call for lower US policy rates, but stated he hasn't spoken to Powell yet but that he may have a call.

- The USD is slightly weaker against but the BBDXY index is close to Wednesday highs. US Tsy yields have drifted a little lower. Gold has rebounded after sharp losses in the past few sessions. US equity futures sit modestly in the red at this stage, as the broader risk rebound pauses somewhat.

- Later the Fed’s Kashkari speaks. US March orders, Chicago Fed index, April Kansas manufacturing index and jobless claims print. The ECB’s Lane participates in a panel and Germany’s April Ifo survey is published.

MARKETS

TYM5 has traded a little higher with a range of 110-20+ to 110.27 during the Asia-Pacific session. It last changed hands at Heading 110-27, up 0.06 from the previous close.

- The US 10-year yield is lower, dealing around 4.35%, down from its close around 4.38%

- The US 2-year yield is lower, dealing around 3.84%, down from its close around 3.87%.

- Risk has struggled to hold onto its gains leaking lower in Asia as the market looks through the Trump administration's attempts at de-escalation.

- “Minneapolis Fed President Neel Kashkari said it’s the central bank’s job to ensure tariffs don’t cause ongoing inflation.”(per BBG)

- The Department of the Treasury will auction $44 billion of an April 2032 note.

- The 10-year Yield has bounced off its support around the 4.25 area once more, the 10-year is consolidating with the range looking something like 4.25/4.50% for now.

- Data/Events : Chicago Fed Activity Index, Durable Goods Orders, Initial Jobless Claims, Existing Home sales.

JGBS: Futures Stronger After Reversing O/N Weakness, Tokyo CPI Tomorrow

JGB futures are stronger and at session highs, +16 compared to the settlement levels, after rejecting overnight weakness.

- According to MNI's Technicals Team, JGBs are holding the bulk of the recent strong bullish reversal, rejecting any test of fresh cycle lows for the M5 contract. This defies the bearish momentum studies drawn on the longer-term chart, clearing moving-average resistance to print 142.40 at the new upper level.

- Cash US tsys are 2-4bps richer in today's Asia-Pac session. After US market close, US President Trump delivered wide-ranging comments in the Oval Office. Trade/tariffs and monetary policy were among the focus points. Today's US calendar will see Chicago Fed Activity Index, Durable Goods Orders, Initial Jobless Claims and Existing Home Sales.

- Cash JGBs are modestly mixed across benchmarks, with yields 1bp higher to 2bps lower, pivoting at the 30-year.

- Today's 2-year bond auction showed improved demand. The low price came in just above the Bloomberg-surveyed forecast, while the cover ratio increased to 3.5801x, and the auction tail narrowed slightly compared to last month.

- Swap rates are 1-4bps lower, with a steeper curve.

- Tomorrow, the local calendar will see Tokyo CPI and Dept Store Sales data alongside BoJ Rinban Operations covering 3-25-year JGBs.

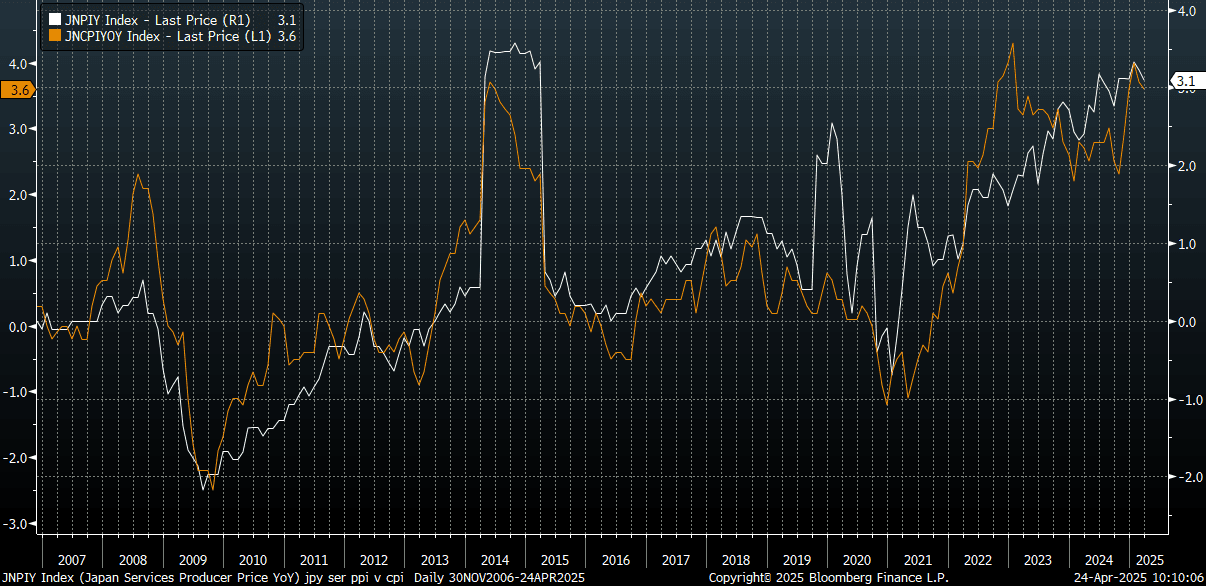

JAPAN DATA: Services PPI Slightly Firmer Than Forecast, Just Off Cycle Highs

Japan's March services PPI printed slightly above expectations at 3.1% y/y, versus 3.0% consensus. The prior outcome was revised up to 3.2% y/y (from 3.0% originally reported). The monthly change was +0.7% after a 0.1% gain in February.

- The PPI for services sits just off cycle highs. The chart below plots this metric against headline CPI (which is the orange line on the chart).

- The result will not impact BOJ thinking ahead of next week's policy meeting. There is very little priced by the market for next week's meeting, with focus on the outlook, particularly the trade/tariff backdrop and what this means for Japan and global growth. Earlier headlines from the IMF pointed to a risk in delaying further hikes from the central bank.

Fig 1: Japan Services PPI (White Line) & Japan Headline CPI (Orange Line)

Source: MNI - Market News/Bloomberg

JAPAN DATA: Local Investors Buy Offshore Bonds For First Time Since End Feb

Offshore inflows into Japan markets remained positive in the week ending the 18th of April. For the third straight week we saw foreign buying of local stocks. This continues the turnaround after strong selling dominated this segment from the start of the year. Offshore investors also purchased local bonds for the third straight week as well, albeit at a more modest pace compared to the prior weeks.

- In terms of outbound Japan flows, we saw local investors resume purchases of offshore bonds, the first such outflows since late Feb. The amount was modest and only partially reverses recent outflows. Such trends will be watched though, given the recent volatility of US Tsys amid concerns the market is losing its status as a bellwether safe haven market.

- On the equity side, local investors continued to buy offshore stocks, marking the fifth straight week of outflows to this segment.

Table 1: Japan Weekly Offshore Investment Flows

| Billion Yen | Week ending April 18 | Prior Week |

| Foreign Buying Japan Stocks | 705.6 | 1044.9 |

| Foreign Buying Japan Bonds | 1000.7 | 2310.7 |

| Japan Buying Foreign Bonds | 223.7 | -511.9 |

| Japan Buying Foreign Stocks | 610.4 | 235.8 |

Source: MNI - Market News/Bloomberg

AUSSIE BONDS: Little Changed After A Subdued Ahead Of Long Weekend

ACGBs (YM flat & XM +1.5) are slightly stronger but well above the morning's lows on a local data light session. Accordingly, the domestic market's attention remained focused on headlines and US tsys.

- Cash US tsys are 2-4bps richer in today's Asia-Pac session. After US market close, US President Trump delivered wide-ranging comments in the Oval Office. Trade/tariffs and monetary policy were among the focus points. Today's US calendar will see Chicago Fed Activity Index, Durable Goods Orders, Initial Jobless Claims and Existing Home Sales.

- Cash ACGBs are flat to 2bps richer with the 3/10 curve flatter and the AU-US 10-year yield differential -11bps.

- Swaps are little changed.

- The bills strip is -1 to -2 across contracts.

- RBA-dated OIS pricing is modestly mixed across meetings today. A 50bp rate cut in May is given an 11% probability, with a cumulative 116bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- Tomorrow, the local market will be closed for the ANZAC Day holiday.

BONDS: NZGBS: Closed At Best Levels Ahead Of ANZAC Day Holiday

NZGBs closed showing modest twist-flattening, with benchmark yields 2bps higher to 1bp lower. This, however, masked the fact that yields finished at or near session bests after opening 6-7bps higher. The NZ-US 10-year yield differential closed 3bps tighter at +17bps.

- The intraday session strength came despite a broad-based pick-up in ANZ consumer confidence. It rose 5.5% to 98.3 in April boosted by another 25bp of monetary easing during the month and despite heightened global uncertainty around US trade policy. It has resumed its uptrend and printed at its highest since December. Both current and future conditions improved.

- Nevertheless, the primary focus for the local market remains abroad. Cash US tsys are 2-4bps richer in today's Asia-Pac session. After the US market close, US President Trump delivered wide-ranging comments in the Oval Office. Trade/tariffs and monetary policy were among the focus points.

- Today’s NZGB supply saw solid demand with cover ratios ranging from 3.32x (May-36) to 4.38x (May-30).

- Swap rates closed flat.

- RBNZ dated OIS pricing closed little changed across meetings. 27bps of easing is priced for May, with a cumulative 80bps by November 2025.

- Tomorrow, the local market will be closed for the ANZAC Day holiday.

NEW ZEALAND: Consumers Subdued But April Sentiment Rises Despite Global Events

There was a broad-based pick up in ANZ consumer confidence with it rising 5.5% to 98.3 in April boosted by another 25bp of monetary easing during the month and despite heightened global uncertainty around US trade policy. It has resumed its uptrend and printed at its highest since December. Both current and future conditions improved.

- ANZ noted that consumer inflation expectations rose 0.5pp to 4.7%, the highest since July 2023, and may have been driven by the uncertainty around tariffs. Price/cost indicators in its business survey have also begun rising again and inflation expectations have stopped moderating.

- Future conditions rose to 105.2 in April from 100.7, despite the major US tariff announcements and subsequent market volatility during the month. The series has been above the breakeven-100 mark since August. The 12-month ahead economic outlook improved 4 points but was still negative at -16%.

- Current conditions rose 6 points to 88 boosted by an 8 point rise in personal finances, likely helped by 200bp of easing in less than a year.

- The time to buy a major household item improved 5 points but remained negative at -11 signalling that private retail spending is likely to stay lacklustre.

NZ ANZ Roy Morgan consumer confidence

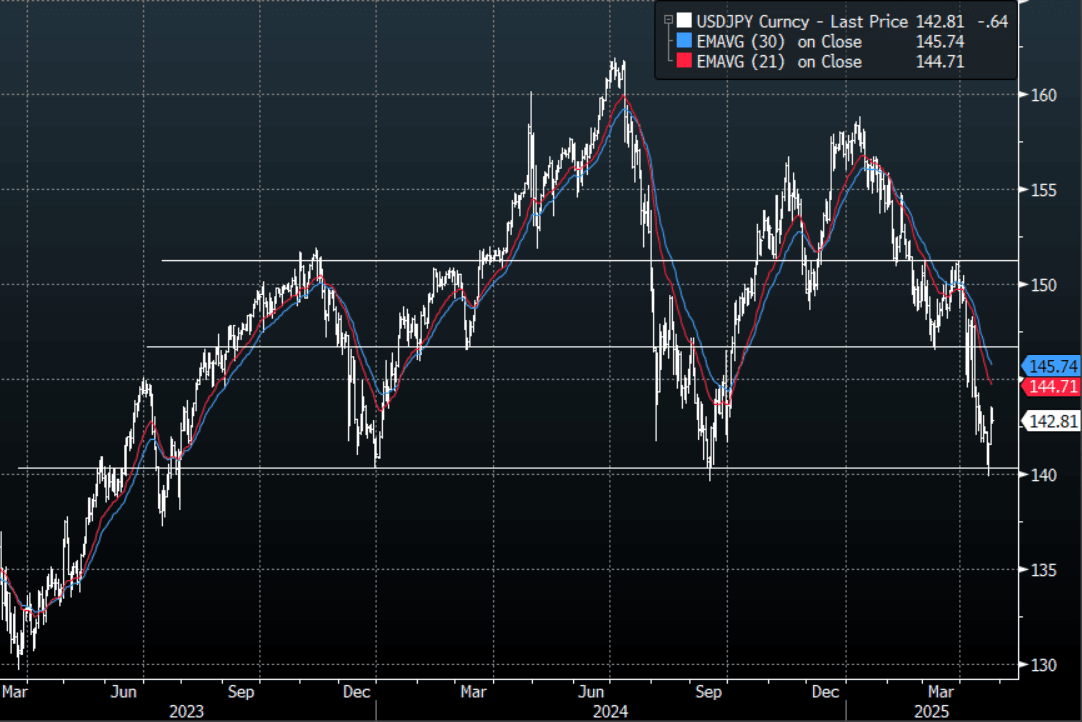

FOREX Wrap - USD Holding Gains, Can It Rebound Further ?

The BBDXY has had an Asian range of 1226.14 - 1228.47, Asia is currently trading around 1227. Trump ramped up pressure on Zelensky to accept a peace deal, “ We are very close to a Deal but the man with ‘no cards’ should now, finally GET IT DONE” he wrote on Truth Social. Bloomberg reports “Christine Lagarde said US tariffs may be more disinflationary than inflationary for Europe, but acknowledged the net impact is still unclear.”

- EUR/USD - Asian range 1.1316 - 1.1358, Asia is currently trading 1.1338.Back at the support around 1.1300, should this area not hold demand should remerge on dips back to 1.1000/1.1100.

- GBP/USD - Asian range 1.3253 - 1.3287,the market seems happy to accumulate GBP on dips but the risk of a short-term retracement remains. Buyers should reemerge back towards the 1.3000 area.

- USD/JPY - Asian range 142.60 - 143.46, has drifted lower for most of the Asia session. On the day the 143 handle should still see some supply, then more importantly the 145/146 area should once more offer good levels for sellers to reengage.

- USD/CNH - Asian range 7.2813 - 7.3039, the USD/CNY fix printed at 7.2098. USD/CNH continues to trade sideways and find support towards 7.2800.

- Cross asset : SPX -0.2%, Gold 3330, US 10yr 4.35%, BBDXY 1227, Crude oil 62.33.

- Data/Events : Chicago Fed Activity Index, Durable Goods Orders, Initial Jobless Claims, Existing Home sales.

Fig 1: USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg

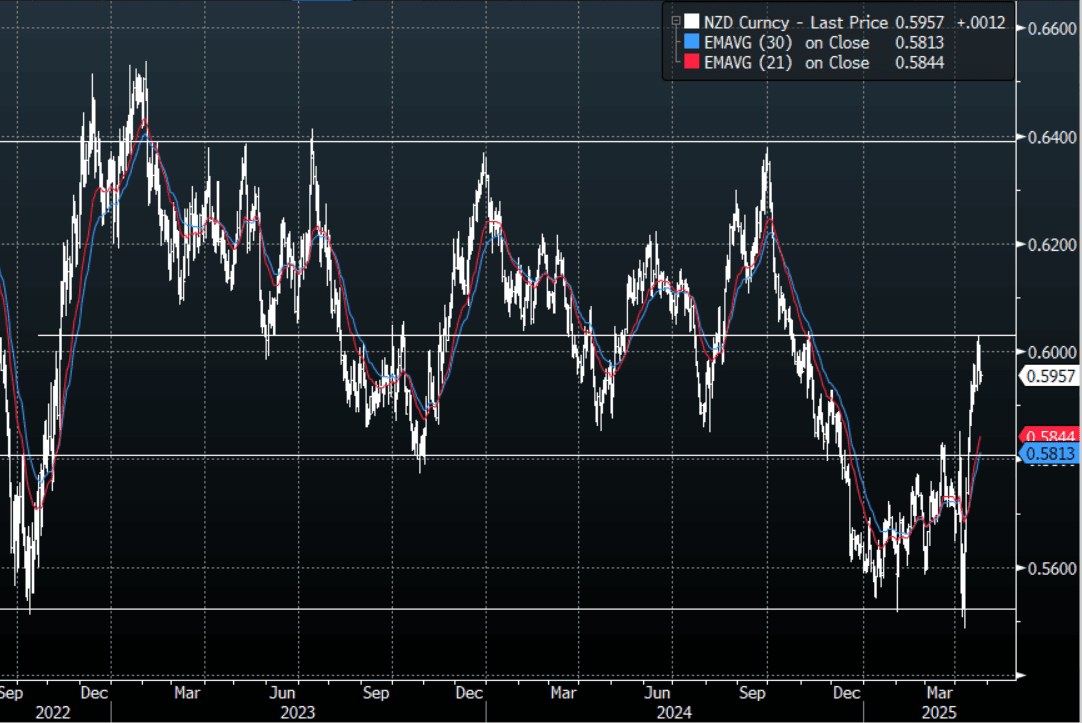

FOREX: Antipodean Wrap - AUD & NZD Consolidate

Risk has struggled to hold onto its gains leaking lower in Asia as the market looks through the Trump administration's attempts at de-escalation. Overall the market seems comfortable buying AUD and NZD on dips, but is wary at current levels as price stalls and potentially signals some sort of a retracement ?

- AUD/USD - Asian range 0.6352 - 0.6372, AUD has traded sideways most of the Asian session. Dips back to the 0.6250/0.6300 area should continue to find demand while the market continues to focus on a lower USD.

- AUD/JPY - Asian range 90.63 - 91.32. Price goes into the London trading around 90.80, still firmly within the last 8 days range of 0.8950/0.9200.

- NZDUSD - Asian range 0.5944 - 0.5963, going into London trading around 0.5950. Price struggles to hold above 0.6000 once more, demand should return first around 0.5900, then around the 0.5850 area.

- AUD/NZD - Asian range 1.0676 - 1.0708, the cross has drifted lower in the Asian session. The cross is going into London pretty directionless but the risks appear skewed towards bounces being capped, with supply returning on bounces back towards the 1.0800 area.

Fig 1 : NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Japan & Aust Firmer, But Taiwan & South Korea Weaker

Outside of Hong Kong losses, trends in other Asia Pac markets have been mixed. US equity futures sit modestly in the red, Eminis under 5400 at this stage, struggling to hold above this level. Focus remains on the next tariff related news flow piece, with Trump stating earlier China's new tariff rate could come in the next 2-3 weeks.

- Japan markets have risen further, last up +0.70% for the Topix. Export related names are rising, perhaps benefiting from the recent rebound in USD/JPY, although other export orientated/tech related markets have struggled today.

- The Taiex is off 0.50%, while the Kospi is down around 0.45%. We had Q1 GDP out of South Korea earlier, which was below market expectations and showed a y/y contraction for the first time 2020.

- In SEA, market shifts are not beyond 1% in either direction at this stage. The ASX 200 is a up a further 0.70%, continuing its recent recovery. The index is now back to early April levels.

CHINA STOCKS: Hong Kong Stocks Pare Recent Gains

Hong Kong stocks are struggling in the first part of Thursday trade. The HSI was last down 1.25%, putting the index back under 22000. If this trend continues through to the close it would be the HSI's first dip since last Wednesday. Trade/tariff concerns remain front and center in terms of market sentiment shifts. The HS tech sub index is off around 2.25% at this stage, so it continues to display a higher beta compared to the main index.

- Mainland China indices have ticked down as well, the CSI 300 last off around 0.20%.

- Earlier remarks were made by US President Trump in the oval office, which suggested the ball was in China's court in terms of a potential trade/tariff deal. He stated if a deal can't be reached then the US will decide on the tariff rate. An announcement on tariff levels was possible within the next 2-3 weeks Trump stated.

- This followed overnight comments from US Tsy Secretary Bessent, who stated that there had been no unilateral offer from Trump to cut China tariffs and that a full trade deal negotiation would take a number of years.

- Such a backdrop may be tempering HK/China equity sentiment, particularly in light of recent gains. The HSI was tracking close to +15% firmer from recent April lows at the start of this week.

- UBS also downgraded Hong Kong stocks back to neutral from overweight, highlighting tariff concerns on the revenue outlook (per BBG).

OIL: Crude Range Trading, Monitoring Tariff & OPEC Developments

Oil prices are little changed during today’s APAC session holding onto Wednesday’s losses given lacklustre risk sentiment with mixed equities and lower commodity prices. Crude has been in a narrow range of less than 50c/bbl. WTI is up 0.1% to $62.36/bbl after an earlier high of $62.54. Brent is +0.1% to $66.21 following today’s peak of $66.40. Benchmarks are likely to remain sensitive to US tariff developments given the consequences for global energy demand. The USD index is down 0.1%.

- There were Reuters reports yesterday that OPEC is under pressure from within to increase output materially again in June, which pushed prices lower. The group meets on May 5 to discuss quotas at a time of lax compliance.

- Politico reported that the White House is considering lifting sanctions on Russia’s Nord Stream 2 gas pipeline but Secretary of State Rubio said that the suggestion is “unequivocally false” and he hadn’t spoken with Middle Eastern envoy Witkoff about easing Russian sanctions and that was not part of talks on a Ukraine deal.

- Later the Fed’s Kashkari speaks. US March orders, Chicago Fed index, April Kansas manufacturing index and jobless claims print. The ECB’s Lane participates in a panel and Germany’s April Ifo survey is published.

GOLD: Rebounds +1% After Recent Losses

After cumulative losses of 4% in the past two sessions, gold has rebounded in the first part of Thursday trade. Bullion got as high as $3367.34, but was last near $3325/30, still up +1.2% for the session. The broader risk rebound has stalled somewhat from a US equity futures standpoint, while region equities are mixed, albeit with Hong Kong weaker, which could be lending some support to gold moves today. The USD BBDXY index is down, but only modestly and remains close to recent highs.

- Near term risk sentiment is likely to be dictated by trade/tariff developments, which will inevitably spillover to gold.

- The structural backdrop for gold still looks sound though: uncertainty around global growth, fragile equity market sentiment and underlying flows from central banks all support points.

- In terms of technicals, firm support is seen at the 20-day EMA of $3,193.5. Shallower selloffs will be considered corrective at this stage. Initial resistance is at $3,500.1, the Apr 22 high. Moving average studies remain in bullish mode.

Asian Growth Outlook Hurt By Increased Protectionism

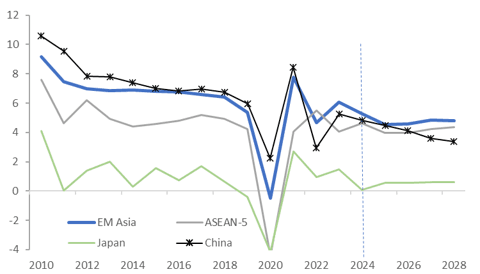

The IMF revised global growth lower in 2025 and 2026 in its April WEO due to increased uncertainty predominantly stemming from trade policy changes. Compared to January forecasts, developments since then are expected to lead to slower growth across DM and EM, slower global trade growth driven by developing economies and only slightly higher inflation mainly in the developed world. Being large traders, Asia stands to be one of the most negatively impacted regions.

- Growth in EM Asia has been revised down 0.6pp to 4.5% in 2025 and 0.5pp to 4.6% in 2026, both down from last year’s 5.3%. ASEAN is forecast to slow to 4.0% in 2025 from 4.6% with 2026 at 3.9% but then it should then stabilise above 4% thereafter.

- In EM, Mexico is the hardest hit with growth down 1.7pp in 2025 to -0.3%.

- China has been specifically targeted by US tariffs and has retaliated resulting in duties of 145% into the US, although President Trump said that the final number should be lower. The IMF didn’t expect China to achieve 5% growth this year and next in its January forecasts and now they have been revised down 0.6pp to 4.0% in 2025 and 0.5pp to 4.0% in 2026 after 5% in 2024.

- India’s growth has also been revised lower but by less than China’s at 6.2% (-0.3pp) and 6.3% (-0.2pp). US Vice President Vance has just visited and stated that the relationship was very important suggesting that there will be an agreement after a tariff of 26% was announced earlier this month.

- DM growth was revised down 0.5pp to 1.4% in 2025 and 0.3pp to 1.5% in 2026 after 1.8% last year. The shift was broad-based but the US saw the largest change at -0.9pp for 2025 more than Canada’s 0.6pp. Japan was revised 0.5pp and 0.2pp lower resulting in lacklustre growth of 0.6% in both 2025 and 2026.

IMF Asia GDP growth outlook %

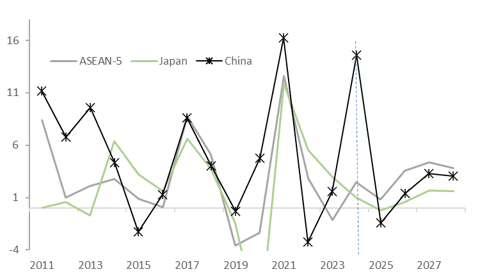

ASIA: China Drives Expected Slowdown In Asian Exports, ASEAN Outlook Positive

The IMF revised down its global trade volume forecasts by 1.5pp to 1.7% in 2024 and by 0.8pp to 2.5% in 2026, with it not expected to return to 2024’s 3.8% over the projected horizon to 2030 as increased trade protectionism reduces flows. Both DM and EM are likely to see a drop in export volumes but the impact is significantly greater on EM and especially Asia due to the US-China trade war.

- EM goods export volumes are forecast to moderate to 0.9% in 2025 from 6.6% in 2024 before picking up to 2.7% in 2026 with the weakness driven by Mexico and China.

- Volumes from EM Asia are forecast to contract 0.7% in 2025 after 2024’s strong 11.2% recovering to only 1.4% in 2026. This is driven by China which sees a sharp slowdown from 14.6% last year to a contraction of -1.4% in 2026 and settling around only 3% thereafter.

- Mexican export volumes are expected to decline 2% this year after rising 2.8% in 2024 before recovering to a subdued 0.7% in 2026. Over 80% of its goods shipments go to the US.

- ASEAN is one group that looks to recover to export growth above 2024’s. The IMF is projecting that it will slow to 0.8% in 2025 from 2.5% in 2024 but then rise to 3.6% in 2026 and 4.3% in 2027.

- DM goods export volumes are only expected to moderate to 0.7% in 2025, with Japan negative though, from 0.9% in 2024 and then rise to 1.9% in 2026.

IMF Asia goods exports outlook %

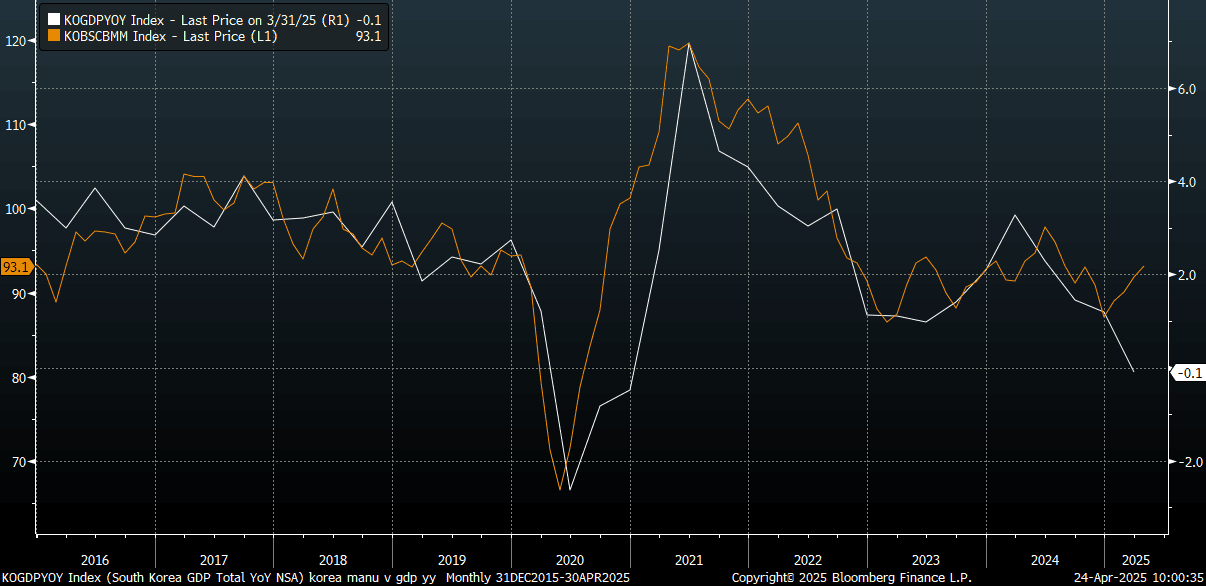

SOUTH KOREA: GDP Below Forecasts, Y/Y Posts First Decline Since 2020

South Korean Q1 GDP printed under market expectations, with q/q at 0.2% versus 0.1% forecast, which was also the prior outcome. The y/y print was -0.1%, below the consensus forecast of flat (prior was +1.2%). This was the first q/q decline since Q2 of last year. For y/y, it was the first decline since the end of 2020.

- In terms of the detail, private consumption was down 0.1% in Q1, after rising 0.2% in Q4 last year. Business investment fell 2.1%q/q, while exports declined by 1.1%. By industry manufacturing fell 0.8%q/q, (from +0.2% in Q4), while construction was down 1.5%q/q. Service were flat after rising 0.4% in Q4 last year.

- The BoK had earlier expected modestly positive growth for Q1, but recently noted the economic outlook had deteriorated.

- At face value, today's data will likely reinforce BoK easing expectations. Earlier we did have manufacturing and non-manufacturing sentiment readings, which both ticked up. The chart below plots the manufacturing heading reading against y/y GDP growth. It suggests we may see some GDP momentum improvement, but confidence is still sub 2024 levels. Also Q2 tariff headwinds are another factor to be mindful of, with April data hitting at further export pressure, while consumer confidence measures are also still well off 2024 levels.

- Per MIPR on BBG, the market looks for close to 2 further 25bps cuts in the next 6 months. The next BoK meeting is on May 29.

Fig 1: South Korean GDP Y/Y (White Line) & Manufacturing Sentiment

Source: MNI - Market News/Bloomberg

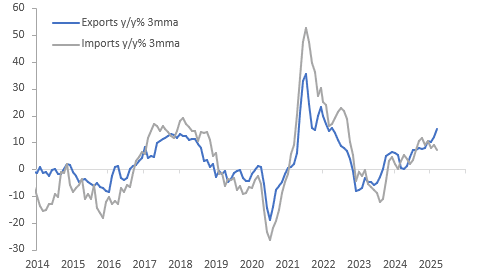

THAILAND: Export Growth Rises As Thailand Negotiates With Major Partner The US

The Thai customs trade surplus narrowed more than expected in March to $973mn following $1988mn. This was despite stronger-than-expected export growth up to 17.8% y/y from 14% but imports also rose more than forecast at 10.2% y/y after 4.0% in February. The Commerce Ministry said that export growth may ease in April due to tariff worries.

Thailand customs exports vs imports y/y% 3-mth ma

Source: MNI - Market News/LSEG

- Q1 customs export growth picked up to 15.1% y/y from 10.5% in Q4, while imports slowed to 7.3% y/y from 10.5%.

- Thailand chose not to retaliate to the proposed 36% US tariff and talks are ongoing although they stalled at the start of the week. Thailand said today that it would be stricter with its certificate of origin and it has proposed to increase its imports of US commodities and reduce its own trade taxes, but the US also wants it to address baht manipulation.

- The Thai government has estimated that the US duty could reduce growth by 1pp in 2025.

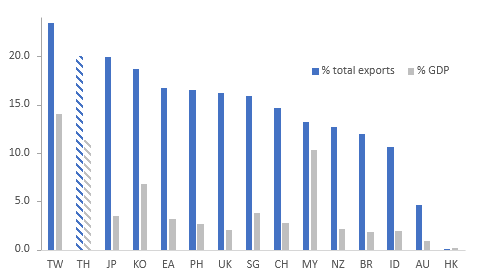

- Thailand’s economy is highly exposed to the US with 20% of its 2024 exports going there worth 11.4% of its GDP, only second to Taiwan in the region. Its exposure to China is a lot less but not immaterial at 12.7% of exports worth 7.2% of GDP and so its already subdued GDP growth could be impacted directly and indirectly from US trade policy.

- In Q1 Thailand ran a surplus with the US of $10.74bn but a deficit with China of $13.96bn.

- The baht has weakened against the greenback today with USDTHB up 0.4% to 33.57 after a low of 33.46 earlier in the session, as the USD is off its intraday low. The pair is still down 1.0% this month though and 4% since the April 9 peak of 34.98.

Merchandise exports to the US 2024 %

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 24/04/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 24/04/2025 | 0700/0900 | ** | PPI | |

| 24/04/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/04/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 24/04/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/04/2025 | 1230/0830 | *** | Jobless Claims | |

| 24/04/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 24/04/2025 | 1230/0830 | * | Payroll employment | |

| 24/04/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 24/04/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/04/2025 | 1300/1500 | ECB's Lane at Peterson Institute Webcast on Monetary Policy Strategy | ||

| 24/04/2025 | 1325/1425 | BOE's Lombardelli on Monetary Policy Strategy | ||

| 24/04/2025 | 1400/1000 | *** | NAR existing home sales | |

| 24/04/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 24/04/2025 | 1500/1100 | ** | Kansas City Fed Manufacturing Index | |

| 24/04/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 24/04/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 24/04/2025 | 1700/1300 | ** | US Treasury Auction Result for 7 Year Note | |

| 24/04/2025 | 2100/1700 | Minneapolis Fed's Neel Kashkari | ||

| 25/04/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 25/04/2025 | 2330/0830 | ** | Tokyo CPI | |

| 25/04/2025 | 0600/0700 | *** | Retail Sales | |

| 25/04/2025 | 0645/0845 | ** | Manufacturing Sentiment | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade | |

| 25/04/2025 | 1230/0830 | ** | Retail Trade |