SOUTH KOREA: GDP Below Forecasts, Y/Y Posts First Decline Since 2020

South Korean Q1 GDP printed under market expectations, with q/q at 0.2% versus 0.1% forecast, which was also the prior outcome. The y/y print was -0.1%, below the consensus forecast of flat (prior was +1.2%). This was the first q/q decline since Q2 of last year. For y/y, it was the first decline since the end of 2020.

- In terms of the detail, private consumption was down 0.1% in Q1, after rising 0.2% in Q4 last year. Business investment fell 2.1%q/q, while exports declined by 1.1%. By industry manufacturing fell 0.8%q/q, (from +0.2% in Q4), while construction was down 1.5%q/q. Service were flat after rising 0.4% in Q4 last year.

- The BoK had earlier expected modestly positive growth for Q1, but recently noted the economic outlook had deteriorated.

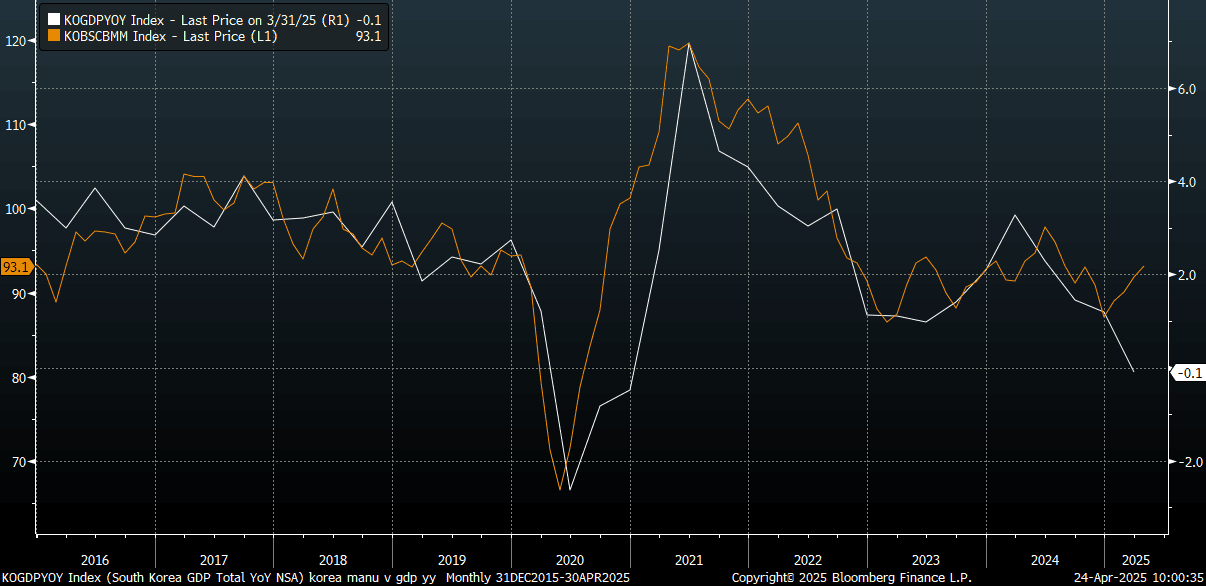

- At face value, today's data will likely reinforce BoK easing expectations. Earlier we did have manufacturing and non-manufacturing sentiment readings, which both ticked up. The chart below plots the manufacturing heading reading against y/y GDP growth. It suggests we may see some GDP momentum improvement, but confidence is still sub 2024 levels. Also Q2 tariff headwinds are another factor to be mindful of, with April data hitting at further export pressure, while consumer confidence measures are also still well off 2024 levels.

- Per MIPR on BBG, the market looks for close to 2 further 25bps cuts in the next 6 months. The next BoK meeting is on May 29.

Fig 1: South Korean GDP Y/Y (White Line) & Manufacturing Sentiment

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGB TECHS: (M5) Within Range of Fresh Cycle Lows

- RES 3: 147.74 - High Jan 15 and bull trigger (cont)

- RES 2: 146.53 - High Aug 6

- RES 1: 142.73/144.48 - High Dec 9 / High Nov 11

- PRICE: 137.72 @ 16:12 GMT Mar 21

- SUP 1: 136.67 - 1.0% 10-dma envelope

- SUP 2: 136.57 - 1.382 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

- SUP 3: 134.89 - 2.000 proj of the Jan 28 - Feb 20 - Feb 26 bear leg

JGBs have traded lower breaching recent key support at 138.71, the Feb 21 low. This confirms a resumption of the bear leg and note too that MA studies are in a bear-mode set-up, highlighting a downtrend. Sights are on 136.57, a Fibonacci projection. For bulls, a show through 140.33 resistance would signal a possible reversal, and open early December highs should the pace be maintained. 144.48 is the medium-term target on any recovery.

CNH: USD/CNH Holding Above 7.2600, Yuan Sees Little Gain From Tariff Headlines

USD/CNH mostly stayed on the front foot through the course of Monday's session. We track near 7.2640/45 in early Tuesday dealings, after posting a modest 0.09% loss in CNH terms on Monday. Spot USD/CNY finished up at 7.2607. The CNY CFETS basket tracker edged a little again on Monday, +0.10% to 98.8805. The index continues to recover from lows amidst higher USD index levels.

- Monday's further modest CNH loss was still the fifth straight decline for the currency. USD/CNH is now back to the 50-day EMA resistance point, which near 7.2650 is close to current spot levels. We are above all other key EMAs. Early March highs in USD/CNH were above 7.3000. The 200-day is back near 7.2400.

- The USD/CNY fixing continues to show a modest upside bias (Monday's print at 7.1780), although there is still a gap with Jan 20's fixing of 7.1886. Nevertheless, this is still probably providing some encouragement to yuan bears.

- CNH didn't appear to see much relief from Trump's comments on more targeted tariffs. There doesn't to have been much progress in terms of lowering tensions between the US and China on trade issues.

- The firmer US yield backdrop/higher equities from Monday, post the Trump tariff headlines and with some data support (better services PMI print) likely helped keep USD/CNH dips supported.

- Locally today, the 1yr MLF is scheduled, but no change is expected from the current 2.00% rate. This rate is being de-emphasized though as a policy tool.

JGBS: US Tsys Weigh On Futures Overnight, BoJ Minutes For Jan MPM

In post-Tokyo trade, JGB futures closed weaker, -14 compared to settlement levels, following a heavy NY session for US tsys.

- Expectations that the April 2 reciprocal tariffs would be flexible, with breaks to countries and sectors as suggested Friday, and would not be as onerous as the more sweeping measures initially threatened underpinned US equities. Indeed, stocks took in their stride with other comments from President Trump about expecting auto tariffs.

- Beliefs that the worst may be over for stocks added to the buying momentum, as did the better-than-expected rise in the S&P Global Services PMI.

- Stocks surged, extending Friday's rally, with NASDAQ's 2.25% jump leading the way. The S&P 500 was 1.75% higher, with the Dow ~1.5% higher.

- The strong risk-on move weighed heavily on US tsys. Concession building ahead of the $183bn in auctions this week added to the selloff, as did the somewhat hawkish comments from the Fed's Bostic, though he is not a voter.

- US 2- and 10-year yields were up 9 bps to 4.03% and 4.33% respectively.

- Today, the local calendar will see the BoJ Minutes for January MPM and Department Sales data alongside an auction for Enhanced-Liquidity 5-15.5-years.