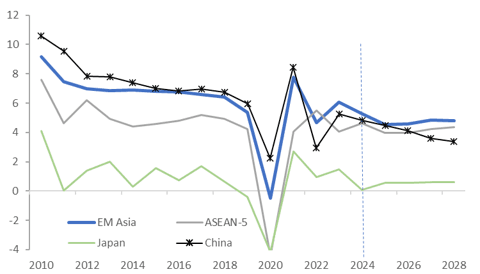

ASIA: Asian Growth Outlook Hurt By Increased Protectionism

The IMF revised global growth lower in 2025 and 2026 in its April WEO due to increased uncertainty predominantly stemming from trade policy changes. Compared to January forecasts, developments since then are expected to lead to slower growth across DM and EM, slower global trade growth driven by developing economies and only slightly higher inflation mainly in the developed world. Being large traders, Asia stands to be one of the most negatively impacted regions.

- Growth in EM Asia has been revised down 0.6pp to 4.5% in 2025 and 0.5pp to 4.6% in 2026, both down from last year’s 5.3%. ASEAN is forecast to slow to 4.0% in 2025 from 4.6% with 2026 at 3.9% but then it should then stabilise above 4% thereafter.

- In EM, Mexico is the hardest hit with growth down 1.7pp in 2025 to -0.3%.

- China has been specifically targeted by US tariffs and has retaliated resulting in duties of 145% into the US, although President Trump said that the final number should be lower. The IMF didn’t expect China to achieve 5% growth this year and next in its January forecasts and now they have been revised down 0.6pp to 4.0% in 2025 and 0.5pp to 4.0% in 2026 after 5% in 2024.

- India’s growth has also been revised lower but by less than China’s at 6.2% (-0.3pp) and 6.3% (-0.2pp). US Vice President Vance has just visited and stated that the relationship was very important suggesting that there will be an agreement after a tariff of 26% was announced earlier this month.

- DM growth was revised down 0.5pp to 1.4% in 2025 and 0.3pp to 1.5% in 2026 after 1.8% last year. The shift was broad-based but the US saw the largest change at -0.9pp for 2025 more than Canada’s 0.6pp. Japan was revised 0.5pp and 0.2pp lower resulting in lacklustre growth of 0.6% in both 2025 and 2026.

IMF Asia GDP growth outlook %

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ASIA STOCKS: India Has Second Day of Big Inflow.

Ongoing outflows from the Indian equity market took a temporary breather on Thursday yet then repeated Friday with one of the largest inflows since early February as regional neighbours all recorded outflows.

- South Korea: Recorded outflows of -$17m yesterday, bringing the 5-day total to +$1,320m. 2025 to date flows are -$3,883m. The 5-day average is +$264m, the 20-day average is -$109m and the 100-day average of -$97m.

- Taiwan: Had outflows of -$345m yesterday, with total outflows of -$1160m over the past 5 days. YTD flows are negative at -$15,170. The 5-day average is -$232m, the 20-day average of -$657m and the 100-day average of -$231m.

- India: Saw inflows of +$610m as of the 21st, with a total inflow of +$515m over the previous 5 days. YTD outflows stand at -$15,417m. The 5-day average is +$103m, the 20-day average of -$234m and the 100-day average of -$183m.

- Indonesia: Posted outflows of -$10m yesterday, bringing the 5-day total to -$388m. YTD flows are negative at -$2,035m. The 5-day average is -$78m, the 20-day average is -$55m the 100-day average of -$36m.

- Thailand: Recorded outflows of -$2m yesterday, totaling -$67m over the past 5 days. YTD flows are negative at -$1,009m. The 5-day average is -$13m, the 20-day average of -$37m the 100-day average of -$19m.

- Malaysia: Experienced outflows of -$64m yesterday, contributing to a 5-day outflow of -$347m. YTD flows stand at -$2,046m. The 5-day average is -$69m, the 20-day average of -$57m the 100-day average of -$36m.

- Philippines: Saw outflows of -$4m yesterday, with net inflows of +$30m over the past 5 days. YTD flows are negative at -$184m. The 5-day average is +$6m, the 20-day average of 0 the 100-day average of -$7m.

AUSSIE BONDS: Cheaper But Off Worst Levels Ahead Of Tonight’s Federal Budget

ACGBs (YM -2.0 & XM -4.5) are weaker but off Sydney session lows on a data-light session.

- Today we will see the Federal Budget presented around 1930 AEDT, ahead of tomorrow's February CPI data.

- A Federal Election is likely to be called soon after. The Budget is expected to show deficits across the forecast horizon with additional expenditure likely in an attempt to win votes.

- “Australia’s February CPI report is likely to show headline inflation slowing. We estimate CPI gains slowed to 2.4% year on year from 2.5% in January, led by softer prices of food and fuel. Core inflation gauges have been trending higher in recent months but remain in the Reserve Bank of Australia’s 2%-3% target band.” (per BBG)

- Cash US tsys are little changed in today's Asia-Pac session after yesterday's heavy session.

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +12bps.

- Swap rates are 3-4bps higher.

- The bills strip is -2 to -3 across contracts.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in April is given a 4% probability, with a cumulative 66bps of easing priced by year-end (based on an effective cash rate of 4.09%).

AUD: Limited Move Higher In A$, Australia’s Budget Later

Aussie is moderately stronger during today’s APAC trading driven by stronger equity sentiment but a lacklustre start to HK/China shares has capped its gains. AUDUSD is up 0.1% to 0.6291 after a high of 0.6295. It fell to 0.6280 before strengthening. The USD index is off its intraday high to be down slightly on the day.

- AUDNZD has approached 1.10, a level it has not been at since 17 March, reaching 1.0989. It is currently 0.1% higher at 1.0988.

- AUDJPY is off its intraday high of 94.92 and is up slightly to 94.75. AUDEUR is 0.1% higher at 0.5823 and AUDGBP +0.1% to 0.4869.

- Equities are mixed with the ASX up 0.5%, CSI 300 +0.2% and Hang Seng down 0.8%. The S&P e-mini is flat. Oil prices are little changed with WTI -0.1% to $69.04/bbl. Copper is up 0.3% and iron ore remains around $102/t.

- Australia’s FY2026 budget is presented around 1930 AEDT. Also later the Fed’s Kugler and Williams speak and US January/February housing data, March consumer confidence & Richmond Fed business conditions and March German Ifo survey are released.