MNI EUROPEAN MARKETS ANALYSIS: US Data In Focus Later

- Focus was on Trump talks with China President Xi and then Japan PM Takaichi. Market impact has been modest, with CNH gaining some ground in the FX space versus the USD. US President Trump will visit China in April next year.

- Elsewhere, the risk on rally lost some momentum, with the USD holding close to recent highs, while Tsy yields ticked up following Monday losses.

- Later delayed US September retail sales and PPI print as well as US preliminary ADP weekly employment, November Philly & Dallas Fed non-manufacturing, Richmond Fed November indices, November consumer confidence and September house prices. Also, German Q3 GDP is released and ECB’s Donnery and Cipollone speak.

MARKETS

US TSYS: Give Back Some of O/N Gains: Eyes Turn to Data Tonight

US bond futures are doing very little today with volumes moderate. The US 10-Yr is flat at 113-11, consolidating it's position above all major moving averages. With data releases continuing, even though some are viewed as stale, the market is highly sensitive for FED members comments.

We saw 2,349 of FVZ5 traded today traded at 109-21 1/4 early afternoon, which had followed a sell of 2,945 of TYZ5 in the morning session at 113-11 and a buy of 2,845 of TUZ5 at 104-15.

Cash is more active with yields higher across the curve by 0.5bps to 1.0bps, with intermediate maturities the worst performers.

- The 2-Yr is at 3.512% (+1.3bps)

- The 5-Yr is at 3.607% (+1.4bps)

- The 10-Yr is at 4.038% (+1.2bps)

- The 30-Yr is at 4.679% (+0.7bps)

Tonight sees a US$85bn 6-week bill, US$50bn 52-week bill, US28bn 2-Yr FRN and US$70bn 5-Year auctions.

This week's data calendar picks up overnight, highlighted by retail sales and PPI inflation for September, although the Conference Board's consumer survey and its labor differential should also command attention, with indicators looking for solid retail sales numbers. PPI data likely viewed as stale and not market relevant. For Wednesday then sees weekly jobless claims brought forward for Thanksgiving, including of note the payrolls reference period for continuing claims in November, along with the catching up of the September durable goods report, the MNI Chicago PMI for November and the Fed's Beige Book.

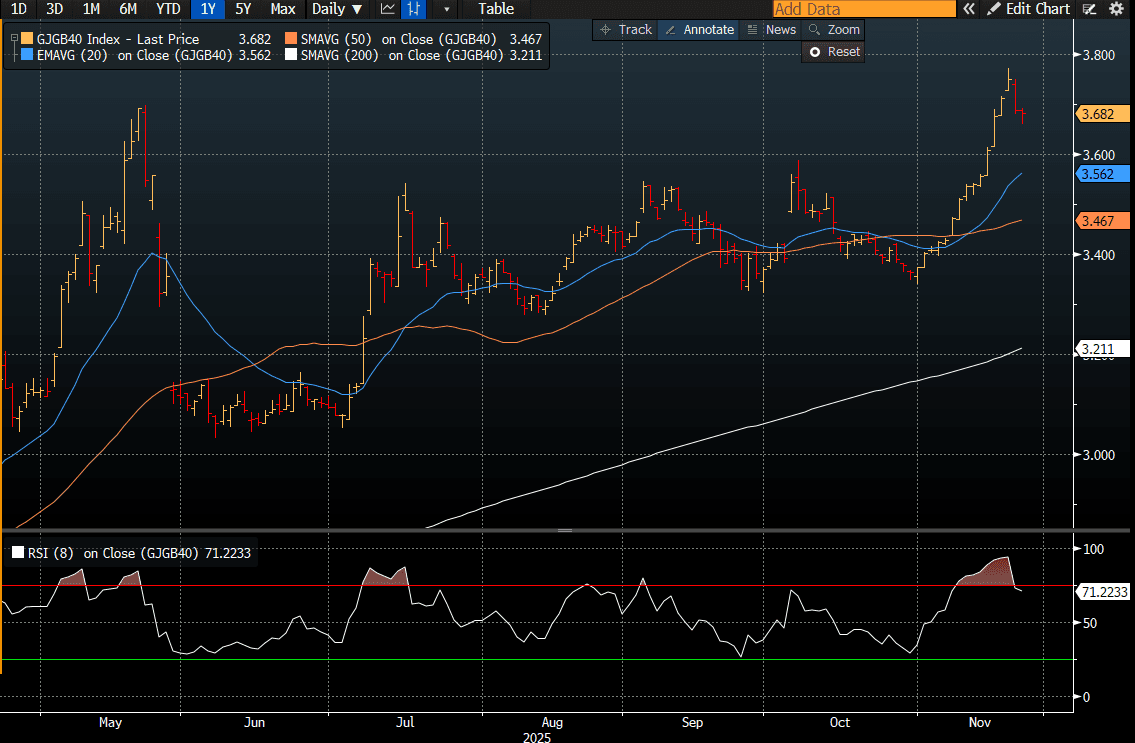

JGBS: 40Y Outperforms Ahead Of Tomorrow's Supply

JGB futures are weaker, -21 compared to settlement levels, and at lows after a choppy start to the session.

- Local calendar has been light, with Dept Sales data due later.

- Japanese PM Takaichi has confirmed she has spoken with US President Trump via a telephone call this morning. The call was made at the request of US President Trump. It came after US President Trump and Chinese President Xi spoke on Monday. Japan/China tensions have been elevated in recent weeks in the aftermath of Takaichi's comments in relation to Taiwan.

- Cash US tsys are ~1bp cheaper in today's Asia-Pac session.

- Cash JGBs have twist-flattened across benchmarks, with yields 2.7bps higher (7-year) to 0.6bp lower (40-year), ahead of tomorrow's 40-year supply.

- The benchmark 40-year yield is at 3.682% versus the cycle high of 3.772%, with the 2/40 yield curve currently positioned at the midpoint of its recent range. (see chart)

- The last 40-year auction was on September 25. That bond auction drew a bid-to-cover ratio of 2.6x compared with 2.127x at the prior auction. At that time, the 40-year bond yielded 3.30%.

- Swap rates are ~2bps higher across the curve.

- Tomorrow, the local calendar will see PPI Services, Machine Tool Orders and Leading/Coincident Index data alongside 40-year supply.

Source: Bloomberg Finance LP

US-JAPAN: Takaichi Speaks With Trump Amid China/Japan Tensions

Japan PM Takaichi has confirmed she has spoken with US President Trump via a telephone call this morning. The call was made at the request of US President Trump. It came after US President Trump and China President Xi spoke on Monday. Japan/China tensions have been elevated in recent weeks in the aftermath of Takaichi's comments in relation to Taiwan.

- Takaichi stated that US President Trump briefed her on the phone call between Trump and Xi. Otherwise though, only high level details have emerged from the Takaichi/Trump call so far. Takaichi stating that Trump said she can call on him at anytime and that they are close friends. Takaichi added that they exchanged a wide range of views on the Indo-Pacific situation.

- The Trump-Xi call earlier was positive per Trump comments, with the US President set to visit China in April next year, while trade talks continue (rare earth talks are aimed at finalizing general licensing agreements by the end of this month, per BBG). China President Xi also stated the two sides should keep the positive momentum going, which was generated from the face to face meeting they had in Seoul recently.

- Also via BBG: " The Chinese leader told Trump that the return of Taiwan to China is a key part of the post-World War II international order, according to a Chinese Foreign Ministry statement."

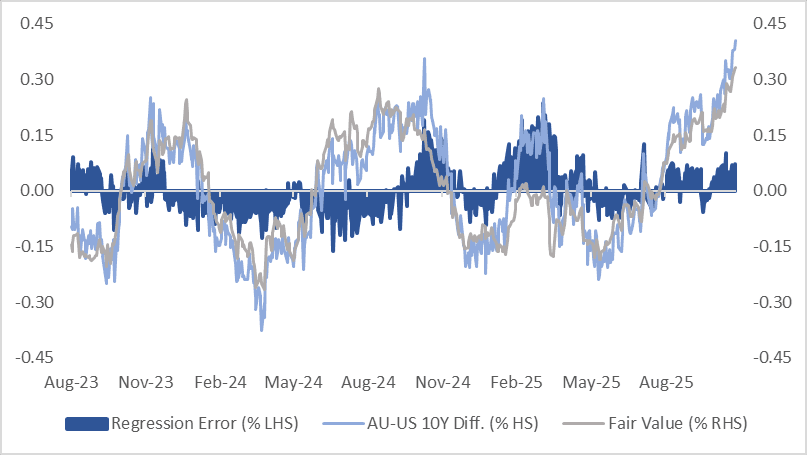

AUSSIE BONDS: AU-US 10Y Diff In Focus As It Pushes Further Out Of Range

ACGBs (YM -0.5 & XM +1.0) are slightly mixed ahead of tomorrow’s October CPI data.

- A partial basket has been published for a while, but the focus has remained on the quarterly series, as they contained updates for all components. RBA Governor Bullock said that the Board will continue to concentrate on quarterly CPI for now as it assesses the trends in the new monthly CPI.

- Cash US tsys are ~1bp cheaper in today’s Asia-Pac session.

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +40bps — its widest level since September 2022.

- This move has pushed the differential decisively above the ±30bps range that had persisted since November 2022.

- However, a simple regression of the 10-year yield differential against the AU–US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is around 7bps too wide relative to fair value.

- Even so, with markets still pricing a 45% chance of an RBA cut by mid-2026, despite recent RBA commentary, it may be premature to position for the narrowing of the differential.

- The bills strip is little changed.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 11bps of easing priced by mid-2026.

Bloomberg Finance LP / MNI

RBNZ: MNI RBNZ Preview-Nov 2025: 25bp Cut & Keeping Options Open

- Download Full Report Here

- The RBNZ is likely to cut rates 25bp on 26 November to 2.25%, edging below its estimate of "neutral". 2/24 analysts on Bloomberg are forecasting 50bp. The data released since the October decision have been consistent with a gradual but soft recovery and importantly close to the RBNZ's August expectations and thus there is unlikely to be another outsized 50bp easing.

- The focus will be on revisions to the RBNZ’s OCR path. Q1 will be the interesting quarter. There is only one meeting scheduled in Q1 on 18 February and a 2.1% would signal further easing.

- The market currently has 27bps of easing priced for November's meeting and a cumulative 35bps by February 2026.

- This is Governor Hawkesby’s last meeting and so optionality is likely to be retained not only given heightened economic uncertainty but so as not to tie the hands of new governor Anna Breman, from Sweden’s Riksbank, who takes over from 1 December.

BONDS: NZGBS: Slightly Richer Ahead Of Tomorrow's RBNZ Policy Decision

NZGBs closed 1-2bps richer across benchmarks ahead of tomorrow’s RBNZ Policy Decision.

- The RBNZ is likely to cut rates 25bp on 26 November to 2.25%, edging below its estimate of "neutral". 2/24 analysts on Bloomberg are forecasting 50bp. The data released since the October decision have been consistent with a gradual but soft recovery and, importantly, close to the RBNZ's August expectations, and thus there is unlikely to be another outsized 50bp easing.

- Total new residential mortgage lending in New Zealand rose to NZ$8.36 billion in October from NZ$8.18 billion in September, according to data from the RBNZ. – MTN via BBG

- RBNZ-dated OIS pricing is mostly unchanged across meetings today ahead of tomorrow’s policy decision.

- Notably, pricing is 6–15bps softer across meetings compared with levels before the October 9 meeting, November 2025 leading.

- Most of that decline occurred on the day the RBNZ cut the OCR by 50bps; pricing has been relatively stable since.

- The market currently prices 27bps of easing for tomorrow’s meeting and a cumulative 35bps by February 2026.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 4.50% May-30 bond and NZ$225mn of the 4.25% May-34 bond.

Bloomberg Finance LP

FOREX: USD - BBDXY Trades Firm As Risk-On Rally Fades

The BBDXY has had a range today of 1226.03 - 1227.37 in the Asia-Pac session; it is currently trading around 1227, +0.05%. This week the standout has been the huge bounce in global risk together with a repricing of a potential US December rate cut, as of yet though there has been a distinct lack of a reaction from the USD, yet ? While the price remains above 1223/24 I would be skewed toward expressing a long, looking for a retest of the 1230-1240 area at some point. A move back through this support and we are back in the 1210/15-1230/35 range.

- EUR/USD - Asian range 1.1519 - 1.1530, Asia is currently trading 1.1515. The pair continues to consolidate around the 1.1500 area. While the EUR remains capped below the 1.1545-65 area the bears remain in charge, and while that is the case I would be skewed short. Above there and the market will start to refocus on the 1.1650 area.

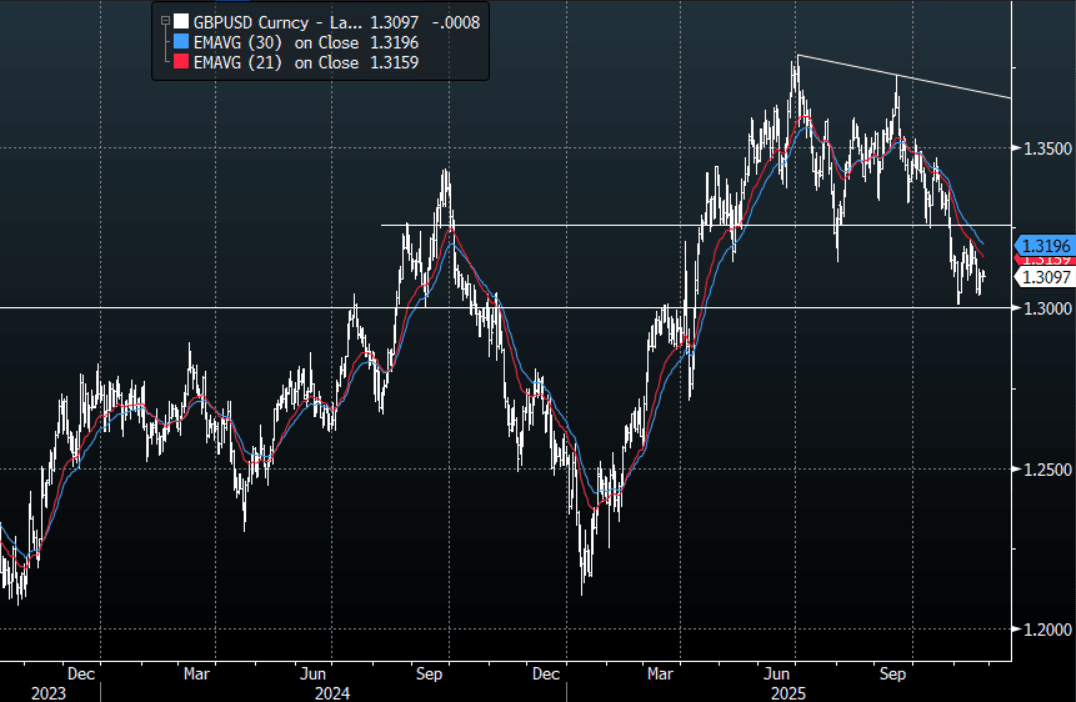

- GBP/USD - Asian range 1.3102 - 1.3116, Asia is currently dealing around 1.3100. The pair traded sideways overnight, unable to move back above the 1.3130-60 area. I continue to favor fading rallies, as GBP looks to have put in a medium term top. While below the 1.3130-60 area I remain skewed toward shorts, a break above here could signal better entry levels back toward the 1.3250 area. Lots of event risk this week with the budget presented on the 26th November.

- Cross asset : SPX -0.02%, Gold $4145, US 10-Year 4.036%, BBDXY 1227, Crude Oil $58.59

- Data/Events : Germany GDP, EZ EU27 New Car Registrations, France Consumer Confidence, Spain PPI

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: USD/JPY - Consolidates On A 156 Handle

The USD/JPY range today has been 156.56 - 156.98 in the Asia-Pac session, it is currently trading around 156.80, -0.05%. The pair has drifted a little lower in a very quiet session even with Japan returning. The price action looks pretty clear for now though and Japanese officials would have to do something extraordinary to change the narrative. The path of least resistance is now a higher USD/JPY and I suspect any dips back toward the 154-155 area would be used as buying opportunities. Shorter term first support looks to be towards 156.00-156.30, and topside is 157.00-157.30 a break of which would open up a retest of the 158.00 area. The large stimulus package has been approved but the market is asking how do you fund this extravagance when you have the highest debt-GDP ratio in the world and yields are exploding higher.

- Chester Ntonifor of BCA research pointed to Yen positioning as a reason this move could still have more to go, “One of the reasons the yen has been weakening by more than dollar strength will suggest is that a lot of speculators have just started to unwind their long positions.”

- Takaichi Speaks With Trump Amid China/Japan Tensions: Japan PM Takaichi has confirmed she has spoken with US President Trump via a telephone call this morning. The call was made at the request of US President Trump. It came after US President Trump and China President Xi spoke on Monday. Japan/China tensions have been elevated in recent weeks in the aftermath of Takaichi's comments in relation to Taiwan.

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($339m),156.00($909m), 157.00($433m). Upcoming Close Strikes : 154.00($2.14b Nov 26), 154.00{$1.28b Nov 28), 155.00($1.86b Nov 26) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 99 Points

AUD/USD - Drifting Lower As Risk Turns Back Down In Asia

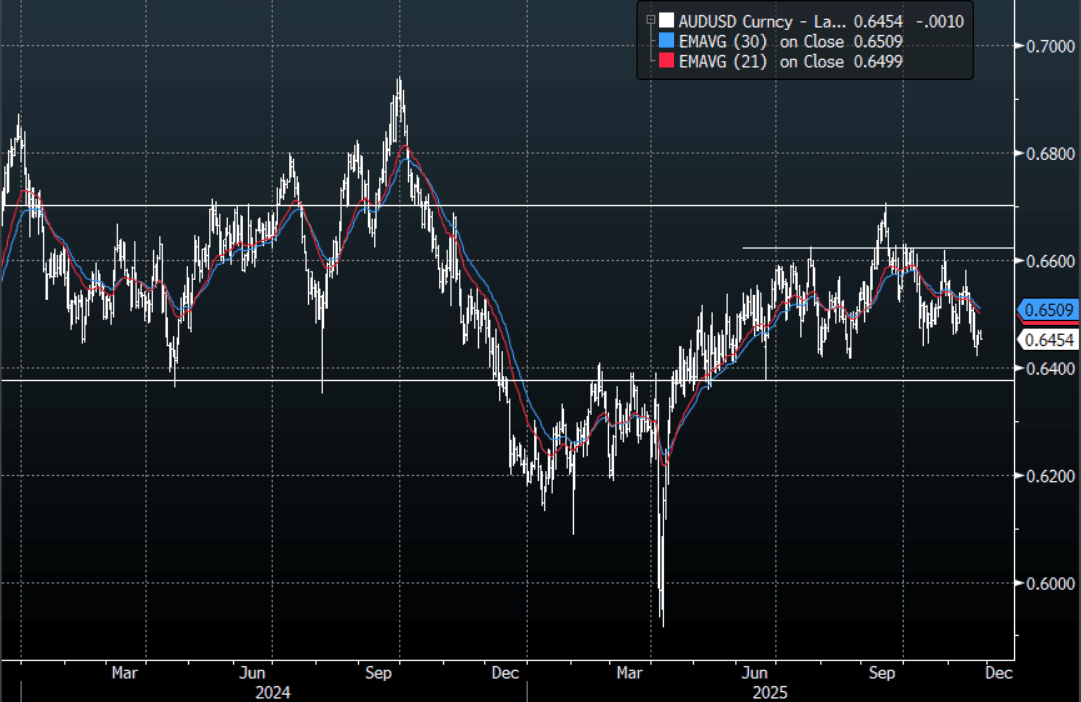

The AUD/USD has had a range today of 0.6452 - 0.6469 in the Asia- Pac session, it is currently trading around 0.6455, -0.15%. The AUD/USD has drifted lower in a quiet Asian session, where risk has not followed through with the overnight strength seen. The AUD continues to consolidate around 0.6450 but given the size of the moves overnight I would have expected a bigger reaction, are currencies lagging or do they just not believe in the rally? The 0.6440-0.6450 area continues to be supportive, a sustained break below here is needed to target the 0.6350 area. On the day, watch to see if price can move above 0.6470-90, If price cannot push back above there then its back toward testing the support.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6500(AUD330m), 0.6650(AUD349m). Upcoming Close Strikes : 0.6450(AUD1.04b Nov 26), 0.6500(AUD1.07b Nov 26), 0.6535(AUD1.69b Nov 26) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 40 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD/USD - Trades Heavy Around 0.5600 As Risk-On Fizzles In Asia

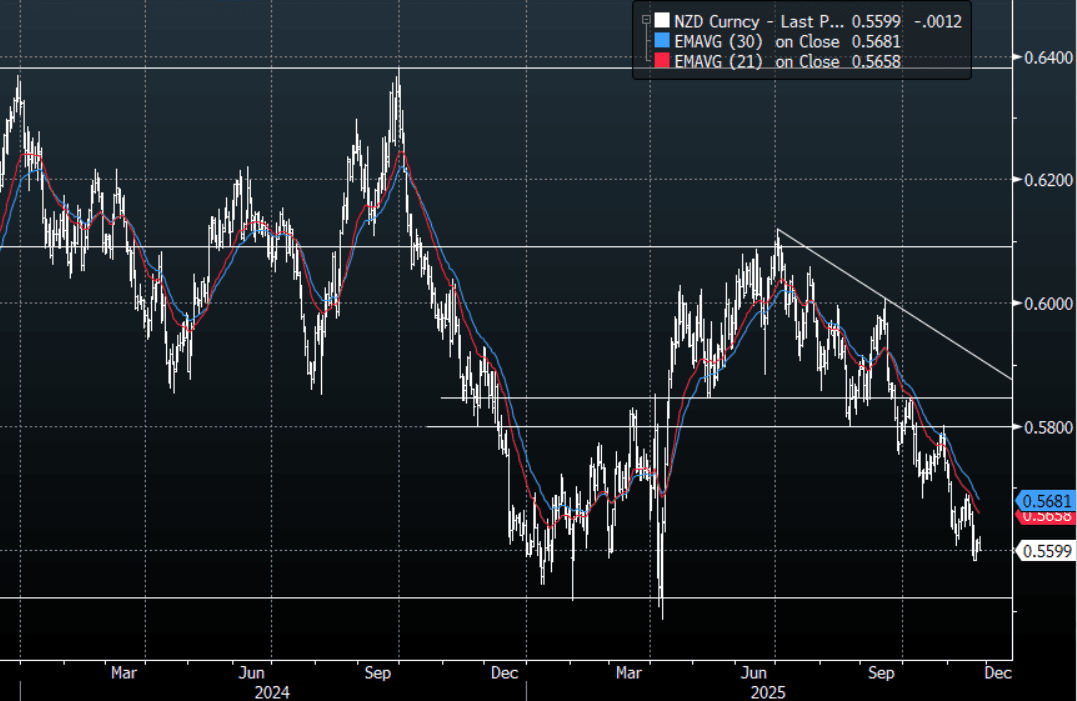

The NZD/USD had a range today of 0.5598 - 0.5622 in the Asia-Pac session, going into the London open trading around 0.5600, -0.20%. The NZD/USD has drifted lower in a quiet Asian session, where risk has not followed through with the overnight strength seen. The NZD is consolidating around the 0.6600 area and like the AUD considering the move in risk overnight I am a little surprised it didn't try to push a little higher. The RBNZ this week will be important as they start to approach neutral, the market is already short NZD so I am mindful of any dovish disappointment. On the day though, while 0.5635-50 caps price the bears remain in charge, a move back below 0.5580 and the market will start lasering onto the pivotal 0.5500 area.

- MNI AU - The RBNZ is likely to cut rates 25bp on 26 November to 2.25%, edging below its estimate of "neutral". 2/24 analysts on Bloomberg are forecasting 50bp. The data released since the October decision have been consistent with a gradual but soft recovery and importantly close to the RBNZ's August expectations and thus there is unlikely to be another outsized 50bp easing.

- The focus will be on revisions to the RBNZ’s OCR path. Q1 will be the interesting quarter. There is only one meeting scheduled in Q1 on 18 February and a 2.1% would signal further easing. The market currently has 27bps of easing priced for November's meeting and a cumulative 35bps by February 2026.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5600(NZD600m), 0.5640(NZD360m), 0.5720(NZD646m). Upcoming Close Strikes : 0.5670(NZD788m Nov 26) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 37 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: China Tech Valuations Lead Bourses Higher

With Japan playing catch up today, more positive cues from Fed Speakers that a rate cut could come at the next Fed meeting has underscored equity markets today. China's major onshore bourses led the way today with Shenzhen Comp up by +1.9% with onshore press suggesting that a bounce in China's tech sector is driving returns. The tech led rally in the US thanks to Alphabet's AI upgrade announcement helped. China's tech valuations are a factor also given they haven't rallied as much as Japan and Korean AI stocks in recent months.

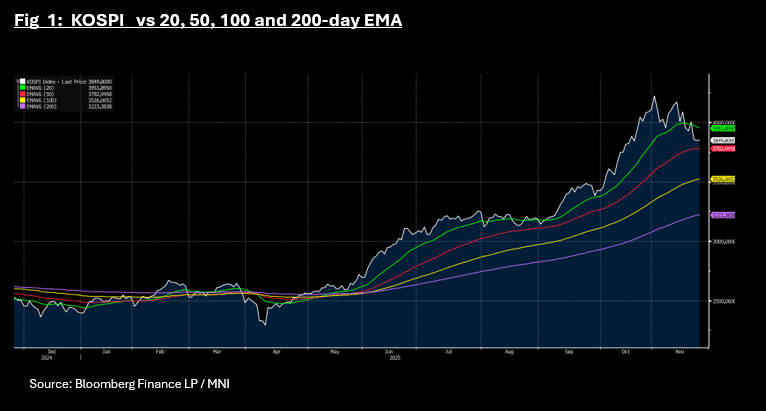

- The NIKKEI appeared to have stayed on holiday from yesterday, rising a mere +0.13% today whilst the KOSPI was flat. The KOSPI's falls in recent days now sees it at the midpoint between the 20-day EMA and the 50-day EMA, looking for a catalyst to break above or below.

- China's major bourses held centre stage with the Hang Seng up +0.62%, the CSI 300 +1.25%, Shenzhen +1.92% and Shanghai +1.1%.

- Despite outflows from Taiwan stocks gathering pace, TSMC's rise of +2.2% today helped the TAIEX rise by +1.40%

- SE Asia' major bourses were mixed with the JCI down heavily after reaching new highs yesterday. In what appeared profit taking the JCI is down -0.75%, taking the FTSE Malay KLCI with it with falls of -0.25% whereas the SE Thai is up +1.05% following very strong import data released for October with local press suggesting it has a sign of improving domestic demand.

- In India the NIFTY 50 is barely positive, unable to recover yesterday's losses despite the RBI Governor suggesting that the upcoming decision on rates could see a cut in the base rate.

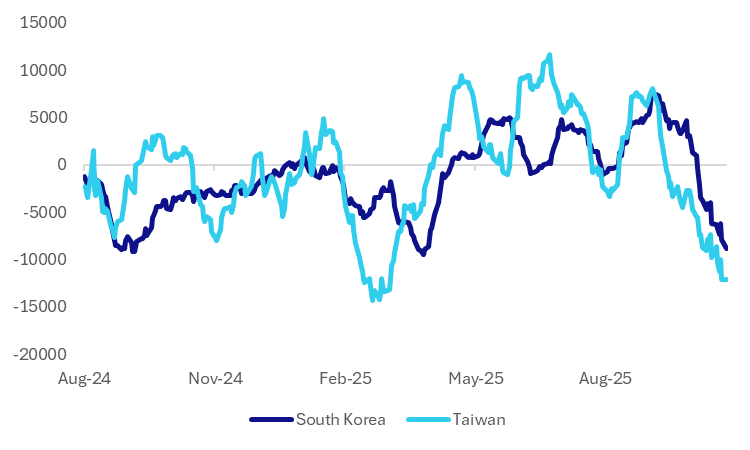

ASIA STOCKS: SK/Taiwan Outflows Near Recent Extremes, Indonesia, Phils Supported

As we approach the end of November, offshore net selling continues for tech sensitive plays like South Korea and Taiwan. Even with signs of rebound momentum/stability in some of the related indices in Monday US trade, we are yet to see that stabilize outflows from these markets. Today, offshore investors have remained net sellers of local South Korean stocks (a further $67mn) per the NBUY function. Outflows have been strong for the past 5 trading days from both of these markets, see the table below. The chart below plots the rolling monthly net inflow trends, with both markets now back close to recent extremes in terms of outflow momentum (over $12bn for Taiwan, and near $9bn for South Korea).

- November to date has been better for the likes of Indonesia, India and the Philippines, which, at this stage, have positive month to date net inflows. Still, India's net inflows of $247mn are very modest compared to the scale of YTD outflows (still near -$16bn).

- Indonesia has likely benefited from less tech exposure and the government's pro-growth mindset. Some offshore dip buyers have emerged for Philippines stocks, but it is has been a consistent theme. The PCOMP is back above 6000, after testing under 5600 earlier in Nov (which was fresh multi year lows).

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | -569 | -3196 | -5898 |

| Taiwan (USDmn) | -902 | -5699 | -7106 |

| India (USDmn)* | -182 | 604 | -15952 |

| Indonesia (USDmn) | 190 | 381 | -1665 |

| Thailand (USDmn) | -35 | -196 | -3403 |

| Malaysia (USDmn) | -79 | -332 | -4622 |

| Philippines (USDmn) | -14 | 40 | -632 |

| Total (USDmn) | -1592 | -8398 | -39278 |

| * Data Up To Nov 21 |

Source: Bloomberg Finance L.P./MNI

Fig 1: Rolling 1 Month Sum - Net Inflows For South Korea and Taiwan (USD mn)

Source: Bloomberg Finance L.P./MNI

OIL: Crude Lower Despite Russian Attack On Kyiv, US Inventories In Focus

After unwinding Friday’s losses on Monday, oil is down slightly during Tuesday’s APAC session but has moved in a narrow range. Brent is down 0.5% to $63.07/bbl, while WTI is 0.4% lower at $58.60/bbl, both close to their intraday troughs.

- While Ukraine developments remain important for oil, it looked through reports of a major Russian bombardment of Kyiv, which suggests that it is unlikely to agree to a revised peace plan consistent with earlier comments that Europe’s proposal “doesn’t fit us at all”. Russian obstinacy should be positive for oil prices, as it means sanctions are unlikely to be eased while the stance persists.

- The US peace plan has apparently been changed to address most of the Ukraine’s issues but disagreements over security guarantees and sovereignty are yet to be resolved. US army secretary Driscoll is meeting Russian officials in Abu Dhabi according to CBS.

- With a record oil surplus forecast for 2026, supply/demand fundamentals remain important. US industry-based inventory data are released later on Tuesday with the official EIA on Wednesday. OPEC meets 30 November to decide January production but last time said that it would hold quotas steady in Q1.

- Later delayed US September retail sales and PPI print as well as US preliminary ADP weekly employment, November Philly & Dallas Fed non-manufacturing, Richmond Fed November indices, November consumer confidence and September house prices. Also, German Q3 GDP is released and ECB’s Donnery and Cipollone speak.

Gold Range Trading Ahead Of US PPI & Retail Data Today

Gold is moderately higher on Tuesday but has range traded as it waits for US data out later today and its impact on Fed cutting expectations. The market currently has around an 86% chance of 25bp of easing on 10 December.

- Bullion is up 0.2% to $4145.0/oz, holding above initial resistance at $4132.9, after a high of $4155.81 which followed a low of $4122.70. Both the US dollar and 2-year yield are slightly higher.

- Silver is 0.3% higher at $51.54, close to the intraday peak, after falling to $51.016.

- Equities are mixed with the S&P e-mini flat, Topix down 0.3% but Hang Seng up 0.6%. Oil prices are lower with WTI -0.4% to $58.60/bbl. Copper is up 1.8%.

- Later delayed US September retail sales and PPI print as well as US preliminary ADP weekly employment, November Philly & Dallas Fed non-manufacturing, Richmond Fed November indices, November consumer confidence and September house prices. Also, German Q3 GDP is released and ECB’s Donnery and Cipollone speak.

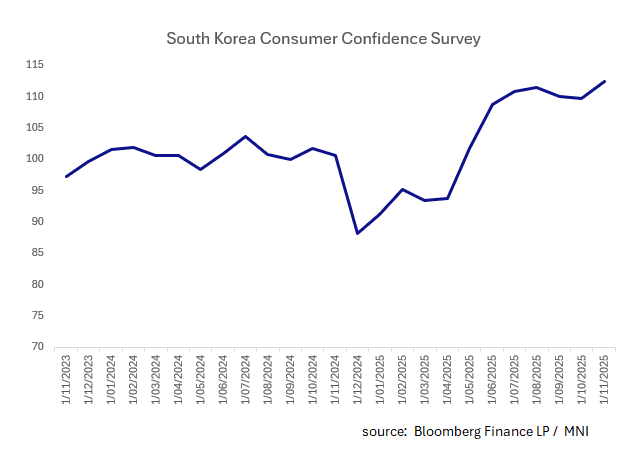

SOUTH KOREA: Consumer Confidence Rises in November

- After two months of moderating, November Consumer Confidence release rebounded to new 5-Year highs.

- At 112.4 for November, over 2,000 households surveyed were comfortable with the current inflation expectations of 2.6%.

- The survey is not surprising given the performance of the KOSP over the month prior in the midst of a tech boom. The KOPSI had delivered +19% in October with key tech stocks hitting record levels.

- The surge in stocks in October and the finalization of a trade deal with the US were enough to make households turn more confident on the outlook.

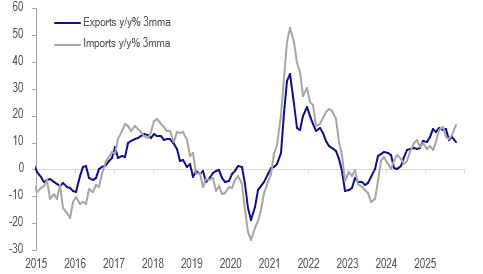

THAILAND: Large October Trade Deficit, Softer Exports Could Drive Easing

Thailand recorded its largest customs trade deficit at $3.44bn since January 2023 as import growth materially exceeded exports. September posted a surplus of $1.28bn. Shipments slowed in October to 5.7% y/y from 19% while imports were up 16.3% after 17.2%, higher than expected. The data can be volatile and the 3-month average of export growth was still up 10.2% y/y in October. Releases over the months ahead will be important to determine if shipments are slowing, which would be a concern for an economy struggling with sluggish growth and possibly drive further monetary easing.

- A sustained trade deficit may reduce some of the appreciation pressure on the baht, which both the central bank and government would like to see. The BIS THB NEER is up 1.0% m/m in November and USDTHB looked through the October trade data and is down 0.4% to 32.36 today.

- Thailand’s Commerce Ministry said the pickup in October imports was driven by an increase in raw material and capex imports from China, while Thailand’s exports to China rose 9.3% y/y. China’s shipments to Thailand rose 6.9% y/y in September but fell 3.3% y/y in October.

- Thailand is one of the most exposed countries in the region to the US with 20% of total 2024 exports worth around 11% of GDP going to there. It imposed 19% tariffs on Thailand in July which may be pressuring its exports as well as generally softer global demand following the increase in protectionism.

- The Bank of Thailand has cut rates 75bp this year to support lacklustre growth. It meets again on 17 December.

Thailand customs exports vs imports y/y% 3-mth moving average

Source: MNI - Market News/LSEG

CNH: Under 7.1000, RR Trending Lower, But Option Mkt Prob Of 7.00 By Yr End Low

USD/CNH tracks near 7.0950/55, slightly up from session lows (7.0922). These earlier lows weren't too far from earlier Nov lows of 7.0907. Still, the pair has had a number of attempts under 7.1000 since mid Sep, with moves under this level ultimately proving short lived. Prospects of a sustained move under 7.1000 may have risen, given the recent US-China leaders call (which affirmed relations appeared to be trending in a positive direction), while rising US Fed easing odds at the Dec meeting is also weighing on US-Ch yield differentials.

- A threat of a move under 7.0850, which would mark fresh YTD lows, could prompt foreign currency holds, like exporters to increase conversion back into the local currency before year end or in early 2026 (ahead of the lunar new year).

- The skew around risk reversals is lower for USD/CNH, although more movement has been evident in longer dated tenors. The 6mth was around flat at the start of the month, but now prints near -0.36. The 1yr is testing under flat, which is around record lows.

- Still, option market pricing suggests overall USD/CNH moves will remain fairly contained. For instance the implied probability of hitting 7.00 in 1 months time (so close to year end) remains under 9%. In 3mths time the market pricing for touching 7.0 is just under 47%.

ASIA FX: SEA FX Mostly Firmer Versus USD, IMF May Reclassify INR FX Regime

In South East Asia FX, the bias has mostly been for a weaker USD. Gains have been modest though, ahead of US data latter (while US yields have also edged up, retracing some of Monday's fall). In the equity space, trends are mixed, volatility continues in the tech related space, while some SEA markets are weaker (mainly Philippines and Indonesia, while Thailand is higher). USD/INR hasn't reacted much to reports that the IMF may change how the country's FX regime is classified.

- USD/IDR is back near 16660/65, close to earlier lows in Nov. Prospects of a potential Fed cut in Dec has likely aided sentiment (not withstanding the nudge higher in US Tsy yields today). Offshore investors have also been consistent buyers of local equities so far this month, while there are also signs of improving offshore debt inflows. A clean break lower could see the 16600 level targeted.

- Spot USD/THB is lower, back near 32.35, with the pair continuing to find resistance above 32.50. We did see a wider than expected customs trade deficit earlier, as exports slowed. This may prompt fresh BoT easing, but FX sentiment hasn't been impacted.

- USD/MYR continues to be biased lower, last near 4.1335. Earlier dips under 4.1300 were supported, but the pair is nearing an oversold technical position once again. USD/SGD is little changed, holding close to 1.3045/50.

- USD/INR is down slightly but remains within recent ranges, last under 89.20. BBG notes the IMF is likely to change the description of India's FX regime. Via BBG: "The new description of the country’s de facto currency regime is likely to include references to a crawling peg, the people said, asking not to be identified discussing private matters. " The new RBI regime, since late last year, has allowed greater INR volatility, but still keeps the pace of rupee depreciation in check.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 25/11/2025 | 0700/0800 | ** | PPI | |

| 25/11/2025 | 0700/0800 | *** | GDP (f) | |

| 25/11/2025 | 0745/0845 | ** | Consumer Sentiment | |

| 25/11/2025 | 0800/0900 | ** | PPI | |

| 25/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 25/11/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 25/11/2025 | 1330/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 25/11/2025 | 1330/0830 | *** | PPI | |

| 25/11/2025 | 1330/0830 | *** | PPI | |

| 25/11/2025 | 1330/0830 | *** | Retail Sales | |

| 25/11/2025 | 1330/0830 | ** | WASDE Weekly Import/Export | |

| 25/11/2025 | 1330/0830 | *** | Retail Sales | |

| 25/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 25/11/2025 | 1400/0900 | ** | S&P Case-Shiller Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Home Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Quarterly Price Index | |

| 25/11/2025 | 1400/0900 | ** | FHFA Quarterly Price Index | |

| 25/11/2025 | 1400/1500 | ECB Cipollone Keynote at Central Bank of Ireland | ||

| 25/11/2025 | 1500/1000 | ** | NAR Pending Home Sales | |

| 25/11/2025 | 1500/1000 | *** | Conference Board Consumer Confidence | |

| 25/11/2025 | 1500/1000 | ** | Richmond Fed Survey | |

| 25/11/2025 | 1500/1000 | * | Business Inventories | |

| 25/11/2025 | 1500/1000 | * | Business Inventories | |

| 25/11/2025 | 1530/1030 | ** | Dallas Fed Services Survey | |

| 25/11/2025 | 1630/1130 | ** | US Treasury Auction Result for 52 Week Bill | |

| 25/11/2025 | 1800/1300 | ** | US Treasury Auction Result for 2 Year Floating Rate Note | |

| 25/11/2025 | 1800/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 26/11/2025 | - | Reserve Bank of New Zealand Meeting | ||

| 26/11/2025 | 0030/1130 | *** | Quarterly construction work done | |

| 26/11/2025 | 0030/1130 | *** | CPI Inflation Monthly | |

| 26/11/2025 | 0100/1400 | *** | RBNZ official cash rate decision | |

| 26/11/2025 | 0700/1500 | ** | MNI China Money Market Index (MMI) | |

| 26/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 26/11/2025 | 1200/0700 | ** | Brazil Preliminary CPI | |

| 26/11/2025 | 1230/1230 | Chancellor Reeves to deliver UK Budget | ||

| 26/11/2025 | 1330/0830 | ** | Advance Trade, Advance Business Inventories | |

| 26/11/2025 | 1330/0830 | *** | Jobless Claims | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders | |

| 26/11/2025 | 1330/0830 | ** | Durable Goods New Orders |