MNI EUROPEAN MARKETS ANALYSIS: US-China Talks To Resume

- The USD has lost ground versus the majors, struggling to hold Friday's firmer tone. US Tsy yields are weaker at the front end of the curve, albeit only unwinding a small part of Friday's gains.

- Japan Q1 GDP revisions were positive but market impact negligible. China CPI remained in deflation, while PPI deflation worsened. Trade data saw exports to the US continue to ease, but the overall trade surplus remained elevated.

- US-China trade talks resume in London today.

- Later US April wholesale data and May NY Fed 1-yr inflation expectations print. The ECB’s Elderson speaks. The focus will be on Wednesday’s May US CPI and Friday’s Uni of Michigan June survey.

MARKETS

US TSYS: Tsys Firmer, Led By Front End, 2yr Struggles Near 4.05% Again

The first part of Monday US Tsy trade has seen outperformance, led by the front end. For the 2-5yr tenor yields are off around 3bps. The 10yr Tsy yield is back under 4.49%.

- The 10yr Sep Tsy future has crept higher throughout the session, last at 110-02+, +05+, versus end Friday levels. A direct catalyst for the move haven't been obvious, although we have only given back a modest part of Friday's sell-off.

- For the 2yr Tsy yield, we have struggled once we approach the 4.05% region, going back to mid March. Despite Friday's data beats in the US, there still may be a sense of more downside risks to growth lie ahead, which in turn could be capping upside yield momentum.

- The 10yr, just under 4.49%, remains fairly close to the mid-point of recent ranges.

- Looking ahead, we have wholesale inventories tonight, then tomorrow NFIP small business sentiment and NY Fed inflation expectations. The main focus will be on Wednesday's CPI print though.

JGBS: Futures Edge Up, Cash JGB Yields Firm, Back End Leads

JGB futures sit slightly above end Friday Friday levels from last week. The June future last 139.20, -.15 versus settlement levels. Outside of a modest rise at the start of the session, we have traded fairly tight ranges so far in Monday trade. A modest rebound in US Tsy 10yr futures has likely seen some positive spill over.

- The local data calendar saw positive Q1 GDP revisions, but these didn't impact JGB sentiment. Consumption was revised slightly higher, while inventories contributed more to growth than the initial estimate. Business spending remained positive but was revised down. Overall q/q growth was flat (from an initial estimate of -0.2%).

- For cash JGB yields, the bias is higher, but we sit away from best levels for the 10yr. We were last near 1.48% (session highs rest at 1.491%). It has been a similar backdrop across other parts of the curve. The 30yr has seen some slight outperformance in yield terms, up close to 4bps, last around 2.92%.

- Focus remains on how government issuance may chance, and/or BOJ bond buying shifts as well. We haven't seen any fresh developments on this front today though.

- PM Ishiba has been on the news wires stating that public and financial market trust in Japan's finances must be maintained (via RTRS).

BONDS: NZGB Yields Firm, But Away From Session Highs

New Zealand government bond yields sit firmer but away from session highs. Spill over from softer US Tsy yields, particularly at the front end of the curve, has been evident as Asia Pac Monday trade has unfolded.

- The 10yr was last around 4.64%, still up around 3bps for the session. Earlier highs were close to 4.67%. Other parts of the curve are up around 2-3bps, except for the 2yr, which is back to flat, last around 3.39%. The US 2yr struggled to build on Friday momentum, we were last near 4.00%.

- NZ-US 2yr swap spreads were last near -62bps, just up from Friday lows.

- On the data front, we had Q1 manufacturing volumes up 2.4%q/q, against a revised 1.2% gain in Q4. Activity was +5.1%q/q, versus 3.0% in Q4.

- RBNZ Chief Economist Conway was interviewed today on Radio NZ and said that the central bank expects core inflation to moderate towards the 2% band mid-point by end-2025 going into 2026 despite the recent pickup in headline inflation. He also expects growth to improve later in the year helped by easier monetary policy, but the “labour market is pretty flat”.

- The local data calendar is empty tomorrow.

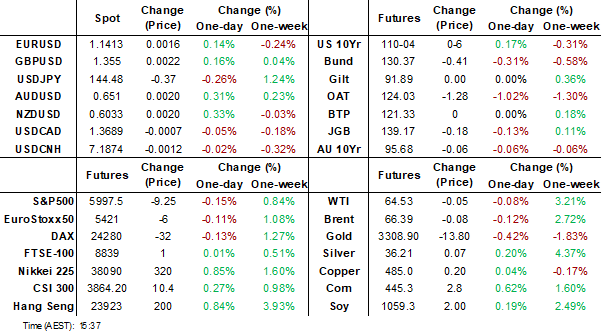

FOREX: US$ Weaker As Yields Fall Following Friday’s Rise, A&/NZ$ Outperform

The BBDXY USD index is down 0.2% today at 1209.86 off the intraday low of 1209.18 with the fall broad based across G10 currencies. It reached 1211.95 early in the session but has been pressured by lower US bond yields with the 2-year down around 3bp from Friday. Kiwi and Aussie have benefited the most as risk appetite also improved and drove equity markets higher across the region.

- NZDUSD is up 0.4% today to 0.6038, close to the intraday high of 0.6042. Earlier Q1 manufacturing volumes were strong up 2.4% q/q, while RBNZ Chief Economist Conway expects core inflation to fall to the band mid-point but noted that the labour market remains lacklustre.

- AUDUSD has trended higher and is currently up 0.4% to 0.6518. Initial resistance is at 0.6538, 5 June high. AUDNZD is slightly higher at 1.0796 following a peak of 1.0803 but has not been able to hold breaks above 1.08.

- USDJPY is down 0.3% to 144.47, close to the intraday low of 144.35. Japanese data today on balance were slightly stronger with Q1 GDP revised up to flat on the quarter from -0.2% q/q, the Eco Watchers survey rose in May and the April trade deficit was slightly lower than expected.

- EURUSD is 0.2% higher at 1.1418 as is GBPUSD at 1.3554 leaving EURGBP flat at 0.8424.

- USDCAD is up 0.1% to 1.3684 after outperforming the G10 on Friday.

FOREX: CFTC Data Mixed, JPY Leveraged & Asset Manager Shifts Offset Each Other

CFTC positioning shifts were mixed across the major currencies in the week ending June 3, see the table below. For yen, we saw leveraged contracts rise, but this was offset by a contraction in asset manager positioning in the currency. Still, asset managers remain long from an outright standpoint, so too do leveraged players.

- For EUR we saw little shift in the leveraged space (with an outright short still present), while asset managers added modestly to existing longs.

- GBP small net purchases for both asset managers and leveraged players. Assets managers are almost back to a net long position.

- AUD and NZD saw leveraged names add modestly to existing shorts. There was little net change in asset manager positioning for these currencies.

Table 1: Weekly Change & Outright Positioning Per Major Currency - CFTC

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | 4728 | 23315 | -4945 | 109920 |

| EUR | 684 | -15355 | 5393 | 344880 |

| GBP | 1257 | 46475 | 1618 | -1283 |

| AUD | -2371 | -19493 | -491 | -32356 |

| NZD | -1235 | -8234 | 639 | -18407 |

| CAD | -888 | -43405 | 2481 | -67496 |

| CHF | 1611 | 2969 | -2167 | -31191 |

| MXN | -150 | -9601 | 3408 | 37251 |

Source: Bloomberg Finance L.P. / MNI

ASIA STOCKS: Major Asia Pac Markets Firmer, Kospi Continues To Outperform

Asian equity markets are mostly trading with a positive footing in the first part of Monday trade. The Nikkei 225 is up around 1%, likewise for the Hang Seng in Hong Kong. The Kospi continues to be an outperformer, up over 1.6%.

- We had a positive lead from US markets on Friday, the SPX up a little over 1%. US data beats, particularly on the wages may have helped. Also, today in London we have US-China trade talks resuming. Positive themes around exports of rare earths resuming to the US and the EU is another positive ahead of these talks.

- Fallout from protests in major US cities (with Trump calling in the National Guard for Los Angeles) is not impacting US equity sentiment greatly at this stage.

- Still, China's CSI 300 is up only modestly, last +0.18% at the lunchtime break, putting the index near 3881. Earlier China data showed CPI remain in deflation, while PPI deflation worsened further. This underscores on-going policy support needs in 2025. On the trade front, export and imports where both below forecasts, with trade to the US continuing to fall.

- The HSI is up +1% at the break, with the tech sub index up +2.3% at this stage.

- The Kospi continues to outperform, up over 1.6%. This puts the index within striking distance of July 2024 highs around 2900. Offshore investors have bought $348mn of local shares today. Optimism around the domestic outlook continue to buoy sentiment.

- In South East Asia, gains are more modest, mostly under 0.50%. Australian and Indonesian markets are closed today.

OIL: Crude Holds Friday’s Gains As US-China Trade Talks Scrutinised

Oil prices have held onto Friday’s 2% gains and are only slightly lower during today’s APAC trading. News that US-China trade talks would take place in London on Monday and data showing no deterioration in the US labour market in May despite heightened trade uncertainty drove the jump in prices last week. WTI is currently down 0.1% to $64.52/bbl, close to the intraday low of $64.47, while Brent is -0.1% to $66.41/bbl following $66.36. The USD index is down 0.2%.

- Oil markets have been concerned that increased protectionism would weigh on global energy demand and so they will be monitoring US-China negotiations closely. A lack of an agreement would likely significantly impact China’s domestic demand and thus oil consumption as it is the world’s largest importer of crude.

- Supply developments remain in focus as OPEC normalises output and the sanctions outlook continues to be unclear. In terms of demand, the US driving season, which began at the end of May, will also be watched closely for signs of weakness.

- Volatility in the oil market has been low recently and futures structures are bullish with the Brent prompt spread widening further in backwardation, according to Bloomberg.

- Later US April wholesale data and May NY Fed 1-yr inflation expectations print. The ECB’s Elderson speaks. The focus will be on Wednesday’s May US CPI and Friday’s Uni of Michigan June survey.

Gold Little Changed Today, Significant Risks Persist Though

Gold prices are currently slightly higher during today’s APAC session and off the intraday low of $3293.64/oz. They are up to $3311.4, just below support at $3313.2, 20-day EMA. Better risk appetite is pressuring gold, while the softer US dollar (USD BBDXY -0.2%) and lower US yields are supporting it.

- Bullion will be monitoring progress closely when the US and China meet later today in London to discuss trade. Any sign that the two sides are unlikely to agree would likely increase safe-haven flows into the yellow metal.

- Data showing that the US jobs market was resilient in May to the increased trade tensions weighed on gold prices on Friday.

- US fiscal developments are also important. Thus, Thursday’s US Treasury bond auction and news on the likelihood of President Trump’s tax cut bill passing the senate will be watched closely. Increased fiscal risks have also driven safe haven flows.

- Silver has range traded and is currently up 0.2% to $36.05. It has moved between $35.92 and $36.09, also between initial support and resistance.

- Equities are stronger with the Nikkei up 1.0% and Hang Seng +1.0% but S&P e-mini down 0.2%. Oil prices are slightly lower with WTI -0.1% to $64.52/bbl. Copper is flat and iron ore is back below $95/t.

- Later US April wholesale data and May NY Fed 1-yr inflation expectations print. The ECB’s Elderson speaks. The focus will be on Wednesday’s May US CPI and Friday’s Uni of Michigan June survey.

CHINA DATA: CPI Remains In Deflation, Risks From Trade War Persist

China’s May CPI inflation remained weak at -0.1% y/y, slightly better than consensus expectations, while core picked up 0.1pp to 0.6% y/y, the highest since January. Producer prices deteriorated further falling 3.3% y/y after -2.7% in April and the weakest since July 2023, signalling some possible upcoming downward pressure on headline inflation. Services & manufacturing PMIs signal a further softening in prices.

- Price wars have pushed prices into deflationary territory and kept them there. There is a significant risk that the CPI will stay negative due to trade tensions with the US, although talks are scheduled to continue today, as well as continued soft demand and intense competition.

- Lower oil prices and negative base effects pushed producer prices further into deflation. Also significant inventory building before the US announced a 90-day reprieve to its punitive tariffs on imports from China pushed input prices lower. Weaker fuel prices would have also impacted headline CPI.

- While talks to come to a trade deal with the US are ongoing, a return to a trade war would likely pressure China’s domestic demand and push prices further into deflation.

- China’s CPI is expected to rise 0.3% y/y this year with PPI -2% y/y, according to a Bloomberg survey.

China CPI vs PPI y/y%

Source: MNI - Market News/LSEG

CHINA DATA: Exports & Imports Below Forecasts, Exports To US Fall Further

China's May trade data saw recent trends broadly maintained, while outcomes were slightly below market expectations. Exports were 4.8%y/y, against a 6.0% forecast and 8.1% prior. Imports fell -3.4%y/y (versus -0.8% forecast and -0.2% prior). This left the trade surplus at $103.22bn, above April's outcome ($96.18bn) and the market consensus of $101.1bn.

- Trade with the US remains a focus point, with exports now down to $28.82bn, versus levels close to $49bn at the end of last year. This a -34%y/y outcome, per Bloomberg. Exports with other parts of Asia were mostly down a touch in May.

- Offset came from exports to the EU, up to $49.50bn from $46.71bn prior. Most individual EU countries saw a rise. Exports to the UK were yup to $7.46bn from $6.92bn and to Brazil, $6.45bn from $5.72bn.

- The trade surplus with the US eased to $18.01bn, from $20.46bn. To the EU it was steady at $26.62bn from $26.67bn. With parts of Asia, China's trade position was little changed from April levels.

- On the import side, volumes for commodity imports were mostly down, except for soybeans and natural gas. Coal, crude oil and iron ore were all off April levels.

- Focus will be on US-China trade talks alter today in London, although trends still slowed in May in terms of exports to the US, even with lower tariff levels agreed to at the meting in Geneva.

ASIA FX: NEA FX Underperforms Softer USD Trend V Majors, US-China Talks Later

In North East Asia FX markets, market moves have been fairly modest in Monday trade so far. These pairs have underperformed a generally softer tone seen for the USD against the majors.

- China released the May inflation data, which showed CPI remaining in deflation, while PPI deflation worsened. We also had the May trade figures, which saw export and import growth below expectations, but the trade surplus remained wide. Exports to the US continued to slow. USD/CNH hasn't reacted much though, holding under 7.1900 for much of today's session, but with limited downside. US-China trade talks resume in London today, with focus on rare earths following positive weekend news around export approvals in this space.

- South Korean markets returned after Friday's break. Spot USD/KRW got to highs above 1364, in catching up with Friday's USD gains, but we turned back lower quickly. The pair got near 1355 before stabilizing, we were last 1357/58, still around 0.15% weaker in won terms from levels last Thursday. Local equities continue to outperform, riding the wave of domestic optimism (the Kospi up a further 1.5%).

- USD/TWD has nudged a little higher but remains under 30.00 at this stage. Later on we get May trade figures for Taiwan.

- USD/HKD remains supported on dips, the pair approaching fresh cycle highs of 7.8480.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 09/06/2025 | 0500/1400 | Economy Watchers Survey | ||

| 09/06/2025 | 0900/1100 | ECB Elderson On Rule Of Law At Italian Court | ||

| 09/06/2025 | - | *** | Trade | |

| 09/06/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/06/2025 | 1400/1000 | ** | Wholesale Trade | |

| 09/06/2025 | 1500/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 09/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 09/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 10/06/2025 | 2301/0001 | * | BRC-KPMG Shop Sales Monitor | |

| 10/06/2025 | 0600/0800 | *** | CPI Norway | |

| 10/06/2025 | 0600/0700 | *** | Labour Market Survey | |

| 10/06/2025 | 0600/0800 | ** | Private Sector Production m/m | |

| 10/06/2025 | 0800/1000 | * | Industrial Production | |

| 10/06/2025 | 1000/0600 | ** | NFIB Small Business Optimism Index | |

| 10/06/2025 | - | *** | Money Supply | |

| 10/06/2025 | - | *** | New Loans | |

| 10/06/2025 | - | *** | Social Financing | |

| 10/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index |