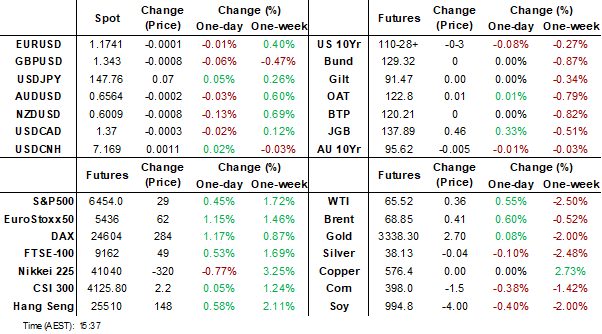

MNI EUROPEAN MARKETS ANALYSIS: Trade Talks Remain In Focus

- EU and US equity futures are higher following headlines of a US-EU trade deal, which will see a 15% tariff apply on most EU exports to the US. Market reaction elsewhere is fairly limited, with early USD weakness reversing, while US Tsy yields are little changed.

- Trade talks remain in focus with US-China discussions taking place in Stockholm today. The trade truce is expected to be extended.

- On the data front, only the July Dallas Fed manufacturing, and the ECB survey of monetary analysts are released.

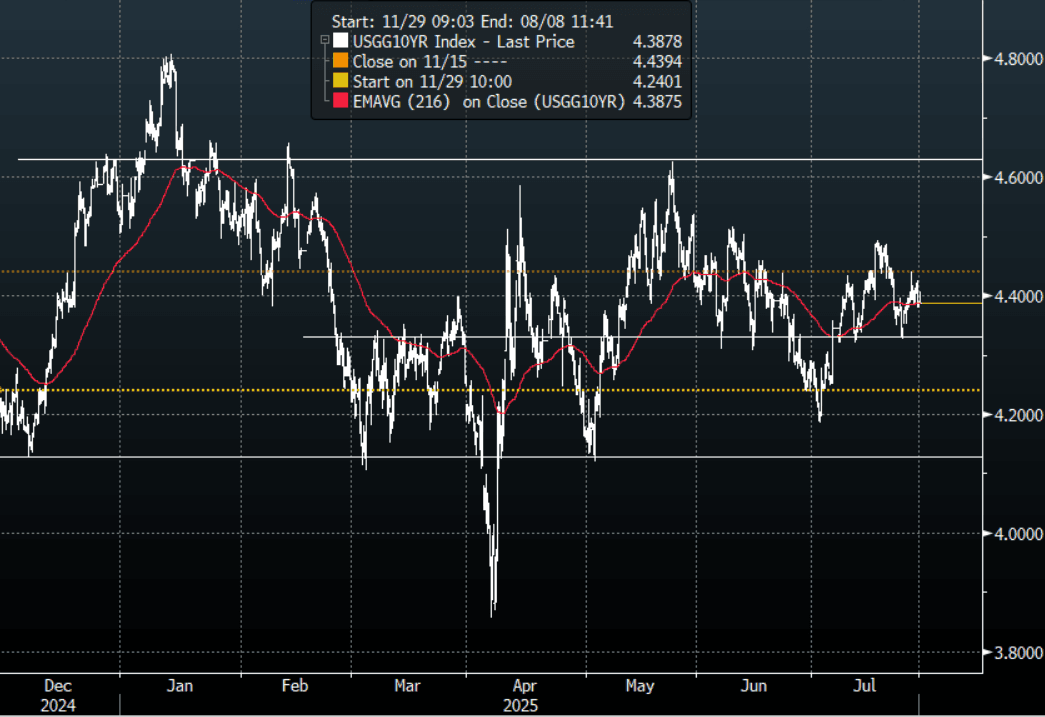

US TSYS: Yields Largely Unchanged In The Asia-Pac Session

The TYU5 range has been 110-26 to 110-30+ during the Asia-Pacific session. It last changed hands at 110-30, down 0-01 from the previous close.

- The US 2-year yield is trading around 3.923%.

- The US 10-year yield is trading around 4.388%.

- The 10-year yield has moved back towards its pivot within the wider range 4.10% - 4.65%, decent supply was seen around 4.30/35% first up. A decent bounce off its support but the move has failed to follow through above 4.40% for now. The Data this week should provide more clarity going forward.

- (Bloomberg) - “Strong demand for investment-grade corporate bond supply is likely to overwhelm a lack of supply this week. That can act to narrow US high-grade bond spreads.”

- (Bloomberg) - “Investors pulled $3.9 billion from Treasuries in June and added $10 billion to US and European IG company debt — a shift away from the idea that US government debt is the safest bet.”

- Data/Events: Dallas Fed Manf. Activity

Fig 1: 10-Year US Yield 120min Chart

Source: MNI - Market News/Bloomberg Finance L.P

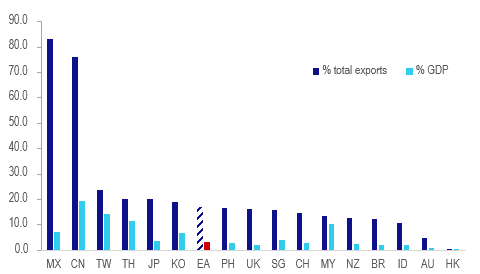

TARIFFS: Europe Large Source Of US Imports But Its Economy Is Less Exposed

A trade deal has been reached between the US and the European Union ahead of this week’s August 1 deadline. The EU was threatened with 30% tariffs but 15% was settled on, in line with Japan, but significantly higher than the current non-agricultural weighted average around 1%. Euro stoxx futures are up 1.0% in APAC trading outperforming the S&P’s +0.4%. EURUSD’s response has been muted.

- The EU is the second largest source of US imports thus a deal was likely but given the significant rise in import duties is also likely to drive higher US prices. The 2024 US deficit with the EU was $235.9bn, but still less than China’s $295.5bn.

- Exports to the US are important with 16.8% of 2024 extra-euro area goods shipments going there but that was worth only 3.2% of GDP, below the exposure of Canada, Mexico and Taiwan but similar to Japan’s.

Exports to the US (ex NAFTA) 2024 %

- The EU is the second largest source of US auto imports and Germany is fifth. Shipments will also face 15% tariffs but below the 25% duty against all US vehicle imports.

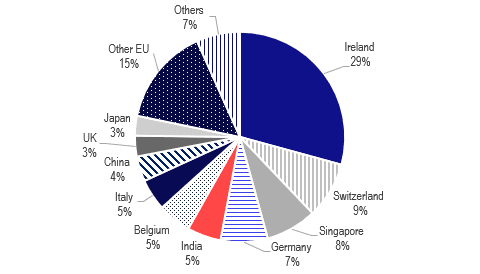

- Pharmaceuticals will also face 15% but it was threatened with up to 200%. 30% of US pharma imports come from Ireland and 57% from the EA accounting for over a quarter of total EA exports to the US.

- The 50% tariff on US imports of steel and aluminium is unchanged but both sides agreed not to tax aircraft and parts.

- Like others, Europe has frontloaded shipments to the US with them peaking at 60.8% y/y in March and easing to 7.3% y/y in May. Bloomberg data showed container ship departures from the EU-6 at around 100/day in the first week of July but that eased to 70 last week well below the pre-2025 average of 95.

US imports of pharmaceuticals & medicines % total 2024

JGBS: Belly Leads Yields Lower, 2Y Supply Tomorrow, BOJ Decision On Thurs

JGB futures are stronger and hovering near session bests, +44 compared to the settlement levels.

- Cash US tsys are little changed in today's Asia-Pac session.

- Cash JGBs are 1-5bps richer across benchmarks, with the futures-linked 7-year outperforming. The benchmark 10-year yield is 4.5bps lower at 1.560% versus the cycle high of 1.616%.

- " Japan's central bank might signal a shift toward a less dovish stance, BofA economists say in a note. The Bank of Japan is widely expected to maintain its policy rate at 0.5% at the monetary policy meeting this week. But it will likely strike a less dovish tone, given the recent trade deal Japan struck with the U.S., they say. The agreement reduces a big uncertainty the BOJ had pointed to as a reason for holding off on tightening policy.” (BBG)

- We expect no policy changes at this week's BOJ policy meeting. The market's focus will be on the forecast changes in the BOJ's Outlook Report and the tone of the Governor's press conference regarding future rate hikes.

- Swap rates are 1-3bps lower, with a steepening bias. Swap spreads are mixed.

- Tomorrow, the local calendar will be empty apart from 2-year supply.

AUSSIE BONDS: Subdued Session, Focus On Wednesday's Q2 CPI

ACGBs (YM +0.5 & XM +0.5) are little changed.

- Cash US tsys are little changed in today's Asia-Pac session. Today's US calendar will see Dallas Fed Manf. Activity.

- The focus of this week will be Wednesday's Q2 CPI data, which is expected to show the underlying trimmed mean measure making further progress towards the band mid-point of 2.5%. Bloomberg consensus is forecasting a 0.7% q/q rise, bringing the annual rate to 2.7% after 0.7% & 2.9% in Q1. This is slightly higher than the RBA's May Q2 forecast of 2.6%. Services developments will also be monitored. The RBA is expected to cut rates 25bp on August 12.

- Cash ACGBs are unchanged with the AU-US 10-year yield differential at -5bps.

- The bills strip is slightly weaker, with pricing flat to -2.

- RBA-dated OIS pricing is slightly firmer across meetings today. A 25bp rate cut in August is given a 91% probability, with a cumulative 57bps of easing priced by year-end (based on an effective cash rate of 3.84%).

- This week, the AOFM plans to sell A$1000mn of the 2.25% 21 May 2028 bond tomorrow and A$1200mn of the 2.75% 21 June 2035 bond on Friday.

BONDS: NZGBS: Closed With A Modest Bull-Flattener

NZGBs closed at session bests, with the 2/10 curve showing a bull-flattener. Yields closed 1-3bps lower after being 1-2bps higher earlier in the session.

- The NZ-US and NZ-AU 10-year yield differentials finished 2-3bps tighter, reversing Friday's widening.

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed little changed across meetings. 21bps of easing is priced for August, with a cumulative 35bps by November 2025.

- This week, the local calendar will see ANZ business confidence for July released on Wednesday. It continues to point to a gradual recovery in the economy. Cost and price components remain elevated, and inflation expectations are at 2.7% off their low.

- ANZ July consumer confidence is out on Friday. It rose sharply in June to 98.8, the highest this year but still off December's 100.2. Rate cuts, which take time to feed through to mortgage payments, have helped with households' financial situation and improved the time to buy component.

- June building permits will also print on Friday. They rose 10.4% m/m in May and indicators suggest that the construction sector is recovering.

- On Thursday, the NZ Treasury plans to sell NZ$275mn of the 4.50% May-30 bond and NZ$175mn of the 4.25% May-34 bond.

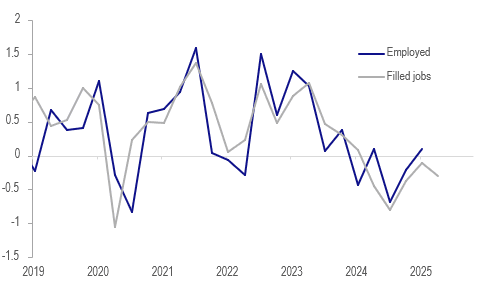

NEW ZEALAND: Labour Market Remained Weak In Q2

June filled jobs rose a lacklustre 0.1% m/m but down 1.1% y/y following a downwardly-revised -0.1% m/m & -1.7% y/y. This left Q2 down 0.3% q/q and -1.6% y/y after -0.1% & -1.7% in Q1, suggesting that while the pace of deterioration has slowed, the labour market continues to struggle. Q2 labour data is published on August 6 and this data implies (there is a 50% correlation between quarterly rates) that employment may have fallen again after rising 0.1% q/q in Q1, which would increase the chance of an August rate cut.

- The primary sector saw a strong rise in filled jobs in June up 0.9% m/m and services a moderate one of 0.2%. Goods-producing industries fell 0.2% m/m.

- Compared to a year ago construction jobs are still down 6%, professional & technical services -2.7% and manufacturing -2.5%. Education and training is 2.0% higher.

- Changes in youth unemployment tend to lead the labour market as a whole, and filled jobs for 15-19 year olds were down 10% y/y in June and for 20-24 years -3.5% y/y. In terms of age, the first group to see an increase is 35-39 years at 2% y/y.

NZ filled jobs vs employment q/q%

FOREX: Asset Managers Sell GBP, AUD & Buy EUR - CFTC

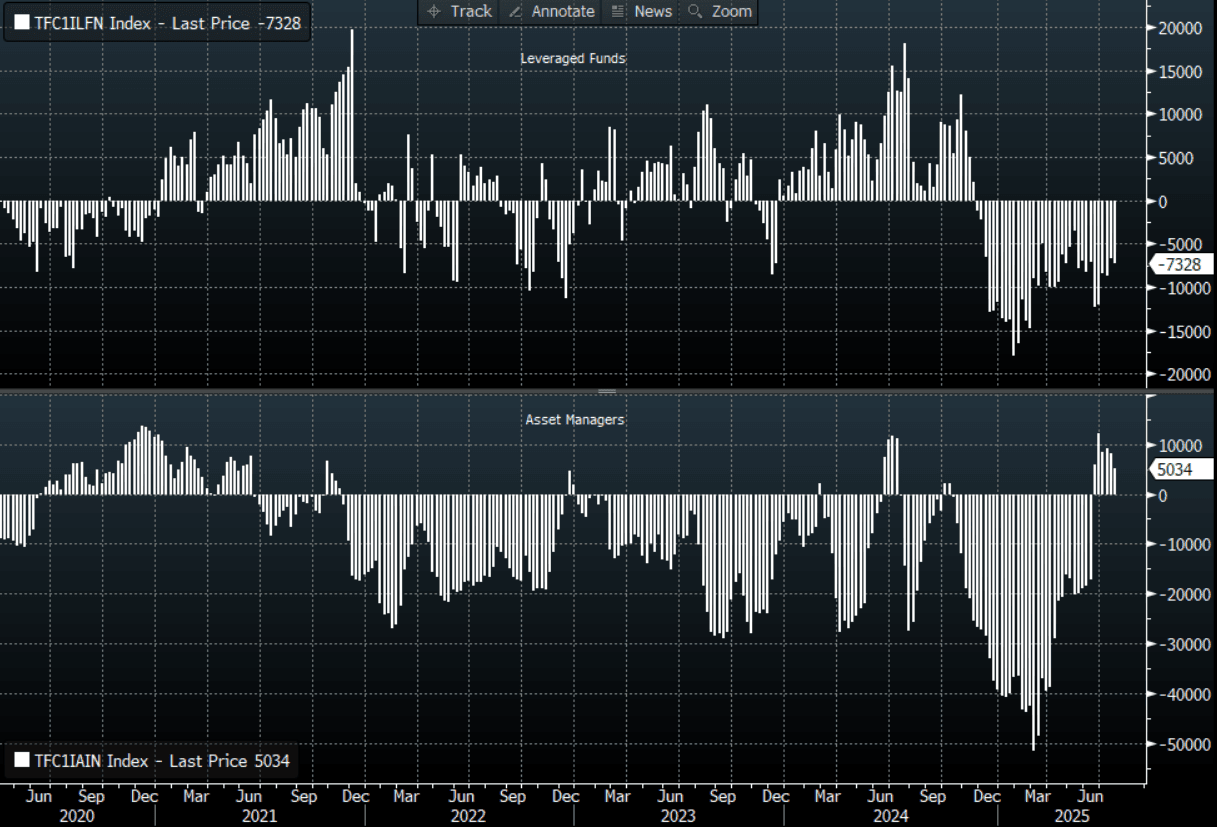

Last week saw asset managers selling both GBP and AUD in decent size, while adding to the EUR. Trends on the leveraged side were more mixed.

- For JPY, we saw little net change in positioning with leveraged investors trimming net shorts modestly, while asset managers added a touch to the net long position.

- EUR trends were mixed, with leveraged investors further selling down EUR holdings, which are still modestly long. Asset managers more than offset these flows though by adding to the already large net long position.

- GBP flows saw leveraged investors add to longs, but asset managers were large sellers of GBP. This segment's outright short is now the largest since mid Feb of this year.

- It was a similar backdrop for the A$, where leveraged investors pared shorts, but asset managers added to their outright holdings.

Table 1: CFTC FX Positioning By Currency - Weekly Change/Outright Positioning

| Leveraged Contracts | Asset manager Contracts | |||

| Weekly Change | Outright Position | Weekly Change | Outright Position | |

| JPY | 1035 | -11571 | 716 | 72326 |

| EUR | -8110 | 7151 | 15494 | 399754 |

| GBP | 5066 | 53535 | -31991 | -58458 |

| AUD | 8038 | -12010 | -15692 | -53959 |

| NZD | -584 | -7328 | -3158 | 5034 |

| CAD | -3332 | -29725 | 2134 | -47805 |

| CHF | -2602 | -2761 | 254 | -33768 |

| MXN | 9898 | 9150 | -4702 | 38373 |

Source: Bloomberg Finance L.P./CFTC/MNI

FOREX: Asia FX Wrap - BBDXY Opens Lower But Claws Back Losses.

The BBDXY has had a range of 1196.82 - 1198.86 in the Asia-Pac session, it is currently trading around 1198, -0.04%. The USD’s slide lower finally stalled at the back end of last week and some profit-taking was seen. The market is much more comfortable selling USD’s and while below 1220 rallies should continue to find supply. There is lots of event risk coming up this week and we are heading into month-end so caution is warranted, this could potentially see some more paring back of USD shorts. Worth noting that corporate month-end tomorrow will most likely see some USD demand as well.

- EUR/USD - Asian range 1.1747 - 1.1770, Asia is currently trading 1.1750. The pair’s upward momentum seems to be stalling towards 1.1800. The price looks a little stretched in the short term, but while the USD is trading poorly the EUR will continue to be the main beneficiary. No real follow through on the trade deal in our session.

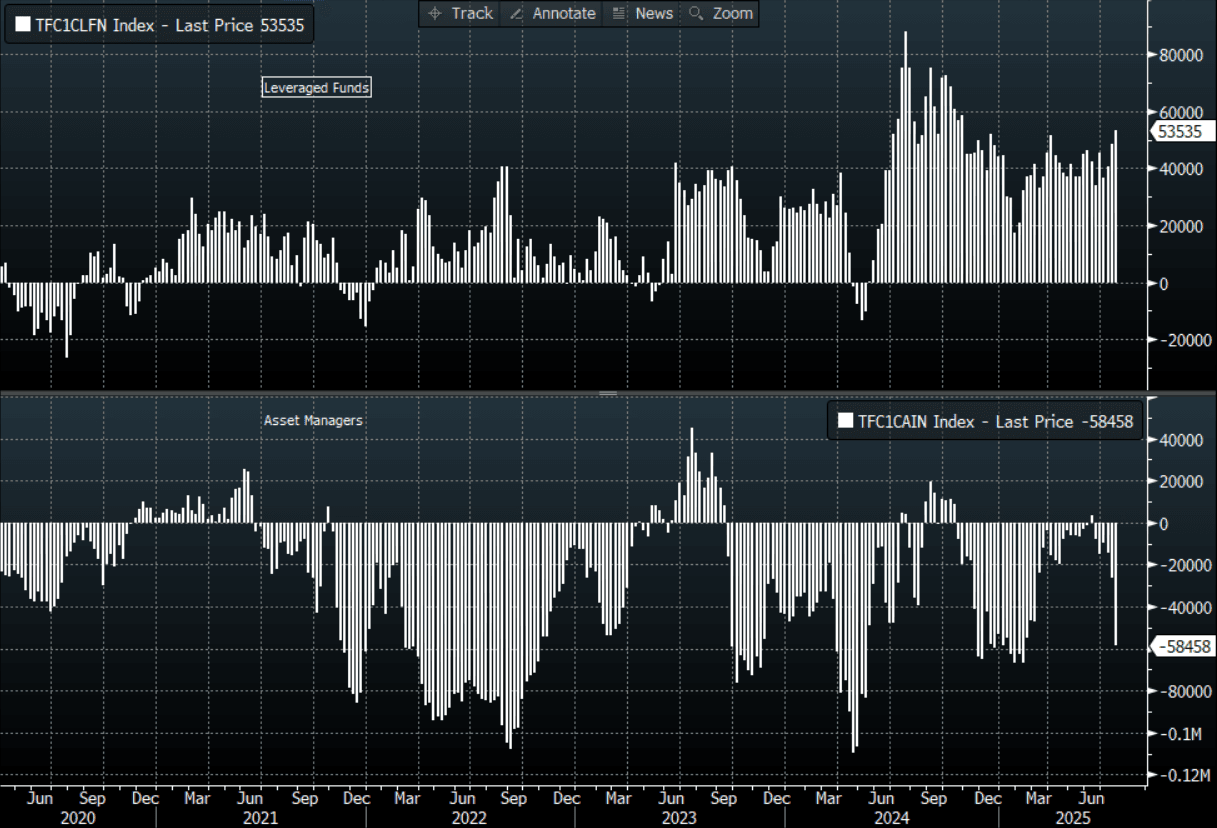

- GBP/USD - Asian range 1.3428 - 1.3453, Asia is currently dealing around 1.3440. The support around 1.3350/1.3400 has proved to be solid first up. The pair could not build on its move higher and has drifted back to the middle of its recent range. While the support holds the market will be encouraged to continue to play from the long side. A sustained break below 1.3350 could signal a deeper correction. CFTC Data shows Asset managers sold quite aggressively last week building their shorts back up -58458(Last -26467)

- USD/CNH - Asian range 7.1511 - 7.1722, the USD/CNY fix printed 7.1467, Asia is currently dealing around 7.1680. Sellers should be around on bounces while price holds below the 7.2000 area and the PBOC manages the fix lower. Above 7.2000 and we could see a test of the USD Shorts.

- Cross asset : SPX +0.42%, Gold $3341, US 10-Year 4.388%, BBDXY 1198, Crude oil $65.43

- Data/Events :

Fig 1: GBP CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia Wrap - USD/JPY Consolidates Above 147.50

The Asia-Pac USD/JPY range has been 147.52 - 148.02, Asia is currently trading around 147.65, -0.03%. USD/JPY found good demand around 146.00 last week and has bounced nicely off its first support. Some demand for USD’s was finally seen as the market takes some risk off the table heading into this week which is filled with event risk and also month-end. Corporate month-end to start the week with most of the USD demand most likely to be seen tomorrow.

- First Squawk on X: “JAPAN SAYS ONLY 1–2% OF $550B U.S. FUND WILL BE DIRECT INVESTMENT; REST TO BE LOANS. Japan expects that just 1% to 2% of its recently announced $550 billion partnership fund with the U.S. will involve actual capital investment, with the remainder provided through loan-based financing, officials said.”

- (Bloomberg) - "Japan’s pledge for a $550 billion US investment fund may have been key to Tokyo getting a trade deal, but neither side seems to agree on what it looks like, Gearoid Reidy writes. The market’s sigh of relief about this pact might still be premature.”

- “The Bank of Japan is likely to hold at its meeting in the coming week. We’ll watch for its assessment of Japan’s trade deal with the US and view on the impact of tariffs on the economic outlook. Inflation pressures still point to the need to pare stimulus. We expect that in October.” - BBG

- "JAPAN ISHIBA CABINET APPROVAL RATING DROPS TO 34.6% IN FNN POLL" - BBG

- Options : Close significant option expiries for NY cut, based on DTCC data: 148.00($1.02b),148.25($1.04b).Upcoming Close Strikes : 145.00($1.3b July 29), 146.00($971m July 31) - BBG.

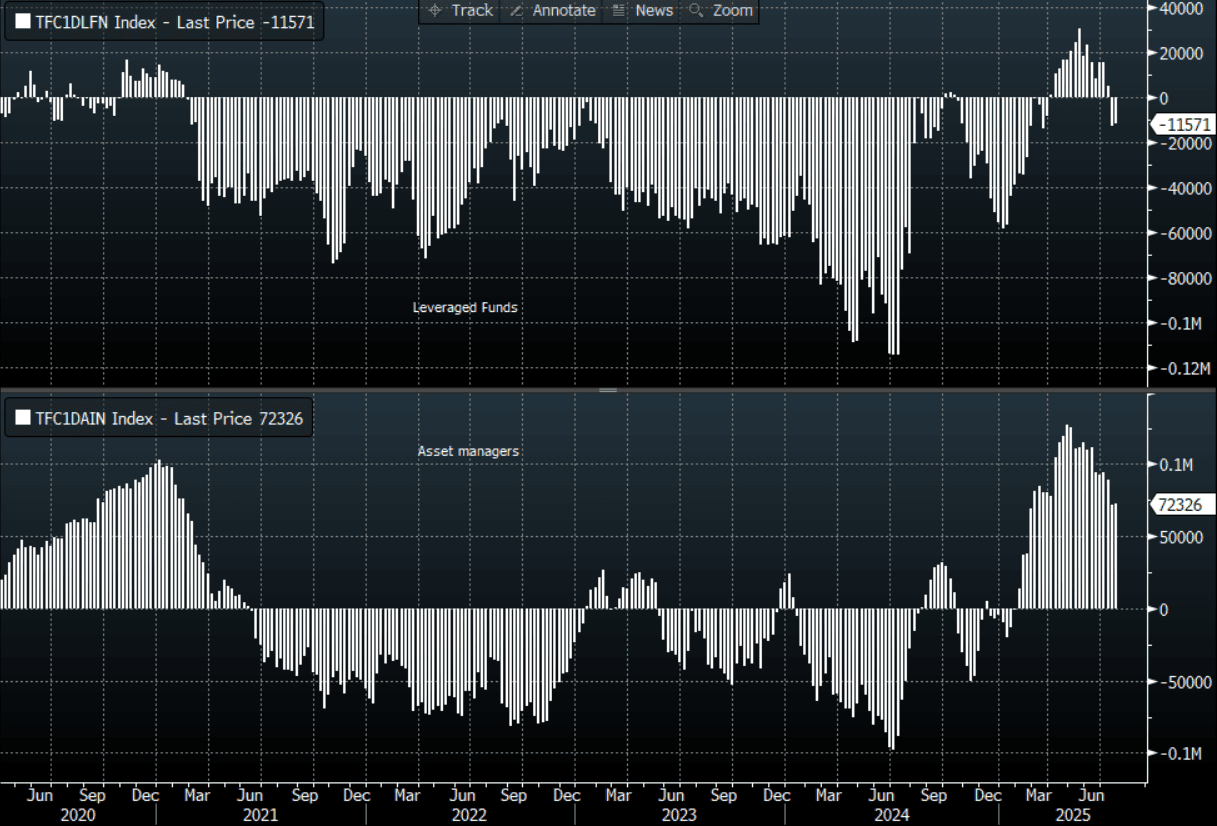

- CFTC data shows Asset managers surprisingly added slightly to their JPY longs +72326( Last +71610), while leveraged funds have slightly reduced their newly built short JPY position -11571(Last -12606).

Fig 1 : JPY CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia Wrap - AUD/USD Tries Higher On Trade Deal, No Follow Through

The AUD/USD has had a range of 0.6566 - 0.6586 in the Asia- Pac session, it is currently trading around 0.6567, +0.02%. The pair traded with a heavy tone all through Friday but has attempted to bounce this morning as the market digests news of a US-EU trade deal. The pair failed to gain any momentum above 0.6600 last week and now awaits a very busy calendar this week which could have meaningful implications for risk. Locally the Australian Q2 CPI on Wednesday will be closely watched and could provide a catalyst for some movement. Worth keeping in mind we are approaching the corporate month-end so there could be a demand for some USD’s today but more likely that flow will be executed tomorrow.

- The focus of this week will be Wednesday's Q2 CPI data, which is expected to show the underlying trimmed mean measure making further progress towards the band mid-point of 2.5%. Bloomberg consensus is forecasting a 0.7% q/q rise, bringing the annual rate to 2.7% after 0.7% & 2.9% in Q1. This is slightly higher than the RBA's May Q2 forecast of 2.6%. Services developments will also be monitored. The RBA is expected to cut rates 25bp on August 12.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD608m), 0.6550(AUD555m). Upcoming Close Strikes : 0.6600(AUD968m July29), 0.6600(AUD1.38b July 31), 0.6465(AUD1.01b July31) - BBG

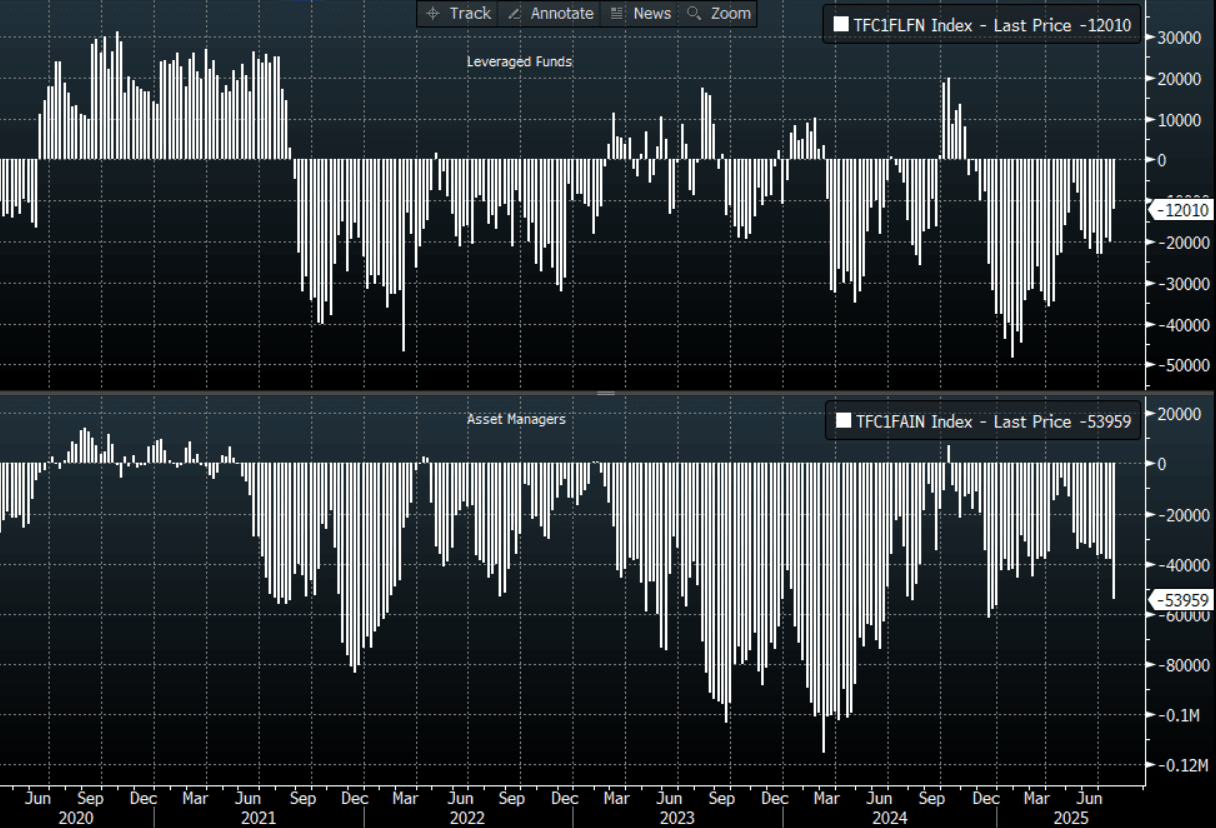

- CFTC Data shows Asset managers added a decent clip to their shorts -53959(Last -38267), the Leveraged community reduced their own shorts to -12010(Last -20048).

- AUD/JPY - Today's Asia-Pac range 97.03 - 97.29, it is trading currently around 96.95, +0.01%. The pair is pressing above its highs of last week. The support between 95.00 - 96.00 held very well last week and the pair is looking to regain its momentum for a move higher. The event-risk coming up this week could provide some short-term headwinds.

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia Wrap -NZD/USD Can't Hold Onto Early Gains

The NZD/USD had a range of 0.6011 - 0.6033 in the Asia-Pac session, going into the London open trading around 0.6011, -0.10%. The pair traded with a heavy tone all through Friday but has attempted to bounce this morning as the market gets news of a US-EU trade deal. Price will need a sustained break back above the 0.6050/0.6100 area to signal a potential base might be in place. There is lots of event risk coming up this week and we are also heading into the corporate month-end so there could be a demand for USD’s starting today but the flow is more likely to be executed tomorrow.

- NEW ZEALAND: Labour Market Remained Weak In Q2. June filled jobs rose a lacklustre 0.1% m/m but down 1.1% y/y following a downwardly-revised -0.1% m/m & -1.7% y/y. This left Q2 down 0.3% q/q and -1.6% y/y after -0.1% & -1.7% in Q1, suggesting that while the pace of deterioration has slowed, the labour market continues to struggle. Q2 labour data is published on August 6 and this data implies (there is a 50% correlation between quarterly rates) that employment may have fallen again after rising 0.1% q/q in Q1, which would increase the chance of an August rate cut.

- (Bloomberg) -- New Zealand farmers are more confident about current economic conditions but less optimistic about the future, according to a survey conducted by Federated Farmers.

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.6000(NZD395m July 30), 0.5965(NZD424m July 31). - BBG

- CFTC Data shows Asset Managers again reduced their newly built longs in NZD +5034(Last +8192), the Leveraged community added slightly to their shorts last week -7328(Last -6744).

- AUD/NZD range for the session has been 1.0914 - 1.0933, currently trading 1.0925. The cross moved higher in response to the NZ CPI. Dips back to 1.0850/1.0900 should continue to find support as the pair tries to build momentum to move higher.

Fig 1: NZD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Mixed Trends Despite Higher EU Futures On US-EU Trade Deal

Asia Pac stocks are mixed in the first part of Monday trade. This comes despite a better tone to both US and EU equity futures. US futures were last up 0.40-0.55%, with the tech side leading. EU futures were around +1% higher, as market took some comfort from the earlier headlines around a 15% tariff deal between the US and EU (for most EU exports to the US). Positive spillover has been limited to this region so far today.

- Japan markets are weaker, the Topix off around 0.50%, while the NKY 225 is down around 0.90%. Sell-side analysts have noted profit taking ahead of key earnings in the Chip sector as a potential headwind (via BBG), while political uncertainty also continues. PM Ishiba has vowed to stay on as PM, despite recently losing upper house elections (and after onshore media outlets indicated he would resign in August).

- In Hong Kong, markets are modestly higher, the HSI up around 0.4%, while the CSI 300 is down a touch in China. Over the weekend we saw profit results remain negative in y/y terms for June, albeit up from the May decline.

- South Korea's Kospi has been volatile, initially rallying at the open, aiding by a large Samsung chip order (for Tesla) but once again the index has struggled above 3200. Focus remains on US-South Korea trade negotiations ahead of the Aug 1 deadline at the end of the week, with officials set to meet later in the week (reportedly July 31).

- Thailand markets are out today, as the US attempts to lead efforts to de-escalate tensions on the Thailand/Cambodian border.

- Indonesia is up +1.25%, one of the better performers in SEA so far today. The initial tone in Indian markets is for modest downside, continuing the recent run of underperformance for these markets.

ASIA STOCKS: Positive Taiwan Inflow Trend Continues, Thailand Inflows Slowed

Taiwan net equity flows remained the standout into the end of last week. The 5-day sum was +$1.422bn. This is down slightly from recent highs (just above $2.5bn), but the 5-day rolling sum of net inflows has been positive since late June, indicating consistent positive inflow momentum, as Taiwan equities ride firmer chip/AI sentiment. The Taiex sits just off multi month highs in latest dealings this morning.

- Inflows also remained positive into South Korea, with last week seeing slightly stronger inflow momentum at +$1.64bn compared to Taiwan. Still, Taiwan maintains better inflow trends more broadly. The Kospi still struggles above the 3200 level though and has been volatile in the first part of trade today. We shot higher on positive Samsung chip order headlines, but haven't been able to sustain these gains.

- Focus also remain on US-South Korea trade negotiations ahead of the Aug 1 deadline this Friday, with focus on US access to South Korean agricultural markets, while South Korea may also invest into US shipbuilding.

- Recent positive Thailand equity inflow momentum slowed on Friday, with border clashes between Thailand and Cambodia not likely helping sentiment. Still net outflows were very modest and remain up strongly in the past 5 days. Note Thailand markets are closed today.

- Elsewhere flow trends were generally negative, with India still struggling to see upside momentum.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 263 | 1640 | -6356 |

| Taiwan (USDmn) | 331 | 1422 | 1695 |

| India (USDmn)* | -231 | -113 | -9008 |

| Indonesia (USDmn) | -14 | -8 | -3611 |

| Thailand (USDmn) | -8 | 273 | -1951 |

| Malaysia (USDmn) | -32 | -21 | -2863 |

| Philippines (USDmn) | 2 | 6 | -616 |

| Total (USDmn) | 310 | 3199 | -22709 |

| * Data Up To July 24 |

Source: Bloomberg Finance L.P./MNI

OIL: Crude Slightly Higher Following EU-US Deal, Key Events This Week

Oil prices are moderately higher during today’s APAC session after falling over a percent on Friday as another trade deal with the US has helped to alleviate concerns that increased protectionism would weigh on global energy demand. WTI is up 0.6% to $65.57/bbl after a low of $65.05. Brent is 0.6% higher at $68.85/bbl off today’s peak of $68.88. The USD index is little changed.

- The EU reached an agreement with the US for tariffs of 15% except steel & aluminium which still face 50% and aircraft & parts that will have no duty. The EU agreed to buy $750bn of US energy over the remainder of President Trump’s term and invest $600bn in the US.

- The oil market will be watching the outcome of US-China talks starting today and Sunday’s OPEC meeting closely as well as the tone from Wednesday’s Fed decision (it is widely expected to keep rates unchanged). Key data this week include US Q2 GDP & June PCE July 30 & 31, and US July payrolls August 1.

- OPEC is meeting today to determine where the oil market is at before the August 3 output decision. It is expected to increase targets again after 411kbd was decided in July for August.

- There are few other events today with only the July Dallas Fed manufacturing, which can impact oil price movements, and the ECB survey of monetary analysts released.

Gold Slightly Higher But Now Waiting For Week’s Key Events

Despite the announcement of an EU-US trade deal, gold is little changed in today’s APAC session. It seems to have priced in trade optimism on Friday when it fell almost a percent and is currently 0.1% higher at $3340.7/oz. With US-China talks and Wednesday’s Fed decision now in focus as well as significant US data over the week, bullion and other markets are range trading. The USD index and US yields are little changed.

- Equities are generally stronger with Euro stoxx futures +1.0% & S&P +0.4%. In Asia, the Hang Seng is up 0.4% but the Nikkei is down 1.0%. Oil prices are moderately higher with WTI +0.4% to $65.45/bbl. Copper is down 0.1%. Silver is up 0.2% to $38.23 after reaching $38.31 earlier.

- Markets are watching this week’s August 1 tariff deadline closely as negotiations with the US continue. In addition, there are the Fed’s decision on July 30, Q2 GDP & June PCE July 30 & 31, and US July payrolls August 1. A dovish Fed or weak US data would be supportive of gold prices.

- There are few events today with only the July Dallas Fed manufacturing and the ECB survey of monetary analysts released.

CHINA: Country Wrap: China Industrial Profits Decline in June (amended)

- US and Chinese officials are meeting Monday to extend their tariff detente beyond a mid-August deadline, and haggle over other ways to further defuse trade tensions. Chinese Vice Premier He Lifeng and US Treasury Secretary Scott Bessent will lead the delegations through Tuesday in Stockholm — their third meeting in less than three months. The agenda includes discussions about how long the current tariff truce can be extended, as well as US levies tied to fentanyl trafficking and Chinese purchases of sanctioned Russian and Iranian oil. (source BBG)

- Over the weekend, the release of China's Industrial Profits for the year provided limited positive news for the current state for China's corporates.

- Industrial profits year-on-year declined -4.3% in June, following the decline of -9.1% in May. The year-to-date number declined further to -1.8% YoY from -1.1% in May. Intensive competition between companies has exacerbated deflationary pressures at a time when exports to the US remain pressurized. The auto sector particularly is seeing increased competition as EV manufacturers vie for sales. State-owned automakers Guangzhou Automobile Group and JAC Group have posted losses driven by the intense pricing pressure in the auto sector. The data showed the gap widening between state owned enterprises and private companies. State-owned firms recorded a 7.6% decline in profits in the first half. Private-sector companies reported a rise of 1.7% while foreign firms logged a 2.5% increase. China's authorities have stated this month that efforts to regulate aggressive price-cutting will be forthcoming, fueling expectations that a fresh round of industrial capacity cuts might be approaching. (source MNI)

- In Hong Kong, markets are modestly higher, the HSI up around 0.4%, while the CSI 300 is down a touch in China. Over the weekend we saw profit results remain negative in y/y terms for June, albeit up from the May decline.

- Yuan Reference Rate at 7.1467 Per USD; Estimate 7.1686

- Bonds are firmer today with the CGB 10yr at +1.72%

SOUTH KOREA: Country Wrap: Tariff Deadline Draws Near

- A pivotal week has begun for Korea's economy as the Aug. 1 deadline for potential U.S. reciprocal tariffs draws near. The outcome of the stalled Korea-U.S. trade negotiations could shape the country's economic trajectory for years. With Washington ramping up the pressure and engaging in deals with the European Union and China, it remains uncertain whether Seoul can reach an agreement in time. The landscape is far from favorable. Under the threat of steep tariffs, other countries are conceding market access and pledging large-scale investments to secure deals with the United States. Japan, for example, agreed to open its rice market and pledged $550 billion in U.S.-bound investment, leading to a reduction in reciprocal tariffs from 25 to 15 percent. Bloomberg and other outlets report that the EU is also likely to accept a 15 percent tariff on most goods, including automobiles. (source Yonhap)

- One month after the introduction of tighter regulations on household loans, new applications for such loans have been more than halved, while the growth rate of outstanding loans at major banks has markedly slowed, data showed Sunday. During the first 18 business days of July, the average daily amount of household loan applications, including mortgage and credit loans, submitted to banks totaled 1.78 trillion won ($1.29 billion), marking a 56.5 percent drop from the same number of business days in June, according to the data by the financial authorities. (source Korea Times)

- South Korea's Kospi has been volatile, initially rallying at the open, aiding by a large Samsung chip order (for Tesla) but once again the index has struggled above 3200. Focus remains on US-South Korea trade negotiations ahead of the Aug 1 deadline at the end of the week, with officials set to meet later in the week (reportedly July 31).

- The Won is out of the gate early this week as the strongest regional performer, up +0.35% at 1,378.49.

- The KTB curve is lower, with some steepening as the short end outperforms. KTB 10yr 2.85%

INDONESIA: Country Wrap: New Loans Up in Q1

- Bank Indonesia reported on Friday that local currency transactions (LCT) surged to 11.7 billion U.S. dollars in the first half of 2025, more than double the 4.7 billion dollars in the same period last year. The number of LCT customers grew by 45 percent year-on-year during the first half of 2025, said the central bank. "Therefore, the National LCT Task Force will continue to encourage the use of local currencies in cross-border transactions to strengthen national economic resilience," said Bank Indonesia Deputy Governor on Friday. (source BBG)

- The latest Banking Survey conducted by Bank Indonesia indicates that new loan disbursements increased in the second quarter of 2025, despite moderating compared with the same period one year earlier. This was reflected by a Weighted Net Balance (WNB) of 85.22% in the second quarter of 2025, up from 55.07% in the first quarter of 2025 yet below the 89.11% recorded in the second quarter of 2024. Growth of new loan disbursements was driven by working capital loans and investment loans. Moving forward, respondents predict new loan disbursements to maintain growth in the third quarter of 2025, with the WNB predicted at 81.71%. (source BBG)

- The Jakarta Composite is having a stellar month up over 10% and is adding +1.3% in today's trade

- The Rupiah is the worst of the regional performers today down -0.14% to 16.344

- Bonds are softer for Monday with the 10yr up at 6.53%

MALAYSIA: Country Wrap: Government Package to Pressurize Fiscal Position

- Local semiconductor players continue to navigate a period of heightened uncertainty as a convergence of tariff and trade uncertainty, supply chain dynamics and foreign-exchange (forex) volatility continue to cloud the outlook for the sector. Fortress Capital Asset Management Sdn Bhd chief executive officer Thomas Yong said the industry is likely to experience a period of “muted and uneven recovery” in the next two to three quarters. In particular, factory utilization rates in segments tied to consumer electronics may remain muted, and earnings for the second quarter of 2025 (2Q25) is expected to be “relatively stagnant on a sequential basis”. (source The Star)

- The Malaysian government’s recent “Appreciation Package,” while aimed at providing immediate relief to citizens and bolstering domestic demand, is poised to introduce fresh fiscal pressures, according to an analysis by Kenanga Research. The package, unveiled by Prime Minister Datuk Seri Anwar Ibrahim on Wednesday, includes a universal RM100 cash aid and a significant reduction in RON95 petrol prices for eligible Malaysians. Kenanga Research views these measures not as a conventional fiscal stimulus but rather a “redistribution of recent macro gains,” such as a stronger Ringgit and stable inflation. While acknowledging their political popularity and positive impact on cost of living, the research house warns that they “heighten the tension between near-term social spending and medium-term fiscal discipline.” (source Business Today)

- The FTSE Malay KLCI is moderately higher today with gains of +0.30%

- The The Malaysian Ringgit finished last week with gains of 0.50% at 4.220. Ahead for the week is the S&P Global Malaysian PMI Manufacturing as the key data release for the SE Asian currency. The Ringgit has opened Monday to trade at 4.2218.

- Bonds remain quiet with the MGS 10yr at 3.42%

ASIA FX: KRW Recovers Some Ground, TWD Weaker, CNH Steady

In North East Asia FX, KRW has unwound some of Friday losses, USD/TWD has pushed higher, while USD/CNH is little changed. USD/HKD remains just under the top end of the peg band.

- USD/CNH drifted lower in the first part of trade, as the EUR strengthened on trade deal headlines with the US. However, there was no follow through to the move. We were last near 7.1690, little changed versus end Friday levels. The USD/CNY fixing moved higher, but the error term was close to unchanged versus the level from Friday. Industrial profits from the weekend (for June) fell again in y/y terms, albeit not as much as the May dip.

- Spot USD/KRW is down slightly, last near 1378.5, up around 0.30% in won terms versus end Friday levels. Focus remains on US-South Korea trade talks, with more talks scheduled for this week ahead of the Aug 1 deadline. Agriculture and ship building continue to feature in terms of some of the media snippets. The Kospi surged at the open on Samsung chip news (to supply chips to Tesla), but has still struggled to hold above the 3200, as has been the case in recent weeks.

- USD/TWD is around 29.45/50, last up 0.15%. This is fresh highs since earlier in July and may reflect seasonality ahead of month end.

- USD/HKD is little changed, last close to 7.8490.

ASIA FX: SEA FX Little Changed, Thailand-Cambodia Talks Expected

In South East Asia FX, the tone has been very steady to start the week. Thailand markets are out today, with focus on the on-going Thailand- Cambodia border dispute. Talks are meant to begin today to diffuse the situation, following weekend prompts from US President Trump. Still earlier headlines crossed that clashes between the two countries were still taking place. USD/THB finished last week at 32.38, while offshore equity inflow momentum slowed.

- USD/IDR is firmer, last just above 16330. This is close to recent highs for July. The better local equity backdrop is not helping IDR at this stage, with month approaching, USD demand may have picked up somewhat. A clean break higher could see the 16400 region targeted.

- USD/MYR is little changed, holding above 4.2200 at this stage, while USD/SGD is near 1.2805/10, with Wednesday's MAS decision in focus.

- USD/PHP is down a touch but still above 57.00 at this stage. Lows from last week in the pair were at 56.64.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 28/07/2025 | 1000/1100 | ** | CBI Distributive Trades | |

| 28/07/2025 | 1400/1000 | ** | housing vacancies | |

| 28/07/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 28/07/2025 | 1530/1130 | * | US Treasury Auction Result for 2 Year Note | |

| 28/07/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 28/07/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/07/2025 | 1700/1300 | * | US Treasury Auction Result for 13 Week Bill | |

| 28/07/2025 | - | FOMC Meeting | ||

| 29/07/2025 | 2301/0001 | * | BRC Monthly Shop Price Index | |

| 29/07/2025 | 0600/0800 | Flash Quarterly GDP Indicator | ||

| 29/07/2025 | 0700/0900 | *** | GDP (p) | |

| 29/07/2025 | 0800/1000 | ** | ECB Consumer Expectations Survey | |

| 29/07/2025 | 0830/0930 | ** | BOE Lending to Individuals | |

| 29/07/2025 | 0830/0930 | ** | BOE M4 | |

| 29/07/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 29/07/2025 | 1230/0830 | ** | Advance Trade, Advance Business Inventories | |

| 29/07/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 29/07/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 29/07/2025 | 1300/0900 | ** | FHFA Home Price Index |