ASIA STOCKS: Mixed Trends Despite Higher EU Futures On US-EU Trade Deal

Asia Pac stocks are mixed in the first part of Monday trade. This comes despite a better tone to both US and EU equity futures. US futures were last up 0.40-0.55%, with the tech side leading. EU futures were around +1% higher, as market took some comfort from the earlier headlines around a 15% tariff deal between the US and EU (for most EU exports to the US). Positive spillover has been limited to this region so far today.

- Japan markets are weaker, the Topix off around 0.50%, while the NKY 225 is down around 0.90%. Sell-side analysts have noted profit taking ahead of key earnings in the Chip sector as a potential headwind (via BBG), while political uncertainty also continues. PM Ishiba has vowed to stay on as PM, despite recently losing upper house elections (and after onshore media outlets indicated he would resign in August).

- In Hong Kong, markets are modestly higher, the HSI up around 0.4%, while the CSI 300 is down a touch in China. Over the weekend we saw profit results remain negative in y/y terms for June, albeit up from the May decline.

- South Korea's Kospi has been volatile, initially rallying at the open, aiding by a large Samsung chip order (for Tesla) but once again the index has struggled above 3200. Focus remains on US-South Korea trade negotiations ahead of the Aug 1 deadline at the end of the week, with officials set to meet later in the week (reportedly July 31).

- Thailand markets are out today, as the US attempts to lead efforts to de-escalate tensions on the Thailand/Cambodian border.

- Indonesia is up +1.25%, one of the better performers in SEA so far today. The initial tone in Indian markets is for modest downside, continuing the recent run of underperformance for these markets.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US FISCAL: Available "Extraordinary" Measures To Ward Off X-Date Pick Up

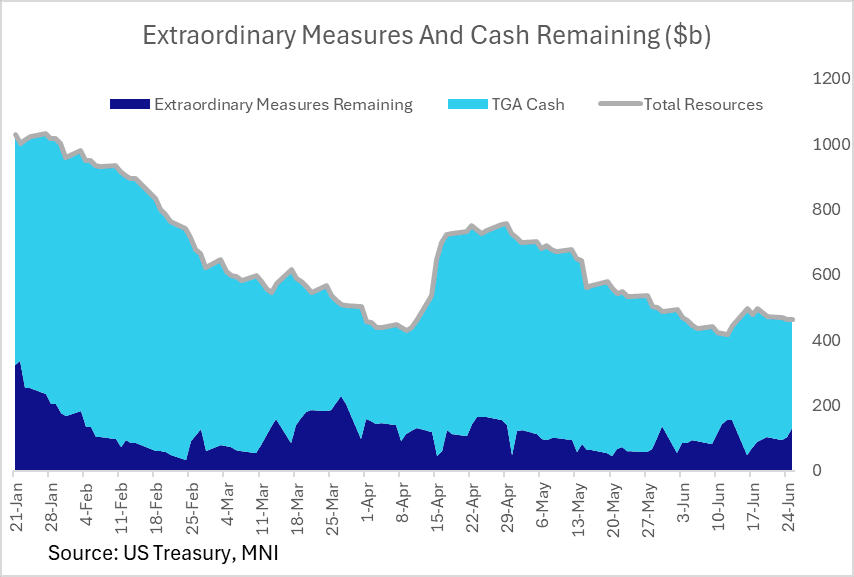

Treasury reported Friday that as of Jun 25 it had $130B in remaining "extraordinary" measures (of a total $378B available) to ward off an "x-date" of running out of resources before defaulting. That's the highest in 2 weeks.

- Combined with $334B cash as of Jun 25 (after a bit of a buildup after the mid-June tax deadline), that's a total of roughly $465B in total resources available.

- We noted earlier this week that Treasury told Congress that it was required to extend its debt issuance suspension period from Jun 27 to Jul 24, in effect prolonging the use of extraordinary measures while we await a resolution to the debt limit impasse, probably through the fiscal legislation currently going through Congress.

- Realistically, fiscal dynamics so far this year point to potential for Treasury to get into September without running out of cash + extraordinary measures. That seems to be the broad market expectation.

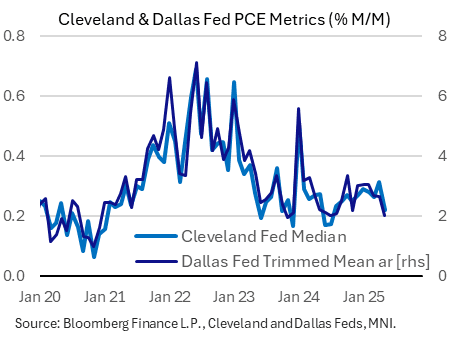

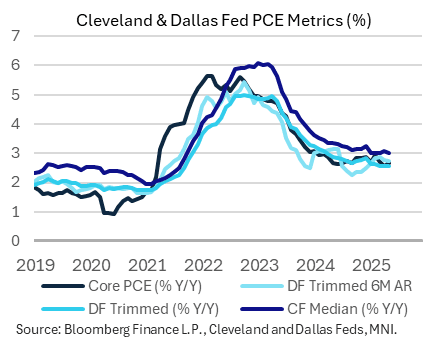

US DATA: Cleveland, Dallas Fed PCE Medians Show Progress But Still Above-Target

The Cleveland and Dallas Fed's median PCE metrics showed a notable drop in May. All indices suggest PCE inflation running above 2%, and higher than the actual core and headline PCE measures, but pressures appear to have cooled from a pickup in the early months of the year.

- The Cleveland Fed's median PCE measure came in at 0.22% M/M, a 10-month low after April's 15-month high 0.31%. This left median PCE at 3.01% on a Y/Y basis, down from 3.06% prior for a the joint-lowest (with Feb) since September 2021.

- The Dallas Fed's annualized median rate fell to 2.01%, from 2.65% prior for a 10-month low. The 6-month annualized rate edged lower to 2.74% (2.76% prior), a 4-month low, with the Y/Y rate ticking down to 2.55% from 2.56%, echoing the Cleveland Fed for the lowest reading since September 2021.

USDCAD TECHS: Pivot Resistance Remains Intact

- RES 4: 1.4111 High Apr 4

- RES 3: 1.4016 High May 12 and 13 and a key resistance

- RES 2: 1.3920 High May 21

- RES 1: 1.2710/3803 20- and 50-day EMA values

- PRICE: 1.3658 @ 16:23 BST Jun 27

- SUP 1: 1.3618 Low Jun 26

- SUP 2: 1.3540 Low Jun 16 and the bear trigger

- SUP 3: 1.3503 1.618 proj of the Feb 3 - 14 - Mar 4 price swing

- SUP 4: 1.3473 Low Oct 2 2024

USDCAD has pulled back from its recent highs. The primary downtrend remains intact and short-term gains appear to have been corrective. Key support and the bear trigger has been defined at 1.3540, the Jun 16 low. Clearance of this price point would resume the downtrend. Any reversal higher would instead signal scope for a stronger retracement. Pivot resistance to monitor is at the 50-day EMA, at 1.3803.