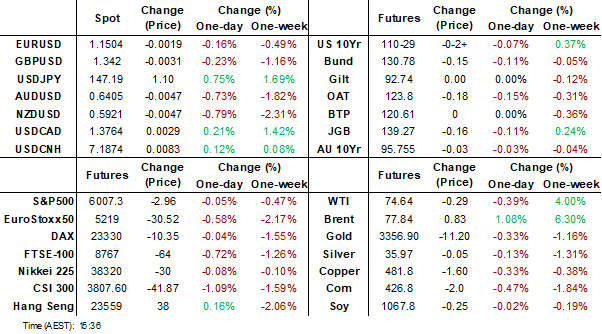

MNI EUROPEAN MARKETS ANALYSIS: Risk Sentiment Weak

- Risk sentiment was weak with most major bourses down today.

- Regional currencies were under pressure also as the USD strengthened on uncertainty.

- Australian PMIs came in better than expected for the June preliminary release.

- President Trump hails the US attack as a 'success'.

MARKETS

US TSYS: Asia Wrap - Yields Edge Higher Led by the Long-End

The TYU5 range has been 110-25+ to 111.04 during the Asia-Pacific session. It last changed hands at 110-27+, down 0-04 from the previous close.

- The US 2-year yield has edged higher trading around 3.916%, up 0.01 from its close.

- The US 10-year yield has bounced higher trading around 4.392%, up 0.02 from its close.

- (Bloomberg) -- “Treasuries may benefit from demand for haven assets and concerns over an economic slowdown unless oil prices rise dramatically, according to Nomura Securities Co.”

- Lance Roberts on X: “While the Fed is quietly sitting on the hands as economic data slows and tariff inflation remains non-existent, other central banks are rapidly cutting rates with the Swiss restarting NIRP. The Fed is likely going to be too late once again adjusting monetary policy which is its history.”

- The 10-year yield continues to find decent supply back towards its 4.30/35% support, this area needs to hold if yields are to move higher. The range looks to be 4.30% - 4.60% for now a break either side would provide a clearer direction.

- Data/Events: S&P Global US PMI’s, Existing Home Sales

JGBS: Modestly Cheaper But Off Worst levels

JGB futures are cheaper, -17 compared to the settlement levels, but well above session lows.

- No. of condominium units supplied in Tokyo and surrounding areas fell 16.9% from a year earlier to units in May.

- “Japan's manufacturing activity expanded in June, crossing the 50 threshold, likely due to front-loading of output ahead of a scheduled increase in US tariffs next month.” (BBG)

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session as the markets digest the possible implications of a longer and more sustained US involvement in the Middle East conflict and how Iran might react to this, potentially blocking the Strait of Hormuz.

- Cash JGBs are flat to 2bps cheaper across benchmarks today, with the 20-year outperforming ahead of tomorrow’s supply. The benchmark 20-year yield is -0.4bps lower at 2.345%

- "Although 20-year bond issuance will be reduced by 1.8 trillion, the decline in yields from the peak in May suggests that it's already priced in. Meanwhile, Tokyo inflation is set to land on Friday after a hot Japan print last week." (per BBG)

- The swaps curve has bear-steepened, with rates 1-4bps higher. Swap spreads are mostly wider.

- Tomorrow, the local calendar will see Dept Sales data alongside 20-year supply.

AUSSIE BONDS: Cheaper With US Tsys, CPI On Wed

ACGBs (YM flat, XM -3.5) are weaker, reversing modest gains seen early in today’s session following US airstrikes on Iranian nuclear sites over the weekend.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session.

- “As international investors pivot out of the U.S., another part of the world — and its bond market in particular — is gaining attention, according to Bank of America. The analysts pointed to Australia's bond market as a potential beneficiary of the dollar losing its safe-haven status.” (CNBC via BBG)

- Cash ACGBs are flat to 3bps cheaper with the AU-US 10-year yield differential -18bps.

- The bills strip has cheapened slightly, with pricing flat to -3.

- RBA-dated OIS pricing is modestly softer across meetings today. A 25bp rate cut in July is given an 84% probability, with a cumulative 74bps of easing priced by year-end.

- Tomorrow, the local calendar will be empty ahead of May CPI data on Wednesday. Consensus expects it to ease to 2.3% y/y from 2.4%. Trimmed mean ticked up to 2.8% y/y in April and has been around 2.7-2.8% since December, suggesting a stalling in disinflation. The next RBA meeting is July 7-8.

- The AOFM plans to sell A$1000mn of the 3.50% 21 December 2034 bond on Wednesday.

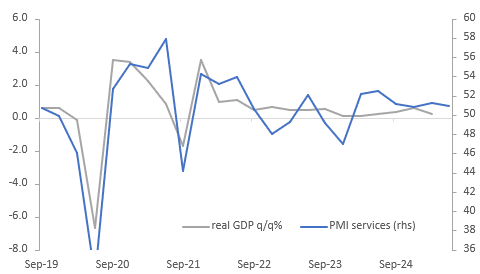

AUSTRALIA: May CPI Prints On Wednesday

In a data light week, the focus will be on Wednesday’s CPI for May which consensus expects to ease to 2.3% from 2.4%. Trimmed mean ticked up to 2.8% in April and has been around 2.7-2.8% since December suggesting a stalling in disinflation. The next RBA meeting is July 7-8.

- The S&P Global preliminary June PMIs are released today. They are holding just above the breakeven 50-mark signalling moderate growth in activity.

- Q2 job vacancies are out on Thursday. They fell 4.5% q/q in Q1 and monthly measures have been trending lower.

AUSTRALIA DATA: Pickup In June Activity But Manufacturing Environment Difficult

The preliminary June S&P Global PMIs showed that services activity in Australia ended Q2 on a more positive note with the index up to 51.3 from 50.6. Manufacturing was stable at 51.0 as the global market becomes more challenging, which left the composite up to 51.2 from 50.5, the highest since March. The Q2 average composite PMI was 50.9 down slightly from Q1’s 51.1, signalling that growth was little changed and remained positive but lacklustre.

Australia GDP q/q% vs PMI services quarter average

- Activity is being supported by domestic demand with an increase in new business but export orders shrank at their sharpest in almost a year often due to US protectionism. Services orders rose at a faster pace but were almost steady for manufacturers, S&P Global reported.

- Businesses seem fairly positive regarding the outlook with hiring continuing, although it slowed, and confidence improving. Sentiment was its highest since January but the optimism was not broad based with manufacturers more pessimistic but they still increased staffing.

- The moderation in cost and selling price inflation was good news for monetary policy, with the latter its lowest since November 2020. Input inflation only moderated for services, while manufacturers saw an increase in shipping and raw material costs, according to S&P Global, which have been impacted by global developments. With oil prices up around 25% in June and petrol prices up over 8c/L, costs are likely to rise in coming months depending on the outcome of the conflict in the Middle East.

- The difficult environment facing manufacturers could also been seen in the drop in their purchasing and running down of inventories.

BONDS: NZGBS: Unhanged, Digest Greater US Involvement In Middle East Conflict

NZGBs closed little changed, reversing early modest gains following US airstrikes on Iranian nuclear sites over the weekend.

- Cash US tsys are 1-2bps cheaper in today's Asia-Pac session as the markets digest the possible implications of a longer and more sustained US involvement in the Middle East conflict and how Iran might react to this, potentially blocking the Strait of Hormuz. Today's US calendar: S&P Global US PMI's, Existing Home Sales.

- (Bloomberg) - "New Zealand's dollar is particularly vulnerable in the event of a haven rally in the US currency should the conflict between Iran and Israel pose constraints on oil supply, according to Bank of America Corp."

- Swap rates closed flat to 1bp lower.

- RBNZ dated OIS pricing closed flat to 4bps softer across meetings. 4bps of easing is priced for July, with a cumulative 28bps by November 2025.

- Tomorrow, the local calendar will be empty, ahead of trade balance data for May on Wednesday.

- On Thursday, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.50% May-35 bond and NZ$50mn of the 1.75% May-41 bond.

FOREX: Asia FX Wrap - Reasons For A USD Correction Mount

The BBDXY has had a range of 1211.64 - 1215.21 in the Asia-Pac session, it is currently trading around 1214.80. The BBDXY has opened higher this morning, breaking through the 1213.00 area in reaction to the US bombing and the implications of potential extended US involvement in the conflict. The Market is caught short USD’s and the reasons for a retracement are beginning to mount. Brian Sullivan on X: ”It's not just the price of oil that's a concern, but also the cost of SHIPPING oil. Oil Brokerage Ltd. tells me that VLCC (very large crude carrier) ship rates near Persian Gulf could hit $100/k per day if disruption in Straight of Hormuz. For comparison, it was $24k/day just 10 days ago.”

- EUR/USD - Asian range 1.1456 - 1.1508, Asia is currently trading 1.1495. EUR has rejected the move above 1.1600 but dips should continue to find demand, first support back towards the 1.1400 area then 1.1100/1200. Price action does suggest we could test the support, the EUR has outperformed against both the AUD and NZD in Asia.

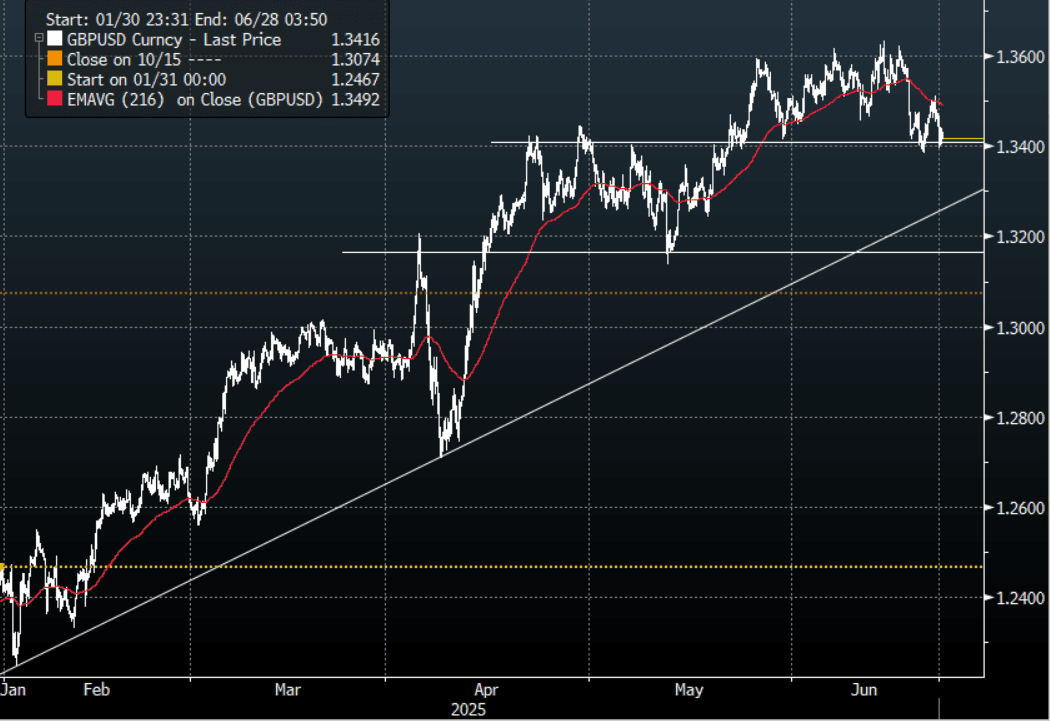

- GBP/USD - Asian range 1.3400 - 1.3442, Asia is currently dealing around 1.3415. The GBP continues to hold just above its support around 1.3400 after failing to break the Weekly 1.35/36 pivot. A sustained move back below 1.3400 and we could see a deeper correction unfold.

- USD/CNH - Asian range 7.1799 - 7.1921, the USD/CNY fix printed 7.1710. Asia is currently dealing around 7.1875. Sellers should be around on bounces while price holds below the 7.2500 area and the PBOC manages the fix lower.

- Cross asset : SPX -0.25%, Gold $3360, US 10-Year 4.39%, BBDXY 1215, Crude oil $75.25

- Data/Events : Ger HCOB PMI's, FRA HCOB PMI's, EZ HCOB PMI's

Fig 1: GBP/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

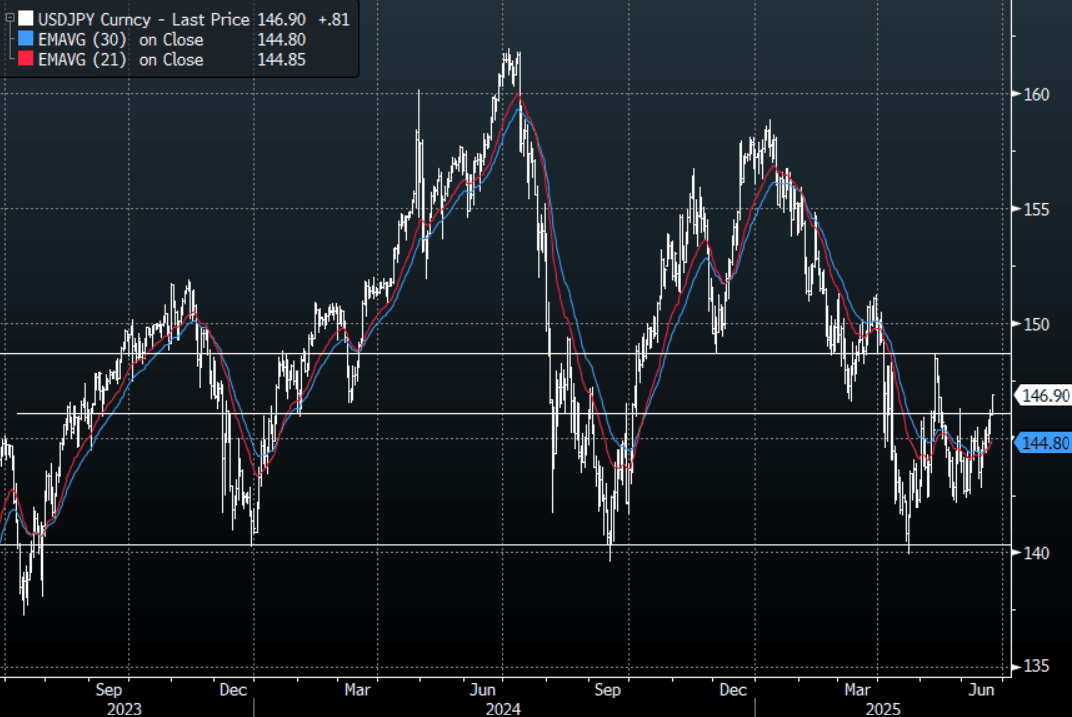

JPY: Asia Wrap - USD/JPY Eyes Oil And Is Challenging A Market Long JPY

The Asia-Pac USD/JPY range has been 146.15 - 146.91, Asia is currently trading around 146.90, +0.55%. USD/JPY has broken through the 146.50 area this morning in reaction to the US bombing and the implications of potential extended US involvement in the conflict. The Market is caught long JPY and the implications of even higher oil prices as Iran contemplates blocking the Strait of Hormuz is challenging their conviction.

- “Pimco has been buying long-term JGBs to take advantage of a “dislocation” in the market, Andrew Balls told the FT, adding there’s a strong case for authorities to “issue more in the parts of the curve where the demand is.”(BBG)

- "HAYASHI: NOT TRUE US DEMANDED 3.5% GDP ON DEFENSE SPENDING" - BBG

- USD/JPY price action continues to point to a market that is positioned long JPY.

- "Asian currencies are likely to see further downside in the near-term, amid rising vulnerability to oil prices"(BBG).

- USD/JPY price action continues to point to a market that is positioned long JPY.

- Having broken above 146.50 this morning the market will be closely watching the oil price for short-term clues.

- The market is positioned for a move lower in USD/JPY and with this positioning at extremes we have seen the risk of pullbacks increase. A sustained break above 146.50/147.00 would begin to challenge the conviction of these shorts and focus will return to the 150.00/151.00 area.

- Options : Close significant option expiries for NY cut, based on DTCC data: 145.50($323m).Upcoming Close Strikes : 144.50($1.34b June 25)

- CFTC data shows Asset managers maintained their already extensive JPY longs, while leveraged funds have pared back their own longs that had just begun to be rebuilt.

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

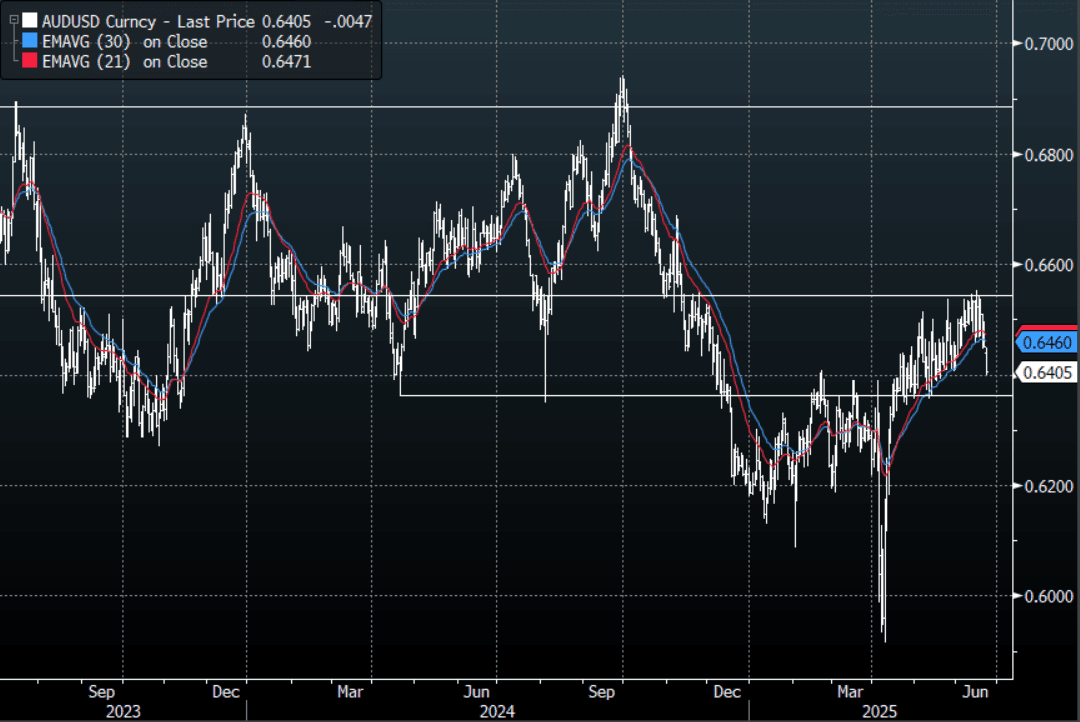

AUD: Asia Wrap - Breaks Below 0.6450, Looking Towards 0.6350 Support

The AUD/USD has had a range of 0.6398 - 0.6449 in the Asia- Pac session, it is currently trading around 0.6405. The AUD has remained under pressure after gapping lower on the Asian open, -0.70%. The market is digesting the implications of a longer and more sustained US involvement in the conflict and how Iran might react to this, potentially blocking the Strait of Hormuz.

- AUSTRALIA DATA: Pickup In June Activity But Manufacturing Environment Difficult. The preliminary June S&P Global PMIs showed that services activity in Australia ended Q2 on a more positive note with the index up to 51.3 from 50.6. Manufacturing was stable at 51.0 as the global market becomes more challenging, which left the composite up to 51.2 from 50.5, the highest since March. The Q2 average composite PMI was 50.9 down slightly from Q1’s 51.1, signalling that growth was little changed and remained positive but lacklustre.

- "FITCH RATINGS: AUSTRALIAN MORTGAGE ARREARS SHOW SHARPER THAN EXPECTED RISE, AUSTRALIA MORTGAGE ARREARS RISE IN 1Q.”(BBG)

- The AUD/USD looks likely to have a look back towards its 0.6350/0.6400 support.

- Price remains in the wider 0.6350 - 0.6550 range for now. After failing to break higher, the focus will now turn to whether the support can hold, a close back below 0.6350 is needed to challenge the newly formed uptrend.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6510(AUD397m). Upcoming Close Strikes : 0.6500(AUD1.21b June 26), 0.6450(AUD553m June 26).

- CFTC Data shows Asset managers maintaining their shorts, the Leveraged community though have again added to their shorts.

- AUD/JPY - Today's range 93.85 - 94.38, it is trading currently around 94.00. Choppy price action as the pair establishes a range between 92.00 - 96.00. A break back below 91.50/92.00 is needed to see the move lower regain momentum and the focus turn back to the year's lows again. The move higher in oil and a market already very long JPY is preventing this pair moving lower in reaction to a souring risk backdrop for now.

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

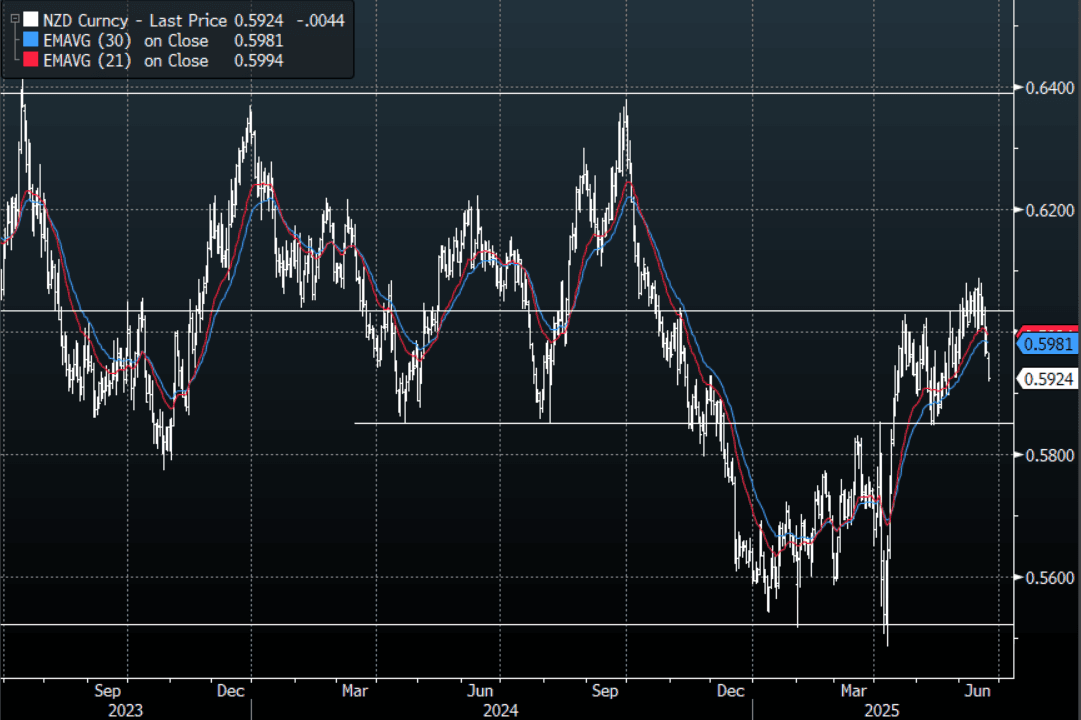

NZD: Asia Wrap - NZD/USD Fails Above 0.6000 As The USD Bounce Builds Momentum

The NZD/USD had a range of 0.5918 - 0.5966 in the Asia-Pac session, going into the London open trading around 0.5925,-0.70%. The NZD has remained under pressure after gapping lower on the Asian open. The market is digesting the implications of a longer and more sustained US involvement in the conflict and how Iran might react to this, potentially blocking the Strait of Hormuz.

- (Bloomberg) - “New Zealand’s dollar is particularly vulnerable in the event of a haven rally in the US currency should the conflict between Iran and Israel pose constraints on oil supply, according to Bank of America Corp.”

- “Among Group-of-10 commodity currencies, the Kiwi “is the only energy importer and most vulnerable if Middle East oil supply is impacted more severely,” wrote Bank of America.”

- The NZD could not get back above 0.6000 on Friday and this morning has seen another wave of selling as the market digests the weekend's news and the implications of what further US involvement might imply.

- Technically while the support around 0.5850 holds in NZD/USD it is still in an uptrend but should risk start to come under more significant pressure the market is likely to test this.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.5830(NZD300m June 23). Upcoming Close Strikes : 0.5690(NZD621m June 25)

- CFTC Data showed Asset managers paring back their shorts slightly once more over the week, the leverage community did likewise.

- AUD/NZD range for the session has been 1.0797 - 1.0828, currently trading 1.0810. The cross is struggling to get any momentum back above 1.0800 for now, it needs to hold above here and start extending higher to put a higher low in place. The longer it fails to extend higher the more likely it begins to drift lower again, a break sub 1.0750 will see downward momentum return.

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Major Bourses Down on Rising Tensions

Many of the major regional bourses all fell today as the escalating situation in the Iran weighed heavy on investor appetite. Regional currencies fell against the USD and even bond markets were down as oil prices jumped and uncertainty grew.

- China has had a mixed day with the Hang Seng starting the week lower by -0.13% and the CSI 300 following suit, down -0.20%. Shanghai Comp bucked the trend and is up modestly be +0.15% and Shenzhen is up +0.21%.

- The TAIEX in Taiwan fell heavily today by -1.38% wiping out last week's gains.

- After a very strong week last week, the KOSPI couldn't avoid the regional weakness and is down -0.50%

- The FTSE Malay KLCI was one of the few outliers, clinging onto gains of +0.44%.

- The Jakarta Composite was under pressure falling -1.85%

- The FTE Straits Times in Singapore is down -0.41% whilst the PSEi in the Philippines is down -2.06% for its biggest fall since early April

- The NIFTY 50 is down -0.97% having closed Friday strongly with gains of +1.29%

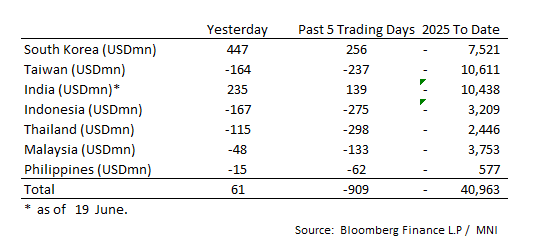

ASIA STOCKS: Strong Inflows for KOREA and INDIA

A subdued end to the week with an overall outflow from major markets

- South Korea: Recorded inflows of +$447m on Friday, bringing the 5-day total to +$256m. 2025 to date flows are -$7,521. The 5-day average is +$51m, the 20-day average is +$191m and the 100-day average of -$78m.

- Taiwan: Had outflows of -$164m as of Friday, with total outflows of -$237 m over the past 5 days. YTD flows are negative at -$10,661. The 5-day average is -$47m, the 20-day average of -$13m and the 100-day average of -$71m.

- India: Had inflows of +$235m as of the 19th, with total inflows of +$139m over the prior 5 days. YTD flows are negative -$10,438m. The 5-day average is +$28m, the 20-day average of +$10m and the 100-day average of -$59m.

- Indonesia: Had outflows of -$167m on Friday, with total outflows of -$275m over the prior five days. YTD flows are negative -$3,209m. The 5-day average is -$55m, the 20-day average -$14m and the 100-day average -$31m.

- Thailand: Recorded outflows of -$115m as of Friday, with outflows totaling -$298m over the past 5 days. YTD flows are negative at -$2,446m. The 5-day average is -$60m, the 20-day average of -$37m and the 100-day average of -$22m.

- Malaysia: Recorded outflows of -$48m as of Friday, totaling -$133m over the past 5 days. YTD flows are negative at -$3,753m. The 5-day average is -$26m, the 20-day average of -$30m and the 100-day average of -$23m.

- Philippines: Recorded outflows of -$15m yesterday, with net outflows of -$62m over the past 5 days. YTD flows are negative at -$577m. The 5-day average is -$12m, the 20-day average of -$16m the 100-day average of -$5m.

OIL: Crude Trends Lower After Initial Spike, Already Contains Risk Premium

Oil prices spiked at the start of today’s trading after the US struck Iranian nuclear facilities. The market is nervous about how Iran will respond and is concerned by a further escalation in the conflict that could significantly impact oil infrastructure in the region. Since the initial reaction though, crude has trended lower as prices already contain a risk premium. WTI is at $74.70/bbl following a peak of $78.40 to be up 1.2% today and Brent is 1.4% higher at $78.07/bbl after rising to $81.40. The USD index is up 0.3%.

- Iranian TV reported that parliament voted to close the Strait of Hormuz but Bloomberg notes that would ultimately require Ayatollah Khamenei’s approval. Even a brief disruption could drive oil prices sharply higher.

- The Greek government warned its shipping to reassess the need to travel through Hormuz and suggested vessels wait for clarification, according to Bloomberg. The EU and Joint Maritime Information Center have increased the risk level of an attack in the region.

- Around 30% of seaborne crude travels through the Strait and shipping rates have risen and some firms are not taking new bookings. Two tankers had to reverse course and head south again as they entered Hormuz as the US attacked Iran.

- Goldman Sachs believes that if seaborne traffic through Hormuz were cut in half then Brent could reach $110/bbl, reported by Bloomberg.

- Later the Fed’s Waller, Bowman, Goolsbee, Williams and Kugler as well ECB President Lagarde speak. US and European preliminary S&P Global/HCOB June PMIs are released.

GOLD: Prospect Of On Hold Policy Sees Gold Fall Despite Geopolitical Risks

Gold prices jumped to $3395.07 at the start of today’s APAC trading, the highest since mid-June, on flight-to-quality following US action in Iran. However, the prospect that the conflict will lead to higher inflation through energy prices thus delaying central bank easing is weighing on non-interest bearing gold with it now down 0.3% to $3357.9 after a low of $3352.1. The stronger US dollar (USD BBDXY +0.3%) and slightly higher US yields are also pressuring bullion.

- Gold continues to trade between initial support at $3338.8 and resistance at $3451.3.

- With positions in gold so long (well above 2016 and 2020 levels), silver and palladium have become safe-have substitutes. Silver is up 0.1% to $36.05 today following a high of $36.20 and a low of $35.84, holding above initial support at $35.43. A bull wave persists with initial resistance at $37.32, 18 June high.

- Middle Eastern developments have driven a pullback in risk with the S&P e-mini down 0.3%, KOSPI -0.5% and Hang Seng -0.1%. Oil prices are higher with WTI +1.7% to $75.09/bbl. Copper is down 0.3%.

- Later the Fed’s Waller, Bowman, Goolsbee, Williams and Kugler as well ECB President Lagarde speak. US and European preliminary S&P Global/HCOB June PMIs are released.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 23/06/2025 | 0700/0300 | Fed Governor Christopher Waller | ||

| 23/06/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 23/06/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 23/06/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 23/06/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 23/06/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 23/06/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 23/06/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 23/06/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 23/06/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 23/06/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 23/06/2025 | - | BOE Bailey At Insurance Chairs Dinner | ||

| 23/06/2025 | 1300/1500 | ECB Lagarde At ECON Hearing | ||

| 23/06/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 23/06/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 23/06/2025 | 1400/1000 | *** | NAR existing home sales | |

| 23/06/2025 | 1400/1000 | Fed Vice Chair Michelle Bowman | ||

| 23/06/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 23/06/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 23/06/2025 | 1720/1320 | Chicago Fed's Austan Goolsbee | ||

| 23/06/2025 | 1830/1430 | Fed Governor Adriana Kugler | ||

| 24/06/2025 | 0800/1000 | *** | IFO Business Climate Index | |

| 24/06/2025 | 0800/0900 | BOE Bailey At Gold Standard Conference | ||

| 24/06/2025 | 0845/1045 | 2025 Budget Press Conference | ||

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0900/1000 | * | Index Linked Gilt Outright Auction Result | |

| 24/06/2025 | 0930/1030 | BOE Green On CB Balance Sheet Mgmt | ||

| 24/06/2025 | 1000/1100 | ** | CBI Industrial Trends | |

| 24/06/2025 | 1115/1315 | ECB de Guindos At XLII APIE seminar | ||

| 24/06/2025 | 1230/0830 | *** | CPI | |

| 24/06/2025 | 1230/0830 | * | Current Account Balance | |

| 24/06/2025 | 1230/0830 | ** | Philadelphia Fed Nonmanufacturing Index | |

| 24/06/2025 | 1255/0855 | ** | Redbook Retail Sales Index | |

| 24/06/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/06/2025 | 1300/0900 | ** | S&P Case-Shiller Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/0900 | ** | FHFA Home Price Index | |

| 24/06/2025 | 1300/1500 | ECB Lagarde Accepts De Sanctis Award "Europa" | ||

| 24/06/2025 | 1315/0915 | Cleveland Fed's Beth Hammack | ||

| 24/06/2025 | 1335/1435 | BOE Ramsden At Barclays-CEPR MonPol Forum | ||

| 24/06/2025 | 1355/1555 | ECB Lane Keynote At Barclays-CEPR MonPol Forum |