MNI EUROPEAN MARKETS ANALYSIS: NZD/USD Rebound Extends

- Risk appetite firmed again in Asia today as the Beige Book release overnight did little to alter the path for rate cuts. China's equity markets brushed off a potential new default threat from China Vanke as it sought to delay the repayment of a bond.

- The BOJ member considered 'Dovish" took a more neutral stance in a speech Thursday emphasizing the importance of timing around rate hikes.

- Australian economic data challenged the doves with business investment posting its biggest increase since early 2021. New Zealand central bank governor Christian Hawkesby said there is now a high hurdle for further interest-rate cuts, reinforcing the signal that the easing cycle has likely come to an end. These shifts aided NZD and AUD FX gains.

- Later December German GfK consumer confidence, October euro area M3 and November European Commission economic sentiment print. The BoE’s Greene, ECB’s Cipollone, Tuominen, Machado and de Guindos speak and the October ECB meeting minutes are published.

MARKETS

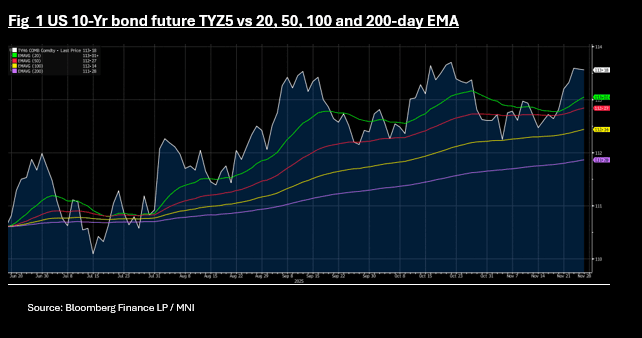

US TSYS: Bond Futures Modestly Down Ahead of Thanksgiving

- With cash markets closed in the Asia trading day, bond futures were the only avenue for risk today.

- The US 10-Yr is down -01 today at 113-18 on low volumes.

- TYZ5 has rallied since November 19 and is now above all major moving averages and at +62 on the 14-day Relative Strength Index; just below 70 that indicates Overbought.

JGBS: Bull-Flattener After Headlines 10-40Y Issuance To Be Unchanged

JGB futures are stronger, +14 compared to settlement levels, after a relatively subdued trading, with cash US tsys out for the Thanksgiving Day Holiday.

- BoJ Board Member Noguchi's speech discussed the need to get rate hike timing right, as hiking too early or too late can cause problems. He stated that hiking too early risks derailing the wage/price cycle and sustainably hitting the 2% inflation target, while raising rates too slowly will risk destabilizing price and activity trends (presumably as policy rates have to rise rapidly to bring down inflation).

- Cash JGBs are flat to 2bps richer across benchmarks, with a flattening bias. The benchmark 10-year yield is 1.0bp lower at 1.799% versus the cycle high of 1.845%.

- Earlier, Reuters reported that the Japanese government will increase issuance of 2-year and 5-year JGBs from January as part of its stimulus-funding plan. Reuters also noted that there are no changes to the planned issuance for 10-40-year tenors.

- The cheapening of the 5-year, in terms of the 2/5/10 butterfly, since early Q2 this year is consistent with today's issuance headlines (see chart).

- Swap rates are little changed.

- Tomorrow, the local calendar will see Tokyo CPI, Retail Sales, IP, Housing Starts, Weekly International Investment Flow and Labour Market data alongside 2-year supply.

Source: Bloomberg Finance LP

AUSSIE BONDS: Richer But Cheaper Than Pre-CPI, 25% Hike Priced For End-2026

ACGBs (YM +3.0 & XM +3.0) are stronger but sit mid-range after a relatively subdued trading, with cash US tsys out for the Thanksgiving Day Holiday.

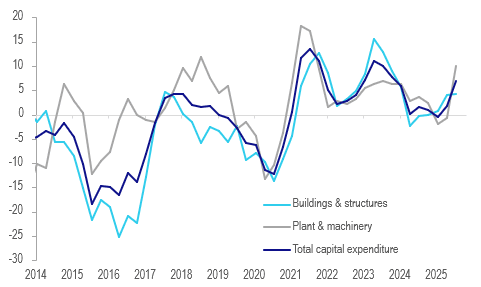

- Q3 private capex volumes soared 6.4% q/q, the fastest since Q1 2012, and are setting up the 3 December GDP release for a solid increase at this stage. Inventory data is out 1 December and the net export and public demand contributions on 2 December.

- The jump in investment in the quarter was across both building and plant & machinery and was driven by an 11.5% q/q jump in the latter from spending on aircraft but also data centres.

- Cash ACGBs are 3bps richer with the AU-US 10-year yield differential at +51bps (albeit with cash US tsys 10-year at yesterday’s closing level).

- The bills strip is flatter, with pricing flat to +3.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 0% probability, with a cumulative 2bps of easing priced by mid-2026. Notably, the market has now shifted to giving a 25% probability to a 25bps by December 2026.

- Tomorrow, the local calendar will see Private Sector Credit data.

- The AOFM plans to sell A$900mn of the 3.75% 21 April 2037 bond on Friday.

Bloomberg Finance LP

AUSTRALIA DATA: Very Strong Private Capex To Support Q3 GDP Print

Q3 private capex volumes soared 6.4% q/q, the fastest since Q1 2012, and is setting up the 3 December GDP release for a solid increase at this stage. Inventory data is out 1 December and the net export and public demand contributions on 2 December. The jump in investment in the quarter was across both building and plant & machinery and was driven by a 11.5% q/q jump in the latter from spending on aircraft but also data centres. Annual growth rates are showing an investment recovery is currently taking place.

Australia real capital expenditure y/y%

- The increase in plant & machinery expenditure was the highest in almost 21 years. Similar growth rates have contributed around 0.3pp to GDP that quarter.

- Non-mining plant & machinery expenditure rose 13% q/q and mining +4.5% q/q. Investment in data centres was seen in the 40.7% q/q increase in information media & telecoms investment. The risk now is that there is payback for such a large jump in the subsequent quarters.

- Private investment in buildings rose 2.1% q/q, the fastest since Q2 2023, to be up 4.3% y/y. This could contribute around another 0.2pp. Non-mining was up 3.6% q/q while mining fell 0.4% q/q.

- Total Q3 capex was concentrated in non-mining (+8.6% q/q) with mining lagging (+0.9% q/q).

- Estimated capex for 2025-26 was revised 9.4% higher.

BONDS: NZGBS: Post-RBNZ Sell-Off Extends Today, Full Hike Priced For Late-26

NZGBs closed showing a bear-flattener, with yields 2-8bps higher. As it stands, yields are 8-14bps higher than pre-RBNZ levels, with the 2/10 curve flatter.

- In a relative sense, NZGBs have also underperformed, with the NZ-US 10-year yield differential 3bps wider at +23bps, and the NZ-AU 10-year differential 1bp higher at -27bps.

- The recent cheapening in NZGBs, however, didn’t deter buyers at today’s weekly auction, with cover ratios ranging from 3.86x (May-30) to 5.46x (May-34).

- Swap rates closed 4-9bps higher, with the 2s10s curve flatter. The curve is around 10bps flatter than yesterday’s pre-RBNZ levels.

- RBNZ-dated OIS pricing closed flat to 9bps firmer across meetings today, led by the late-2026 contracts, extending yesterday’s post-policy decision firming. Indeed, relative to pre-RBNZ levels, pricing is 8-20bps higher across meetings, again led by late-2026 contracts.

- Notably, as well, November 2026 now assigns a 25bps hike with a 37% probability (see chart). The push into positive territory for 12-month forward expectations for the RBNZ in mid-November was the first time since October 2023.

- Tomorrow, the local calendar will see ANZ Consumer Confidence and Filled Jobs data.

Bloomberg Finance LP

NEW ZEALAND: Business Survey Signals Stronger H2 Growth & Lower Q4 Inflation

The ANZ November business survey is consistent with RBNZ’s Hawkesby’s comment following Wednesday’s rate cut that the recovery “is happening right now through Q3 and Q4”. It is a piece of high frequency data consistent with rates staying at 2.25% for now. Businesses are their most positive since 2014. Activity compared to a year ago, a good indicator for GDP, rose to 21.3 from 4.6 with ANZ saying that only construction remains negative. Thus it appears that growth recovered further in Q4.

- ANZ notes that while the economy is coming off a low base, “something has clearly changed”.

- Q4 averages suggest that GDP growth should recover and inflation turn lower again.

- Business confidence rose to 67.1 in November from 58.1, the highest since March 2014.

- The activity outlook picked up to 53.1 from 44.6, also the highest since Q1 2014. Export and employment intentions both rose in November but investment fell almost 2 points.

- Hiring compared to a year ago rose to -2.4 from -10.0 driven by services up 6 points to +7. Another sign the labour market has turned.

NZ ANZ business activity outlook vs employment intentions

- Hawkesby was asked at yesterday’s press conference about sluggish investment and he said that businesses need to be confident in the durability of the recovery and not just see lower lending rates before investing. The improvement in business confidence and profit expectations should help drive a pickup in capex but likely with a lag. When they do invest, credit conditions won’t be a constraint with “ease of credit” at its highest since 2009.

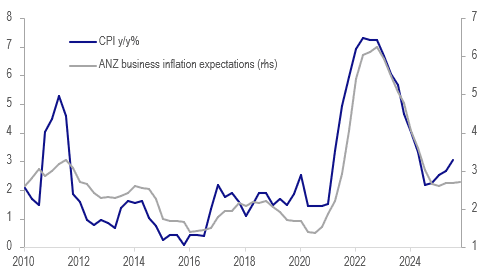

- Inflation expectations remained steady around 2.7% but pricing intentions rose to 50.5 from 43.9 with the increase 3-mths out rising 0.3pp to 1.9%. Cost expectations were lower though and wage expectations steady.

NZ inflation outlook %

Source: MNI - Market News/LSEG

RBNZ: MNI RBNZ Review-Nov 2025: On Hold If Progress As Expected

- Download Full Report Here

- The MPC voted 5-1 to cut rates 25bp to 2.25%, as was widely expected. The discussion was between a hold or 25bp of easing with no consideration for another 50bp cut. The dissenter voted to hold policy.

- The updated OCR projections showed Q1 at 2.25% and there is only one meeting in the quarter (18 February). Then Q2 is 2.20% and Q3 2.23%, suggesting that if the economy develops as expected then the RBNZ is now on hold.

- The profile helps the MPC to keep its optionality though with outgoing Governor Hawkesby noting that the 2.20% OCR projection signals an easing bias.

- Compared with levels prior to yesterday’s RBNZ decision, pricing is 7-17bps higher across meetings, again led by late-2026 contracts. Notably, September 2026 now assigns a 25bps hike a 21% probability.

JPY: USD/JPY - Consolidates Around 156.00, BoJ Speak No Hints On Dec Hike Risk

The USD/JPY range today has been 155.73 - 156.49 in the Asia-Pac session, it is currently trading around 156.00/05, -0.30%. The pair again found some solid demand toward 155.50 in our session and has stalled the pullback for now. The move in the Yen looks like it is going to force the BOJ into action in December and we now have the market pricing in imminent cuts in the US. This could have an impact or at least slow what looked like a situation that was about to get out hand. Technically USD/JPY continues to look like it wants to test higher with the first big support back toward the 154-155 area which we suspect buying interest may emerge. Look for some consolidation to continue as the market contemplates if these moves by central banks are enough to challenge the weakening Yen trajectory.

- MNI AU - Extra Issuance In 2-5yr Tenors, No Change For 10-40yr Per Reuters: Rtrs reports that the Japan government will increase the issuance of 2yr and 5yr JGBs from January next year, as part of its plan to fund the stimulus package. It also notes that there are no changes to planned issuance for 10-40yr tenors. JGBs have been under pressure amid increased scrutiny on the fiscal outlook.

- MNI AU - Noguchi -Favours Gradual Hikes As Economy Adjusts To New Price Backdrop : Noguchi spoke about the need to get rate hike timing rate, as hiking too early or too late can cause problems. He stated that hiking too early risks derailing the wage/price cycle and sustainably hitting the 2% inflation target, while raising rates too slowly will risk destabilizing price and activity trends (presumably as policy rates have to rise rapidly to bring down inflation). Note that market pricing has firmed for a Dec move, but is still only just above 50% pricing (or around +13bps).

- Options : Close significant option expiries for NY cut, based on DTCC data: 154.00($665m),155.75($750m). Upcoming Close Strikes : 154.00{$1.28b Nov 28), 155.00($744m Dec 1), 155.00($2b Dec 2) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 105 Points

NZD/USD - Correction Extends Above 0.5700-0.5710, First Target 0.5760

The NZD/USD had a range today of 0.5693 - 0.5732 in the Asia-Pac session, going into the London open trading around 0.5730/35, +0.55%. The NZD/USD extended its surge higher moving above the 0.5710 resistance with better NZ data and Hawkesby saying the hurdle is high for more cuts. Positioning still looks to be an issue in the short term. While the risk backdrop remains so constructive this will provide further headwinds for the NZD shorts and I suspect we see more of the weaker hands pressured. On the day dips back toward 0.5680/0.5700 will likely be supported, if this break above 0.5710 is sustained the market will be looking toward 0.5760 first then the more important 0.5800-50 resistance.

- MNI AU - Strong Retail Spending Consistent With RBNZ Pause: Q3 retail sales volumes were significantly stronger than expected and rose for the fourth consecutive quarter. They were up 1.9% q/q to 4.5% y/y, the fastest pace since Q4 2021 and consistent with the RBNZ on hold for now as signalled by its revised November OCR path. Governor Hawkesby said in the decision press conference that there were signs easing was supporting consumption and this data is in line with that sentiment.

- MNI AU - Business Survey Signals Stronger H2 Growth & Lower Q4 Inflation. The ANZ November business survey is consistent with RBNZ’s Hawkesby’s comment following Wednesday’s rate cut that the recovery “is happening right now through Q3 and Q4”. It is a piece of high frequency data consistent with rates staying at 2.25% for now. Businesses are their most positive since 2014. Activity compared to a year ago, a good indicator for GDP, rose to 21.3 from 4.6 with ANZ saying that only construction remains negative. Thus it appears that growth recovered further in Q4.

- “RBNZ’S HAWKESBY SAYS HURDLE IS HIGH FOR ANY FURTHER RATE CUTS, CANNOT KEEP DOOR OPEN TO EASING FOREVER" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5700(NZD356m Dec 2), 0.5940(NZD427m Dec 1) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 47 Points

AUD/USD - AUD Looks To Challenge 0.6540-0.6560

The AUD/USD has had a range today of 0.6517 - 0.6536 in the Asia- Pac session, it is currently trading around 0.6535, +0.25%. The AUD/USD opened very well bid this morning and extended above its overnight highs.The AUD is now firmly back above 0.6500 and is looking to test the pivot toward 0.6540-60 within its wider 0.6350-0.6700 range. I suspect dips on the day back toward 0.6480-0.6500 will remain supported. A sustained break above the 0.6560 area is needed to potentially signal a move toward the top-end of its range, targeting 0.6625 first and then the 0.6700 area.

- MNI AU - Very Strong Private Capex To Support Q3 GDP Print. Q3 private capex volumes soared 6.4% q/q, the fastest since Q1 2012, and is setting up the 3 December GDP release for a solid increase at this stage. Inventory data is out 1 December and the net export and public demand contributions on 2 December. The jump in investment in the quarter was across both building and plant & machinery and was driven by a 11.5% q/q jump in the latter from spending on aircraft but also data centres. Annual growth rates are showing an investment recovery is currently taking place.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6650(AUD578m). Upcoming Close Strikes : 0.6550(AUD521m Dec 1), 0.6800(AUD532m Dec 2) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 42 Points

ASIA STOCKS: US Rates Continue to Drive Optimism; FTSE Malay Below Key Tech

Global market optimism driven by growing expectations of a Federal Reserve interest rate cut is a major driver of Asian equity markets again today. India's Nifty 50 has reached a new record high due to growth optimism and GST cuts starting to filter through to the broader economy. The ever present China property market concerns were highlighted today as China Vanke sought to delay paying the principal on a CNY2bn bon due mid December, risking another default for the sector. In M&A, China's ANTA Sports is said to be considering a bid against Li Ning Co for PUMA SE, employing advisors in Hong Kong. The KOSPI and NIKKEI were up again today with tech stocks leading with Japan's Advantest was up sharply and SK Hynix in Korea.

- The NIKKEI is up +1% today and over 3% for the last five trading days. The KOSPI is approaching the 4,000 level again, up +0.45% today yet 5% lower than the November 3 high.

- China's have shrugged off the Vanke headlines, despite bond markets worrying about another default. The Hang Seng, CSI 300 and Shenzhen are all up +0.30% whilst Shanghai outperformed its domestic rivals with gains of +0.49% EV battery material producer Anhui Estone Materials up 20% today.

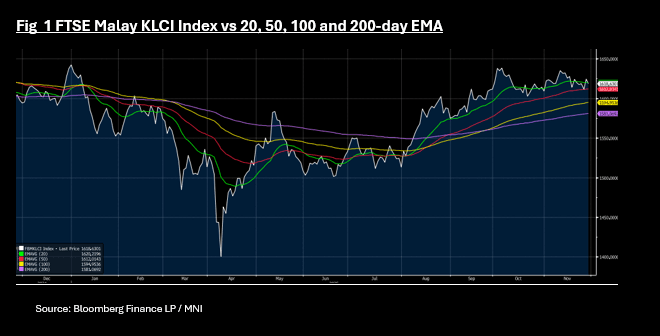

- SE Asia's major bourses all fell today as profit takers took over in Jakarta dragging sentiment with it. The JCI is down -0.60% today, the SE Thai -0.05% and the FTSE Malay KLCI down -0.33%. The KLCI declines sees it break below the 20-day EMA. At 1,619 for the index, below is the 50-day EMA of 1,612.

- The NIFTY 50 has opened up by +0.20% to reach a new high of 26,259 with almost all sectors up, with metals and oil & gas leading. The market is positioning further for an RBI cut next month following the firming of US rate bets, and comments from the RBI governor coupled with local commentators flagging a rebound in domestic consumption coming following the GST cuts.

ASIA STOCKS: Scope Remains For A Further Recovery In Inflow Momentum

Yesterday saw positive inflow momentum across the Asia Pac region. This has scope to continue into month end, given the rebound in global indices (aided by the more dovish Fed backdrop) over the past week. Most markets are still running at net outflows for the past 5 trading days though, particularly South Korea and Taiwan. For South Korea's Kospi we are firmer today, but haven't been able to sustain above the 4000 level. Per NBUY we have seen further inflows so far today (+$113mn). The BoK left rates on hold, as expected, but local rates rose on reduced easing prospects. This may be tempering local equity market sentiment at the margins.

- At the other end of the spectrum, Indian inflows may gain ground into year end, amid heightened RBI easing risks for Dec. The NIFTY has broken to fresh highs above 26200. Local FX is weaker, but RBI is managing depreciation trends.

- In South East Asia, inflows were mostly positive yesterday, but Indonesia remains the standout in Nov.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 494 | -1371 | -5325 |

| Taiwan (USDmn) | 491 | -2600 | -6379 |

| India (USDmn)* | 109 | -89 | -16275 |

| Indonesia (USDmn) | -33 | 212 | -1717 |

| Thailand (USDmn) | 15 | -58 | -3339 |

| Malaysia (USDmn) | 29 | -132 | -4581 |

| Philippines (USDmn) | 41 | 68 | -643 |

| Total (USDmn) | 1146 | -3970 | -38257 |

| * Data Up To Nov 25 |

Source: Bloomberg Finance L.P./MNI

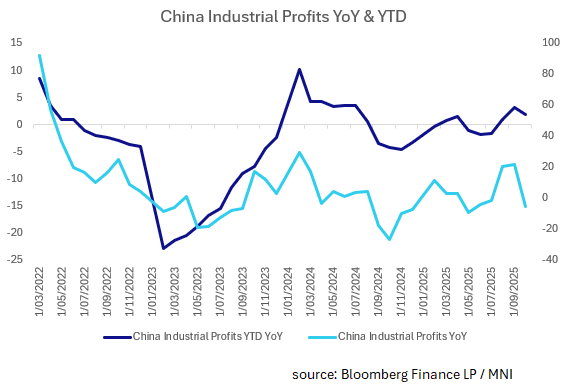

CHINA: Industrial Profits Moderate, Trade War Impacts Remain

- Unsurprisingly Industrial Profits in China slipped in October with the YoY number negative and the YTD result below September.

- Industrial output had lifted in September ahead of the planned Xi Trump meeting as producers increased output. Industrial Production then moderated in the October release.

- The August and September Industrial Profit results saw profit growth both in excess of 20%, the best consecutive month result since mid-2021.

- Industrial profit releases tend to be volatile and with the added layer of trade war uncertainty the decline of -5.5% looks at this stage like a correction rather than a change in direction and any changes to monetary policy will likely remain on hold until the new year.

- Year to data moderated to +1.9% from +3.2%, ahead of the negative three year average.

OIL: Crude Likely To Finish November Down, Trading May Be Thin Due To US Holiday

Oil prices are lower in Thursday’s APAC trading after rising around a percent yesterday. Trading is likely to be thin with the US closed for the Thanksgiving holiday. WTI is down 0.6% to $58.30/bbl off the day’s trough at $58.27, while Brent is 0.5% lower at $62.80/bbl. Benchmarks have been in a $2 range this week as they react to progress and doubts regarding a Ukraine peace deal. Excess global supply remains its main concern which is likely to limit any upside.

- OPEC meets on 30 November to decide January production levels but the group decided at the last meeting to leave quotas unchanged in Q1 given seasonally soft demand. So it seems unlikely to surprise with another output increase, especially given an additional monthly fall in the oil price.

- US special envoy Witkoff is to visit Russia next week to present the revised peace agreement. The US also said it won’t include security guarantees for Ukraine in the plan until there is a deal. Disagreements over territory are also unresolved and so an agreement still seems elusive.

- Later December German GfK consumer confidence, October euro area M3 and November European Commission economic sentiment print. The BoE’s Greene, ECB’s Cipollone, Tuominen, Machado and de Guindos speak and the October ECB meeting minutes are published.

Gold Lower As US Closed, No New US Information Until Monday

Gold is 0.2% lower at $4153.0/oz in Thursday’s APAC session in what has generally been a positive week for the metal driven by increased Fed rate cut pricing for the 10 December meeting following dovish comments from NY Fed’s Williams. There is now around 22bp of easing priced in. Bullion appears to be stabilizing now as there will be little news from the US until Monday due to the Thanksgiving holiday. The weaker US dollar (BBDXY -0.1%) also hasn’t provided support today.

- Technicals suggest that gold’s dominant trend is upwards. Bullion fell to a low of $4142.79 today, holding well above initial support at the 50-day EMA of $3966.8.

- Bloomberg estimates that flows into gold ETFs have been flat over the last three weeks.

- Silver is down 0.9% to $52.89 after a low of $52.701. It jumped 3.7% to $53.36 on Wednesday.

- Equities are mixed with the S&P e-mini and ASX flat but Hang Seng up 0.3% and Jakarta Comp down 0.5%. Oil prices are lower with WTI -0.6% to $58.31/bbl. Copper is steady.

- Later December German GfK consumer confidence, October euro area M3 and November European Commission economic sentiment print. The BoE’s Greene, ECB’s Cipollone, Tuominen, Machado and de Guindos speak and the October ECB meeting minutes are published.

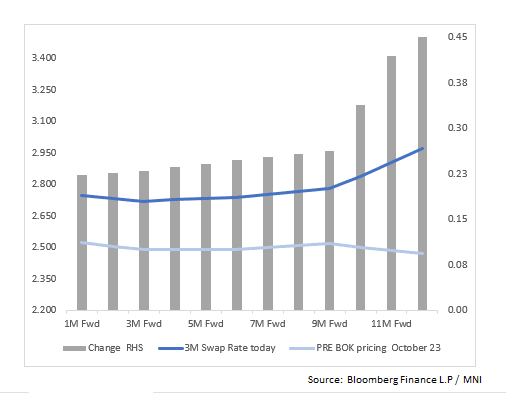

SOUTH KOREA: KRW Swaps See No Cuts Over Next 12 Months

- As markets awaited the BOK governors press conference, focus on the forward-looking guidance from voting members. At the prior meeting, four members kept the door open to a rate cut. Today’s meeting sees that down to three.

- Against a backdrop of a weaker won (which pushes up import costs) and persistent housing-market pressure, Rhee signaled that monetary easing is effectively paused for now — at least until more clarity emerges on currency and property-market stability

- Governor Rhee was clear that “now is not the time to discuss rate hikes,” before noting that ‘it takes on average 12 months to move to hike from pause.” That would be July 2026.

- The focus on Seoul property prices and CPI YoY at its highest since June 2024 has seen swap prices expecting the BOK to be on hold for some time with limited changes priced in over the next 12 months, as is now increasingly likely.

- Over the next 1, 2 and 3 months there was a cumulative 12bps of cuts priced in at the start of the week relative to levels at the October meeting, and today that is just 4bps, and over the next 12 months +8bps of increases ( from +9bps earlier this week.)

- The MIPR function on BBG has 6bps of increases over a 12 month period.

- Markets turn their attention this week to tomorrow's industrial production.

CNH Edges Lower Post Fixing, Scope To Give Back Some Recent Outperformance

USD/CNH is just off session highs (7.0772), last near 7.0760/65. We have largely maintained a positive bias since the stronger than expected USD/CNY fixing (fixing above mkt forecasts for the first time since July), while onshore USD/CNY spot has edged back above 7.0800 in the first part of trade. For USD/CNH we expect to see some selling interest in the 7.0900/7.1000 region, as this area marked recent lows in the pair. Note that 20-day EMA is back around 7.1045/50.

- The 1 month risk reversal is at -0.6250, which is near 2025 lows. If this stabilizes it may also aid a steadier USD/CNH spot backdrop, (at least based off historical correlations).

- CNH is underperforming broader USD softness, with the BBDXY down a further 0.1% so far today. CNH/JPY is off, but still above 22.05. Given the CNY CFETS basket tracker is still close to multi month highs, there is scope for yuan underperformance in the near term, if we see further broader USD index losses.

- Earlier we had a notable slowing in the Oct industrial profits to -5.5%y/y (from 21.6% in Sep). Still, local equities are higher, the CSI 300 up around 0.30%. Fresh property woes, amid a push by Vanke to delay a bond payment, has seen the CSI 300 real estate fall by 1.5%, but this isn't dragging the aggregate index lower.

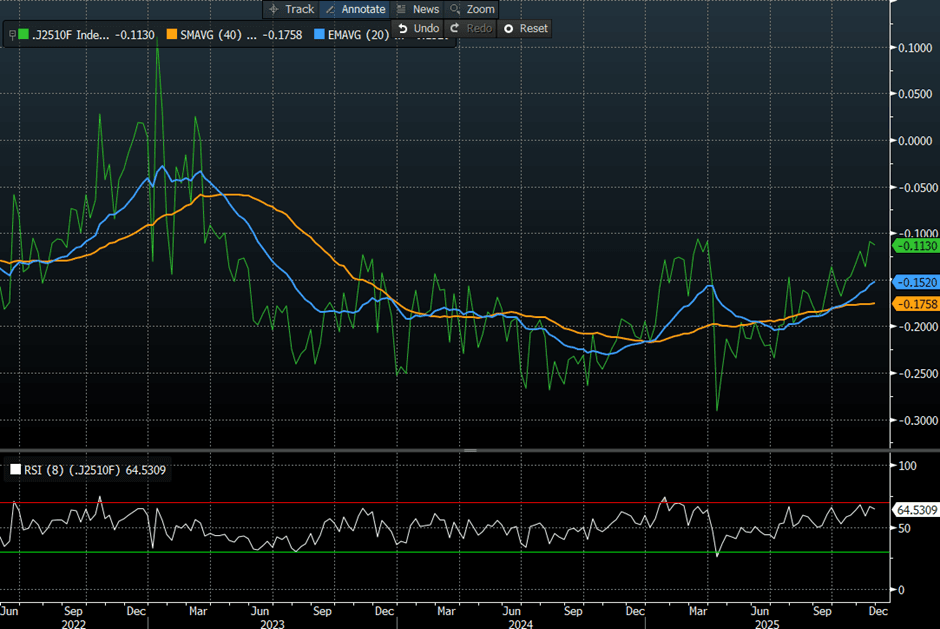

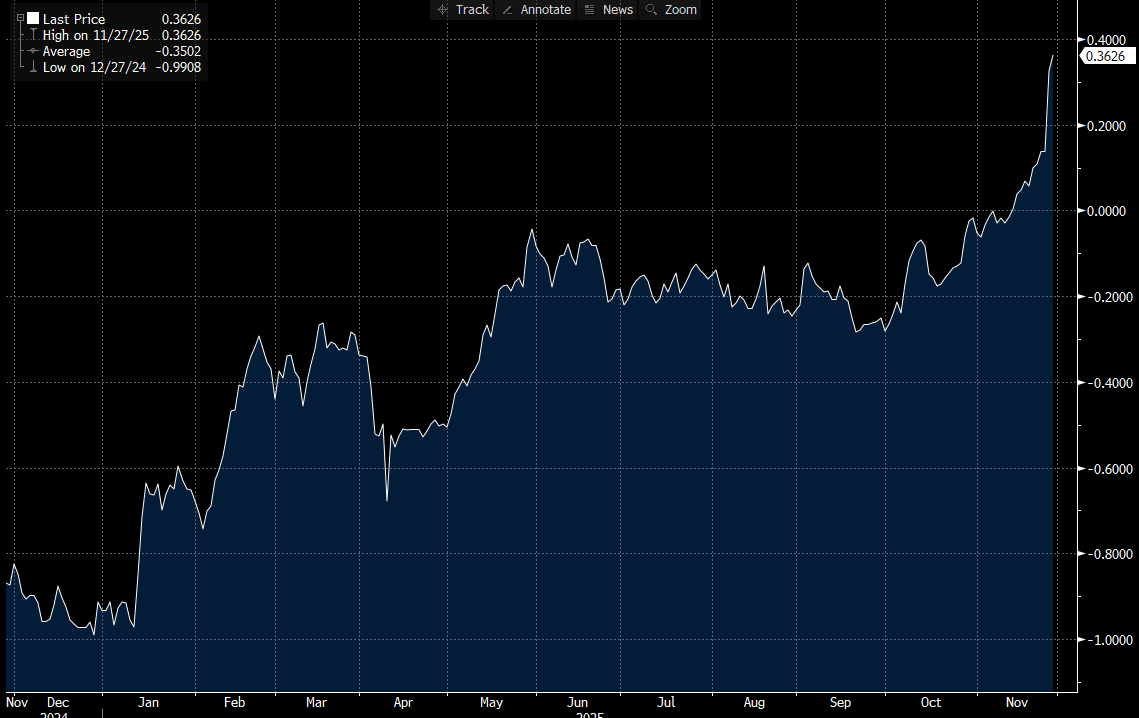

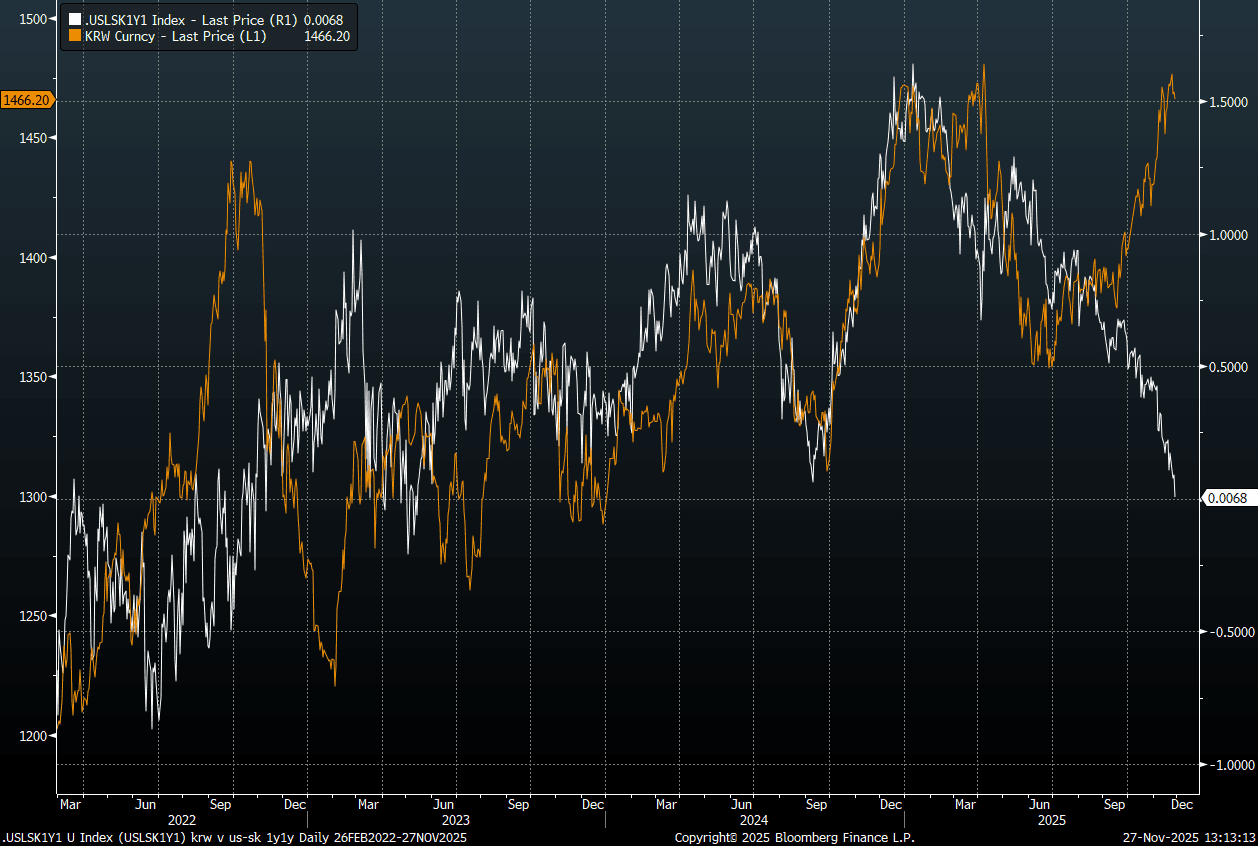

KRW: Won Can't Rally With Hawkish BoK, Wedge With Yield Differentials Widens

USD/KRW has seen some volatility as headlines from BoK Governor Rhee cross, but remains within recent ranges (1466/67, up around 0.15% in won terms so far today). The hawkish from the rates market is yet to meaningfully benefit the won post today's decision. USD/CNH is higher, psot the stronger than expected USD/CNY fixing, so this may be offsetting.

- The BoK did leave the door ajar for further easing, but it did remove the explicit easing bias from the statement. The SK NDIRS rate has risen to fresh highs of 2.97%, levels last seen in late 2024. This is pushing the US-SK rate differential towards flat, see the chart below. There remains a significant wedge with USD/KRW levels, with domestic outflow pressures still a headwind for the won.

- Governor Rhee noted in his press conference a further Fed easing should benefit the won, although as the chart below highlights, this backdrop is yet to materialize.

- Rhee stated that the central bank has the tools to stabilize if needed, noting domestic (leveraged) retail outflows are risky, while the National Pension Service needs to have discussions with the government and the BOK, as its size has gotten too big (this was likely made in reference to the domestic outflow pressures the NPS creates, thereby impairing FX balance).

- A the South Korea FinMin stated yesterday, via BBG: "The government has begun talks with key market players to establish a "new framework" for FX stability, and the finance minister expects cooperation from exporters."

- Until we get greater clarity on what steps are being taken (or signs of NPS hedging flows) USD/KRW may remain elevated against yield differentials. We would still expect one-sided/sharp moves higher in USD/KRW to draw a policy response though.

Fig 1: Spot USD/KRW Elevated Relative to US-SK 1y1 Rate Differential

Source: Bloomberg Finance L.P./MNI

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 27/11/2025 | 0700/0800 | * | GFK Consumer Climate | |

| 27/11/2025 | 0800/0900 | ** | Economic Tendency Indicator | |

| 27/11/2025 | 0830/0930 | ECB Cipollone Remarks at Euro Cyber Resilience Board | ||

| 27/11/2025 | 0900/1000 | ** | M3 | |

| 27/11/2025 | 0900/1000 | ** | ISTAT Consumer Confidence | |

| 27/11/2025 | 0900/1000 | ** | ISTAT Business Confidence | |

| 27/11/2025 | 1000/1100 | * | Consumer Confidence, Industrial Sentiment | |

| 27/11/2025 | 1100/1200 | ECB de Guindos Remarks at CEDE Congress of Executives | ||

| 27/11/2025 | 1330/0830 | * | Current account | |

| 27/11/2025 | 1330/0830 | * | Payroll employment | |

| 27/11/2025 | 1630/1630 | BOE Greene Speech at Goodbody Conference | ||

| 28/11/2025 | 2330/0830 | ** | Tokyo CPI | |

| 28/11/2025 | 2330/0830 | * | Labor Force Survey | |

| 28/11/2025 | 2350/0850 | * | Retail Sales (p) | |

| 28/11/2025 | 2350/0850 | ** | Industrial Production | |

| 28/11/2025 | 0700/0800 | *** | GDP | |

| 28/11/2025 | 0700/0800 | ** | Retail Sales | |

| 28/11/2025 | 0700/0800 | ** | Import/Export Prices | |

| 28/11/2025 | 0700/0800 | ** | Retail Sales | |

| 28/11/2025 | 0745/0845 | *** | HICP (p) | |

| 28/11/2025 | 0745/0845 | ** | PPI | |

| 28/11/2025 | 0745/0845 | *** | GDP (f) | |

| 28/11/2025 | 0745/0845 | ** | Consumer Spending | |

| 28/11/2025 | 0745/0845 | Payrolls | ||

| 28/11/2025 | 0800/0900 | *** | HICP (p) | |

| 28/11/2025 | 0800/0900 | ** | KOF Economic Barometer | |

| 28/11/2025 | 0800/0900 | *** | GDP | |

| 28/11/2025 | 0855/0955 | ** | Unemployment | |

| 28/11/2025 | 0900/1000 | *** | GDP (f) | |

| 28/11/2025 | 0900/1000 | *** | Bavaria CPI | |

| 28/11/2025 | 0900/1000 | *** | North Rhine Westphalia CPI | |

| 28/11/2025 | 0900/1000 | *** | Baden Wuerttemberg CPI | |

| 28/11/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 28/11/2025 | 1000/1100 | *** | Italy Flash Inflation |