BONDS: NZGBS: Post-RBNZ Sell-Off Extends Today, Full Hike Priced For Late-26

NZGBs closed showing a bear-flattener, with yields 2-8bps higher. As it stands, yields are 8-14bps higher than pre-RBNZ levels, with the 2/10 curve flatter.

- In a relative sense, NZGBs have also underperformed, with the NZ-US 10-year yield differential 3bps wider at +23bps, and the NZ-AU 10-year differential 1bp higher at -27bps.

- The recent cheapening in NZGBs, however, didn’t deter buyers at today’s weekly auction, with cover ratios ranging from 3.86x (May-30) to 5.46x (May-34).

- Swap rates closed 4-9bps higher, with the 2s10s curve flatter. The curve is around 10bps flatter than yesterday’s pre-RBNZ levels.

- RBNZ-dated OIS pricing closed flat to 9bps firmer across meetings today, led by the late-2026 contracts, extending yesterday’s post-policy decision firming. Indeed, relative to pre-RBNZ levels, pricing is 8-20bps higher across meetings, again led by late-2026 contracts.

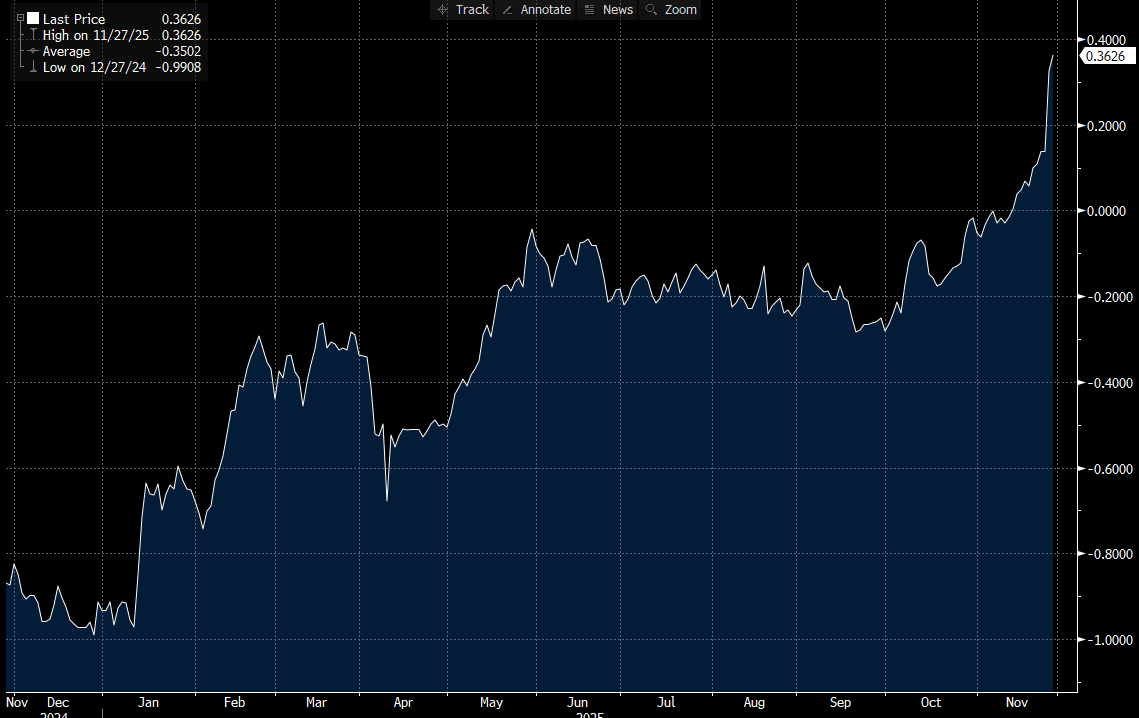

- Notably, as well, November 2026 now assigns a 25bps hike with a 37% probability (see chart). The push into positive territory for 12-month forward expectations for the RBNZ in mid-November was the first time since October 2023.

- Tomorrow, the local calendar will see ANZ Consumer Confidence and Filled Jobs data.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Quiet Day as Curves Modestly Flatter

Despite weakness across major equity bourses, US bond futures didn't see a lead in with TYZ5 posting only modest gains. Up +02 at 113-15+ the the 10-Yr price action was muted as volumes remained modest throughout the trading day.

Cash volumes were light also, capping yield moves.

- The US 2-Yr is 3.499% (+0.4bp)

- The US 5-Yr is 3.607% (+0.3bp)

- The US 10-Yr is 3.979% (-0.4bps) as it consolidates below the 4.00% recent range bottom.

- The US 30-Yr is 4.551% (-0.3bp)

Focus for markets tonight will be US$69bn 2-Yr auction, US$70bn 5-Yr auction and various bill auctions.

Economic Data focus is on :

10/28/2025 9:00 FHFA House Price Index MoM (-0.1%, -0.1%)

10/28/2025 9:00 S&P Cotality CS 20-City MoM (-0.07%, -0.10%), YoY (1.82%, 1.40%)

10/28/2025 10:00 Richmond Fed Mfg Index (-17, -10)

10/28/2025 10:00 Conf. Board Consumer Confidence (94.2, 93.4)

10/28/2025 10:30 Dallas Fed Services Activity (-5.6, --)

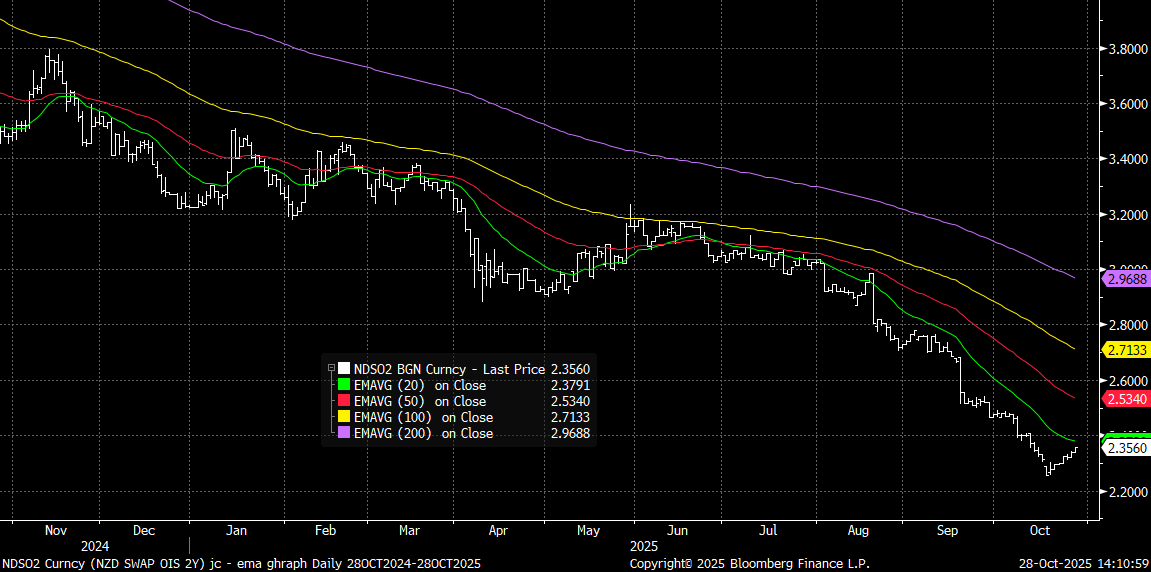

BONDS: NZGBS: 2yr Swap Close To 20-day EMA Resistance, Better Data Helps

NZGB yields have been biased higher as Tuesday trade unfolded, supported by earlier data outcomes. The 2yr is up nearly +2bps to 2.54%, while the 5yr is up near 3bps. The 10yr has seen a more modest rise and is still sub 4.00% at this stage. We are still sub key EMAs, but focus will rest on whether we can test higher. The 2yr swap rate is close to 2.36%, closing in on a test of its 20-day EMA resistance point, see the chart below.

- Earlier data showed Q3 NZ filled jobs rose 0.1% q/q signalling that employment likely stabilised in the quarter after falling 0.1% q/q in Q2. Q3 labour market data print on 5 November and will be an important input into the 26 November RBNZ decision.

- Other data showed NZ’S household living-costs price index (HLPI) for Q3 rose 2.4% y/y, below the CPI at 3.0%, down from 2.6% in Q2 and 3.8% in Q3 2024. It tends to lead real private consumption growth by two to six quarters. The recent trend signals that the tentative recovery in spending growth should continue after Q2’s 1.5% y/y rate.

- RBNZ pricing still has a 25bps cut priced in for the Nov meeting, but OIS dated contracts for 2026 are slightly firmer. For July 2026 we are around 2.18%, against mid Oct lows near 2.00%.

- The NZ 2/10s curve has flattened today, off around 2bps to +146bps. The NZ-US10yr spread is holding above flat, last +3bps.

- Tomorrow, the local data calendar is empty.

Fig 1: NZ 2yr Swap Rate & Key EMAs

Source: Bloomberg Finance L.P/MNI

ASIA STOCKS: Markets Mixed as Investors Wait for News from APEC Summit

The record period for Asia's major bourses took a breather today ahead of the APEC summit as the world awaits to see what 'deals' are announced. With the focus on a US China pact and further news on the USD$350bn investment fund for Korea investment in the US, China and Korea were among the fallers today. The hopes of a US China trade pact has seen flows into EM funds strengthen with the Vanguard FTSE Emerging Markets ETF has had over $400m of net inflows in recent days with investors seeking to benefit from a cooling of the trade war. This comes despite key markets hitting new all time highs in advance of the APEC summit.

- The KOSPI was one of the biggest fallers of the major markets down -1.25% and back below 4,000.

- The NIKKEI has done very little whereas the major bourses in China have all delivered modest gains with onshore indexes +0.20 - 0.40% higher whilst the HSI did very little.

- The Jakarta Composite fell heavily yesterday and the weakness carried on into today with falls of -0.18%. The losses sees the JCI at 8,106 and dip below the 20-day EMA of 8,126. It has traded below the 20-day EMA only once in the last month, failing to hold losses as buyers returned.

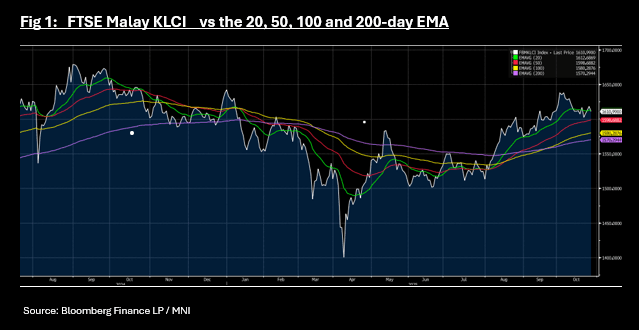

- The FTSE Malay KLCI is one of the biggest fallers, despite the potential for a trade deal that could be imminently announced with the US, as President Trump visits. Malaysia and the US upgraded ties to the highest rung possible, and the two sides pledged to deepen maritime security cooperation at a time when the US and China are competing for influence across the region (per BBG). Down -0.45% today sees the index break below the 20-day EMA which it has tried unsuccessfully to hold below on several occasions this month.