KRW: Won Can't Rally With Hawkish BoK, Wedge With Yield Differentials Widens

USD/KRW has seen some volatility as headlines from BoK Governor Rhee cross, but remains within recent ranges (1466/67, up around 0.15% in won terms so far today). The hawkish from the rates market is yet to meaningfully benefit the won post today's decision. USD/CNH is higher, psot the stronger than expected USD/CNY fixing, so this may be offsetting.

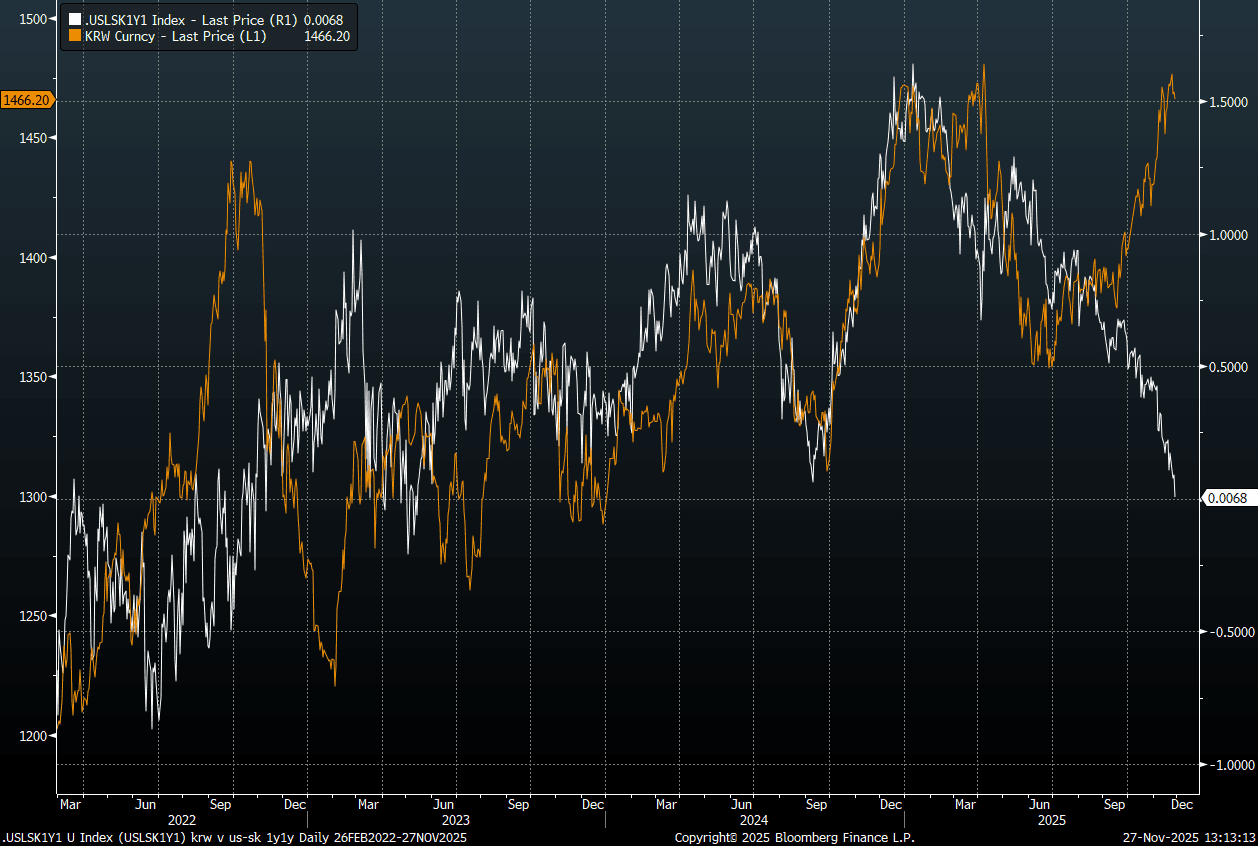

- The BoK did leave the door ajar for further easing, but it did remove the explicit easing bias from the statement. The SK NDIRS rate has risen to fresh highs of 2.97%, levels last seen in late 2024. This is pushing the US-SK rate differential towards flat, see the chart below. There remains a significant wedge with USD/KRW levels, with domestic outflow pressures still a headwind for the won.

- Governor Rhee noted in his press conference a further Fed easing should benefit the won, although as the chart below highlights, this backdrop is yet to materialize.

- Rhee stated that the central bank has the tools to stabilize if needed, noting domestic (leveraged) retail outflows are risky, while the National Pension Service needs to have discussions with the government and the BOK, as its size has gotten too big (this was likely made in reference to the domestic outflow pressures the NPS creates, thereby impairing FX balance).

- A the South Korea FinMin stated yesterday, via BBG: "The government has begun talks with key market players to establish a "new framework" for FX stability, and the finance minister expects cooperation from exporters."

- Until we get greater clarity on what steps are being taken (or signs of NPS hedging flows) USD/KRW may remain elevated against yield differentials. We would still expect one-sided/sharp moves higher in USD/KRW to draw a policy response though.

Fig 1: Spot USD/KRW Elevated Relative to US-SK 1y1 Rate Differential

Source: Bloomberg Finance L.P./MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MNI EXCLUSIVE: MNI Discusses BoJ's Hike Path Amid Sluggish Underlying CPI

FOREX: USD/JPY Lower As Key US Officials Meet, But Above Key Support

The USD is continuing to moderate, the BBDXY off a little over 0.10% to be 1210/11 in the first part of Tuesday trade. Recent lows were back around 1205. Underperformers from Monday, JPY and CHF, are seeing some catch up, particularly on the yen side. A reminder from the Japan authorities around FX moves has likely helped USD/JPY lower, while a visit from key US officials (including President Trump) has also potentially encouraging some paring of longs in the pair. Still, the 50-day EMA is sub 150.00 (versus current levels of 152.40/45, off 0.30% so far today), so there is still some gap to important support points. USD/CHF was last near 0.7940/45, down around 0.15%.

- Earlier we saw: "JAPAN ECONOMY MINISTER KIUCHI: IT'S IMPORTANT TO AVOID RAPID, SHORT-TERM FLUCTUATIONS IN FX MOVES" (via RTRS), which reminded the market intervention risks are still apparent.

- Takaichi/Trump meeting headlines have been fairly high level, with the two leaders signing a joint framework on critical minerals.

- AUD and NZD are drifting a little higher, more so NZD/USD, last near 0.5780. The pair is looking to build a base above its 20-day EMA (near 0.5770) and test through 0.5800. Data outcomes today suggest gradual improvement in the labour market, with NZ yields edging higher.

- AUD/USD was last around 0.6560/65, lagging yen and NZD but still above all key EMAs. Earlier Oct highs were close to 0.6630.

- USD/CNH has tested under 7.1000, but has been unable to sustain the break so far.

- Cross asset trends are muted from a US equity futures standpoint, with steady trends so far today. US Tsy yields are mixed, with some modest gains at the front end.

RBA: Higher Core CPI Could Drive RBA Pause In November & Await More Data

The RBA August projections had another 25bp of easing in Q4 based on market pricing. This still allowed underlying inflation to settle close to the 2.5% band mid-point over 2026. Wednesday’s Q3 CPI data will be important for how it impacts the RBA’s inflation outlook which will be key for the 4 November decision. A pause at the November meeting is likely to leave the December meeting live though. Market pricing reflects a good degree of uncertainty around November.

- The AUD OIS is currently not sure with 10bp priced in for November and 17bp by year end but this could move sharply with Q3 CPI.

- Key watch points for CPI tomorrow are as follows: Bloomberg consensus expects trimmed mean to print at 0.8% q/q & 2.7% y/y, which would see a pickup in the 2q/2q annualised rate to 2.8% from 2.6%. This outcome could argue for a hold or a cut dependent on the revised outlook and services inflation result.

- Contained services, core around 2.6-2.7% y/y or below would likely drive further easing, but even 2.8% could see another hold in November as the Board waits for more data, especially given it sees “signs that private demand is recovering”.

- Bullock said the Board was concerned about the rise in some of monthly CPI components, especially services. She noted that it has been sticky overseas and so the change in Q3 market services prices will be monitored. It moderated to 2.9% y/y in Q2 from 3.3%.

- This week Bullock reiterated that labour data are volatile and while the 0.2pp rise in the September unemployment rate to 4.5% was surprising, it could fall again in October. Thus she would like more information. The Board also looks at the 3-month averages and the Q3 unemployment rate only rose 0.1pp to 4.3% while underemployment fell 0.2pp to 5.8%.

- There are a lot of key data before the December meeting which could drive a November pause to wait and see, including surveys but also October jobs on 13 November, Q3 wages 19 November, October CPI 26 November (first full sample monthly CPI) and Q3 GDP 3 December.