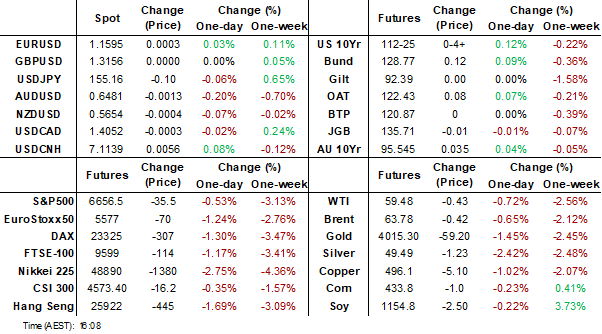

MNI EUROPEAN MARKETS ANALYSIS: JGB Curve Steepens Further

- Risk off has dominated the equity space, with tech sensitive markets in Asia Pac seeing the largest losses. Spill over has been evident from crypto weakness, as Bitcoin has tested sub 90k.

- The USD is higher against higher beta plays, but gains are modest for the most part. USD/JPY fell back under 155.00 as risk off drove safe haven flows, but this move proved short lived.

- The JGB curve continues to steepen, the 2/30s back within striking distance of recent highs. This comes ahead of the Takaichi/Ueda meeting, which kicks off shortly.

- Later the Fed’s Barr & Barkin, BoE’s Pill & Dhingra, and ECB’s Buch, Elderson, Machado & Tuominen speak. Delayed US IP and final August orders are released as well as ADP weekly employment estimates, November NY Fed services and NAHB housing.

MARKETS

US TSYS: Risk-Off Pushes Yields Lower

TYZ5 is dealing at 112-26, -0-05+ from closing levels in today's Asia-Pac session, as risk turns down, led by Bitcoin.

- Stocks have extended Monday's weakness in today’s Asia-Pac session. Chip makers led declines yesterday, followed by financials. Investors all of a sudden appear wary of lofty tech valuations, ahead of Nvidia Corp.’s earnings and a key US jobs report later this week.

- Cash US tsys are 2-3bps richer, with a steepening bias, in today's Asia-Pac session.

- However, JGBs have bear-steepened in today's session. "A “sell Japan” trend is likely to persist across equities, bonds and the yen unless Tokyo de-escalates its ongoing diplomatic spat with China, according to Tomo Kinoshita, global market strategist at Invesco." - BBG

- Tuesday's data schedule is light, with markets gearing up for the now-much-delayed September NFP print due this Thursday.

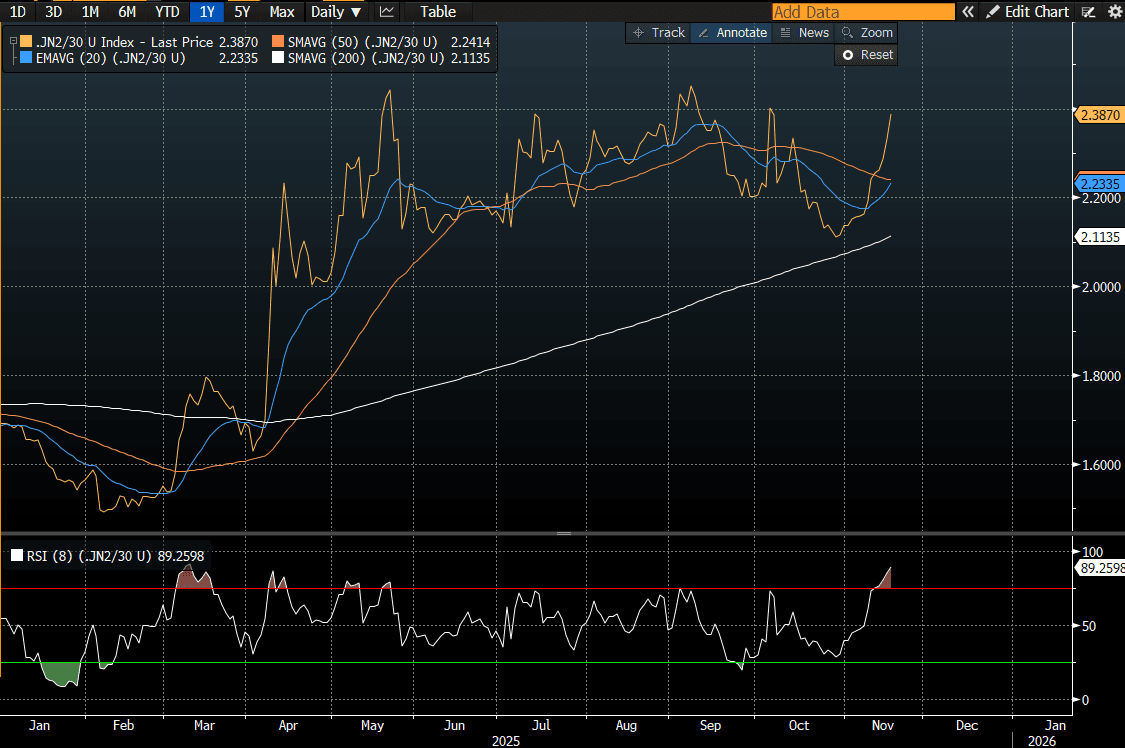

JGBS: Twist-Steepener, 2/30 YC Back Near Highs, PM/BOJ Meeting Due

JGB futures have clawed back to unchanged versus settlement levels.

- With the local calendar light, the domestic market, out to the futures-linked 7-year, has benefited from general global risk-off sentiment.

- "Japanese Prime Minister Sanae Takaichi is set to meet with Bank of Japan Governor Kazuo Ueda on Tuesday as she mulls support for an economy that shrank over the summer. The two will meet at 3:30 p.m. in Tokyo, according to the prime minister's office. - BBG

- Cash US tsys are 2-3bps richer in today's Asia-Pac session.

- JGBs have twist-steepened in today's session, with cash JGBs 1bp richer to 7bps cheaper across benchmarks. The benchmark 20-year yield is 3.6bps higher at 2.786% after setting a fresh cycle high of 2.816% ahead of tomorrow's supply.

- "A "sell Japan" trend is likely to persist across equities, bonds and the yen unless Tokyo de-escalates its ongoing diplomatic spat with China, according to Tomo Kinoshita, global market strategist at Invesco." – BBG

- Today’s move also places the 2/30 curve within striking distance of its recent high. (see chart)

- Swaps have twist-steepened, with rates 1bp lower to 4bps higher.

- Tomorrow, the local calendar will see Trade Balance and Core Machine Orders data.

Source: Bloomberg Finance LP

AUSSIE BONDS: Risk-Off Drives Bond Rally Ahead Of WPI Tomorrow

ACGBs (YM +4.0 & XM +3.5) are richer and at session highs as risk turns down, led by Bitcoin.

- Cash US tsys are 2-3bps richer, with a steepening bias, in today's Asia-Pac session.

- Cash ACGBs are 4bps richer with the AU-US 10-year yield differential at +32bps.

- Today’s Jun-54 bond auction saw the weighted average yield print 0.18bps through prevailing mids. However, demand weakened dramatically, as reflected by a cover ratio of 2.8500x, down from 4.0533x from the previous auction.

- The AOFM plans to sell A$1000mn of the 2.75% 21 June 2035 bond tomorrow and A$700mn of the 1.25% 21 May 2032 bond on Friday.

- The November meeting minutes reiterated that the RBA's central scenario is "in balance" with risks to both the downside and upside. With core inflation above target and ongoing signs of a recovery in demand, policy is likely to be on hold in December and into early 2026, depending on the data.

- RBA-dated OIS pricing is softer today, showing a 25bp rate cut in December at a 5% probability, with a cumulative 15bps of easing priced by mid-2026.

- The bills strip has bull-flattened, with pricing +3 to +5.

- Tomorrow, the local calendar will see the Wage Price Index and the Westpac Leading Index.

Bloomberg Finance LP

RBA: 2-Way Risks, How They Develop Likely To Determine If Hold Prolonged

The November meeting minutes reiterated that the RBA’s central scenario is “in balance” with risks to both the downside and upside. How these risks will develop is likely to determine whether monetary policy stays on hold or rates are cut further and while it is “not yet possible to be confident” about which scenario will materialise, the Board will “remain cautious and data dependent”. With core inflation above target and ongoing signs of a recovery in demand, policy is likely to be on hold in December and into early 2026, depending on the data.

- It can “afford to be patient” as it watches the data and assesses what the implications for its estimates of spare capacity and the degree of restrictiveness. The October jobs data came out the week after the decision and were tentatively in line with the view of stronger growth supporting the labour market, and thus rates on hold.

- The discussion was centred on the outlook for policy beyond the November decision. Rates could be held at the current 3.6% if the recovery is stronger than expected. This could be driven by a better global backdrop or stronger household consumption due to higher incomes and wealth.

- Also, if inflation stays high or productivity weaker than expected, then the RBA could adjust its spare capacity estimates lower. Another factor keeping rates unchanged would be a change in the view that policy is still restrictive.

- It noted that “information received since the previous meeting had increased the probability” of the factors above occurring.

- The Board would ease if spare capacity increased driven by the labour market weakening “materially” especially in the “market sector” or growth turning out softer than expected due to cautious households.

BONDS: NZGBS: May-36 Yield Finishes At Low After Tap

NZGBs closed showing a twist-flattener, with benchmark yields 1bp higher to 3bps lower.

- NZGBs held by international investors increased to 60.3% in October from 59.6% in September.

- RBNZ Business Expectations Survey for Q4 showed the weighted mean 1-year ahead inflation expectation falling to 2.42% from 2.53% in Q4. 2-year declines to 2.39% from 2.64% - BBG

- NZ Treasury issued NZ$6bn of May 2036 nominal NZGB after a syndicated tap. The issue was capped at NZ$6bn, with a total book size at final price guidance at NZ$24.8bn. It was priced at 12bps over the May 2035 nominal bond to yield 4.34%. JLM: ANZ Bank New Zealand, JPMorgan Securities Australia, UBS AG, Australia Branch and Westpac.

- Inflation-adjusted New Zealand existing home sales average price NSA fell 4.2% in October from the same period last year, according to Bloomberg calculations using official data.

- Swap rates closed little changed.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 33bps by February 2026.

- Tomorrow, the local calendar will see PPI data.

Bloomberg Finance LP

FOREX: Asia-Pac USD: BBDXY Testing Above 1220 As Risk Extends Lower

The BBDXY has had a range today of 1219.71 - 1220.63 in the Asia-Pac session; it is currently trading around 1220, +0.05%. The USD has drifted sideways in our session even with risk having another leg lower. The USD has bounced nicely off the 1210-1215 support area where it found some solid demand first up. Risk started the week on the backfoot yesterday again and the USD was the beneficiary. I continue to watch for signs of a base forming from which to move higher again if risk stays under pressure. On the day look for dips toward 1217-18 to now be supported first up, a break of the 1221-1222 area remains the pivot on the topside, above there and it could look to rebuild momentum for a test of the 1230-35 area.

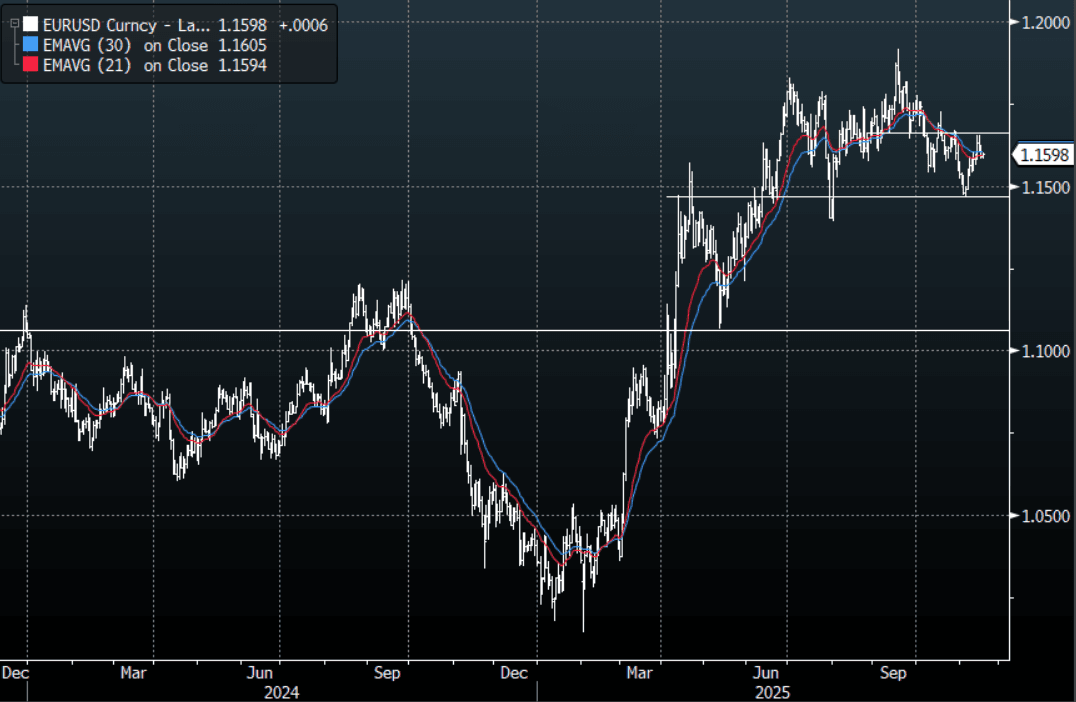

- EUR/USD - Asian range 1.1585 - 1.1597, Asia is currently trading 1.1595. The pair stalled and moved lower after finding some decent resistance toward the 1.1650-1.1700 area. This has been the pivot within the larger 1.1400-1.1900 range over the past few months. On the day look for the 1.1615-30 area to cap looking for a move lower.

- GBP/USD - Asian range 1.3145 - 1.3160, Asia is currently dealing around 1.3150. I continue to favor fading rallies, as GBP looks to have put in a medium term top. A sustained move back below 1.3080-1.3100 support would see the momentum lower reinstated and focus turn back toward the 1.3000 area. Suspect rallies back toward the 1.3250-1.3300 will be sold into if we see a bounce.

- Cross asset : SPX -0.70%, Gold $4010, US 10-Year 4.11%, BBDXY 1220, Crude Oil $59.46

- Data/Events : Spain Home sales

Fig 1: EUR/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

JPY: Asia-Pac: USD/JPY - Consolidates Gains Above 155.00

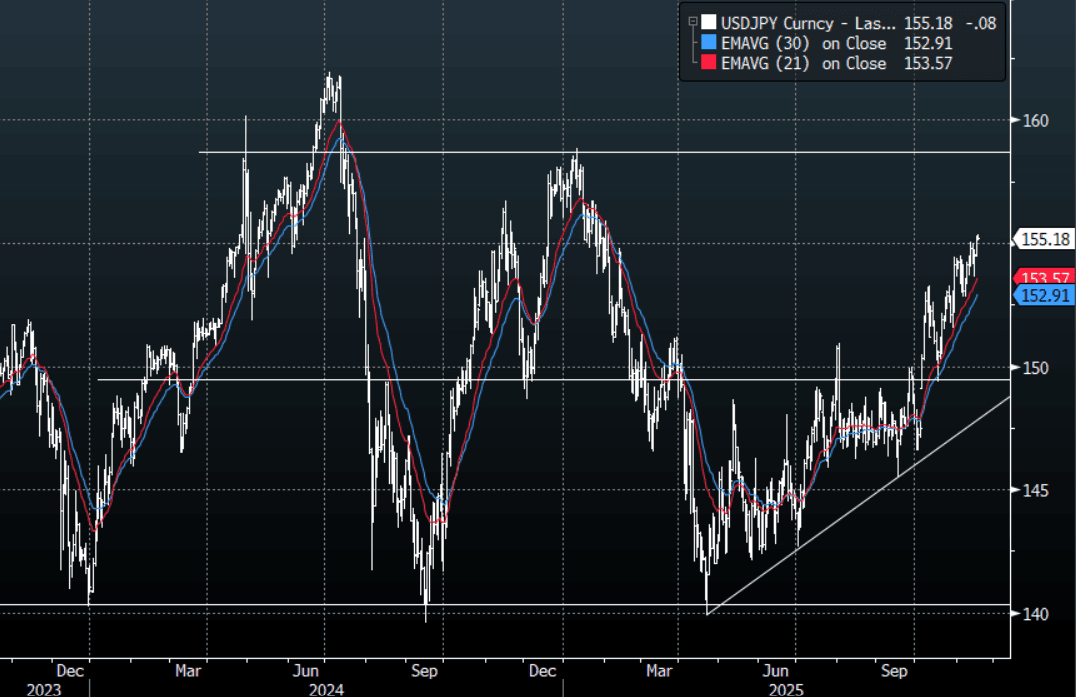

The USD/JPY range today has been 155.11 - 155.38 in the Asia-Pac session, it is currently trading around 155.20, -0.05%. The move lower in risk did not bring the usual bout of Yen buying as its safe haven status begins to be questioned. USD/JPY I suspect will remain well supported on dips as the market remains wary of the new leadership policies together with a reticence to hike rates. I will be watching today to see if the pair can build on its move above 155.00 and regain its momentum higher, look for dips in the Asian session back toward 144.70-144.90 to be supported on dips initially. A sustained move above here and the market will turn its focus back toward 160, much to the displeasure of the MOF/BOJ.

- "Japanese Prime Minister Sanae Takaichi is set to meet with Bank of Japan Governor Kazuo Ueda on Tuesday as she mulls support for an economy that shrank over the summer. The two will meet at 3:30 p.m. in Tokyo, according to the prime minister's office. The meeting comes after a report showed the Japanese economy contracted in the three months through September on a US tariff-linked slump in exports and a sharp drop in property buying." - BBG

- MacroEdge reporting on X that, "Japanese 20Y hits highest level since July 1999 as Prime Minister doubles down on printing."

- “JAPAN FINMIN KATAYAMA: RECENTLY SEEING ONE-SIDED, RAPID MOVES, ALARMED OVER FX MOVES. WILL THOROUGHLY MONITOR FOR EXCESSIVE FLUCTUATIONS AND DISORDERLY MOVEMENTS IN FOREX MARKET, WITH HIGH SENSE OF URGENCY - RTRS"

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.50($527m). Upcoming Close Strikes : 155.00($1.34b Nov 20), 150.00{$1.3b Nov 20) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 99 Points

Fig 1 : USD/JPY Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

AUD: Asia-Pac: AUD/USD Drifts Lower As Risk-Off Sentiment Grows

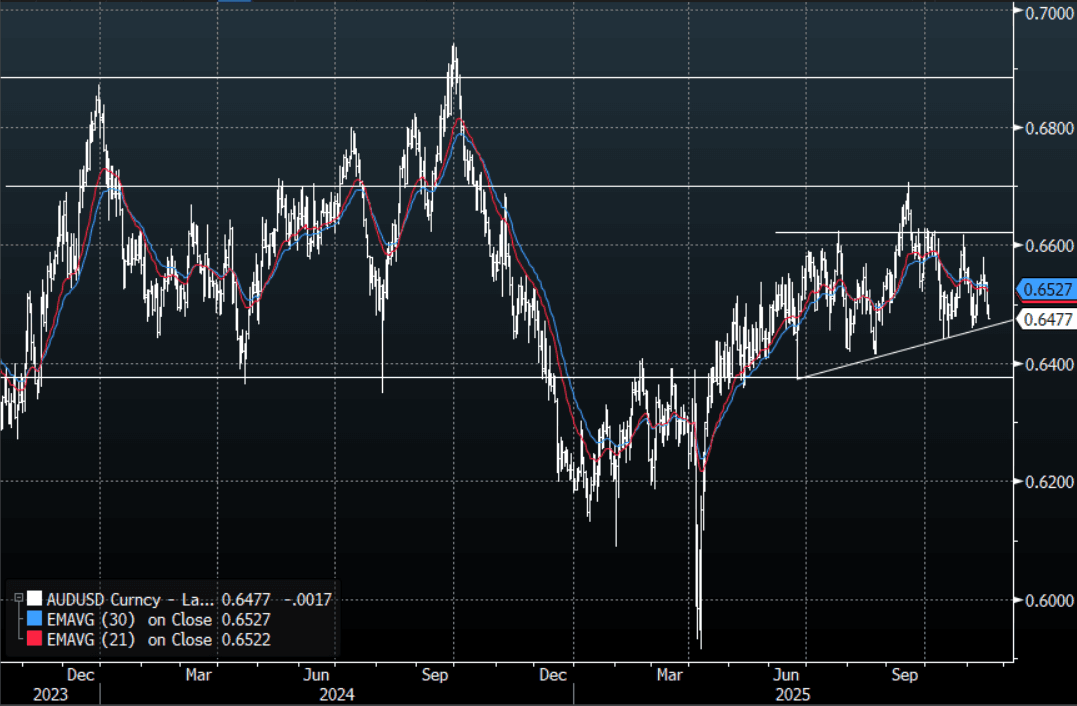

The AUD/USD has had a range today of 0.6477 - 0.6499 in the Asia- Pac session, it is currently trading around 0.6480, -0.25%. The AUD/USD has drifted lower in our session being led by the move lower in risk, driven predominantly by the collapse in Crypto. Bitcoin and Crypto continue to lead this leg lower as leverage is being squeezed, Bitcoin below the pivotal $90k area could add to the current market headwinds. The AUD/USD is testing below 0.6500 this morning, some good support back toward 0.6440-0.6460 which has been pretty solid the last couple of months, then 0.6350 below that. It would need this move lower in risk to accelerate and become something more significant to challenge down there I would think.

- MNI AU - RBA: 2-Way Risks, How They Develop Likely To Determine If Hold Prolonged. The November meeting minutes reiterated that the RBA’s central scenario is “in balance” with risks to both the downside and upside. How these risks will develop is likely to determine whether monetary policy stays on hold or rates are cut further and while it is “not yet possible to be confident” about which scenario will materialise, the Board will “remain cautious and data dependent”. With core inflation above target and ongoing signs of a recovery in demand, policy is likely to be on hold in December and into early 2026, depending on the data.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD913m), 0.6600 (AUD729m). Upcoming Close Strikes : 0.6550(AUD2.28b Nov 21) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 47 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NZD: Asia-Pac: NZD/USD - Back Under Pressure As Risk Extends Lower

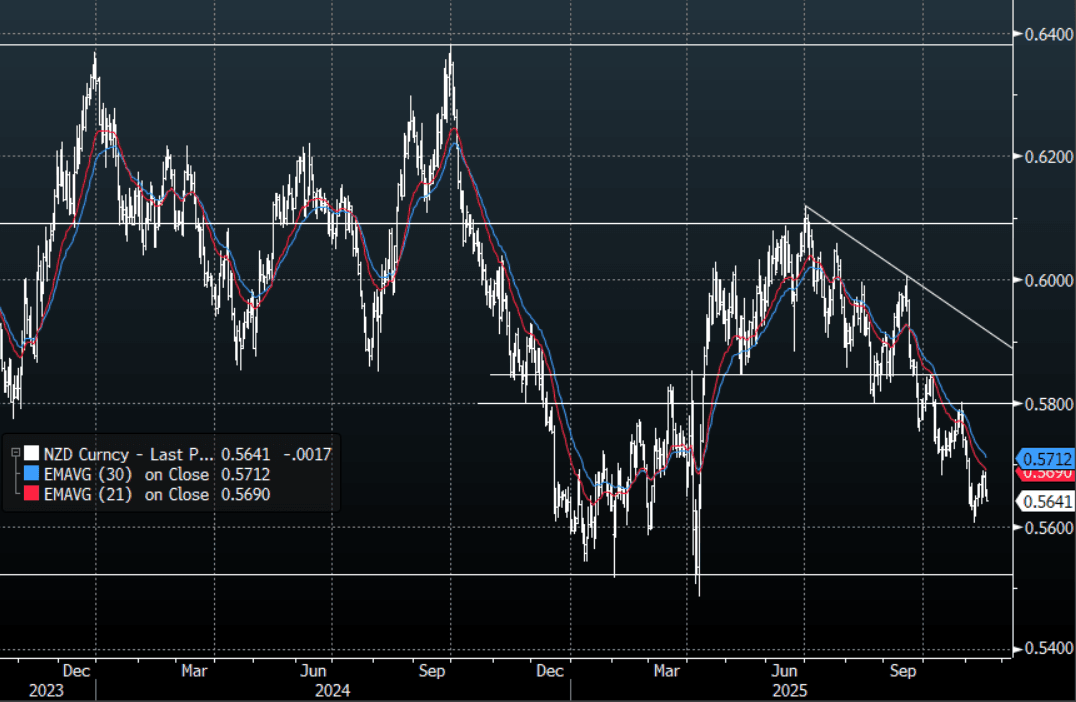

The NZD/USD had a range today of 0.5639 - 0.5661 in the Asia-Pac session, going into the London open trading around 0.5640, -0.30%. The NZD/USD has drifted lower in our session with risk continuing to trade under pressure. The NZD reaction lower was still rather underwhelming and continues to hint toward a market that is all the same way and therefore paring back some risk. Should this move lower in risk grow into something more than just a pullback then the NZD should once again come back under pressure though. On the day watch to see if the NZD stalls toward the 0.5665-80 area again looking for a move lower later.

- "RBNZ Business Survey Shows Lower Two-Year Inflation Expectation. Reserve Bank of New Zealand publishes Tara-ā-Umanga Business Expectations Survey, for 4q. Weighted mean 1-year ahead inflation expectation falls to 2.42% from 2.53% in 3q, 2-year declines to 2.39% from 2.64%" - BBG

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5480(NZD644m Nov 21), 0.5730(NZD434m Nov 19), 0.5835(NZD300m Nov19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 41 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: All Major Markets Down, As Risk Off Grows, Tech Hit Hardest

All the major indices are down in Asia Pac so far today, with tech sensitive plays the worst hit. Japan markets off over 2%, likewise Taiwan, while the South Korean Kospi is down around 3%. Focus remains on the crypto space, where Bitcoin is under 90k, which is fresh lows back to April of this year. Markets will be mindful of deleveraging if we see further downside and spill over to broader risk trends. US equity futures are off, Eminis down close to 0.60%, while Nasdaq futures sit down over 0.750%. Eminis are at levels last seen in mid Oct. The next downside target may be the 100-day EMA near 6586 (we were last around 6654)

- Japan markets are off over 3%, with the NKY 225 testing under 49000. This is an important support area in light of the recent step uptrend. USD/JPY is back under 155.00 amid the risk off mood. Japan is also looking to mend ties with China - via BBG: "Foreign Minister Toshimitsu Motegi told lawmakers on Tuesday that Tokyo has been working on multiple fronts to clarify Takaichi’s remarks, including sending a senior diplomat to Beijing this week. “Our stance is being conveyed clearly at various levels,” Motegi said.

- We also have the meeting later at 3:30pm local time between PM Takaichi and BoJ Governor Ueda.

- In Hong Kong the HSI is off around 1.5%, while the CSI 300 is down a more modest 0.22% at the lunch time break (as is typical for risk off days).

- The Taiex is down over 2%, while the Kospi has fallen by over 3%, continuing its high beta/vol trend of late. This puts the index back under the 4000 level. The other focus point for chip/AI related markets is Nvidia results on Wednesday. Tech is seen as susceptible to further risk off though as this is where we have seen strong outperformance so far in 2025.

- In South East Asia markets are weaker, we are down, but losses are generally more modest, and less than 1% at this stage. In Australia the ASX 200 is down 2%.

ASIA STOCKS: Tech Related Inflows Firm To Start The Week, But Will They Sustain?

Yesterday saw a return to positive offshore inflow momentum for both South Korea and Taiwan. However, it remains to be seen if these recovery trends continue. Overnight tech equity weakness continued in US markets with the SOX down a further 1.55%, while the MSCI IT lost 1.44%. The technical set up for both indices doesn't look favourable, as we await Nvidia earnings (due Wednesday). Both South Korea and Taiwan net outflows have been sizable in Nov to date (more than $6bn) and both markets are back to YTD outflows, see the table below.

- For South Korea so far today, the Kospi is tracking weaker. We were last off around 1.55%, which is close to session lows, but we are still above 4000 at this stage.

- Elsewhere, the see-saw pattern of Indian flows continued, leaving last week with a modest net outflow bias. Local equities are back close to recent highs, while Indian officials stated late on Monday the US trade deal is being close to concluded.

- In South East Asia, Indonesia inflows remain positive, with YTD outflows now at just -$2bn. Tomorrow we get the BI outcome, although the consensus doesn't expect a change.

- In the Philippines, yesterday's surge in local stocks (albeit from depressed levels) didn't induce any strong offshore buying inflows.

Table 1: Asian Markets Net Equity Flows

| Yesterday | Past 5 Trading Days | 2025 To Date | |

| South Korea (USDmn) | 326 | -940 | -2702 |

| Taiwan (USDmn) | 248 | -2420 | -1407 |

| India (USDmn)* | -525 | -668 | -16556 |

| Indonesia (USDmn) | 42 | 247 | -2046 |

| Thailand (USDmn) | 53 | -118 | -3207 |

| Malaysia (USDmn) | 4 | 105 | -4290 |

| Philippines (USDmn) | -3 | 0 | -673 |

| Total (USDmn) | 145 | -3795 | -30880 |

| * Data Up To Nov 14 |

Source: Bloomberg Finance L.P./MNI

GOLD: Weaker, Eyeing Sub $4000, Risk Off Doesn't Aid Sentiment

Gold is back close to $4010, off a further 0.90% so far today. the risk off evident in the crypto space and in equity markets has done little to aid gold safe haven related demand. Some offset is coming from a higher USD (albeit with mixed trends today, higher against higher beta plays, but safe havens, JPY and CHF are rising), as Fed easing expectations remain uncertain. A break under $4000 could bring the 50-day EMA support point into play, which comes in at $3927.5. Initial resistance is at $4264.7.

- FOMC members appear split between believing further easing is needed to restart the labour market and holding as inflation remains above target. The Fed’s Waller noted earlier today that the focus should be on jobs data and not inflation and that the fiscal position is not sustainable.

- US real 10yr yields remain elevated compared to recent history, last at 1.85% (recent lows were under 1.70%).

- Structural support for gold still appears evident from an asset allocation standpoint. Via BBG: "China added an estimated 15 tons of gold to its forex reserves in September as central banks accelerated their purchases of bullion after a seasonal summer lull, according to Goldman Sachs Group."

OIL: Crude Unwinds Week’s Gains As Excess Supply Worries Outweigh Geopolitics

Oil has unwound Monday’s gains during today’s APAC session on weaker risk appetite. WTI is down 0.8% to $59.50/bbl, close to the intraday low, and has traded below $60 over the day. Brent is 0.7% lower at $63.74, the day’s trough. While crude has trended lower over November, geopolitical risks have pushed back against market surplus concerns keeping it in a narrow range.

- Conflict is impacting fuel output in Russia and Sudan, while Iran’s redirection of a tanker in the Gulf of Oman into its own waters increases the risk to the significant shipments travelling through the area.

- The grace period before the introduction of sanctions on Russia’s Rosneft and Lukoil ends in a few days and it remains unclear how they will impact the oil majors’ exports and overseas assets driving the discount on Russia’s Urals benchmark to its highest since June 2023, according to Bloomberg. Meanwhile, Ukraine continues to strike ports and refineries.

- With the oversupply situation firmly in focus, inventory data will continue to be important. US industry-based stocks are released later on Tuesday with the official EIA data on Wednesday.

- Both OPEC and non-OPEC have increased output this year and Bank of Montreal is reporting that Canadian oil sands production reached a record in June which is set to rise to 6mbd by 2030.

- China’s product exports were strong in October with gasoline up 11.8% y/y and diesel +55.7% y/y. However YTD they were down 10.3% y/y and 22.7% y/y.

- Later the Fed’s Barr & Barkin, BoE’s Pill & Dhingra, and ECB’s Buch, Elderson, Machado & Tuominen speak. Delayed US IP and final August orders are released as well as ADP weekly employment estimates, November NY Fed services and NAHB housing.

ASIA FX: Equity Risk Off Drives USD Gains, USD/KRW Still Sub 1470, CNH/JPY Lower

North East Asia FX is weaker against the USD, weighed down by broader risk off and regional equity market losses. Weakness in the crypto space is spilling over into equity sentiment. Most notably the Kospi has fallen 3% so far today. Taiwan's Taiex is off around 2.5%. China markets are more resilient, but still down around 0.55% for the CSI 300.

- USD/CNH has continued to rise, putting some distance now with last week's lows near 7.0900. We were last close to 7.1150, near session highs and 20-day EMA resistance. CNH is outperforming higher beta plays, but has given up some ground versus the yen. The CNH/JPY cross got to fresh highs above 21.85 in the first part of trade, but now tracks under 21.80, as risk off benefits yen at the margin. The USD/CNY fix rose but remains close to recent lows.

- Spot USD/KRW is higher, but found selling resistance around the 1467.5 region. We were last back under 1465 level as risk appetite has stabilized somewhat (bitcoin back above 90k etc). Focus will be on whether we see increased supply in 1470/80 (or slightly higher) region, as the authorities look to improve supply/demand in the FX market. Earlier data showed a rise in household credit, firming the case for no change next week at BoK's policy announcement.

- Spot USD/TWD is up, maintaining the recent uptrend. We were last 31.22, against fresh highs back to early May of this year. Equity weakness is likely a factor in keeping this uptrend intact. The 1 month USD/TWD NDF has now fully retraced Friday's sell off, last at 31.15.

ASIA FX: USD/MYR Recovery Continues, USD/IDR Back Near Late Sep Highs

In South East Asia FX markets, it has been a similar theme for the most part in terms of USD gains. USD/MYR upside has been the standout, with ringgit continuing to unwind some of its recent outperformance. More modest losses have been evident for the likes of IDR, THB and PHP though. SGD FX is steady, bucking the firmer USD/Asia trend (lower USD/JPY levels are likely helping SGD FX).

- USD/MYR has risen around 0.60%, last near 4.1750, which is right around 20-day EMA resistance. The pair has corrected higher from oversold conditions, while offshore equity inflows have slowed, with recent global equity jitters probably driving some caution in this space. More firmer resistance in the pair may be around the 50-day EMA (4.1970) but a break above this level may see the market question the ringgit outperformance theme.

- USD/IDR is at fresh highs since late Sep, last near 16760/65. Broader risk off will be weighing, particularly given mostly positive offshore inflows into Indonesian stocks in Nov to date. Upside focus for the pair will rest at late Sep highs just under 16790.

- USD/PHP is back above 59.00, but tracking within recent ranges. Focus is on yesterday's cabinet change announcements, although broader financial market fallout has been contained so far.

- USD/THB has edged higher, last in the 32.45/50 region. USD/SGD is little changed, holding close to 1.3030.

SOUTH KOREA: Q3 Household Credit Remains Firm, BoK Waiting For Policy To Impact

Q3 credit data to households broadly maintained recent trends, albeit at a slightly slower pace compared to Q2. In level terms we rose to a fresh record high of KR1968.3trln. This should add to the bias for a steady hand at next week's BoK meeting. Recent comments from Governor Rhee noted that while the official bias is easing, the policy outlook is data dependent and will determine the next move in rates (which could also shift to a tightening bias at some stage). Rhee noted last week, via BBG: “But the magnitude and timing of the cut or even the change of direction will depend on the new data that we’ll see.”

- The data showed credit to households up 0.8%q/q, versus a 1.3% gain in Q2. In y//y terms, we were up 2.8%, versus 3.0% in Q3. Credit card debt continues to rise at a faster clip, but is a much smaller aggregate share (relative to loans).

- Via Yonhap, quoting the BoK: "Overall, the slower growth in household credit was largely attributable to government regulations. The additional measures announced in October to ease conditions in the property market are expected to help stabilize the pace of mortgage lending," he added."

- These measures were announced Oct 15, and designed to cool rising household debt, with additional areas in Seoul designated as speculative zones, while lending rules were also tightened (per Yonhap).

INDONESIA: MNI BI Preview-Nov 2025: BI Could Hold To Wait & See

- Download Full Preview Here

- Bank Indonesia (BI) announces its rates decision on Wednesday 19 November and could hold or ease as it has reasons for both. Bloomberg consensus is expecting it to be on hold with only 5/30 forecasting 25bp of easing but recently BI has gone against majority expectations.

- If BI holds in November, it is likely to reiterate that it is “monitoring the transmission effectiveness of accommodative monetary policy” and that it would like to see lower lending rates and an improvement in lending growth to support economic activity (it is forecasting 2026 loan growth of 8-12%).

- USDIDR has trended higher over November and BI has intervened to stall the move. However, at around 16762, it is up a percent since the 22 October decision.

- It could still cut in December, if the rupiah has stabilised and the Fed eases too.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 18/11/2025 | 1000/1100 | ECB Elderson at Banking Supervision Press Conference | ||

| 18/11/2025 | 1300/1300 | BOE Pill Fireside Chat on MonPol | ||

| 18/11/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 18/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index | |

| 18/11/2025 | 1415/0915 | *** | Industrial Production | |

| 18/11/2025 | 1500/1000 | ** | NAHB Home Builder Index | |

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1500/1000 | ** | Factory New Orders | |

| 18/11/2025 | 1530/1030 | Fed Governor Michael Barr | ||

| 18/11/2025 | 1600/1100 | Richmond Fed's Tom Barkin | ||

| 18/11/2025 | 1700/1700 | BOE Dhingra on Income Growth and Consumption | ||

| 18/11/2025 | 2100/1600 | ** | TICS | |

| 18/11/2025 | 2300/1800 | Dallas Fed's Lorie Logan | ||

| 19/11/2025 | 2350/0850 | * | Machinery orders | |

| 19/11/2025 | 0001/0001 | * | Brightmine pay deals for whole economy | |

| 19/11/2025 | 0030/1130 | *** | Quarterly wage price index | |

| 19/11/2025 | 0700/0700 | *** | Consumer Inflation Report (1dp) | |

| 19/11/2025 | 0700/0700 | *** | Producer Prices | |

| 19/11/2025 | 0700/0700 | *** | Consumer Inflation Report (2dp) | |

| 19/11/2025 | 0900/1000 | ** | EZ Current Account | |

| 19/11/2025 | 1000/1000 | ** | Gilt Outright Auction Result | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1000/1100 | *** | EZ HICP Final | |

| 19/11/2025 | 1200/0700 | ** | MBA Weekly Applications Index | |

| 19/11/2025 | 1330/0830 | ** | Trade Balance | |

| 19/11/2025 | 1330/0830 | ** | Trade Balance |