JGBS: Twist-Steepener, 2/30 YC Back Near Highs, PM/BOJ Meeting Due

Nov-18 05:03

JGB futures have clawed back to unchanged versus settlement levels.

- With the local calendar light, the domestic market, out to the futures-linked 7-year, has benefited from general global risk-off sentiment.

- "Japanese Prime Minister Sanae Takaichi is set to meet with Bank of Japan Governor Kazuo Ueda on Tuesday as she mulls support for an economy that shrank over the summer. The two will meet at 3:30 p.m. in Tokyo, according to the prime minister's office. - BBG

- Cash US tsys are 2-3bps richer in today's Asia-Pac session.

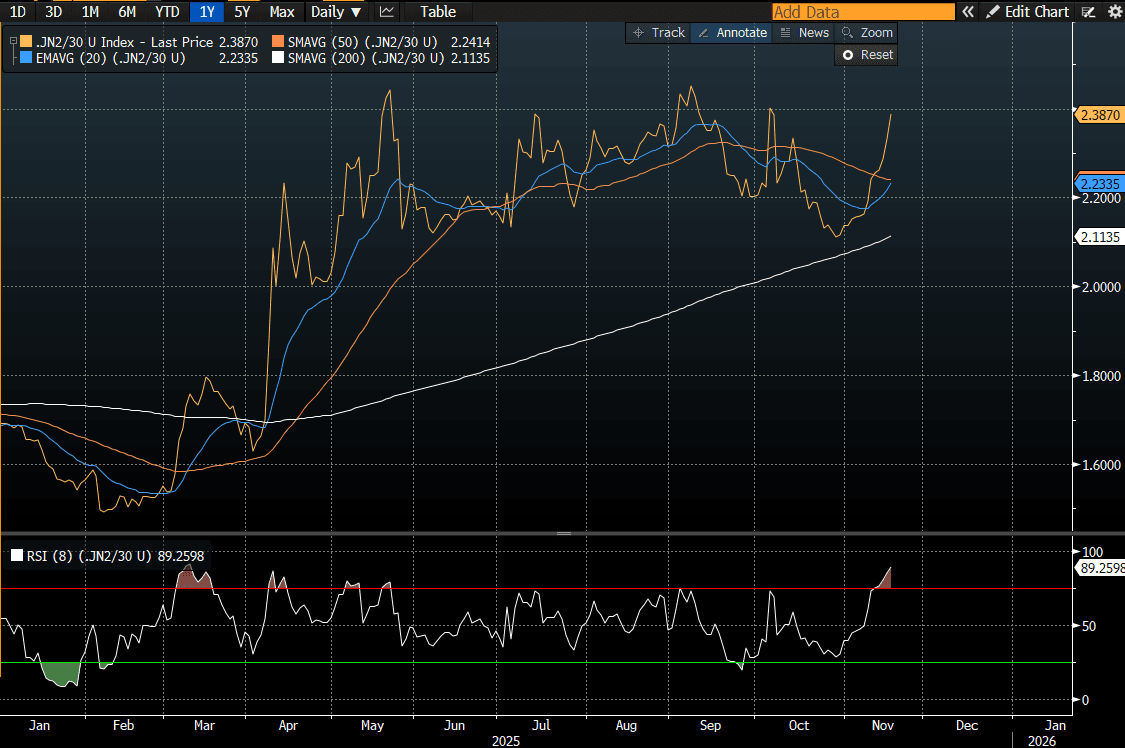

- JGBs have twist-steepened in today's session, with cash JGBs 1bp richer to 7bps cheaper across benchmarks. The benchmark 20-year yield is 3.6bps higher at 2.786% after setting a fresh cycle high of 2.816% ahead of tomorrow's supply.

- "A "sell Japan" trend is likely to persist across equities, bonds and the yen unless Tokyo de-escalates its ongoing diplomatic spat with China, according to Tomo Kinoshita, global market strategist at Invesco." – BBG

- Today’s move also places the 2/30 curve within striking distance of its recent high. (see chart)

- Swaps have twist-steepened, with rates 1bp lower to 4bps higher.

- Tomorrow, the local calendar will see Trade Balance and Core Machine Orders data.

Source: Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LOOK AHEAD: US Week Ahead Headlined By Delayed CPI Report On Friday

Oct-17 20:51

- The September US CPI report will be released on Friday, delayed amidst the government shutdown but with the BLS making a special exception on social security payment considerations.

- Bloomberg consensus looks for headline CPI inflation at a rounded 0.4% M/M after 0.38% back in August and for Y/Y inflation to firm two tenths to 3.1% for what would be its highest since May 2024.

- Core inflation is seen at a rounded 0.3% M/M after 0.35% in August (exceeding the median unrounded estimate of 0.31%) and 0.32% in July. It’s expected to see core CPI inflation hold at 3.1% Y/Y having in August increased to its highest since February.

- Core details should see focus on both goods and services angles: underlying goods inflation has clearly firmed in recent months on tariff pressures although the median increase has currently seen a peak back in June, whilst services will be watched for any spillover after some strong recent non-housing readings.

- The report will come within the FOMC blackout period ahead of the Oct 28-29 decision, with a 25bp cut fully priced and likely needing a large surprise to alter this.

- As for broader inflation details, Fed Chair Powell this week confusingly suggested that we will have the September PPI report but the BLS had previously said “No other releases will be rescheduled or produced until the resumption of regular government services”.

US DATA: Latest Jobless Claims Estimates During The Shutdown

Oct-17 20:30

As noted earlier, MNI estimates initial jobless claims at a seasonally adjusted 218k in the week to Oct 11 and continuing claims at a seasonally adjusted 1929k in the week to Oct 4.

- To give a better idea of sensitivity around these estimates, which rely on estimates for some missing states, we note the below analyst estimates:

- Goldman Sachs have a central estimate of 217k for initial claims in a range of 211-225k, whilst they see continuing claims at 1917k in a range of 1885-1930k.

- JPMorgan meanwhile also see 217k for initial claims whilst they see continuing claims as having held constant at 1927k.

NATGAS: Venture Global in Talks with Ukraine for more LNG Deliveries, Reuters

Oct-17 20:28

Ukraine is seeking more cargoes from Venture’s Plaquemines facility as the embattled nation approaches the winter heating season, according to Reuters sources

- Venture is in talks with Ukraine’s DTEK to procure more LNG cargoes after a year of gas infrastructure attacks by the Russians.

- Venture Global CEO Michael Sabel met with President Volodymyr Zelenskiy on Thursday October 16.

- DTEK signed an agreement in 2024 for an undisclosed amount of LNG from the facility, as well as 2 mtpa from Calcasieu Pass Phase 2 currently under construction.

- Plaquemines currently has spare capacity to deliver more cargoes to Ukraine on the spot market, per Reuters.

- Plaquemines now sends out the second highest LNG volume in the US, with feedgas demand averaging 3.45 bcf/d according to MNI figures.