MNI EUROPEAN MARKETS ANALYSIS: Japan GDP Falls, Solid Detail

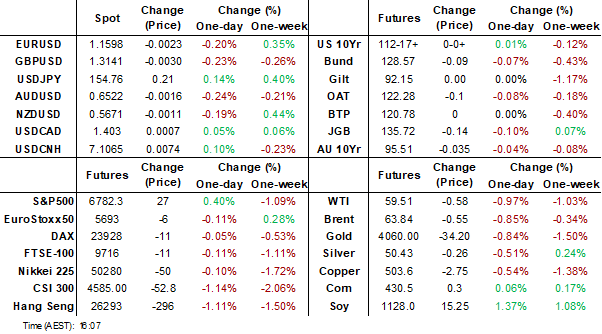

- Japan Q3 GDP was negative q/q, but above market forecasts thanks to resilient business spending. Cash JGBs are flat to 4.5bps cheaper across benchmarks, with a steepening bias. Weekend media reports were focused on the upcoming economic stimulus.

- The USD is mostly higher, along with broader risk gauges like US equity futures and Bitcoin (although AUD and NZD are down). USD/Asia pairs are higher as well. Gold and oil are off highs from late last week.

- Looking ahead, we have BoE and Fed central bank speak, while Canadian CPI prints.

MARKETS

US TSYS: Little Changed, Focus On Upcoming Data & Nvidia Results

TYZ5 is trading at 112-17+, +0-00+ from closing levels in today's Asia-Pac session.

- Cash US tsys are 1bp richer to 1bp cheaper, with a steepening bias, in today's Asia-Pac session. On Friday, US tsys finished showing a modest bear-steeper, with benchmark yields 1-4bps higher.

- US equity futures are slightly firmer in today's Asia session. The S&P looked to be rolling over again on Friday night, down almost 1.5% before it found solid demand during the N/Y session and pared back all the day's losses.

- The market will be looking toward the release of some US data this week (September's delayed nonfarm payrolls report for next Thursday) to get a gauge on things and also heavily focused on the upcoming Nvidia results, which will heavily impact the direction of markets this week.

- Friday's Fed commentary (with the usual exception of Gov Miran calling for further easing in December) was roundly hawkish, with Dallas's Logan and KC's Schmid reiterating their opposition to a December rate cut, largely out of concern over entrenched inflation. A December cut remained around 50/50 priced.

- Along with the newly-rescheduled data, this week's calendar includes the October FOMC minutes (we're watching for colour on the debate over whether to ease any further) and flash November PMI data.

JGBS: Bear-Steepener As Market Focuses On Econ Stimulus, 20YY Highest Since '99

JGB futures are weaker and at session lows, -17 compared to settlement levels, after the release of Q3 GDP data.

- Q3 GDP (preliminary) in Japan was negative q/q, but not as much as the market forecast, thanks to upbeat business spending (+1.0%q/q versus -0.1% forecast). This was the first GDP decline since Q1 2024, but the detail paints a resilient underlying economic backdrop and comes ahead of fresh fiscal stimulus from the new Takaichi government.

- The data will likely bolster the Takaichi administration's conviction that aggressive fiscal spending is needed to shore up the economy, with the premier expected to unveil her first economic package as soon as this week. The Finance Ministry is preparing an economic package of roughly Y17tn, according to a Nikkei report published Saturday.

- Cash US tsys are flat to 1bp richer, with a steepening bias, in today's Asia-Pac session.

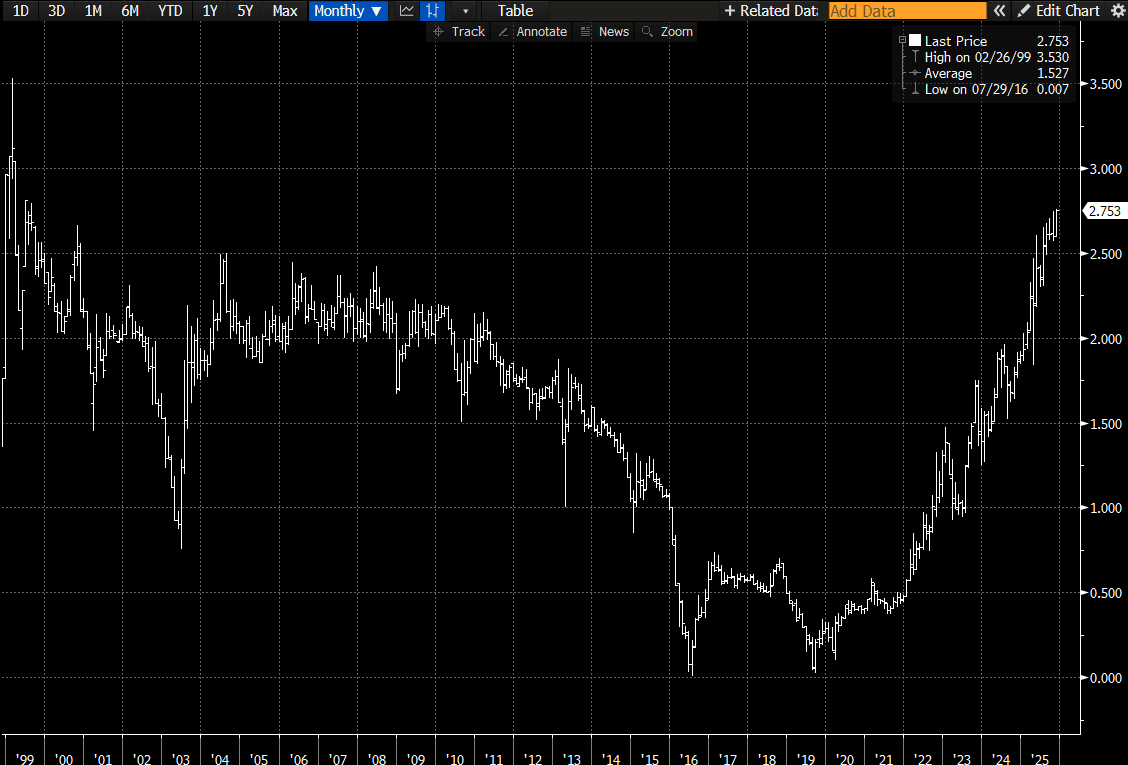

- Cash JGBs are flat to 4.5bps cheaper across benchmarks, with a steepening bias. The benchmark 10-year yield is 2.3bps higher at 1.733%, a fresh cycle high.

- Meanwhile, the yield on 40-year climbed as high as 3.603%, while the 20-year yield reached 2.756%, the highest since 1999. (see chart)

- Swap rates are flat to 5bps higher.

- Tomorrow, the local calendar will be empty.

Source: Bloomberg Finance LP

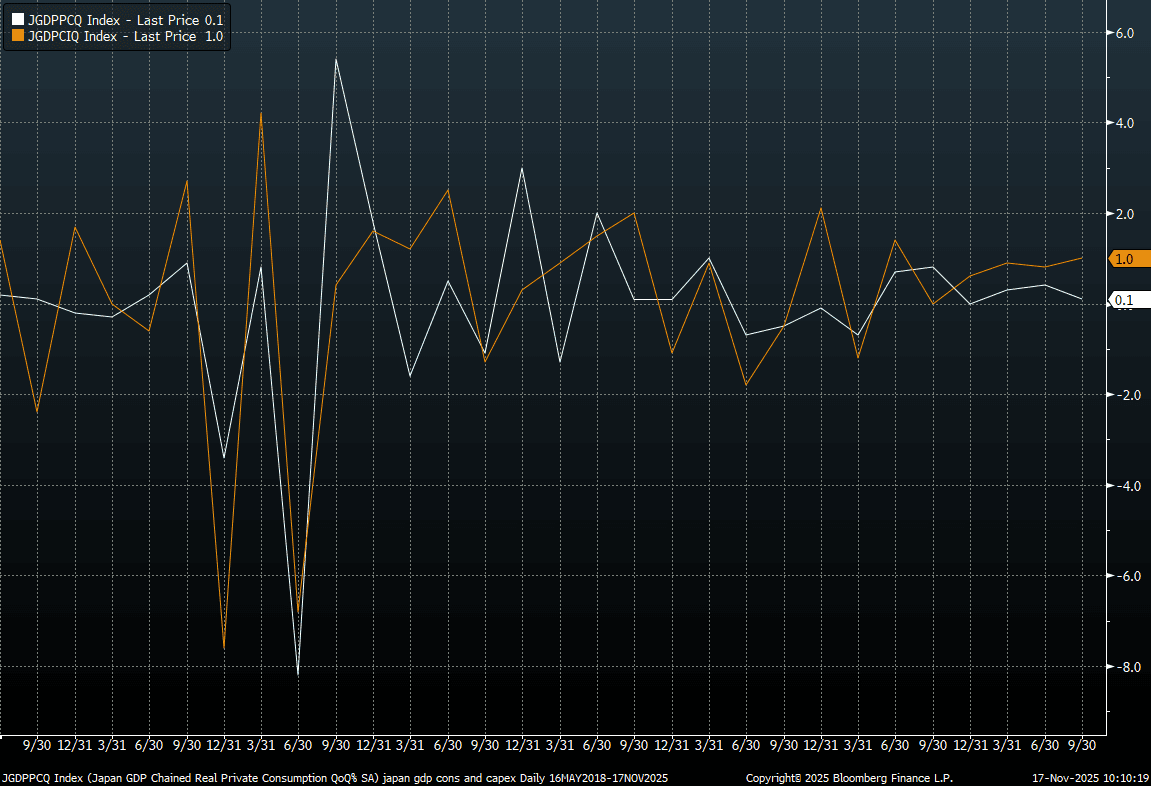

JAPAN DATA: Q3 GDP Contracts, But Resilient Detail, Particularly Business Spend

Q3 GDP (preliminary) in Japan was negative q/q, but not as much as the market forecast, thanks to upbeat business spending (+1.0%q/q versus -0.1% forecast). This was the first GDP decline since Q1 2024, but the detail paints a resilient underlying economic backdrop and comes ahead of fresh fiscal stimulus from the new Takaichi government. Today's GDP data should add some confidence, at the margins, the BOJ has in the GDP backdrop (particularly in terms of the drivers). We await Ueda's early Dec speech for details around hike timing.

- The q/q outcome for GDP was -0.4% against a -0.6% forecast. Note Q2 growth was revised to +0.6% from 0.5% originally reported. In annualized terms, growth -1.8%q/q, versus -2.4% forecast and a revised 2.3% gain in Q2. Note business s[ending was also revised up in Q2 to 0.8% from 0.6%q/q. Other components of GDP were close to forecasts, consumption up 0.1%q/q, while inventories were a -0.2ppt drag and net exports also trimmed -0.2ppt off growth.

- Whilst this is just a preliminary GDP print, the detail should be welcomed by the authorities. The q/q trends for private consumption (the white line) and business spending are plotted in the chart below.

- The resilience to strength in business spending, in particular, will be welcome. Via our Tokyo policy team: Private consumption and capital investment, the major components of the economy, are likely to firm in or after the fourth quarter, the official said. Private consumption, particularly non-durable goods, was hit by high prices and scorching weather in Q3, but is undergoing a moderate recovery supported by improving consumer sentiment, the official added.

- This also comes ahead of fresh fiscal stimulus, via BBG: "The Finance Ministry plans an economic package worth about ¥17 trillion ($110 billion), the Nikkei reported on Saturday, without identifying its sources. The supplementary budget to fund the spending is expected to reach about ¥14 trillion, exceeding last year’s ¥13.9 trillion compiled under former Prime Minister Shigeru Ishiba, the report said." - BBG

Fig 1: Japan GDP Components, Q/Q (Consumption (White Line) & Business Spending (Orange Line)

Source: Bloomberg Finance L.P./MNI

AUSSIE BONDS: Modestly Cheaper Ahead Of Tomorrow's RBA Minutes & Wed's WPI

ACGBs (YM -2.5 & XM -4.0) are weaker on a data-light session.

- Cash ACGBs are 2-4bps cheaper with the AU-US 10-year yield differential at +33bps.

- The bills strip is -2 to -3 across contracts.

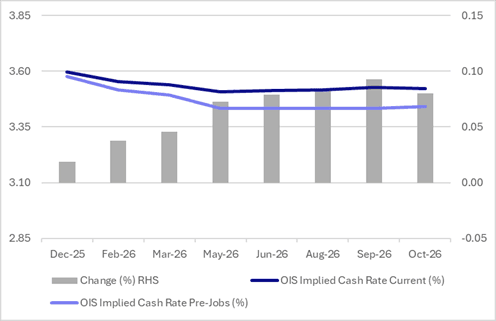

- Interest rate expectations in Australia out to mid-2026 have firmed just shy of 10bps over the past week. The key driver of this move was October’s employment data. The labour market normalised, with unemployment returning to 4.3% after September’s 4.5% spike. OIS pricing implies just a 1% probability of a 25bp December cut (9% pre-data), with cumulative easing of 9bps priced by mid-2026 (down from 17bps pre-data). (see chart)

- Even still, as previously noted, markets may still be overestimating the likelihood of further cuts, given that rising annual inflation has historically ended RBA easing cycles.

- Tomorrow, the local calendar will see RBA Minutes of the Nov. Policy Meeting ahead of the Wage Price Index on Wednesday.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond on Tuesday, A$1000mn of the 2.75% 21 June 2035 bond on Wednesday and A$700mn of the 1.25% 21 May 2032 bond on Friday.

Figure 1: RBA-Dated OIS – Current Vs. Pre-Jobs

Source: Bloomberg Finance LP / MNI

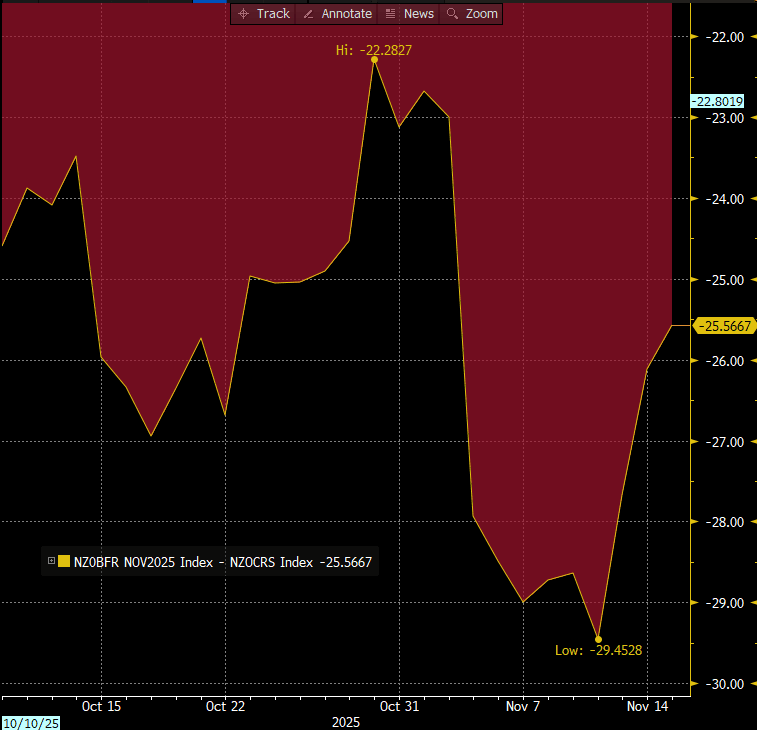

BONDS: NZGBS: Cheaper But Best In $-Bloc, Nov Cut Hopes Stable

NZGBs closed showing a modest bear-steepener, with benchmark yields 1-2bps higher.

- Today’s move leaves the 2/10 yield curve around cycle highs, the highest since 2021.

- NZGBs outperformed their $-bloc counterparts, with the NZ-US and NZ-AU 10-year yield differentials 1-2bps tighter.

- “On average, respondents believed there was a 38% chance of finding a new job, down from 41.2% in 3q and the lowest since the survey began in 1q 2022.” - RBNZ via BBG

- “October selected prices update presents no obstacles to another rate cut from the RBNZ at next week's policy meeting, said Westpac in a report on Monday. Westpac has revised its forecast for December quarter inflation to +0.3% and +2.8% for the year to December, both down 0.1 percentage points from the bank's earlier forecast.” - BBG

- Swap rates closed 2-3bps higher.

- RBNZ dated OIS pricing closed little changed across meetings. 25bps of easing is priced for November, with a cumulative 34bps by February 2026. Pricing has been relatively stable over the past month. (see chart)

- Tomorrow, the local calendar will see Non-Resident Bond Holdings.

Bloomberg Finance LP

NEW ZEALAND: Oct Services PMI Up But Still Sub 50, Pointing To Tepid Recovery

The Oct services PMI (via BNZ and Business NZ) edged up to 48.7 from 48.3 in Sep. We look to be on a steady improvement trend, but from depressed levels and the index hasn't been above the 50.0 expansion/contraction point since early 2024. The sub indices mostly ticked higher, but also remain under 50.0. Activity was 48.9, versus 48.0 prior, employment up to 48.8, versus 47.9 in Sep. The employment index eased back to 49.5 from 49.7 prior.

- The outcome doesn't point a sharp turn higher in early Q4 economic momentum. BNZ noted (via BBG): "Sector continues to struggle for forward momentum with the sub-component gauges all below long-term averages and making for ”dreary reading”.

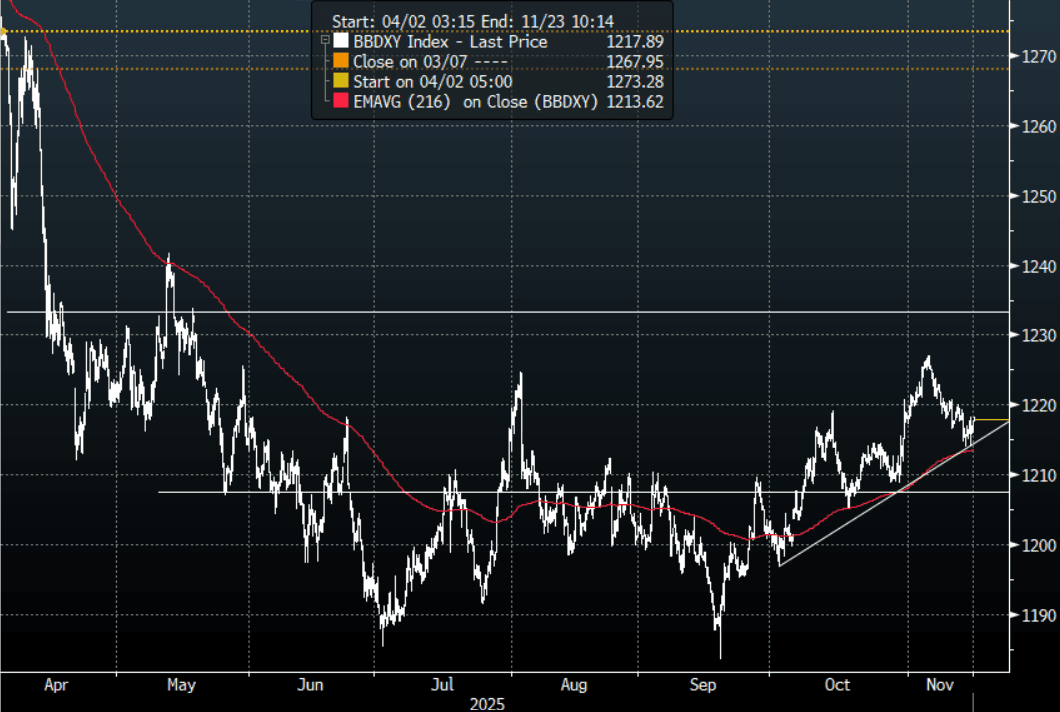

FOREX: Asia-Pac USD: BBDXY Moves Higher, Support Building Around 1213

The BBDXY has had a range today of 1216.04 - 1218.27 in the Asia-Pac session; it is currently trading around 1218, +0.15%. The USD has drifted higher in our session thanks to demand across USD/Asia, this might be differentiated when London comes in with risk turning higher after opening under early pressure. The USD again found support on Friday in the 1210-1215 area and is looking to build a base from which to move higher. I expect we do some more work around these levels but I would be looking for signs of a base forming from which to potentially move higher again. Short-term the 1221-1222 area remains the pivot on the topside and we would need a move back above there to build for a retest of the 1230-35 area.

- EUR/USD - Asian range 1.1597 - 1.1625, Asia is currently trading 1.1600. The pair stalled and moved lower after finding some decent resistance toward the 1.1650-1.1700 area. This has been the pivot within the larger 1.1400-1.1900 range over the past few months.

- GBP/USD - Asian range 1.3142 - 1.3176, Asia is currently dealing around 1.3145. I continue to favor fading rallies, as GBP looks to have put in a medium term top. A sustained move back below 1.3080-1.3100 support would see the momentum lower reinstated and focus turn back toward the 1.3000 area. Suspect rallies back toward the 1.3250-1.3300 will be sold into if we see a bounce.

- Cross asset : SPX +0.40%, Gold $4080, US 10-Year 4.144%, BBDXY 1216, Crude Oil $59.57

- Data/Events : France Bloomberg Nov. France Economic Survey, EZ Bloomberg Nov. Eurozone Economic Survey/European Commission Publishes Autumn Economic Forecasts, Spain Bloomberg Nov. Spain Economic Survey, Italy Bloomberg Nov. Italy Economic Survey, Germany Bloomberg Nov. Germany Economic Survey/CPI

Fig 1: BBDXY Spot 4H Chart

Source: MNI - Market News/Bloomberg Finance L.P

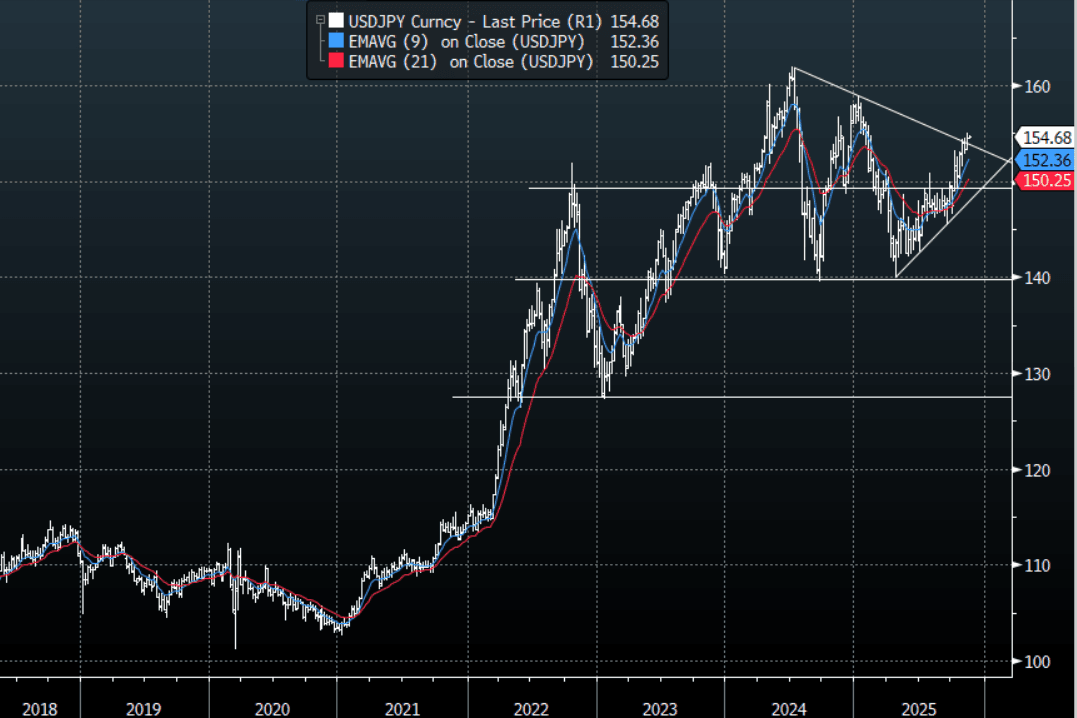

JPY: Asia-Pac: USD/JPY Looking To Mount Another Challenge Of 155.00

The USD/JPY range today has been 154.42 - 154.79 in the Asia-Pac session, it is currently trading around 154.70, +0.10%. The pair has traded better bid together with USD/Asia across the board in the Asian session. Usd/Jpy seems to remain well supported on dips as the market remains wary of the new leadership policies and a US December rate cut comes into doubt. The price action points to a renewed challenge to the resistance toward 155.00, a sustained break above here and it could start to pick up momentum to the topside again potentially targeting another push toward 160.

- "Japan Plans Bigger Extra Budget This Fiscal Year”: Media Reports. "The Finance Ministry plans an economic package worth about ¥17 trillion ($110 billion), the Nikkei reported on Saturday, without identifying its sources. The supplementary budget to fund the spending is expected to reach about ¥14 trillion, exceeding last year’s ¥13.9 trillion compiled under former Prime Minister Shigeru Ishiba, the report said." - BBG

- "JAPAN ECONOMY MINISTER KIUCHI ON JULY-SEPT GDP: NO CHANGE TO OUR VIEW ECONOMY GRADUALLY RECOVERING, WILL COMPILE ECONOMIC STIMULUS PLAN SWIFTLY" RTRS

- Options : Close significant option expiries for NY cut, based on DTCC data: 155.00($1.39b), 154.70($400m). Upcoming Close Strikes : 155.00($1.31b Nov 20), 150.00{$1.3b Nov 20) - BBG.

- The USD/JPY Average True Range(ATR) for the last 10 Trading days: 85 Points

Fig 1 : USD/JPY Spot Weekly Chart

Source: MNI - Market News/Bloomberg Finance L.P

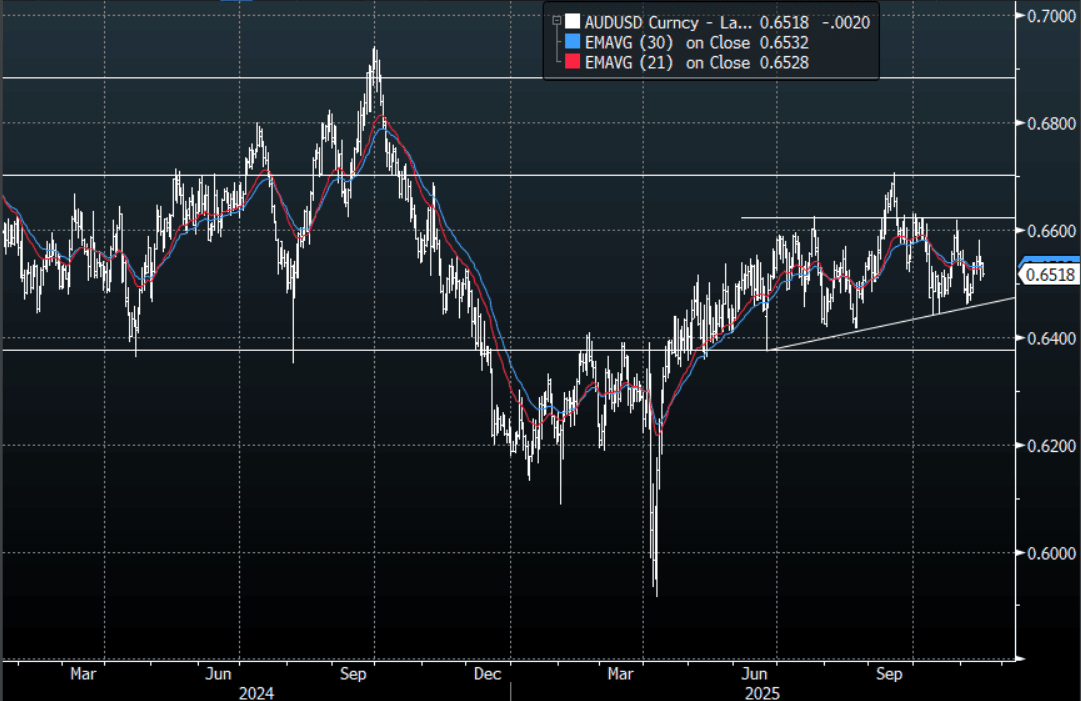

AUD: Asia-Pac: AUD/USD Drifts Lower As USD/ASIA Extends Higher

The AUD/USD has had a range today of 0.6512 - 0.6537 in the Asia- Pac session, it is currently trading around 0.6520, -0.30%. The AUD/USD has drifted lower in our session being led by the move higher in USD/Asia. The AUD/USD tested the 0.6500 area on Friday but bounced into the weekend with US stocks. The AUD/USD looks a little lost and is chopping around in a clearly defined range. Bitcoin gapped lower on the open but has since recouped all its losses moving back above $95k, the moves in crypto have recently been leading the market but for this to get legs it would need to break below the pivotal $90k area to add to the current market malaise. The AUD/USD has basically traded 0.6350-0.6650 since April this year and we will need a catalyst for this to break, otherwise it looks like more of the same unfortunately.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6525(AUD394m). Upcoming Close Strikes : 0.6400(AUD913m Nov 18), 0.6550(AUD674m Nov 20), 0.6600 (AUD679m Nov 18) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 39 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

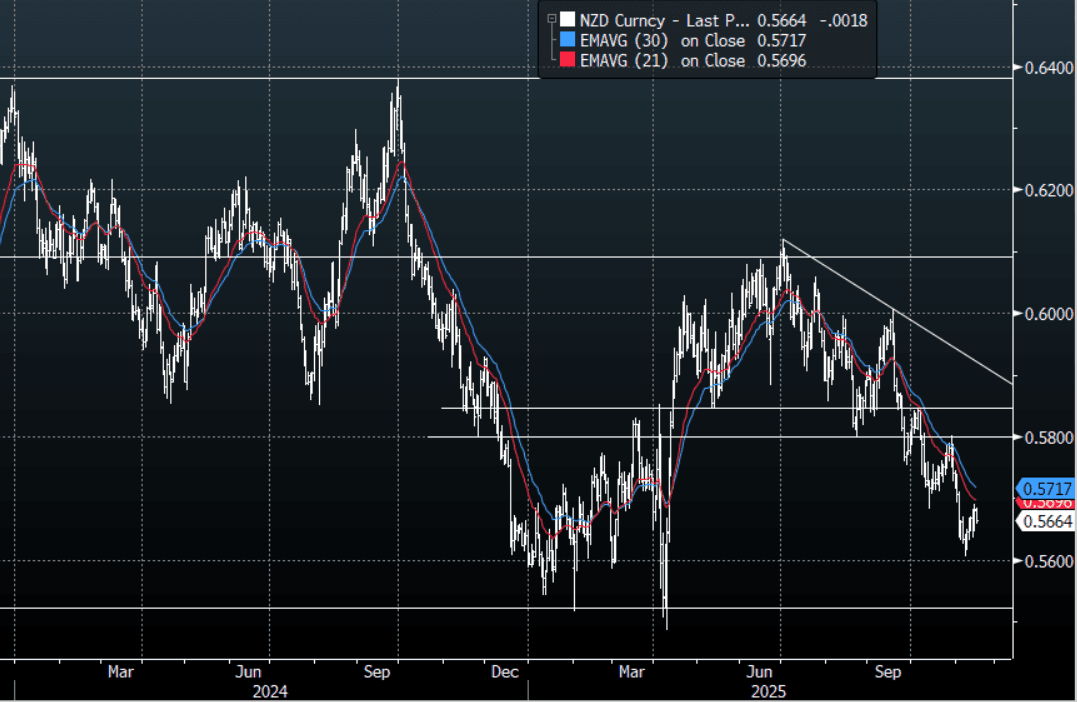

NZD: Asia-Pac: NZD/USD Drifts Back Toward 0.5650 Area

The NZD/USD had a range today of 0.5658 - 0.5681 in the Asia-Pac session, going into the London open trading around 0.5665, -0.30%. The NZD/USD has drifted lower in our session being led by the move higher in USD/Asia. The NZD is one of those currencies in which positioning can become an issue because of the size of the market so when it grinds higher like it did at the back of last week while risk turned lower it is price action worth noting. The place to fade NZD again is closer toward 0.5800 should we see that area again.

- Bloomberg reports: “Nomura Likes Long NZD/USD on Expectation RBNZ Will Hold Rates. The Reserve Bank of New Zealand will refrain from lowering borrowing costs at its meeting on Nov. 26, even though the market is pricing in a reduction, according to Nomura strategists. “The market has been pricing in too aggressive an easing path for the RBNZ,” they wrote in a Friday note. “The RBNZ has hinted that it sees the activity outlook as having bottomed and that prior easing will start to have a more positive impact on economic momentum.”

- MNI AU - Oct Services PMI Up But Still Sub 50, Pointing To Tepid Recovery: The Oct services PMI (via BNZ and Business NZ) edged up to 48.7 from 48.3 in Sep. We look to be on a steady improvement trend, but from depressed levels and the index hasn't been above the 50.0 expansion/contraction point since early 2024. The sub indices mostly ticked higher, but also remained under 50.0. Activity was 48.9, versus 48.0 prior, employment up to 48.8, versus 47.9 in Sep. The employment index eased back to 49.5 from 49.7 prior. The outcome doesn't point to a sharp turn higher in early Q4 economic momentum. BNZ noted (via BBG): "Sector continues to struggle for forward momentum with the sub-component gauges all below long-term averages and making for "dreary reading".

- Options : Closest significant option expiries for NY cut, based on DTCC data: none. Upcoming Close Strikes : 0.5675(NZD300m Nov 20), 0.5730(NZD434m Nov 19), 0.5835(NZD300m Nov19) - BBG

- The NZD/USD Average True Range for the last 10 Trading days: 35 Points

Fig 1: NZD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

ASIA STOCKS: Mixed Trends, Japan Down On China Concerns, Philippines Rebounds

Asia Pac stocks are mixed so far in Monday trade. Japan and China stocks sit weaker, while South Korea and Taiwan are higher. In South East Asia, the Philippines is the standout up over 3% (after making fresh multi year lows in recent dealings). US equity futures are tracking higher, led by Nasdaq futures, up close to 0.70% (Eminis are around +0.45% firmer). Focus is on crypto for broader risk trends, with Bitcoin up +1.65% so far today and likely aiding the US equity futures moves.

- Japan stocks are down modestly, the NKY off around 0.35%, while the Topix is off by 0.55% at the time of writing. The NKY is still above 50k at this stage. Near term focus is on China-Japan tensions. This is weighing on tourism and retail related stocks, which benefit from China visitors. Via BBG: "Yuyuantantian, a social media account linked to China’s state broadcaster and frequently used to signal official policy, published a commentary this weekend warning that Beijing “has made full preparations for substantive retaliation.” This comes after new Japan PM Takaichi made comments regarding Taiwan recently. Q3 GDP in Japan printed above expectations, but still fell in the quarter. The underlying resilience of business spending will be welcome though.

- Hong Kong's market is softer, the HSI down 0.80%, while HSTECH is down 1.2%, and looking poorer from a technical standpoint. The CSI 300 on the Mainland is off close to 0.70%.

- South Korea's Kospi is up over 1.6%, with dips supported near 4000. The Taiex is up around 0.60%. Last Friday saw close to $2bn in outflows from both markets by offshore investors. Today's better risk tone in US equity futures may be helping at the margin.

- The Philippines bourse is up a little over 3%, putting the index back to 5750/55. On Friday the index did make fresh lows back to 2020, so may be seeing some dip buyers emerge. Domestic fundamentals remain focused on fallout from the corruption scandal. From the weekend and via BBG: " More than half a million people took part in a rally organized by an influential church in Manila, calling for accountability in the Philippine government over a widening corruption scandal."

OIL: Benchmarks Down, Trump Ok With Sanctions On Russian Trading Partners

Oil benchmarks sit off recent highs, Brent last around $63.85/bbl, unable to breach above the $65 level from late last week. So far we are down around 0.85% versus end Friday levels. WTI was last close to $59.50/55/bb, off by a similar amount (with Friday highs at $60.65/bbl). BBG notes signs of a resumption in supply from a key Russian port, (which was attacked by Ukraine last week) has been a factor in downside pressure today.

- Trump also spoke to reporters late US time on Sunday, noting he would support Senate legislation that targeted countries that were buying oil from Russia. Via BBG: "President Donald Trump said proposed Senate legislation to sanction countries conducting business with Russia would be “okay with me”."

- Broader surplus concerns still keep downside risks in play for oil. For WTI, from a technical standpoint, a continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low. Clearance of this level would confirm a resumption of the downtrend. Note that it is still possible a bullish corrective cycle remains in play. Resistance to watch is $62.59, the Oct 24 high. Clearance of this hurdle would signal scope for a stronger correction.

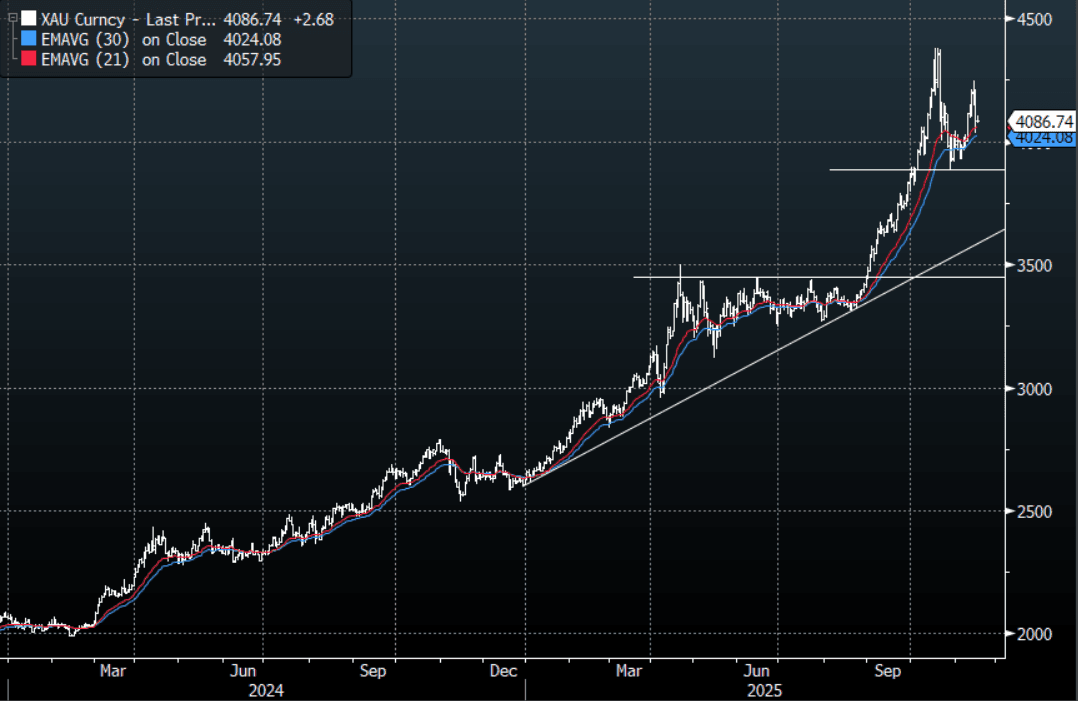

Gold - Drops Back, Support Seen Back Toward The $$3,900-$4,000 Area

The range Friday night for gold was $4,032.31/oz - $4,186.98/oz, Asia is currently trading around $4,090/oz, +0.15%. Gold slipped lower on Friday as the market looked toward eventually having a look at some US data starting this week and the implications of a Fed that seems to be pushing back on a December rate cut for the moment. Gold has technically put in a lower high now around the $4,250/oz area but strong support is seen back toward the $3,900/oz area. The market is trying to form a base from which to test higher again, while the $3900-$4000 area continues to hold dips should continue to be supported.

- Otavio Costa of Crescat Capital reiterated he believes more cuts in the US to come on X, “The Cass Freight index is now back to levels last seen during the pandemic. Unlike the labor data, this can’t be spun as an AI-displacement narrative. It’s a clear sign that economic activity is deteriorating sharply. Major rate cuts are still ahead of us, in my view.”

Fig 1 : Gold Daily Chart

Source: MNI - Market News/Bloomberg

ASIA FX: USD/TWD NDFs Rebound Strongly, USD/CNH Pushing Towards 7.1100

In North East Asia, the USD is firmer, with USD/KRW a notable riser, with USD/TWD NDFs have surged, recouped a good proportion of Friday's losses. USD/CNH is tracking towards a 7.1100 test. Broader USD trends are higher, particularly against higher beta plays, while regional equity market sentiment is mixed. Doubts over whether the Fed will ease in Dec is likely lending some USD support, although Tsy yields are down a touch so far today.

- USD/CNH is drifting higher, last around 7.1060. The pair tried late last week on multiply occasions to test under 7.0900 but couldn't, which may signify a short term base. Equally, we still expect upticks to be sold (USD/CNY fixing another fresh low for this year today), with the 50-day EMA back around 7.1275.

- Spot USD/KRW is probing higher, but has found some selling interest above 1460 so far today. Recent support was evident sub 1450, with Friday seeing benefit from the official rhetoric around stabilizing FX supply/demand imbalance, while later on the sharp move lower in USD/TWD NDFs likely saw spill over to the won as well. We expect any up moves in USD/KRW into the 1470/80 region to likely draw selling interest.

- Spot USD/TWD dipped at the open but was supported ahead of 31.00 (lows just under 31.04). We have since recovered to 31.18, which is fresh highs back to May of this year. Friday's announced agreement between the Taiwan central bank and the US Treasury - pledged to avoid manipulating exchange rates and disclose FX intervention and - importantly - prevent "public investment vehicles such as pension funds" from investing abroad for the purposes of targeting the FX rates.

- The market may have been fearful of a repeat of the late April/May sell off in the pair, as local investors increased FX hedges on overseas assets. This hasn't proven to be the case so far and Taiwan has seen to $10bn in offshore outflows in the past trading month from local equities.

- 1 month USD/TWD implied vol spiked towards 10% in the first part of trade, but is now back under 9%. The 1 month USD/TWD NDF is back close to 31.00 (after getting near 30.30 on Friday). We are up +1.5% so far today.

ASIA FX: MYR Corrects From Overbought Conditions, THB Ignores Softer GDP

In South East Asia FX, the trend has been towards a firmer USD. Notably MYR has given some of its recent outperformance. In India, the rupee is slightly firmer, but USD/INR remains close to record highs.

- USD/MYR is back near 4.1500, with the RSI (14) correcting from recent oversold conditions (reading back to 34). Recent lows in USD/MYR rest at 4.1217. Upside focus may rest around the 20-day EMA (near 4.1740), but more importance resistance will be at the 50-day EMA (just under 4.2000).

- USD/THB remains within recent ranges, the pair last near 32.42. Earlier we had weaker than expected Q3 GDP, which should keep BoT with an easing bias. Moves towards 32.25/30 may draw buying interest, but equally we haven't been able to sustain +32.50 levels in recent weeks.

- USD/PHP is holding above 59.00, but off earlier highs of 59.185. Local equities are surging, comfortably up over 3%. However, this followed a multi year low in terms of Friday's close, as the corruption scandal continues to cast a shadow over the domestic outlook (with more protests over the weekend).

- Spot USD/INR is near 88.55/60, so away from recent highs near 88.80. Lower oil and some headlines around India completing its first structured contract for US LPG (via RTRS), is likely helping at the margin. Intervention risks will continue to lurk as well around the 88.80 region.

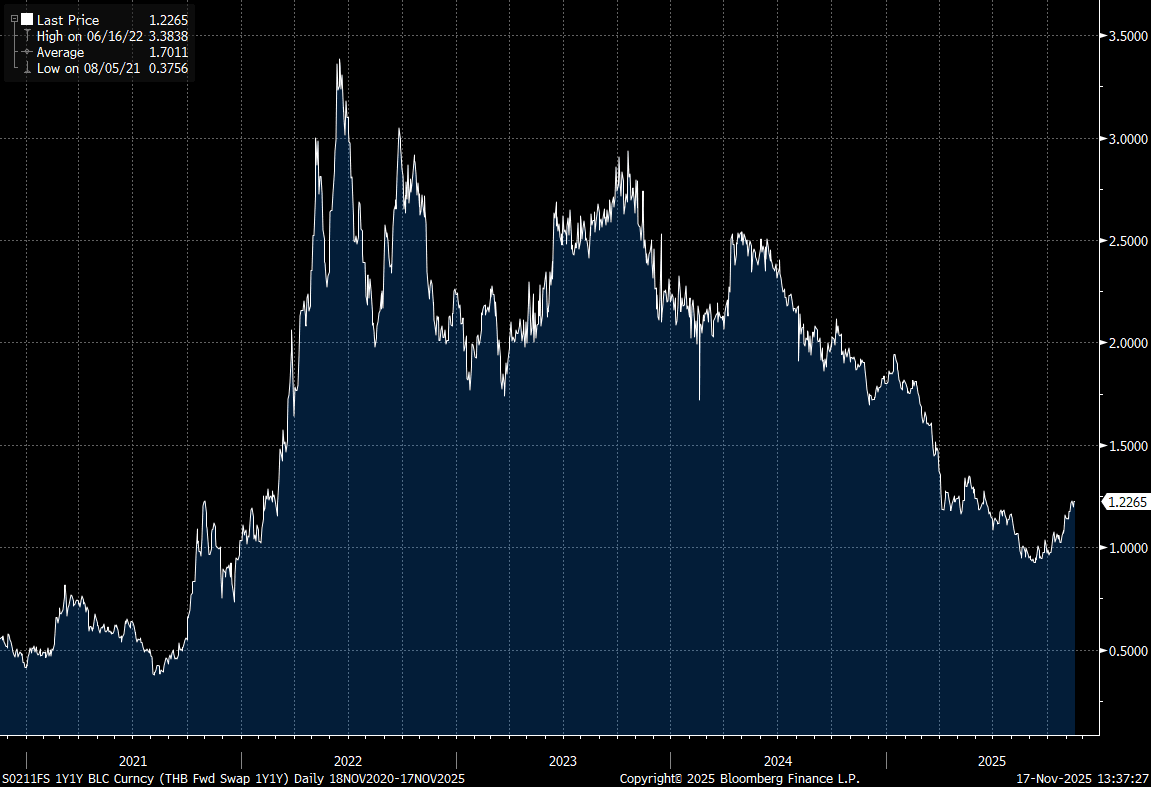

THAILAND: Q3 GDP Sub Expectations, Will This Help Slow The Rise In Local Rates?

Thailand Q3 GDP was weaker than forecast, falling -0.6%q/q, versus the market consensus of a -0.3% drop. This was the first fall in quarterly GDP since the end of 2022. Y/Y growth was 1.2% (against a 1.6% forecast and 2.8% prior). This is the weakest growth pace in y/y terms since the end of 2021. The planning agency notes that growth in y/y terms for Q4 may be around 0.6%y/y. Full growth for this year is expected at around 2%, while the 2026 projection is 1.2-2.2%.

- Such a backdrop is likely to keep the BoT with an easing bias, while the government will hope its recent stimulus efforts gain traction. The planning agency noted that Q4 GDP in q/q terms may not be a contraction. Inflation is expected to remain benign into 2026 (0% to 1%).

- The Thailand NDRIS 1y1y rate sits near +1.23%, around multi month highs. Early Sep lows were close to 0.93%. The current policy rate is at 1.50% and as noted above the bias is likely to be further easing over the coming 6 months rather than a shift to tighten policy settings.

- USD/THB is little changed, last near 32.43, up from recent lows in the 32.30/35 region, but moves above 32.50 have drawn selling interest of late.

- The detail on today's print showed private consumption down lightly in q/q terms, but still up 2.6%y/y (unchanged from Q3). Government consumption fell 3.9% y/y (from 2.2% in Q2). Investment growth slowed to 1.1% from 5.8%y/y prior. Exports were softer, up 6.9% from 11.2%y/y prior, with services exports slowing to -10.7% from -2.6% prior, as tourism slowing started to impact.

Fig 1: Thailand NDIRS 1y1y

Source: Bloomberg Finance L.P/MNI

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 17/11/2025 | 0800/0900 | Flash GDP | ||

| 17/11/2025 | 0815/0915 | ECB de Guindos Speech at Euro Finance Week | ||

| 17/11/2025 | 0900/1000 | ** | Italy Final HICP | |

| 17/11/2025 | 1000/0500 | * | CREA Existing Home Sales | |

| 17/11/2025 | 1315/0815 | ** | CMHC Housing Starts | |

| 17/11/2025 | 1320/1320 | BOE Mann on DMP and MonPol | ||

| 17/11/2025 | 1330/0830 | * | International Canadian Transaction in Securities | |

| 17/11/2025 | 1330/0830 | *** | CPI | |

| 17/11/2025 | 1330/0830 | ** | Empire State Manufacturing Survey | |

| 17/11/2025 | 1400/0900 | New York Fed's John Williams | ||

| 17/11/2025 | 1430/0930 | Fed Vice Chair Philip Jefferson | ||

| 17/11/2025 | 1445/1545 | ECB Lane Lecture on ECB MonPol | ||

| 17/11/2025 | 1500/1000 | * | Construction Spending | |

| 17/11/2025 | 1500/1000 | * | Construction Spending | |

| 17/11/2025 | 1600/1700 | ECB Cipollone at ECON Digital Euro Hearing | ||

| 17/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 17/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/11/2025 | 1800/1300 | Minneapolis Fed's Neel Kashkari | ||

| 17/11/2025 | 2035/1535 | Fed Governor Christopher Waller | ||

| 18/11/2025 | 1000/1100 | ECB Elderson at Banking Supervision Press Conference | ||

| 18/11/2025 | 1300/1300 | BOE Pill Fireside Chat on MonPol | ||

| 18/11/2025 | 1330/0830 | ** | Import/Export Price Index | |

| 18/11/2025 | 1355/0855 | ** | Redbook Retail Sales Index |