MNI EUROPEAN MARKETS ANALYSIS: FOMC Seen On Hold

- Risk sentiment was supported on early headlines of US-China trade talks scheduled in Switzerland for later this week. This was followed by PBoC easing steps (lower rates and a RRR cut). Equity markets are away from best levels though.

- US yields edged higher, while the USD has mostly risen against the majors. In NZ, there were some tentative signs in the Q1 labour market data that there is some stabilisation but at weak levels.

- Later the focus will be on the Fed decision, which is widely expected to leave policy unchanged. March German factory orders and euro area retail sales print.

MARKETS

US TSYS: Asia Wrap - Yields Edge Higher

TYM5 has traded lower within a range of 111-04 to 111-11 during the Asia-Pacific session. It last changed hands at 111-10, unchanged from the previous close.

- The US 10-year yield is a little higher, dealing around 4.31%, up 0.02 from its close.

- The US 2-year yield is a little higher, dealing around 3.80%, up 0.02 from its close.

- The People's Bank of China, announced today a cut to the seven-day reverse repurchase rate to 1.4% from 1.5%.

- The PBOC also announced a reduction in the amount banks must own in reserve (known as the RRR) by 0.5% which is expected to see CNY1tn of long term capital released into the market.

- The PBOC also announced two new funding schemes of up to CNY800bn to support the stock market. These announcements aim to stabilize markets and expected to lower borrowing costs for those looking to invest in the stock market.

- Treasuries opened lower on the news of the US-China meeting but has since clawed back those losses during the session as the market awaits the FOMC later.

- The 10-year Yield range seems to be 4.10% - 4.45%, price has moved back to the 4.30% pivot and with more supply to come this week a good chance this level holds. Focus will be on the FOMC tonight and Powell's statement.

- Data/Events : US FOMC

JGBS: Bear-Steepener, BoJ Minutes (Mar) & 10Y Supply Tomorrow

JGB futures are weaker, -27 compared to settlement levels, as trading resumed after the extended long weekend.

- Outside of the previously outlined Jibun Bank PMIs, there hasn't been much by way of domestic drivers to flag.

- Cash US tsys have twist-flattened, pivoting at the 20-year, with benchmark yields 2bps higher to 1bp lower.

- The FOMC today will be watched closely, MNI Economist - "The FOMC will extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement. As the FOMC awaits clarity in both government policy and the data on the degree to which one if not both dual mandate targets will be missed, most participants will continue to support a holding pattern until there is a clearer signal to act."

- The cash JGB curve has bear-steepened, with yields flat to 8bps higher. The benchmark 10-year yield is 2.8bps higher at 1.292% versus the cycle high of 1.596%.

- Swaps are flat to 3bps higher, with swap spreads tighter.

- Tomorrow, the local calendar will see BoJ Minutes of March Meeting and Tokyo Avg Office Vacancies data alongside 10-year supply.

AUSSIE BONDS: Richer Ahead Of FOMC Decision

ACGBs (YM +6.0 & XM +6.5) are stronger and near Sydney session bests on a local data-light session. The local calendar will be empty for the rest of the week.

- Cash US tsys have twist-flattened, pivoting at the 20-year, with benchmark yields 2bps higher to 1bp lower.

- The FOMC today will be watched closely, MNI Economist - "The FOMC will extend its series of rate holds to a third meeting in May, keeping the Fed funds target rate at 4.25-4.50% while maintaining its forward guidance in the Statement. As the FOMC awaits clarity in both government policy and the data on the degree to which one if not both dual mandate targets will be missed, most participants will continue to support a holding pattern until there is a clearer signal to act."

- Cash ACGBs are 6-7bps richer with the AU-US 10-year yield differential at -4bps.

- The bills strip has bull-flattened, with pricing flat to +8.

- RBA-dated OIS pricing is flat to 7bps softer across meetings today, with mid-2026 leading. A 50bp rate cut in May is given a 4% probability, with a cumulative 107bps of easing priced by year-end.

- The AOFM plans to sell A$700mn of the 2.75% 21 November 2029 bond on Friday.

BONDS: Bull-Steepener, UE Unchanged, RBNZ's FSR Published

NZGBs closed showing a bull-steepener, with benchmark yields 5-7bps lower, following today’s labour market data.

- However, with the NZ-US and NZ-AU 10-year yield differentials little changed on the day, the data's impact appears to have been limited.

- The Q1 labour market data shows some stabilisation, but at weak levels.

- While the unemployment rate was stable at 5.1%, better than the consensus, it appears that the rise in labour supply that was expected didn’t materialise. Thus, the data is close enough to what the RBNZ expected in February, and another 25bp rate cut on May 28 remains likely.

- The RBNZ warned that financial stability risks have risen over the past six months amid global uncertainties and said banks have enough buffers to cushion the economy should things get worse, according to its FSR report.

- Swap rates closed 4-5bps lower.

- RBNZ dated OIS pricing closed slightly softer across meetings. 26bps of easing is priced for May, with a cumulative 77bps by November 2025.

- Tomorrow, the local calendar will see the NZ Government's 9-Month Financial Statements.

- Tomorrow, the NZ Treasury plans to sell NZ$225mn of the 3.00% Apr-29 bond, NZ$175mn of the 4.25% May-36 bond and NZ$50mn of the 2.75% May-51 bond.

NEW ZEALAND: Labour Market Still Weak But Could Be Stabilising

There were some tentative signs in the Q1 labour market data that there is some stabilisation but at weak levels. There was a 0.1% q/q rise in employment driven by a 2.2% q/q jump in part-timers, indicating a cautionary move back into hiring. While the unemployment rate was stable at 5.1%, better than consensus, it appears that the rise in labour supply that was expected didn’t materialise. Thus the data is close enough to what the RBNZ expected in February and another 25bp rate cut on May 28 remains likely.

- Wage inflation slowed with the labour cost index rising 0.5% q/q, the slowest quarterly rate in four years, bringing the annual pace down to 2.9% from 3.3%, the lowest since Q4 2021. Private sector wages rose 0.4% q/q after 0.8% q/q in Q1 2024.

NZ wages y/y%

- The RBNZ should be reassured that wages have adjusted to the lower inflation environment and spare capacity in the labour market.

- While part-time employment rose, full-time fell 0.5% q/q to be down 1.9% y/y. This is also reflected in the 0.3%q/q & 2.9% y/y drop in hours worked and the 0.2pp pickup in the underutilisation rate to 12.3%. While the labour market may have reached a turning point, both of these series show that it remains weak.

- The number of unemployed was flat in Q1 but still up 16.4% y/y, but this was the lowest quarterly change since Q2 2022. The number of people who say there isn’t enough work available rose 26.3% y/y, according to Statistics NZ.

NZ employment y/y%

STIR: RBNZ Dated OIS Pricing Little Changed After Q1 Employment Report

RBNZ dated OIS pricing is flat to 3bps softer across meetings after the release of the Q1 Employment Report.

- There were some tentative signs in the Q1 labour market data that there is some stabilisation, but at weak levels. There was a 0.1% q/q rise in employment driven by a 2.2% q/q jump in part-timers, indicating a cautionary move back into hiring.

- While the unemployment rate was stable at 5.1%, better than consensus, it appears that the rise in labour supply that was expected didn’t materialise. Thus, the data is close enough to what the RBNZ expected in February, and another 25bp rate cut on May 28 remains likely.

- 26bps of easing is priced for May, with a cumulative 77bps by November 2025.

Figure 1: RBNZ Dated OIS Latest vs. Pre-Jobs Levels (%)

Source: MNI - Market News / Bloomberg

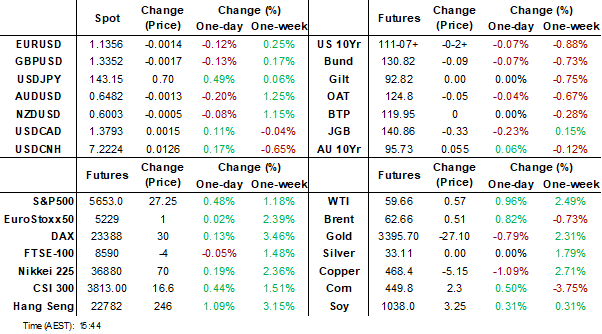

FOREX: USD Struggling To Bounce

The BBDXY has had an Asian range of 1217.76 - 1220.50, Asia is currently trading around 1219. The USD continues to be sold on any rallies, Asia has seen a small bounce on the news of a US-China meeting to be held in Switzerland. MNI - The People's Bank of China, announced today a cut to the seven-day reverse repurchase rate to 1.4% from 1.5%. The PBOC also announced a reduction in the amount banks must own in reserve (known as the RRR) by 0.5% which is expected to see CNY1tn of long term capital released into the market. The market's focus will turn to the FOMC later today.

- EUR/USD - Asian range 1.1326 - 1.1375, Asia is currently trading 1.1350. Intra-day support is around the 1.1250 area, should this area not hold demand should remerge on dips back to 1.1100.

- GBP/USD - Asian range 1.3333 - 1.3382, Asia is currently dealing around 1.3350. Intra-day support is around the 1.3250 area, then the pivotal 1.30/31 support is next.

- USD/JPY - Asian range 142.45 - 143.31, has held most of its early gains in the Asia session. Can the FOMC be the catalyst to test the 140.00 area again ?

- USD/CNH - Asian range 7.1892 - 7.2265, the USD/CNY fix printed 7.2005. The PBOC cut has seen USD/CNH bounce from below 7.2000, currently trading 7.2215. Sellers should return back towards 7.2500.

- Cross asset : SPX +0.68%, Gold $3385, US 10-Year 4.31%, BBDXY 1219, Crude oil $59.64.

- Data/Events : SW CPI, Ger Factory orders, IT Retail sales, US FOMC

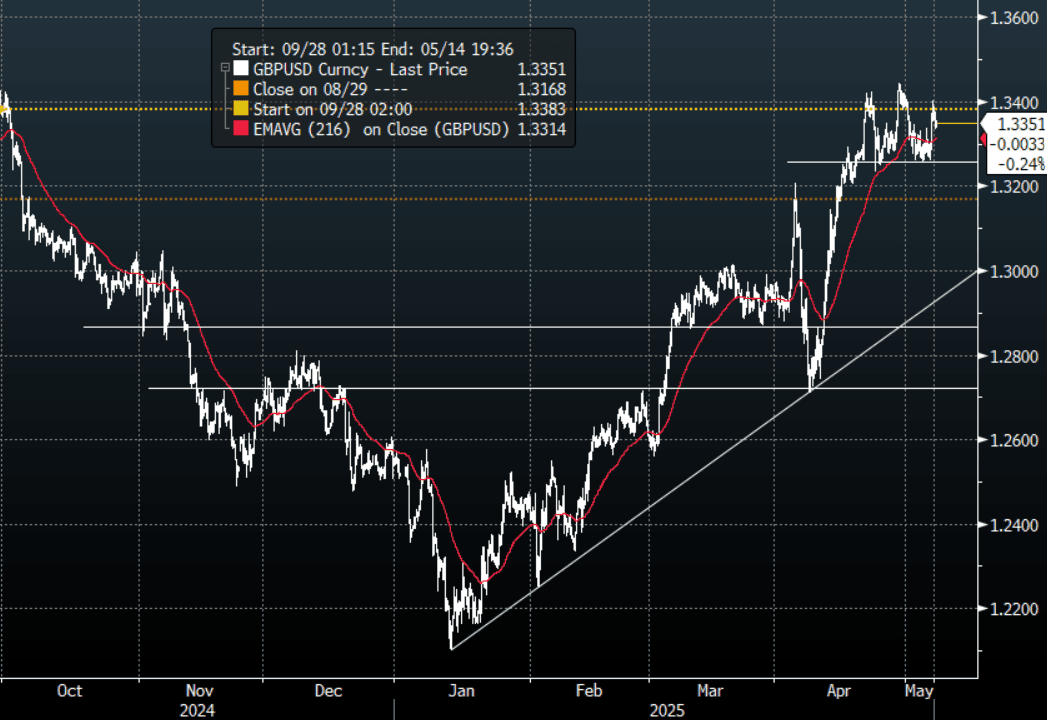

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

FOREX: Antipodean Wrap - AUD & NZD Give Back Early Gains

The Asian session started off on the front foot with US stocks bouncing on news that Scott Bessent and Jamieson Greer will hold trade talks with He Lifeng in Switzerland this week. Both the AUD and NZD have both given back their early gains over the Asian session to end smalls lower on the day. MNI Economist - NZ Labour : “There were some tentative signs in the Q1 labour market data that there is some stabilisation but at weak levels. While the unemployment rate was stable at 5.1%, better than consensus, it appears that the rise in labour supply that was expected didn’t materialise. Thus the data is close enough to what the RBNZ expected in February and another 25bp rate cut on May 28 remains likely.”

- AUD/USD - Asian range 0.6478 - 0.6515, the AUD is currently dealing around 0.6485. Support should be seen back towards 0.6350/6400, a break below 0.6300 needed to reverse direction.

- AUD/JPY - Asian range 92.45 - 93.33, price goes into London trading around 92.80. Price continues to stall back towards the resistance seen around 94.00. Support seen back towards the 91.50/92.00 area.

- NZDUSD - Asian range 0.5989 - 0.6023, going into London trading around 0.5995. The NZD continues to hold up well, given the NZD seems to find bids in all scenarios for risk at the moment watch for this to gain momentum.

- AUD/NZD - Asian range 1.0800 - 1.0832, the Asian session is currently trading 1.0805. Sellers have returned back towards the 1.0850 area.

Fig 1 : AUD/USD Spot Daily Chart

Source: MNI - Market News/Bloomberg

ASIA STOCKS: Equities Bounce on PBOC Measures.

China began its economic support today with a range of various measures announced to support the economy, especially in the face of 145% tariffs from the US. The key PBOC announcement being a 0.10% in the interbank funding rate and a 0.50% reduction in the RRR. In September the concept of the "national team" was created which effectively is key asset management companies through which support for equity markets will occur. Today sees the addition of two more entities being China Chengtong Holdings, China Reform Holdings and Central Huijin Investment Ltd. The PBOC also announced two new funding schemes of up to CNY800bn to support the stock market also.

- Markets liked the news with the Hang Seng up +0.49%, CSI 300 +0.48%, Shanghai up +0.65% and Shenzhen up +0.47%.

- In the first day back post holidays, the KOSPI is up also by +0.33%.

- In Malaysia the FTSE Malay KLCI is up +0.42% whilst the Jakarta Composite continues its good run rising +0.90%.

- Singapore’s FTSE Straits Times is higher by just +0.07% and the PSEi in the Philippines is up +1.43% on improving local data.

- As news of the escalation of action between India and Pakistan filters through the market reaction in India has been somewhat muted. The NIFTY 50 is lower by -0.30%, having fallen -0.33% yesterday.

OIL: Crude Rises Further As US-China Talks Follow Less Expected US Output

Oil prices continued rallying today after rising sharply on Tuesday following the EIA’s downward revision to its expectations for US shale production this year because of lower prices. Today’s increase in crude has been driven by news that US-China trade talks will occur this week with US Treasury Secretary Bessent and Trade Representative Greer meeting China’s Vice Premier Lifeng in Switzerland on the weekend. This has helped boost the US dollar (USD BBDXY index +0.3%).

- WTI is up 1.1% to $59.73, close to the intraday high, while Brent is 0.9% higher at $62.72. Both are currently around 2.4% higher this week. Benchmarks declined sharply over recent weeks on concerns that increased protectionism and current uncertainty would weigh on global energy demand.

- Bessent noted that current tariff levels are “unsustainable” and that de-escalation with China needs to occur before they “can move forward”.

- Meanwhile, China announced further stimulus and measures to support property & equities today. The PBoC cut the SLF rates used for financial institutions’ short-term funding, the 7-day reverse repo and reserve requirements. China is the world’s largest oil importer.

- Official EIA data are published later and with the EIA downward revision to US production and the industry-reported 4.49mn barrels stock drawdown last week, it is likely to continue to be monitored closely. Signs of a reduction in demand due to current uncertainty will also be considered.

- Later the focus will be on the Fed decision, which is widely expected to leave policy unchanged. March German factory orders and euro area retail sales print.

Gold Lower Again as Equities Strong

- As the PBOC announced stimulus measures today, equities got a boost and gold fell.

- Gold is down -1.3% in the Asia trading day at US$3,384.54, having opened at $3,431.60.

- The PBOC announced a range of measures with the key being a 0.10% in the interbank funding rate and a 0.50% reduction in the RRR.

- This comes after US President Trump suggested that China is eager to negotiate due to its 'struggling' economy but emphasized the talks would take place at the right time.

- Another Central Bank reported overnight that their gold reserves are on the increase with the Central Bank of Ghana's gold reserves up by 31 tonnes in March.

- As gold does not pay interest it can be highly sensitive to interest rates as that dictates the borrowing cost to buy gold. Gold markets will watch carefully tonight as the push pull on rates continues with the White House demanding a rate cut and the FED talking more neutra

CHINA: Stimulatory Measures Announced by PBOC

- Markets have agonized for some time as to when there would be new measures announced by authorities to support the Chinese economy in a bid to ensure the 5% GDP growth target is achievable in the face of 145% tariffs from the US.

- The Central Bank, the People’s Bank of China, announced today a cut to the seven-day reverse repurchase rate to 1.4% from 1.5%. The reverse repo is the preferred measure for managing interbank liquidity by the PBOC. The PBOC conducts daily operations known as open market operations. The change will come into effect from tomorrow.

- The PBOC also announced a reduction in the amount banks must own in reserve (known as the RRR) by 0.5% which is expected to see CNY1tn of long term capital released into the market.

- The PBOC will set up a CNY500bn relending tool for consumption and elderly care with more details to follow.

- The PBOC will increase its relending fund for technology companies by CNY300bn to support innovation.

- The PBOC will increase its relending fund by CNY300bn for agriculture to support the sector.

- The measures could see upward pressure on yields as banks tend to put excess liquidity held for reserves into the bond market. The PBOC had halted a bond buying program earlier this year as yields ratcheted lower and any upward movement in yields could see that the program restarted.

- The regional governments and central governments have enormous issuance requirements this year. The first test post this announcement will come on Friday when the central government issues CNY71bn of 2055 and CNY170bn of 2026 bonds

- The CGB market and bond futures have reacted very little to the news with CGB 10yr unchanged at 1.62% and bond futures marginally higher. The news of the RRR cut is not a sell order for banks so no mass liquidation of bonds is expected. However over time it is likely to see selling pressure on yields, something the PBOC will likely seek to manage.

CHINA: Further Measures Announced to Support Real Estate Sector

- Amongst the raft of new initiatives announced today, a cut in the loan rates for the individual housing provident fund by 0.25bps was announced.

- This directly impacts home loans that have a maturity of greater than 5 years with the PBOC governor suggesting it will save borrowers up to CNY20bn of interest annually.

- China has been in the grips of a multi year downturn for the property sector with recent data showing that used home prices have contracted every month since July 2021.

- The housing provident fund is a long-term housing savings plan made up of compulsory monthly deposits by both employers and employees. It can only be used by employees for house-related expenses.

CHINA: Standard Lending Facility Rates Cut

- PBOC will cut standing lending facility rates starting from May 8, according to a statement.

- The Standing Lending Facility (SLF) is a monetary policy tool used by the People's Bank of China (PBOC) to provide liquidity to financial institutions. Typically financial institutions use the facility to borrow short-term funding, using bonds to collateralize the loan.

- Overnight standing lending facility will be cut to 2.25% from 2.35%

- Cut 7-day SLF rate to 2.4% from 2.5%

- Cut 1-month SLF rate to 2.75% from 2.85%

- This is an additional measure that not only will free up liquidity (and capital) but could result in bond market selling over time and has the potential to put upward pressure on yields.

CHINA: Measures Announced to Support Stocks

- In September the concept of the “national team” was created which effectively is key asset management companies through which support for equity markets will occur. Today sees the addition of two more entities being China Chengtong Holdings, China Reform Holdings and Central Huijin Investment Ltd.

- The PBOC also announced two new funding schemes of up to CNY800bn to support the stock market.

- These announcements aim to stabilize markets and expected to lower borrowing costs for those looking to invest in the stock market.

- The funding schemes will have lower interest rates than those on offer previously.

- The PBOC noted of their intention to support insurance companies in their investing in stock markets also

- The PBOC announced further support for Central Huijin Investment Ltd (a state owned investment company) to allow it to increase its index holdings in the stock market.

MNI BNM Preview - May 2025: On Hold for Now.

Download Full Report Here:

We see the BNM on hold for now given:

- The implications of tariffs from the US remains unclear.

- Inflation has softened further, yet upside risks are present given the trade war.

- Domestic consumption remains robust and the recent delay in the GST hike is supportive of the consumer.

UP TODAY (TIMES GMT/LOCAL)

| Date | GMT/Local | Impact | Country | Event |

| 07/05/2025 | 0600/0800 | ** | Manufacturing Orders | |

| 07/05/2025 | 0600/0800 | *** | Flash Inflation Report | |

| 07/05/2025 | 0645/0845 | * | Foreign Trade | |

| 07/05/2025 | 0730/0930 | ** | S&P Global Final Eurozone Construction PMI | |

| 07/05/2025 | 0800/1000 | * | Retail Sales | |

| 07/05/2025 | 0830/0930 | ** | S&P Global/CIPS Construction PMI | |

| 07/05/2025 | 0900/1100 | ** | Retail Sales | |

| 07/05/2025 | 0900/1000 | ** | Gilt Outright Auction Result | |

| 07/05/2025 | 1100/0700 | ** | MBA Weekly Applications Index | |

| 07/05/2025 | 1400/1000 | Treasury Secretary Scott Bessent | ||

| 07/05/2025 | 1430/1030 | ** | DOE Weekly Crude Oil Stocks | |

| 07/05/2025 | 1800/1400 | *** | FOMC Statement | |

| 07/05/2025 | 1900/1500 | * | Consumer Credit | |

| 08/05/2025 | - | NorgesBank Meeting | ||

| 08/05/2025 | 0600/0800 | ** | Trade Balance | |

| 08/05/2025 | 0600/0800 | ** | Industrial Production | |

| 08/05/2025 | 0700/0900 | ** | Industrial Production | |

| 08/05/2025 | 0730/0930 | *** | Riksbank Interest Rate Decison | |

| 08/05/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1102/1202 | *** | Bank Of England Interest Rate | |

| 08/05/2025 | 1130/1230 | BOE Press Conference | ||

| 08/05/2025 | 1230/0830 | *** | Jobless Claims | |

| 08/05/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 08/05/2025 | 1230/0830 | ** | Preliminary Non-Farm Productivity | |

| 08/05/2025 | 1300/1400 | Decision Maker Panel data |