FOREX: USD Struggling To Bounce

The BBDXY has had an Asian range of 1217.76 - 1220.50, Asia is currently trading around 1219. The USD continues to be sold on any rallies, Asia has seen a small bounce on the news of a US-China meeting to be held in Switzerland. MNI - The People's Bank of China, announced today a cut to the seven-day reverse repurchase rate to 1.4% from 1.5%. The PBOC also announced a reduction in the amount banks must own in reserve (known as the RRR) by 0.5% which is expected to see CNY1tn of long term capital released into the market. The market's focus will turn to the FOMC later today.

- EUR/USD - Asian range 1.1326 - 1.1375, Asia is currently trading 1.1350. Intra-day support is around the 1.1250 area, should this area not hold demand should remerge on dips back to 1.1100.

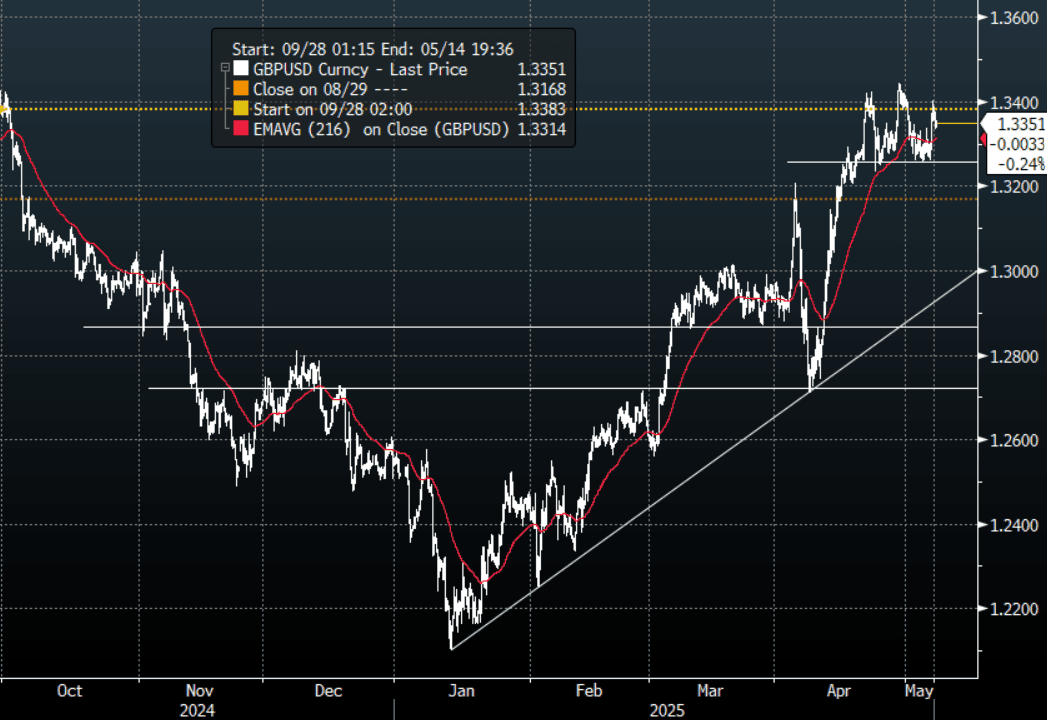

- GBP/USD - Asian range 1.3333 - 1.3382, Asia is currently dealing around 1.3350. Intra-day support is around the 1.3250 area, then the pivotal 1.30/31 support is next.

- USD/JPY - Asian range 142.45 - 143.31, has held most of its early gains in the Asia session. Can the FOMC be the catalyst to test the 140.00 area again ?

- USD/CNH - Asian range 7.1892 - 7.2265, the USD/CNY fix printed 7.2005. The PBOC cut has seen USD/CNH bounce from below 7.2000, currently trading 7.2215. Sellers should return back towards 7.2500.

- Cross asset : SPX +0.68%, Gold $3385, US 10-Year 4.31%, BBDXY 1219, Crude oil $59.64.

- Data/Events : SW CPI, Ger Factory orders, IT Retail sales, US FOMC

Fig 1: GBP/USD Spot Hourly Chart

Source: MNI - Market News/Bloomberg

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Futures Holding Sharply Higher At Lunch But Off Bests

At the Tokyo lunch break, JGB futures remain sharply higher at 142.19, +53 compared to settlement levels, but well off session bests (142.95).

- “Details in Japan’s February labor cash earnings contained bad news for the Bank of Japan — the pace of increase in base pay for full-time workers on a same-sample basis — the central bank’s preferred gauge — slowed sharply and undershot the consensus forecast.” (per BBG Economics)

- The local calendar will also see Coincident & Leading Indices data later.

- Markets continue to be hit by the ongoing trade-related pullback in risk appetite, although some have begun to stabilise at lower levels due to selling fatigue and profit-taking, including risk-sensitive AUD and oil prices. US equity futures are down sharply but also off their intraday lows.

- Some Asian countries have said today that they will take steps to stabilise markets if needed and Japan has said it will speak with the US.

- Nevertheless, the market are continuing to digest the implications Friday’s unveiling of a 34% duty on all US imports by China.

- Cash JGBs are flat to 11bps richer across benchmarks out to the 30-year (40-year flat), with the belly leading. The benchmark 10-year yield is 9.7bps lower at 1.120% versus the cycle high of 1.596%.

- Swap rates are 6-11bps lower. Swap spreads are mixed.

CHINA: Bond Futures Strong at Open.

- China’s bond futures are rallying hard at the open with the 10YR leading.

- The 10YR future is up +0.50 to 109.08, breaking through a key technical level of 109.00in this morning’s trading.

- The 2YR future is up +0.09 to 102.64, this morning's trading seeing the 2YR trade through the 100-day EMA of 102.60.

- Cash moves has been significant with the 10YR lower by -8bps to 1.63%, a big drop since the high of 1.89% on March 17.

AUSSIE BONDS: Richer But Well Off Bests As Risk-Off Pared

ACGBs (YM +10.0 & XM +7.0) are richer but well below today's Asia-Pac session bests.

- Markets continue to be hit by the ongoing trade-related pullback in risk appetite, although some have begun to stabilise at lower levels due to selling fatigue and profit-taking, including risk-sensitive AUD and oil prices.

- US equity futures are down sharply but also off their intraday lows.

- Some Asian countries have said today that they will take steps to stabilise markets if needed and Japan has said it will speak with the US.

- US tsy futures (TYM5) are dealing sharply higher at 113-19, +17 from closing levels, albeit well off the early high of 114-10. Cash US tsys are 3-13bps richer in today’s Asia-Pac session.

- Cash ACGBs are 5-7bps richer with the AU-US 10-year yield differential at +24bps.

- Bill strip pricing is +7 to +11, with whites leading.

- RBA-dated OIS pricing gives a 50bp rate cut in May a 50% probability, with a cumulative 117bps of easing priced by year-end (based on an effective cash rate of 4.09%).

- Earlier in the session, a 50bp rate cut in May was given an 80% probability, with a cumulative 133bps of easing priced by year-end.